What Does the QE Experience Say About Rates in a Shrinking Fed Balance Sheet World?

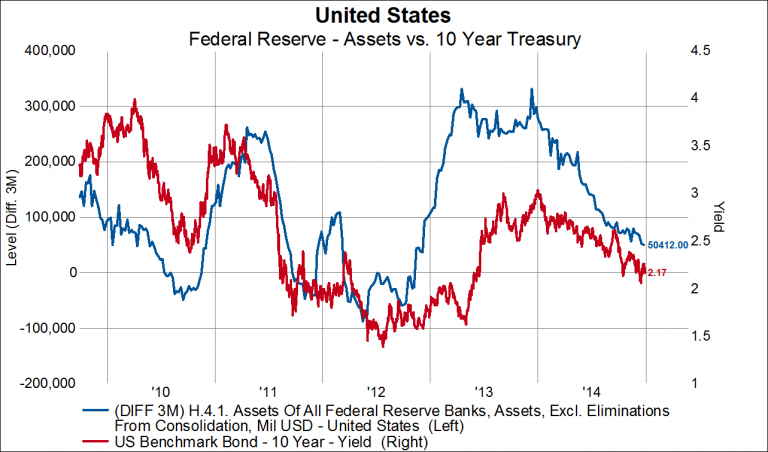

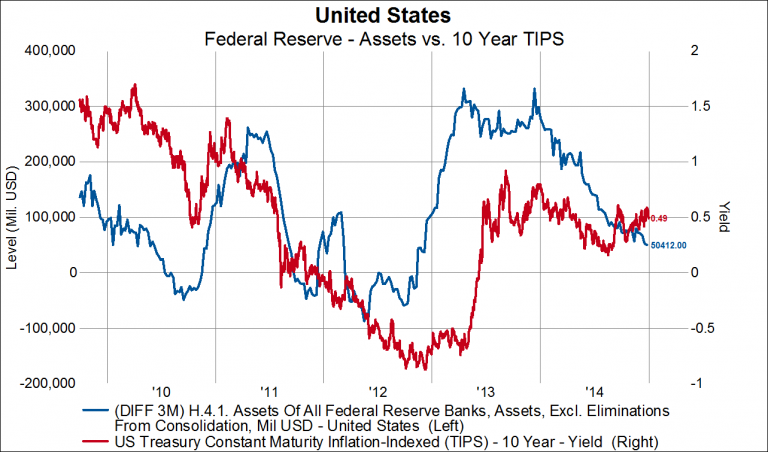

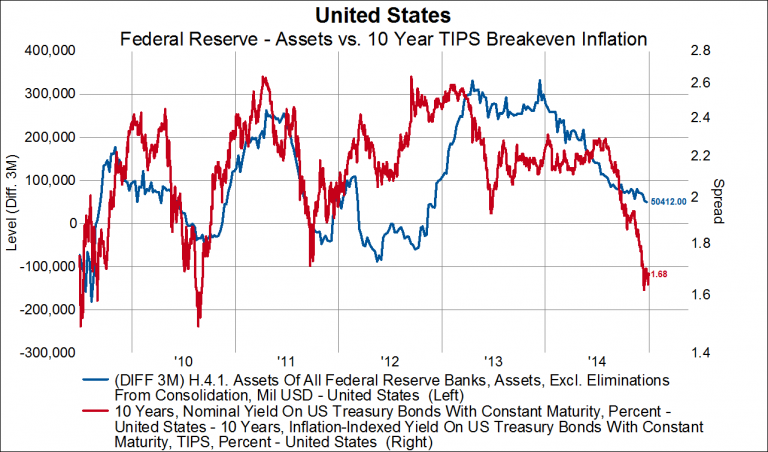

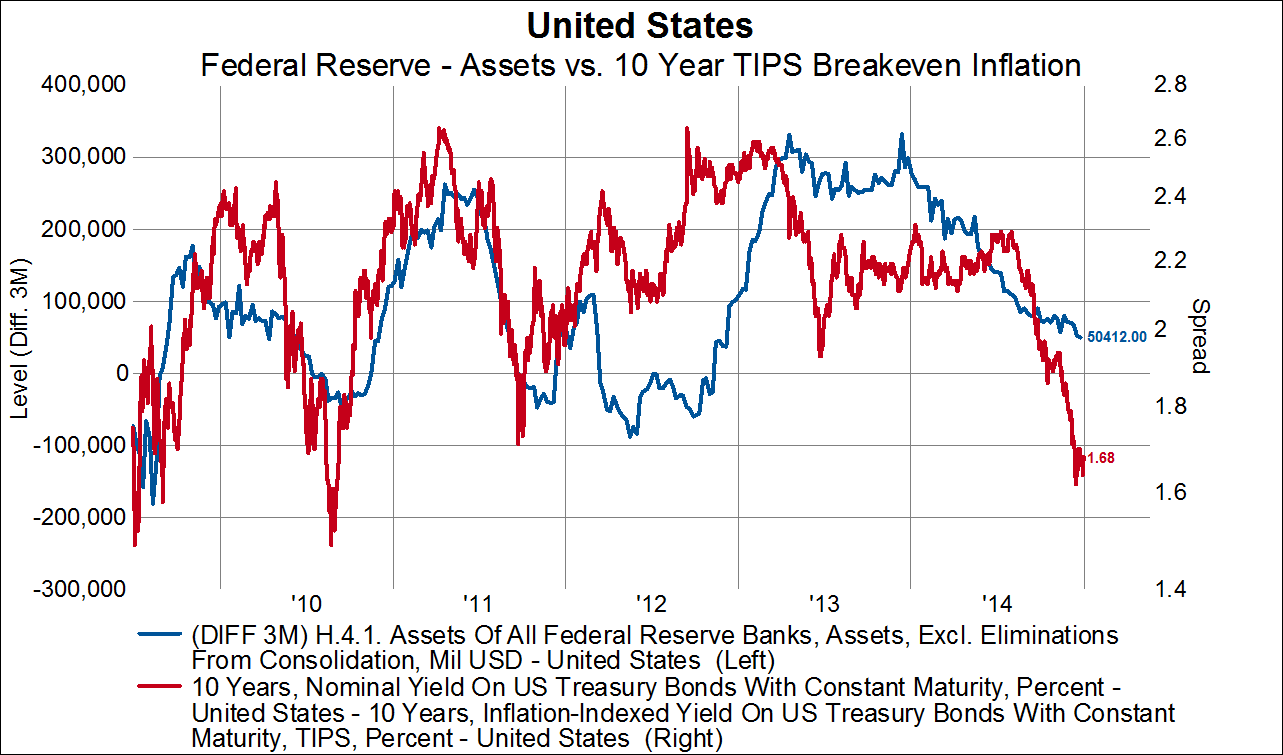

The Federal Reserve is likely to decide next week to begin letting assets roll of its balance sheet as bonds mature, instead of reinvesting the proceeds. This means that the balance sheet will begin to shrink in size and other market participants will be forced to absorb the supply of new issuance of treasury and mortgage backed securities. Conventional analysis of supply and demand dynamics might suggest the exiting of a large marginal buyer of these securities would cause yields to rise to some higher equilibrium level, but the QE experience suggests something else entirely. When the Fed was engaged in asset purchases and the rate of change in the Fed’s balance sheet was rising (late 2010, mid 2012 through early 2013) long-term treasury yields rose on the back of juiced growth and inflation expectations produced by the stimulus. When the rate of change in the Fed’s balance sheet would flat line or fall (most of 2010, most of 2013 through 2014) treasury yields fell on the back of subdued growth and inflation expectations. Importantly, it was both real rates (TIPS) and breakeven inflation that followed this pattern, which is indicative of the level of economic stimulus produced by QE. Chart 1 below shows 10-year nominal rates (red line, right axis) overlaid on the three month difference in the Fed’s balance sheet (blue line, left axis). Chart 2 below shows 10-year real rates (red line, right axis) overlaid on the three month difference in the Fed’s balance sheet (blue line, left axis). Chart 3 below shows 10-year implied breakeven inflation expectations (red line, right axis) overlaid on the three month difference in the Fed’s balance sheet (blue line, left axis).

But all that is history. The question now is what will happen to rates as the Fed begins to unwind its balance sheet. Is there a reason to believe that inflation and growth expectations will rise as the Fed tightens policy? In other words, is there reason to believe rates will act differently during the unwind than they did during the wind? We think the same economic mechanisms that were in place between 2009-2014 are still in place today and that long rates are likely to move lower as the Fed tightens policy via a smaller balance sheet.