1. Harvey to be Largest Natural Disaster in US History

2. 80% of Houston Homes Have No Flood Insurance

3. America’s Middle Class Making Strong Comeback

4. So, When is the Next Recession?

Overview

For most of this year, I’ve had a sense that the American middle class is increasingly growing, and that wages/incomes are increasing more than the Labor Department reports. I have been saving articles upon articles on this subject and was planning to extract the highlights and summarize them for you in the next week or two in these pages.

Over the weekend, however, I ran across an excellent piece on the expanding middle class from one of my favorite writers, Robert Samuelson, who has already done all the work for me on this particular topic. I will reprint it in its entirety below.

As you read it, pay particular attention to the section (with underlining) where he makes the case that wages for full-time workers are increasing at a median rate of 4% annually, rather than the apprx. 2.5% the Labor Department reports. I have read similar analyses from other independent sources elsewhere.

Before we get to the uplifting piece from Samuelson on the middle class, I have some thoughts and some facts and figures regarding Hurricane Harvey and the heartbreaking devastation along the Gulf Coast and parts of southeastern Texas.

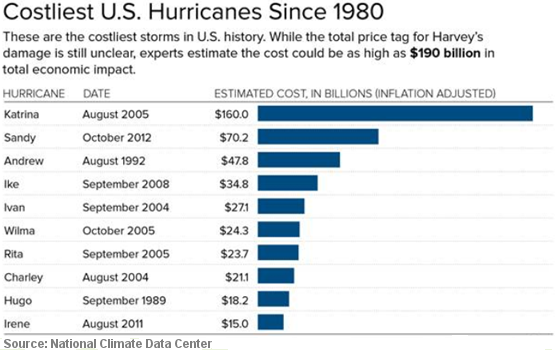

Harvey to be Largest Natural Disaster in US History

Hurricane Harvey has dealt a devastating blow to the Houston region, which was recently on track to account for almost 2.5% of the nation’s economy (GDP) this year. The question is, how much will the disaster in Texas and Louisiana impact the overall economy in America?

The answer, of course, depends on how much it will cost to clean up all the damage and rebuild all or most of what was destroyed. Estimates of what it will cost to do this vary widely, but a consensus is growing that it may cost as much as $190 billion – and that number could grow.

This means that Hurricane Harvey is the largest natural disaster in US history in terms of the overall cost to the economy. Take a look:

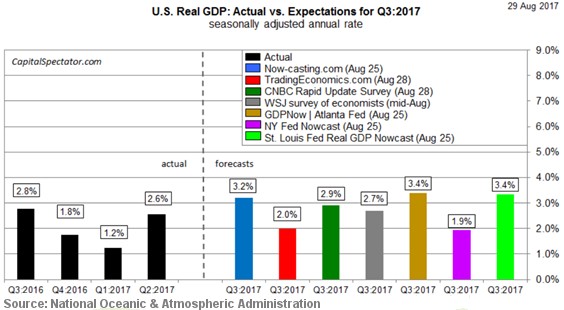

While Harvey devastated the Texas Gulf Coast and parts of Louisiana, and will take years to rebuild, estimates vary widely as to how much effect it will have on the national economy. Some forecasters predict Harvey will shave up to one full percent off of GDP nationally, while others continue to believe that 3Q GDP will come in above 3% when the first Commerce Department estimate is released at the end of October.

Historically, it is true that big hurricanes and other natural disasters tend to reduce near-term economic output. But it is also true that they have the effect of increasing longer-term economic growth because of reconstruction efforts.

While household wealth in the Houston region will take a huge hit from the storm, the price tag may not show in the GDP data. The energy sector, which has a large economic footprint in Houston, will certainly suffer, with the economic consequences rippling out across the nation. Gasoline prices have already increased by over 30 cents per gallon on average since the monster storm hit.

Despite that, the Atlanta Fed's GDPNow model is still indicating slightly higher GDP growth of 3.1% in the 3Q, up from 3.0% in the 2Q (as of September 1). The question is how or if the Q3 GDP predictions will change in the days ahead, once a deeper measure of Hurricane Harvey's damage is factored into the mix.

Here are some estimates for 3Q GDP since the hurricane hit. The consensus is 2.8%. Note that the latest Commerce Department estimate of 2Q GDP came in at 3.0% (not the earlier 2.6% shown below).

80% of Houston Homes, Businesses Have No Flood Insurance

One of the most shocking statistics to come out of the hurricane disaster is the apparent fact that apprx. 80% of Houston homes and businesses that were hit hardest by Harvey do not have flood insurance. This is according to Risk Management Solutions (RMS), the world’s leading catastrophe risk modeling company.

That means families with water-damaged walls, soaked furniture and homes still flooded will likely have to dig deep into their pockets or take on more debt to fix up their homes. Some may be forced to sell, if they can, and leave their communities.

Homeowners insurance typically covers just damage from winds, not floods. For that, you need separate coverage from the federally-run National Flood Insurance Program. The insurance must be bought by homeowners with federally-backed mortgages living in the most vulnerable areas, called Special Flood Hazard Zones.

About 1.2 million properties in the Houston-Sugar Land-Baytown area are at high/moderate risk of flooding but are not in a designated flood zone requiring insurance, research firm CoreLogic estimates. That’s roughly half of all properties — residential and commercial — in that area.

