“While asset prices have decoupled from fundamentals, the gap has been filled by quantitative easing,

large cash reserves by corporations and worsening inequality.”

– Mohamed El-Erian: In Investing, The Journey Is Not The Destination

Last week, investors were lamenting the lack of inflation. This week, they’re fixated on its rise. On Thursday, data showed consumer prices climbed 0.4% in August from a month earlier and 1.9% from a year earlier, a sign that inflation is once again on the upswing after months of soft readings.

The report, “brought an end to the recent deceleration of consumer prices in the U.S. Large declines in the rate of change for headline, shelter, services, and core have now bottomed out,” on a year-over-year basis, said analysts at Bespoke Investment Group in a research note. (Source: WSJ)

We have reached a 5000 year low in interest rates. The ECB owns 40% of all Eurozone government debt. If any central bank is in danger of collapsing, in my view it is the ECB. But what and when and maybe not. A rise in interest rates might be the trigger. It will be rising inflation that causes the rise in rates. So today, let’s focus in on inflation.

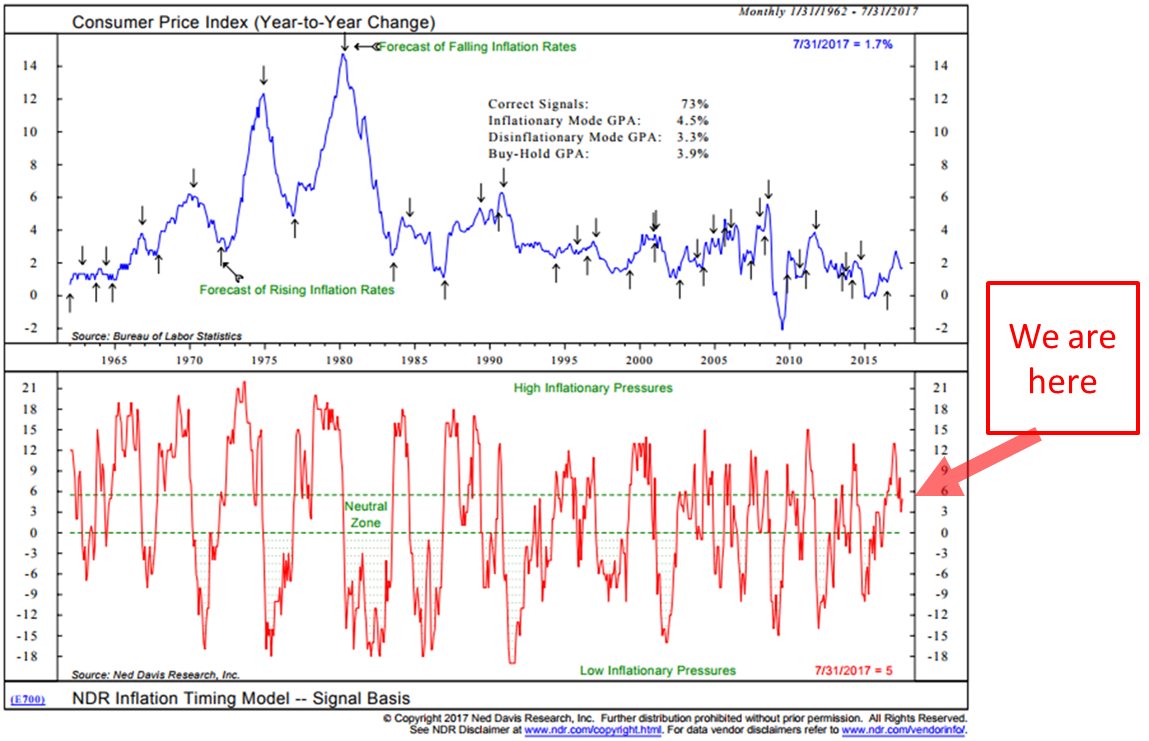

The following chart measures various levels of U.S. “inflationary pressures” – high, neutral or low. Data is through July 2017 and shows neutral inflationary pressures. You can see that the reading at the end of July was “Neutral Inflationary Pressures”.

