“The message from a string of BIS [Bank of International Settlements] reports is that the US dollar

is both the barometer and agent of global risk appetite and credit leverage.

Episodes of dollar weakness – such as this year – flush the world with liquidity and

nourish asset booms. When the dollar strengthens, it becomes a headwind for stock markets and credit.”

– Ambrose Evans-Pritchard

The US Federal Reserve and fellow central banks can be forgiven for telling us a white lie: nothing would be gained from admitting that they do not know how to extricate the world safely from their extreme monetary experiment.

Fed chair Janet Yellen has finally pulled one major trigger after countless retreats. The long-awaited reversal of quantitative easing will kick off in October.

Deutsche Bank calls it the start of the ‘Great Central Bank Unwind,’ candidate ‘Number One’ for the world’s next financial crisis.

The puzzle is why the Yellen Fed – usually so cautious – has chosen to enter these treacherous waters when there is no strict need to do so and before it has raised interest rates to minimum safe levels. This tightening sequence makes no sense.

Source: Yellen Fed courts fate by reversing QE so soon

Ambrose Evans-Pritchard is the International Business Editor of The Telegraph. He has covered world politics and economics for 30 years. Follow him. He’s good.

Fed day has passed and consensus is that the Fed is hawkish (pulling the punch bowl from the party by raising rates and reducing its balance sheet of assets purchased during QE). Yields around the globe moved higher, the 10-year Treasury note is trading back above 2.25%, the dollar rallied and remains slightly higher than prior to the Fed announcement. Gold sold off on the news and is testing its recent upside breakout.

U.S. equities weathered the news with the broad markets mostly unchanged and financials (beneficiaries of higher rates) rallied. International developed and emerging markets are slightly lower.

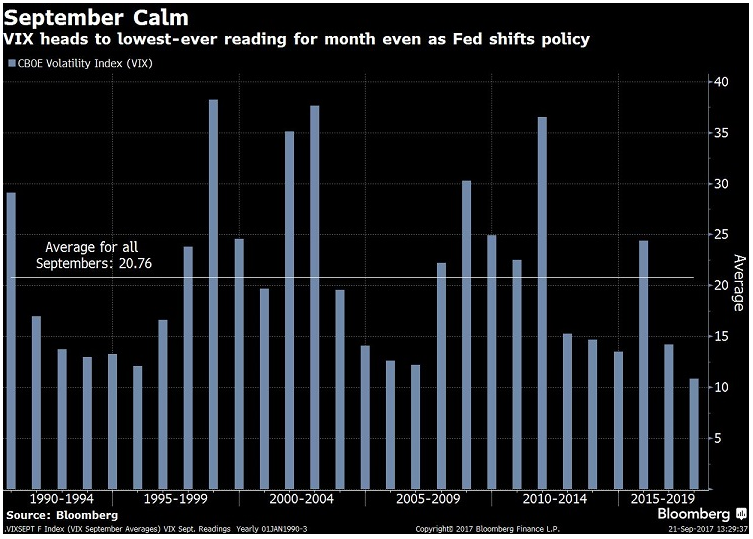

August and September are the two worst performing months for stocks each year. You wouldn’t know it from the relative calm in the market. From Bloomberg’s David Wilson, “This month’s pattern of calm for U.S. stocks persisted even after Federal Reserve officials laid out plans to begin selling some of the central bank’s bond holdings. The CBOE Volatility Index, or VIX, is headed for its lowest daily average in any September since calculations began in 1990. Wednesday’s 0.4-point decline in the VIX, to 9.78, as the Fed announced the monetary-policy shift.” The all-time low was in early 2007 at 9.39. Readings below 10 are rare.

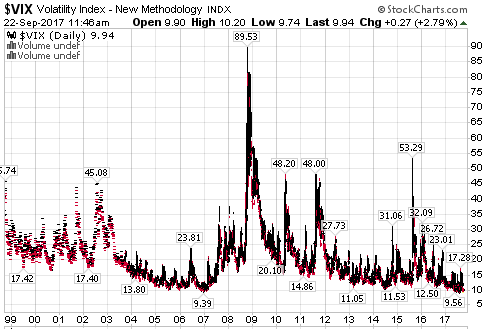

Here is a look at the VIX Volatility Index since 1999. Imagine the calm confidence that set over the market in 2007. VIX measures perceived risk. We should get worried when everyone is comfortable and see opportunity when others are in fear.

