In her post-FOMC press conference, Federal Reserve Chair Janet Yellen is expected to provide a concise evaluation of the current economic situation. That includes a discussion about the recent trend in low inflation and the economic impact of hurricanes Harvey and Irma. She is not expected to signal what the Fed will do with short-term interest rates in the months ahead. At this point, nobody knows – that’s the point of monetary policy being “data-dependent.”However, we can expect to hear a lot about the “temporary” or “transitory” nature of forces on the economy – and it will take some time for upcoming data reports to present a clear picture.

On the inflation front, Fed officials have signaled a belief that much of the recent trend in low inflation is transitory. Notably, March’s sharp drop in the price index for wireless telecom services shaved about 0.2 percentage point from the year-over-year increase in headline CPI inflation (and about 0.25 percentage point in the core CPI). At the same time, officials are aware that structural changes in the labor market may be preventing wage growth from rising as much as in the past.

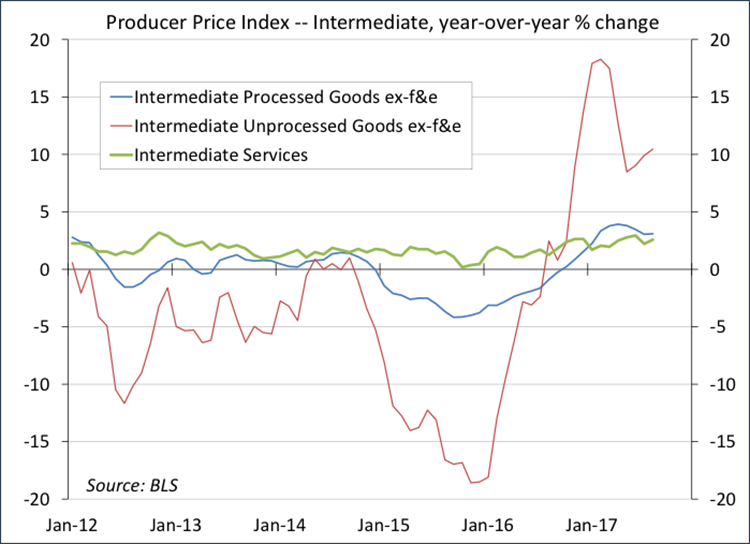

Drilling into the details of the August CPI report, we’re still seeing a continued deflationary trend in consumer goods ex-food & energy. Despite a pickup in global economic growth, there appears to be plenty of excess capacity in the production of goods. The producer price data had shown moderate pressure in finished goods, but this failed to flow through much to the consumer level. More recently, prices of intermediate goods and materials have begun to reflect pressure. A softer dollar, now down around 10% against the major currencies since the start of the year, may add further pressure.

Last week, the key mid-month economic data (retail sales and industrial production) were disappointing. Retail sales were weaker than expected in August, with significant downward revisions to the figures for June and July. Industrial production fell far short of expectations, although partly reflecting unseasonably mild East Coast temperatures. Hurricane Harvey likely had an impact, with mixed, but mostly negative effects on retail sales (the Bureau of Census says it’s impossible to tell how much of an impact Harvey had). Oil and gas well drilling, which has been recovering since last May, had a sharp setback, which was almost certainly related to Harvey.

We can expect to see a bounce back from Harvey’s effects in the weeks ahead. Energy exploration should pick back up and retail sales will rebound as Houston gets back to normal. Speaking from personal observation, Irma had a widespread impact on Florida’s economy, disrupting activity in the week before the hurricane’s arrival and in the aftermath. At the end of the week, many homes and businesses were without power, but activity should get back to normal in the weeks ahead. Don’t expect rebuilding to have a big impact on growth. It’s never enough to offset the loss of activity. However, whatever impact we see on 3Q17 GDP growth (probably 0.2-0.4 percentage point) should come back in the fourth quarter.

Still, there’s some question about what the economy’s strength is beyond the impact of the hurricanes. Adjusted for inflation, hourly earnings were about flat year-over-year in the first quarter. We saw a pickup in May, June, and July, as gasoline prices began to stabilize. However, August brought a decline; and we’re likely to see some softness in real earnings in September as well. Every month in 2017, motor vehicle sales have been reported lower than a year ago. Vehicle production was a source of strength in the economic recovery, but having likely topped out, we shouldn’t expect much contribution to consumer spending or industrial production from here on. So, the moderate pace of GDP growth isn’t likely to be temporary. Demographic constraints (slower labor force growth) will likely keep GDP growth in the 1.5-2.0% range over the next few years, whether or not we see much change coming out of Washington.

This restrained outlook for growth isn’t necessarily bad for the stock market. While growth is expected to be slower than historical norms, it’s still projected to be positive. Interest rates are expected to be lower than they would be otherwise, and lower interest rates imply the P/E ratios can be higher than usual. Of course, we could get some negative shock to the economy, or there may be some necessary adjustments if expectations prove to be too unrealistic, but a steady hand on the monetary policy tiller should help.

The greater uncertainty is who will be at the helm beyond February. The Wall Street types in the White House will likely have a significant hand in the president’s decision on the next Fed chair, but at this point, who knows?

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James