However, the updated data, released just yesterday, shows the year-over-year change in the CPI (consumer price index) rose to 1.9% from 1.7% in August. No alarm bells just yet, but I suspect we just moved back into the “High Inflationary Pressures” zone. Bears watching…

About the model:

The NDR’s Inflation Timing Model consists of 22 indicators that primarily measure the various rates of change of such indicators as commodity prices, consumer prices, producer prices, and industrial production. The model totals all of the indicator readings and provides a score ranging from +22 (strong inflationary pressures) to -22 (strong disinflationary pressures).

High inflationary pressures are signaled when the model rises to +6 or above (upper zone above green dotted line). Low inflationary pressures are indicated when the model falls to zero or less (bottom zone).

What this means to you and your portfolio is that in high inflationary environments, interest rates rise. It also means that your $100 doesn’t buy you as much. Bond investments don’t do well in high inflationary periods. For example: Who wants to buy your 2% Treasury note if rates rise to 4% or 5%? Your bonds lose in value as the price declines and your portfolio loses in value relative to inflation.

As I shared in last week’s post,1966 to 1982 was a different type of secular bear experience. While the decline in the S&P 500 over the 16-year period was -1.1% annualized per year turning $100,000 into $83,645, after factoring inflation into the return the real after inflation return was -7.9% turning $100,000 in spending value into just $26,801. The point is inflation matters.

We want not too hot, not too cold but just right. And as investors we should keep our eye on too hot and too cold. Right now the central banks have us in the just right range. So that’s good… yet we watch.

I like to review NDR’s inflation timing model to get a feel for where interest rates might be headed next. As a quick aside, we are seeing managers reallocate that bond portion within a portfolio and replace it with tactical fixed income and liquid alternative strategies. With yields across the globe at near 5000 year lows, that seems like good sense to me.

Money For Nothing

Now look at them yo-yo’s that’s the way you do it

You play the guitar on the MTV

That ain’t workin’ that’s the way you do it

Money for nothin’ and chicks for free

Lyrics and Song

Speaking of low yields (negative in parts of Europe), perhaps the more immediate risk comes from Europe. The European Central Bank owns 40% of all Eurozone government debt. 40%! Not a typo. It’s more than 60% in Japan, but let’s focus on Europe for now. Printing and buying bonds. Money for nothing comes to mind. Now look at them yo-yo’s, that’s the way you do it, money for nothin’… The developed world if fighting deflation. I worry we may just get inflation. With so much debt, the rise in rates is a serious risk.

I believe that if any central bank is in danger of collapsing, it is the ECB. Raising rates in Europe will create a huge hole in the ECB’s balance sheet. At which point, the true cost of quantitative easing (“QE”) will be revealed. When Mario Draghi stops the bond buying program, the void must be filled with real buyers.

We remain in a surreal and creative central bank liquidity-driven world. No one knows how this will play out. A beautiful or ugly deleveraging as Ray Dalio calls it? We don’t yet know. I’m praying for beautiful. It requires global political coordination and each country’s internal political resolve. As central banks attempt to exit unprecedented participation in markets, we need to be aware of what this might mean. As risk managers, we measure and we watch.

BTW, Draghi knows that when he ceases to buy the debt, it will cause rates to rise for governments will be forced to find real buyers. If I had to pick one spot on the globe that may be the next crisis epicenter, my best guess is Europe.

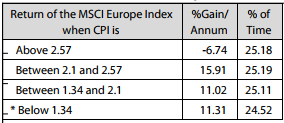

To that end, inflation pressures remain low in Europe at just 1.3% year-over-year at the end of July 2017. And how does inflation in Europe effect European stocks, you ask? It looks like this (data 1991 through July 2017 – from our friends at NDR). So far, ‘money for nothing’ is working. It’s when it gets above 2.7 that we don’t get our stock returns for free.