Where is the demand for equities coming from?

One strong answer is the central banks… With a nod toward “party on” the Bank of Japan (BOJ) voted to keep its current easy monetary policy unchanged by a vote of 8-1 (with the lone dissenter arguing for more aggressive easing). BOJ Governor Haruhiko Kuroda said that ETF purchases are still necessary to achieve the 2% inflation target by reducing equity risk premium. Print and buy… no concern of price or return… “Still necessary to achieve inflation…” One has to ask/wonder what the other side of this might look like. But when? For now, no “other side,” at least in Japan, is in sight. Their markets rallied on the Fed news.

I had a conversation with David Bianco of Deutsche Asset Management in early August at Camp Kotok in Maine. He made a strong argument that we really should be keeping our eyes on the European Central Bank. It is that liquidity that is finding its way into global equity markets, including the U.S. Perhaps he is on to something.

Here’s what I mean…. When Draghi’s European Central Bank (ECB) creates money and buys bonds, the seller of those bonds is flush with new cash and needs to next decide what to buy. That money finds its way to something and I contend it is bidding up stock prices.

Bank of America’s Michael Hartnett is saying the same thing. He noted in a recent post that the Fed is not the world’s sole central bank. We have to consider the liquidity created by the ECB, the BOJ, the Bank of England (BOE) and the People’s Bank of China (PBOC). Hartnett notes that central banks have purchased nearly $2 trillion of financial assets year to date.

That is almost as much as the Fed purchased under QE1 during the crisis period in the early innings of the “Great Recession.” Today, there is clearly no sign of even a mild recession, yet the love keeps on coming.

Bottom line: Those foreign central bank purchases translate to a vast sea of liquidity supporting stocks. Hartnett calls it the “supernova of liquidity” and “the flow that conquers all.” My motivation and title for today’s piece.

Stocks are hitting new all-time highs in both the U.S. and globally, seemingly absent any concern about the gap in fundamentals, the age of the business cycle or the geopolitical risks that seem to be sitting on a knife’s edge.

And I think it’s gonna be a long long time

‘Till touch down brings me round again to find

I’m not the man they think I am at home

Oh no no no I’m a rocket man

Rocket man burning out his fuse up here alone

– Elton John, “Rocket Man”

Yet more buyers than sellers is what it is and, at the end of the day, it is what moves prices. Our trend models remain bullish on equities, our tactical models are long risk assets and our fixed income trend signals still bullish.

I’ve long posted a Don’t Fight the Fed and Tape (Trend) chart in Trade Signals and it’s remained bullish despite the Fed hikes since December 2015. But we should be mindful of the liquidity coming from other central banks because that capital does find its way here.

To that end, the BOJ remains all in, game on, the Bank of England just completed its QE program in the spring. The ECB has indicated it will begin to taper and the Fed begins its tapering journey next month.

Look, my view is that the significant risk we face is a coming “Sovereign Debt Crisis.” The seminal issue is we sit at the end-stage of a long-term debt super cycle and a reset is likely. Europe is a possible ground zero due to the size of debt, lack of common debt and challenged political union from north to south. China is a possible ground zero, as are the emerging markets you’ll find listed below in the body of OMR.

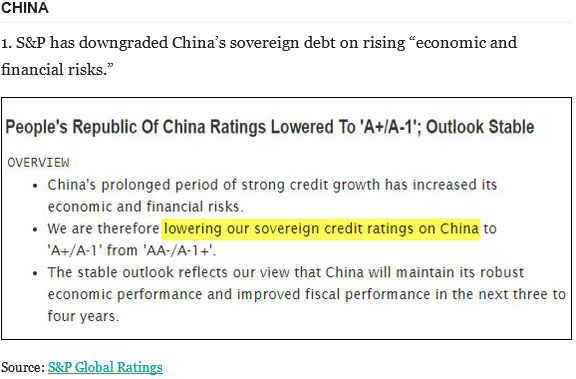

And just to make it a little more interesting, S&P downgraded China’s sovereign debt citing rising “economic and financial risks.”

