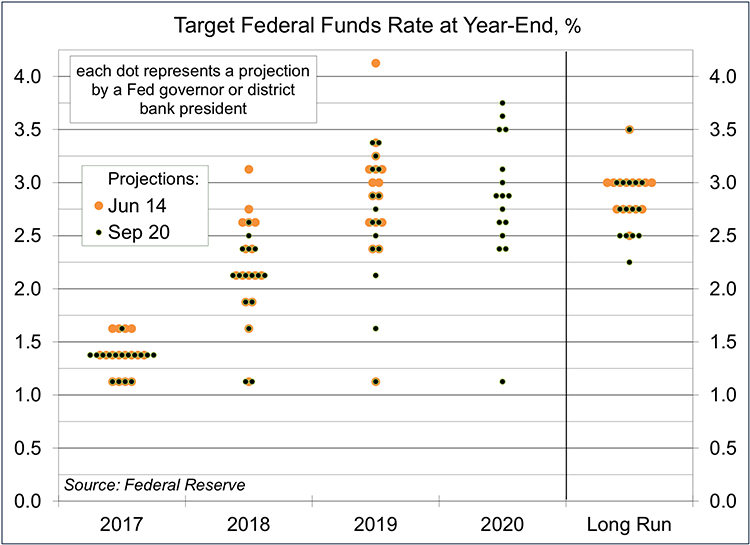

As expected, the Federal Open Market Committee left the federal funds target range unchanged (at 1.00-1.25%) after its September 19-20 policy meeting. The FOMC also announced the beginning of balance sheet reduction. The Fed had outlined how this would work in mid-June, and officials did a good job of telegraphing when it would start. Investors were more surprised by the dot plot, which continued to show a majority of Fed officials anticipating one more rate hike by the end of the year.

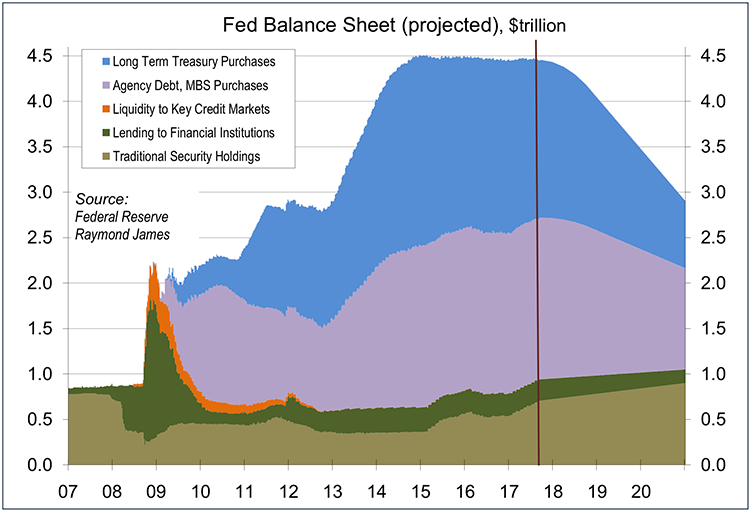

The Fed’s three large-scale asset purchase programs (quantitative easing, or “QE”) added $3.4 trillion to the Fed’s balance sheet. The Fed is not planning on selling these securities. It will continue to reinvest maturing securities, but will allow a certain amount to run-off each month. The cap on the monthly run-off starts slow ($10 billion), but increases every three months, reaching full stride ($50 billion) in October 2018.

In her post-FOMC press conference, Chair Janet Yellen said that the Fed does not plan on making adjustments to the balance sheet normalization program. The run-off is not “active” policy. The Fed will still rely on the federal funds target rate as “the primary means of adjusting the stance of monetary policy.” Still, the Fed could stop the program, or even purchase more securities if the economy were to experience a large negative shock (the federal funds rate would have to be dropped toward zero first). The Fed likely feared some adverse market reaction to balance sheet reduction, as we saw a few years ago with the taper tantrum. However, the Fed has signaled its plans well in advance and will start slow.

What does this mean for investors? Again, balance sheet reduction was well advertised. There’s nothing surprising in the announcement. All else equal, balance sheet reduction should mean a gradual increase in long-term interest rates, but there are a lot of factors driving bond yields (including inflation expectations and bond yields outside the U.S.). QE lowered the 10-year Treasury note yield by 50-100 basis points, so the unwinding would likely push yields up accordingly (all else equal). However, the size of the balance sheet is unlikely to fall back to where it was before the Fed’s asset purchases. The Fed will continue the run-off until the size of the balance sheet is “appropriate,” but it’s unclear what that means.