Before you click through, I visited the NASDAQ today for a quick interview with Jill Malandrino, NASDAQ’s global markets reporter. Behind me is the options trading area and you’ll hear some of the noise in the background. The interview clip is just five minutes long and I touch on the history of bull and bear markets, valuations and the ongoing equity bull market trend.

You’ll note some load background noise. It’s options expiration Friday and well, let’s just say, it gets loud in Philly. If your video feed stops at the five second mark, just bump it slightly forward with your mouse. Click on the photo below to see the clip.

Jill Malandrino, NASDAQ’s Global Markets Reporter. Click on the photo to see the short interview:

Grab a coffee and read on. The balance of the post is short but may print longer because of the charts. I picture story just how interwoven we are to global trade. And you’ll see that the Trade Signals remain bullish.

I did promise you last week a link to the Barry Ritholtz – Professor Richard Thaler interview from the recent Morningstar ETF Conference. They are working on getting it formatted and posted. Stay tuned, it’s coming. Do have a great weekend. The weather in Philly looks great. I see golf and youth soccer in my weekend forecast. And a cold IPA. Maybe two!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- Volume Precedes Price

- Charts of the Week

- Trade Signals – Equity and Fixed Income Price Trends Remain Bullish

- Personal Note

Volume Precedes Price

In the ‘what you can do category,’ you can control a good portion of the risk in your clients’ portfolios. I share ideas each week in Trade Signals (link below). There are other processes like putting a 200-day stop loss rule in place. Though that is not my preferred method. I liked this next quote from Ned Davis.

“The late analyst, Joseph Granville, liked to say that “volume precedes price.” By this, he meant that daily and weekly volume on the stock exchanges usually peak out prior to the bull market peak in prices. I think this is almost universally correct at tops, and is often true at bottoms where the peak volume comes on a selling climax with lower volume on a test of these lows.” – Ned Davis