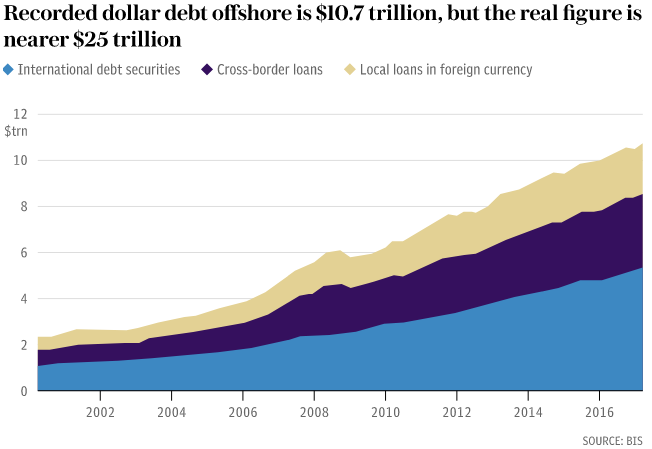

But wait, there’s more: According the to the Bank of International Settlements (BIS), what was believed to be $10 trillion or so in EM U.S. dollar denominated debt turns out to be nearly $25 trillion. Seems someone was creatively hiding $14 trillion off-balance sheet. Shades of Enron comes to mind.

We live in a complex global interconnected system. Because of the massive size of global debt (approximately 327% of global GDP), I believe it will be a rising dollar that trips the switch. Perhaps something else. When? No one can possibly know. A lot depends on fiscal policy, global policy coordination and central bank activity. Watch the dollar!

Let’s make sure to play both good offense and good defense. Participate and protect and get to the next great 2009-like investment opportunity in good shape.

Grab a coffee and read on. One more bump on my promise to deliver Barry Ritholtz’s great interview of Professor Richard Thaler. I hope it will be available on Monday. I’ll tweet out a link, share it on LinkedIn and include it in next week’s post. It’s really that good.

Below, I summarize and link to an excellent piece from the great Ambrose Evans-Pritchard. It is worth the read. You’ll love how he thinks/writes. Finally, I also share with you a few ideas on how you might manage your downside risk. Hope you find the information helpful and do have a great weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- BIS discovers $14 trillion of dollar debt offshore, hidden in “footnotes”

- Trend Following – Two Actionable Ideas

- Trade Signals – Inching Higher in Bull Market Trend – 09-20-2017

- Personal Note

BIS discovers $14 trillion of dollar debt offshore, hidden in ‘footnotes’

By Ambrose Evans-Pritchard, The Telegraph (September 17, 2017)

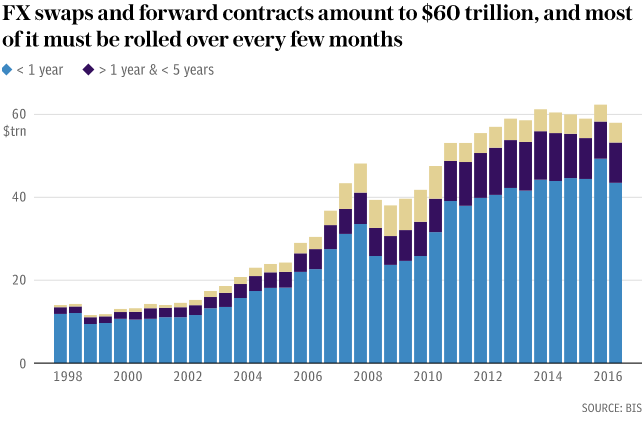

The world’s top financial watchdog has uncovered $14 trillion of global dollar debt hidden in derivatives and swap contracts, a startling sum that doubles the underlying levels of offshore dollar credit in the international system.

The scale of this lending greatly increases the risk of a future funding crisis if inflation ever forces the US Federal Reserve to tighten hard, draining worldwide liquidity and potentially triggering a dollar surge.

A forensic study by the Bank for International Settlements says enormous liabilities have accrued through FX swaps, currency swaps, and ‘forwards’. The data is tucked away in the “footnotes” of bank reports. “Contracts worth tens of trillions of dollars stand open and trillions change hands daily. Yet one cannot find these amounts on balance sheets. This debt is, in effect, missing,” said the BIS analysis, written by team under chief economist Claudio Borio.

“These transactions are functionally equivalent to borrowing and lending in the cash market. Yet the corresponding debt is not shown on the balance sheet and thus remains obscured,” they wrote in the BIS’s quarterly report.

A breath-taking gap in global accounting rules mean that the debt is booked as a notional derivative, “even though it is in effect a secured loan with principal to be repaid in full at maturity.”