Even so, RMS predicts that Harvey could be the largest event ever directed at the federal flood insurance program managed by FEMA. It remains to be seen how much disaster relief will be coming from Congress just ahead. President Trump has asked for an initial outlay of nearly $8 billion, but most agree it will ultimately be much bigger.

This accelerates the critical issue of raising the debt ceiling. Some argue that Congress can’t dole out billions in disaster relief until the debt ceiling is raised or suspended. Expect this debate to get bigger and louder in the days just ahead. I’ll stay on top of it.

Now let’s move on to Robert Samuelson’s excellent column on the growing middle class.

“America’s Middle Class Making A

Major Comeback Under Donald Trump

by Robert J. Samuelson

On this Labor Day, the American middle class survives. Indeed, it’s expanding. That’s not the conclusion of some arcane scholarly study. It’s the judgment of Americans themselves, though it hasn’t received much attention from politicians or the media. Most Americans have moved beyond the fears bred by the Great Recession. The middle-class comeback may be the year’s most underreported story.

Public opinion polls depict the change. In its surveys, Gallup regularly asks people to report their social class. They are given five choices: upper class; upper middle; middle; working; and lower class. In 2006, before the recession, 60 percent of Americans identified themselves as either middle or upper middle class, while 38 percent chose working class and lower class. Only 1 percent put themselves in the upper class.

The 2008-09 financial crisis and the Great Recession demolished these long-standing class patterns. The middle class shrunk dramatically amid high unemployment, home foreclosures and heavy debts. As late as 2015, the country was almost evenly split between those in the middle and upper middle classes (51 percent) and those in the working and lower classes (48 percent), according to Gallup.

No more. In its latest poll on class identity, done in June, Gallup found that 62 percent put themselves in the broadly defined middle class, while only 36 percent classified themselves as working class or lower class. The shifts, said Gallup, began in 2016 and demonstrated “that subjective social class identification has stabilized close to the prevailing pattern observed before 2009.”

This is no fluke.

The temptation is to dismiss the Gallup results as an outlier. Don’t. Karlyn Bowman, the polling expert at the American Enterprise Institute, spends her time searching for opinion trends. She finds that countless polls tell a similar story. People are more optimistic. Many polls have, like the survey on class, returned to pre-crisis patterns. “We’re back economically” is how she puts it.

Consider trends from three polls:

■ Jobs are more plentiful. A Gallup poll in August found that 59 percent of respondents thought it was a “good time to find a quality job.” In 2009 and 2010, this rating hovered around a meager 10 percent.

■ More people feel they’re getting ahead. In July, 42 percent of respondents to a Fox News poll reported personal gains, up from only 23 percent in 2008 and beating the previous peak of 41 percent.

■ Most workers do not believe their jobs will be outsourced abroad, contrary to much commentary. A Gallup poll this year reported that nine of 10 workers feel unthreatened by outsourcing.

It is not that U.S. workers have no worries. But job growth, up by 17 million since the recession-low point, and wage gains have reduced anxieties.

Indeed, wages for many middle-class workers may be understated. Median weekly earnings grew almost 2 percent annually from 2012 to 2016. But these numbers are depressed by the retirement of well-paid baby boomers and their replacement by lower-paid, younger workers. When economists at the San Francisco Federal Reserve eliminated these effects, median wages grew nearly 4 percentannually for continuously employed full-time workers.

All this is reassuring. Middle-class values of order, predictability and personal responsibility have not entirely vanished. People could repay debts or add to savings. The University of Michigan Survey of Consumers reports that half of households say their “finances had recently improved, the best reading since 2000,” notes director Richard Curtin.

Just how this new middle-class confidence fares in the next (inevitable) recession is unknowable. Meanwhile, it poses two immediate questions. Has it raised President Donald Trump’s popularity? And second, has it reduced pessimism about American institutions, from Congress to the media? The answer to both seems to be “no.”

Here’s how the CBS News Poll assessed the effect on Trump: “President Donald Trump’s approval rating is unchanged from June and remains at 36 percent, while favorable views of the U.S. economy continue to soar to heights not seen in more than 15 years. … Americans say they’re evaluating him more on culture and values than on how they’re faring financially.”

As for an uplifting effect on other American institutions, there isn’t much yet. Gallup asks respondents whether they have “quite a lot” or “a great deal” of confidence in 14 institutions. The average level was 35 in June; Congress was 12, internet news 16 and big business 21. The highest rated institution was the military at 72, followed by small business at 70.

A successful America requires a large — and largely successful — middle class. The middle-class revival is evidence of optimism. The lingering question on this Labor Day is whether the revival has staying power. Or will memories of the Great Recession come back to haunt us?”

END QUOTE

* Robert Samuelson is a regular, nonpartisan columnist for The Washington Post.

So, When is the Next Recession?

As Mr. Samuelson argues, the growth in the US middle class seems on-track to continue for the next couple of years, at least until the “inevitable” recession occurs. The question is, when will that be? Of course, that is impossible to know.

Yet barring any major negative surprise(s), this economy feels like it is on solid footing even if it is getting a bit long in the tooth.

On the other hand, the odds of a major negative surprise(s) have increased in the last couple of years, especially with the deterioration of relations between the US and North Korea, among other global threats.

As always, I’ll keep you posted just ahead.

Best end of summer regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by Halbert Wealth Management, Inc. Gary D. Halbert is the president and CEO of Halbert Wealth Management, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, Halbert Wealth Management, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management