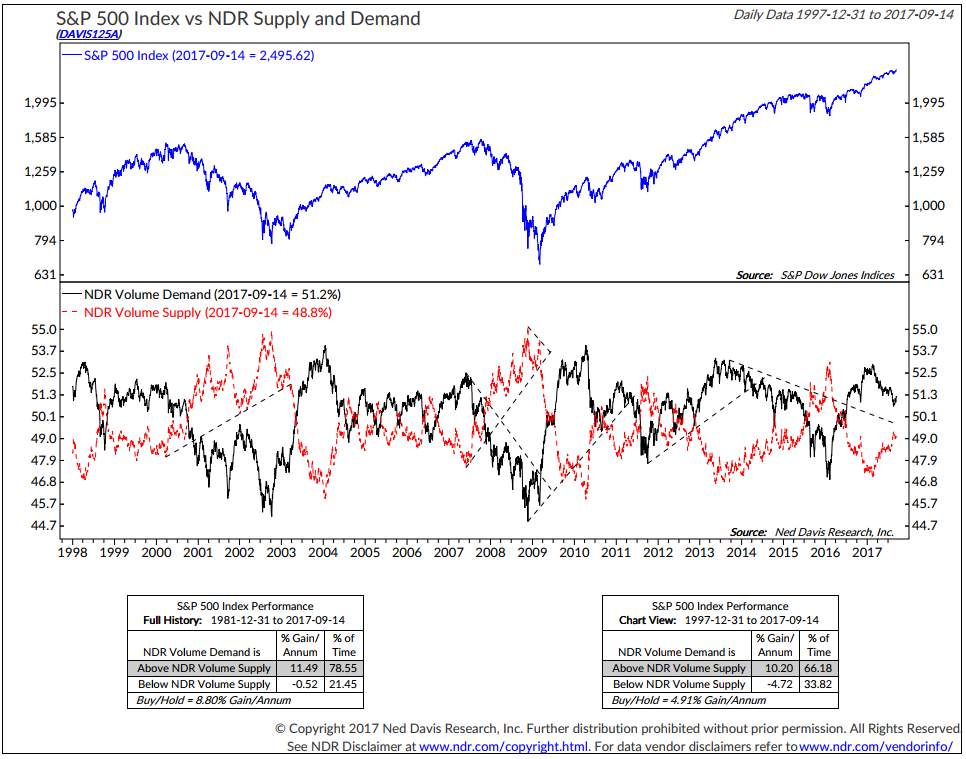

NDR tests just about everything. By now you know I’m a big fan. My friend, Robert Schuster, refers to NDR as “myth busters.” Maybe that’s why I like them so much. Recently, they shared some of their research that takes an objective look at volume and found volume more useful when divided into up (demand) and down (supply) volume.

One of the Trade Signals I post each week looks at just this. It measures volume demand (think of it as buyers) vs. volume supply (sellers). More buyers than sellers is what drives prices higher or vice versa. Looked at statistically, it looks like this:

Here is how you read the chart:

- Focus in on the stats boxes at the bottom of the chart.

- Shaded is the current regime, i.e., more buyers than sellers.

- Note the returns in each regime.

- The middle section (black line) tracks the volume demand (buyers) and the (red line) tracks the selling supply.

- Note the great sell signal in 2007 and the one in 2000.

I like watching this chart because it removes noise and tells me what’s happening in the markets. For now, there are more buyers than sellers and this indicator still leans mildly bullish. Not perfect but nothing in this business is.

Long-time readers know that I am a big fan of Ned Davis Research. I’ve been a client for years and value their service. If you’re interested in learning more about NDR, please call John P. Kornack Jr., Institutional Sales Manager, at 617-279-4876. John’s email address is [email protected]. I am not compensated in any way by NDR. I’m just a fan of their work.