The hidden lending comes on top of $10.7 trillion of recorded offshore dollar debt outside US jurisdiction. It pushes the combined total to $25 trillion or a third of global GDP. While these contracts serve as a lubricant and hedging device for world commerce, they can be plagued by currency and maturity mismatches.

The dollar swaps serve as a ‘money market’ for global finance. Investors often take out short-term contracts that must be rolled over every three months. The great majority have maturities of less than a year. Much of the money is used to make long-term investments in illiquid assets, the time-honoured cause of financial of financial blow-ups. “Even sound institutional investors may face difficulties. If they have trouble rolling over their hedges, they could be forced into fire sales,” said the Swiss-based watchdog.

While the BIS is careful to talk in broad terms, it is known that Chinese developers have borrowed heavily in US dollars through the FX swaps market. They do so because rates are lower and to dodge credit curbs. If funding suddenly dries up, Chinese regulators may be reluctant to bail them out for political reasons – until the situation is very serious.

“A defining question for the global economy is how vulnerable balance sheets may be to higher interest rates,” said Mr Borio, the High Priest of the global banking fraternity.

Signs of excess are visible everywhere. “Corporate debt is now considerably higher than it was pre-crisis. Leverage indicators have reached levels reminiscent of those that prevailed during previous corporate credit booms. A growing share of firms face interest expenses exceeding earnings before interest and taxes,” said the report.

The BIS warned that margin debt used on equity markets exceeds the dotcom extreme in 2000. So-called ‘leveraged loans’ have surged to a record $1 trillion, and the share with risky ‘covenant-lite’ terms have jumped to 75pc. Everything looks fine so long as low bond yields underpin the asset edifice, but they may not stay low. “Equity markets continue to be vulnerable to the risk of a snapback in bond markets,“ it said.

The structure is deeply unhealthy. Central bankers dare not lift rates despite economic recovery because of what they might detonate. “There is a certain circularity that points to the risk of a debt trap,” said Mr Borio.

The Achilles Heel is global dollar debt. It was a seizure of the offshore dollar capital markets in late 2008 that turned the Lehman and AIG bankruptcies into a global event, and came close to bringing down the European banking system. “The meltdown in dollar-denominated structured products caused funding markets to seize up and banks to scramble for dollars. Markets calmed only after coordinated central bank swap lines to supply dollars,” said the BIS.

The Fed effectively saved Europe from disaster. It is an open question whether the US Treasury would authorize such a rescue under the Trump Administration.

The Sword of Damocles still hangs precariously a decade later. Global dependence on dollar liquidity has since become even more extreme. Over 90pc of all FX swaps and forwards worldwide today are in US currency. The dollar is even used within Europe for most swaps involving the Polish zloty or the Swedish krona for example, a pattern that would probably astonish European politicians. “The dollar reigns supreme,” said the BIS.

What is odd is that Asian central banks and European multilateral bodies are huge players in this trade, effectively aiding and abetting a dangerous game.

The message from a string of BIS reports is that the US dollar is both the barometer and agent of global risk appetite and credit leverage. Episodes of dollar weakness – such as this year – flush the world with liquidity and nourish asset booms. When the dollar strengthens, it becomes a headwind for stock markets and credit.

If the dollar spikes violently, it sets off global tremors and a credit squeeze in emerging markets. This is what could happen again if President Trump’s tax reform plans lead to a big fiscal expansion and a repatriation of trillions of US corporate cash held overseas.

Currency analysts say it would be an emerging market bloodbath. While the ‘fragile five’ – India, South Africa, Indonesia, Turkey, Brazil – have mostly cut their current account deficits and are in better shape than during the ‘taper tantrum’ of 2013, the problem has rotated to oil producers. China’s corporate debt has soared to vertiginous levels. Recorded dollar debt in emerging markets has doubled to $3.4 trillion in a decade, without including the hidden swaps. Local currency borrowing has risen by leaps and bounds. They are no longer low-debt economies.

The BIS credit gap indicator of banking risk is flashing a red alert for Hong Kong, reaching 35pc of GDP. While it has dropped to 22.1pc in China, the country is still in the danger zone. Any sustained reading above 30 is a warning signal for a banking crisis three years later.

Canada is also vulnerable at 11.3. Turkey (9.7) and Thailand (9) are on the edge. Most would be in trouble if global borrowing rose by 250 basis points.

The UK is well-behaved on the credit gap metric. That is small comfort. There will be nowhere to hide if the world ever faces a dollar ‘margin call’.

Ok, you get the point. Debt and leverage lead to bubbles. And bubbles eventually pop. Let’s keep our eye on the dollar. A rising dollar means the foreign borrowers will owe more. For example, if the dollar rises 10%, $25 trillion owed quickly becomes $27.5 trillion. Of course, if the dollar declines that’s a net win for the borrower. The problem is the size of the debt owed. The Fed is dismounting from QE at a very tricky time.

A rising dollar is the pin to the bubble. We keep watch…

And thus the current conundrum with the Fed raising rates and reversing course on QE. It leads to an interest rate mismatch globally (higher yields in the U.S.) and to a stronger dollar as that higher yield spread attracts money to dollar assets. Give me negative yield returns in Europe? No thanks. So yeah, there’s that.

The point is, like the sub-prime problem risk (we wrote about and got it right… yet honestly I underestimated the size of the systemic outcome), this current “Sovereign Debt” issue much larger than sub-prime.

What can you do? In the next section I share another in a series of “what you can do” to protect your backside.

Put a few well vetted simple rules-based processes in place that you trust and can stick to. Otherwise, find a professional who can help you.

Trend Following – Two Actionable Ideas

In the “what can you do about it” category, here are a couple ideas to think about.

Let’s look at two very simple trend following ideas.

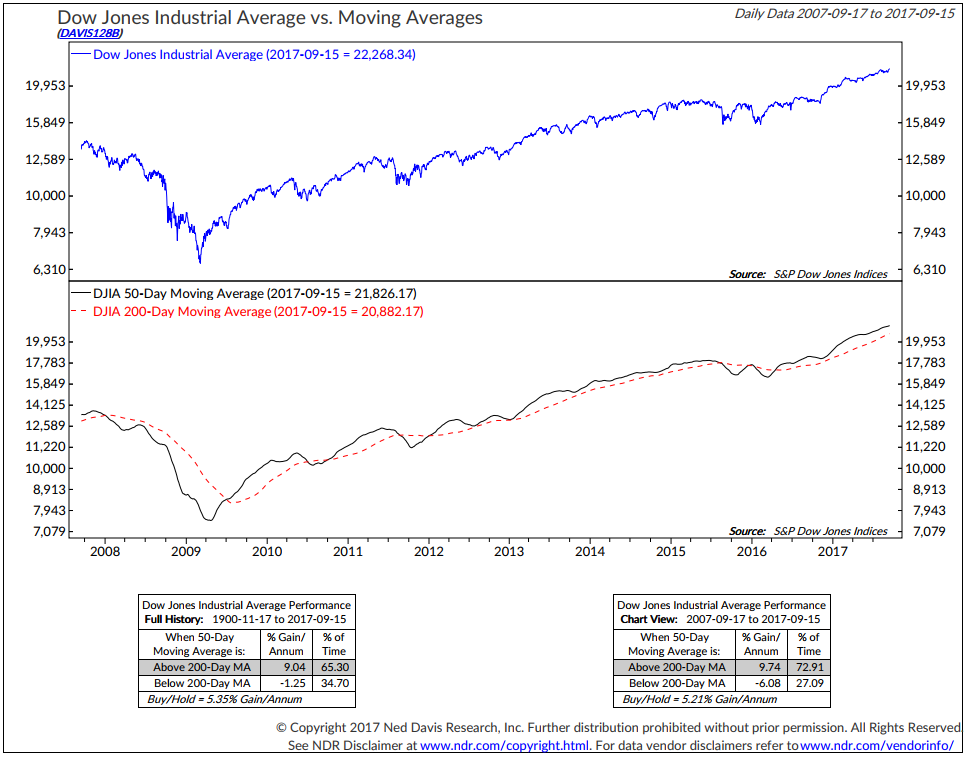

Most of us are familiar with the 200-day moving average (MA). It is simply a smoothing of the average price of, for example, the S&P 500 Index over the last 200 days. Take all the daily closing prices, add them up and divide by 200. It creates a smooth trend line that enables you to see if the trend is moving up or moving down.

In an uptrending period, the average price is moving higher. In a downtrend, it is moving lower. Investors can use the trend as an indicator as to when to be invested and when to hedge or get out of the market. But one needs to have a rule to trigger a signal. It’s one thing to see the trend line moving higher or lower, but it is another to know when to act.