Charts of the Week

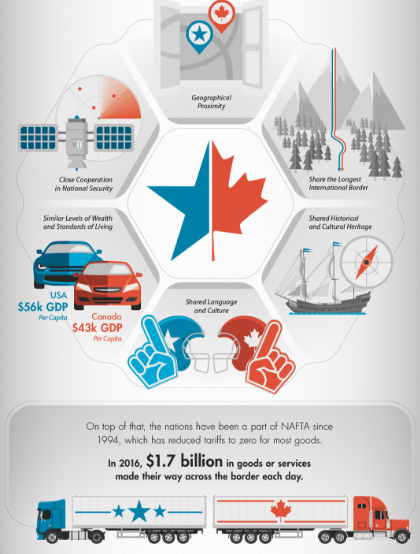

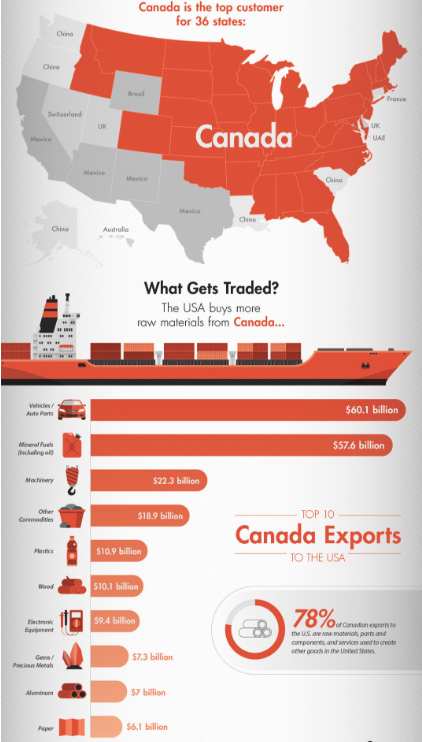

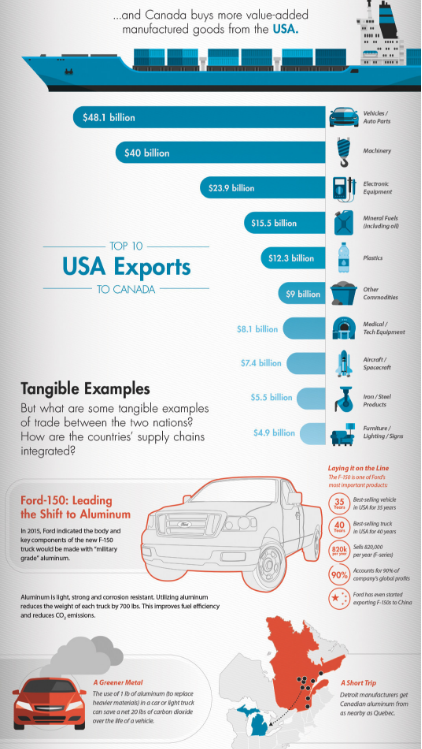

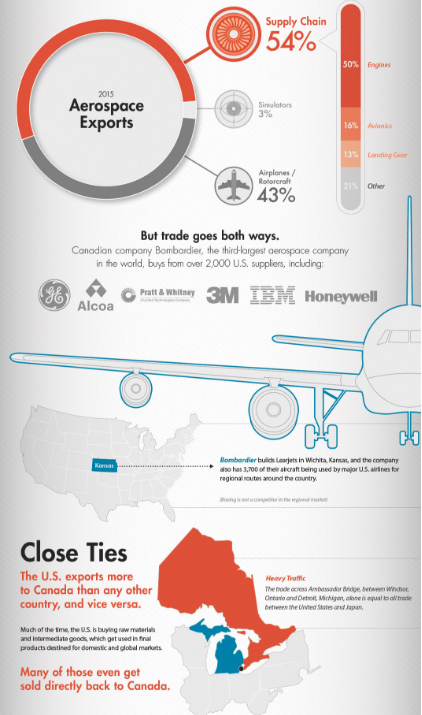

Who is the U.S.’s biggest customer? I guessed Mexico. I thought China was bigger than 8% and Japan bigger than 4%. It’s Canada and to give you a feel for how important global trade is to the economic system, this chart of the week will give you a feel.

In a picture story it looks like this:

A few bullet points:

- It’s estimated that 78% of Canadian exports to the U.S. are raw materials, parts and components, and services used to create other goods in the United States

- Through many years of trade, the supply chains between the two countries have become highly integrated.

- Much of the time, the U.S. is buying raw materials and intermediate goods, which get used in final products destined for domestic and global markets. Many of those even get sold directly back to Canada.

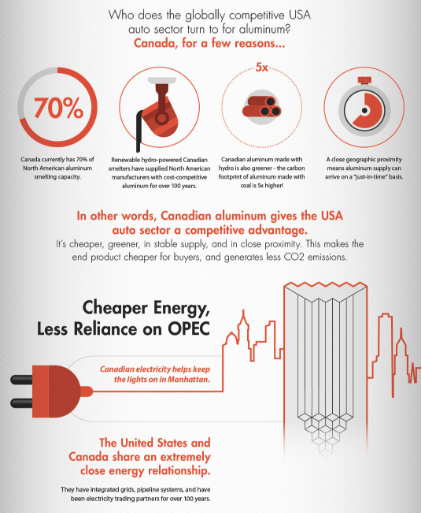

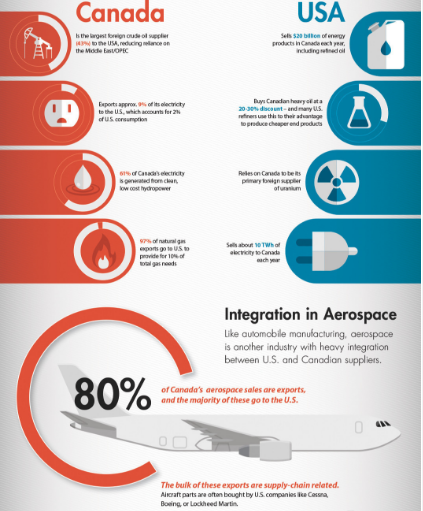

- This could be buying Canadian crude to reduce reliance on OPEC, importing low cost hydroelectricity during times of heavy rainfall, or using Canada’s steady supply of aluminum to make more environmentally-sound vehicles.