One of the more popular trading indicators is called the “golden cross.” It is when the 50-day MA price line (the shorter-term trend) crosses above or below the 200-day MA price line (the longer-term price trend). A buy signal when it crosses above. A sell signal when it crosses below.

Statistically, the model looks like this (next chart):

- The middle section plots both the 50-day MA (black line) and the 200-day MA (dotted red line). A change in trend is signaled at the point in which they cross.

- Note the two data boxes in the bottom section of the chart.

- The left one looks at data from 1900 to September 15, 2017.

- The right one looks at data from September 17, 2007 to September 15, 2017.

- The gray shaded areas show the current signal. Buy signals when the 200-day MA is above the 50-day MA.

- Note the returns in each “buy” regime of better than 9% annualized.

- Note the annualized returns in each “sell” regime.

- Also, I like the “% of Time” data.

- Since 1900, the DJIA has spent 65.30% of the time in buy signals and 34.70% of the time in sell signals.

- Since 2007, the DJIA has spent 72.91% of the time in buy signals and 27.09% of the time in sell signals.

Now, if your annualized return was 9.74% since September 17, 2007 for 72.91% of the time, your annualized portfolio return would be approximately 7.25% (if you used this process to reduce risk on sell signals.) It would actually be higher because you would have earned money market returns when you moved to cash. By comparison, a buy-and-hold strategy would have returned 5.21% over the same period. Emotionally, it would also have helped you move through the period more comfortably. You can get to a similar comparison looking at the data since 1900 in the data box (lower section of above chart – left hand side.)

Bottom line: As you see in the above chart and in Trade Signals below, the current stock market trend remains bullish. I like the idea of reducing risk especially if you are nearing or are in retirement.

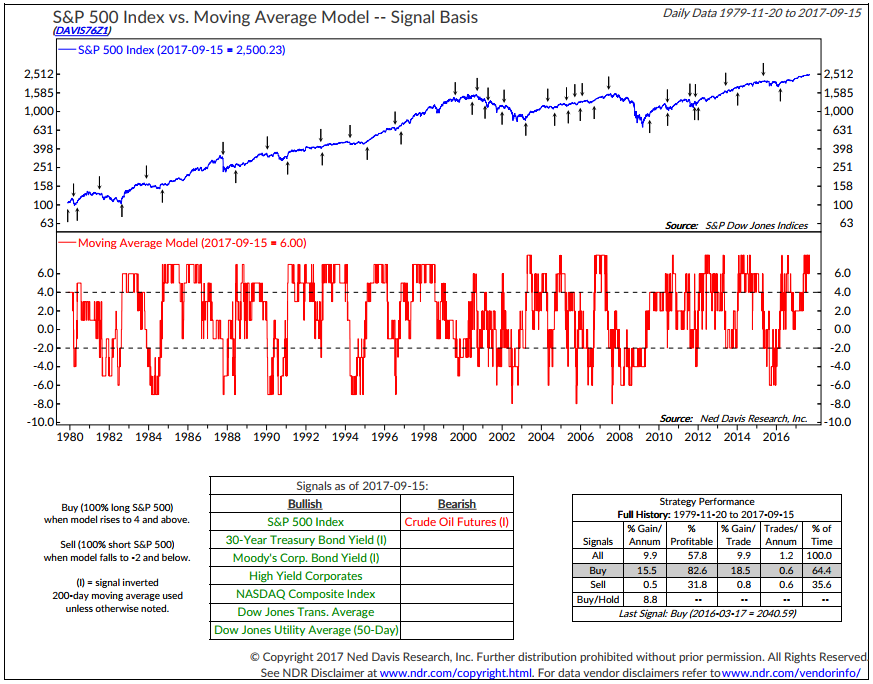

The next model tracks the moving averages of eight different asset classes and scores them up to determine the overall trend of the stock market:

- Upper section of the chart plots the signals: Buy (up arrows) and sell (down arrows).

- Eight different indices are tracked and scored bullish or bearish (data box in the lower left-hand side of the chart.) The middle red section plots the combined score.

- The data box in the lower right-hand section of the chart details the results.

- S&P 500 Index % Gain Per Annum equaled 15.5% with 82.6% of the signals producing profitable trades.

- The percent of time invested November 11, 1979 to September 15, 2017 was 64.4% of the time for a return of 9.98%, not including earnings on money market funds held 35.6% of the time.

I’ll see if I can get permission from Ned Davis Research to share this chart with you each week in Trade Signals. It’s a big ask. I’ll also ask if I can share the process rules with you. Let me know if you’re interested in learning more… And stay tuned…

Bottom line: I like incorporating several different processes to risk manage exposure. If you are a “DIY’er” (do-it-yourselfer) and have the discipline to stick to a process (and remove emotion from your trading), then consider using two or three different processes. For example, follow the NDR CMG U.S. Large Cap Long/Flat Index for one-third of the equity exposure in your portfolio, use the 200-day MA cross for one-third and find another process for the final one-third. None are perfect. Make sure there are high win rates in the strategies.

Diversify to several different trading processes. That’s one idea of a game plan. Hope it gets your risk management mind going.

The goal is to get from here to there in good shape – to participate in the secular bull trends (the current state) and minimize downside losses during the secular bear trends. Investing is about how money compounds over time. It takes a 100% return to overcome a 50% loss and a 300% return to overcome a 75% loss. Thus the need for downside risk management. See “The Merciless Mathematics of Loss.”

If you are 25 to 35 years old, dollar cost average and party on. If you are a pre-retiree like me or retiree with nearly 75% of all U.S. self-directed assets, well, we can’t afford the hit nor can we afford the 10-15 years of lost investment production it may likely take just to get back to even.

I smell a Sovereign Debt Crisis on the horizon. It will trip the global system. Defaults will rise, EM debt will sell off hard, banks will have issues, leverage will unwind, and liquidity will disappear.

If I’m right, the opportunity it will create will be outstanding. You will want to be in a position to take advantage of the opportunity. If I’m wrong, let the trend be your friend.

As a quick aside: Long-time readers know that I am a big fan of Ned Davis Research. I’ve been a client for years and value their service. If you’re interested in learning more about NDR, please call John P. Kornack Jr., Institutional Sales Manager, at 617-279-4876. John’s email address is [email protected]. I am not compensated in any way by NDR. I’m just a big fan of their work.

Trade Signals — Inching Higher in Bull Market Trend

S&P 500 Index — 2,507 (9-20-2017)

Notable this week:

The Ned Davis Research (NDR) CMG U.S. Large Cap Long/Flat Index is back to 100% fully invested in large cap exposure. Sentiment has turned bullish, suggesting short-term caution for equities. No other significant changes this week. The trend remains bullish for both equity and fixed income. High yield is in a buy signal (positive trend) as is gold.

Click here for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Personal Note

The winless Shipley Gators are coming off a 0-0 tie to an impressive team. My son, Kyle, is the goalkeeper and let’s just say he’s been getting a lot of action. But the team is improving and they host a home game against a league rival tomorrow. Stepson Kieran also has a game, so we’ll be racing from one to the other. I just don’t want this time to end.

My son, Matthew, will be about an hour away on a trip to raise money for Penn State’s annual dance marathon with proceeds going to children with cancer. They are paired with a wonderful young person and their family and get to feel the love and see the impact of their efforts. That makes dad happy.

Brianna is also coming home for the weekend, so we’ll try to catch the PSU-Iowa football game with Matt Saturday night. Yes, I’m one of those crazed Penn State fans and have brilliantly brainwashed my kids as well. Admittedly over the top, Susan just gives me that look (as she should.) But hey, it’s fun and I have a little side action with my friend, John Arthur, and his son, Chris. They are crazed Iowa Hawkeye fans.

The highlight of the weekend will be watching my niece, Ashley, play in a softball tournament on Sunday. My brother, Mike, passed suddenly last month and Ashley lost her wonderful father. Mike didn’t miss a game and was affectionately nicknamed “Waterboy” by the team.

“Waterboy”

Mike Blumenthal and his daughter Ashley

The upcoming travel schedule is not too bad. I’m in DC on October 11-12 for a conference and Dallas on October 25-26 for a famous Mauldin Solutions chili dinner. He really does make the best chili I’ve ever had and his prime rib is equally outstanding. John and the four strategists that make up his Mauldin Solutions Smart Core portfolio will be presenting to a select group of independent investment advisors. I’ll be in beautiful Charleston for a meeting with Forbes publishing on October 30. That should be interesting.

Wishing you a wonderful weekend. Hug your family… and love and enjoy the ride as much as you can. Life is way too short. Really looking forward to watching Ashley play on Sunday.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group