- Few countries in the world have this kind of economic interdependence – and the history, integration, and value of goods traded makes this arguably the world’s closest bilateral trade relationship.

Here is the bottom line: Can you imagine the implications if one of the two partners, or both, throws a monkey wrench in bike spokes of this highly integrated and co-dependent system?

Keep a close eye on what is to come out of Washington as it relates to the global trade picture for it may, depending on tax, walls and trade gates, have immediate impact on not only the global economy but ours as well. Tweet tweet… just saying.

Source: @wef; Read full article

Trade Signals — Equity and Fixed Income Price Trends Remain Bullish

S&P 500 Index — 2,495 (9-13-2017)

Notable this week:

No significant changes since last week’s post. Investor sentiment is now neutral having worked off extreme pessimism. The trend remains bullish for both equity and fixed income. High yield is in a buy signal (positive trend) as is gold.

Trend Dashboard

Equity Trade Signals (Green is Bullish, Orange is Neutral and Red is Bearish):

- Ned Davis Research CMG U.S. Large Cap Long/Flat Index: Partial Sell Signal – The indicator remains Bullish for Equities; however, the process reduced large-cap market exposure from 100% to 80% on 6-13-17

- Long-term Trend (13/34-Week EMA) on the S&P 500 Index: Buy Signal – Bullish Cyclical Trend Signal for Equities

- Volume Demand (buyers) vs. Volume Supply (sellers): Buy Signal – S/T Bullish for Equities

- Don’t Fight the Tape or the Fed: Indicator Reading = +1 (Bullish Signal for Equities)

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Neutral Optimism (S/T Neutral for Equities)

- Daily Trading Sentiment Composite: Neutral Sentiment (S/T Neutral for Equities)

Fixed Income Trade Signals:

- CMG Managed High Yield Bond Program: Buy Signal — S/T Bullish on HY

- CMG Tactical Fixed Income Index: Bullish on Muni and EM Sovereign Debt

- Zweig Bond Model: Buy Signal — Bullish on L/T Bond Market Exposure

Economic Indicators:

- Global Recession Watch Indicator – Low Global Recession Risk

- Recession Watch Indicator – Low U.S. Recession Risk

- Inflation Watch – Low Inflation Risk

Gold:

- Long-term Indicator — 13-week vs. 34-week exponential moving average: Buy Signal

- Short-term Indicator — Daily Gold Model: Buy Signal

Click here for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances. All investments involve risk of loss.

Personal Note

Can I just say…I’m really excited about our future!…and about the opportunities in the markets. I’m a ‘participate and protect guy’ and believe that trend following can help you and me. I believe it is more important now than at any time since I began my career in 1984.

I, nor did most of my colleagues, have any idea a new bull market had been born. It was all about inflation. Treasury yields reached 16%. WIP (whip inflation now) buttons were worn. Volker dished out tough love. Now we are on the other side of that trade and Yellen is giving us cupcakes. Be aware of the risk, stay nimble and prepared with a solid game plan in hand. A lot of people will make mistakes – similar to 2000 and 2008. See the opportunity, not the worry.

Susan has been in California all week. Her step-father had a serious stroke and he’ll pass over any moment. He and Susan’s mom, Pat, flew from Sarasota, Florida last Friday to escape the storm. My plan is to send him love and celebrate who he is. I’m sad. Too much loss in too short of time. We should all have family that loves us so much.

While Pat and Susan sit with Bob, a story came up about something Bob did or said. Susan turns to Pat and said perhaps we should whisper. Dad’s unconscious but the doctors say the last thing to go is the hearing. Pat laughs and said, he could never hear us anyway. I’m looking forward to Susan coming home.

I hope you and your family are doing well. If you were impacted by the last two storms, please know we are thinking about you. … One step in front of the other. Forward we go…

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group