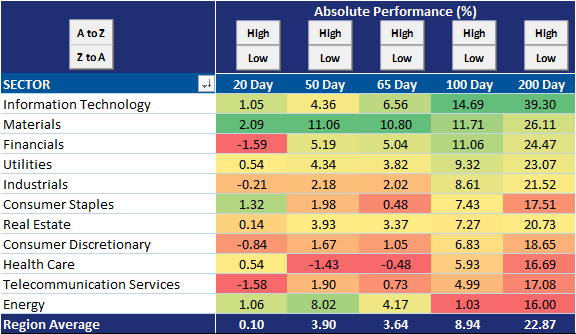

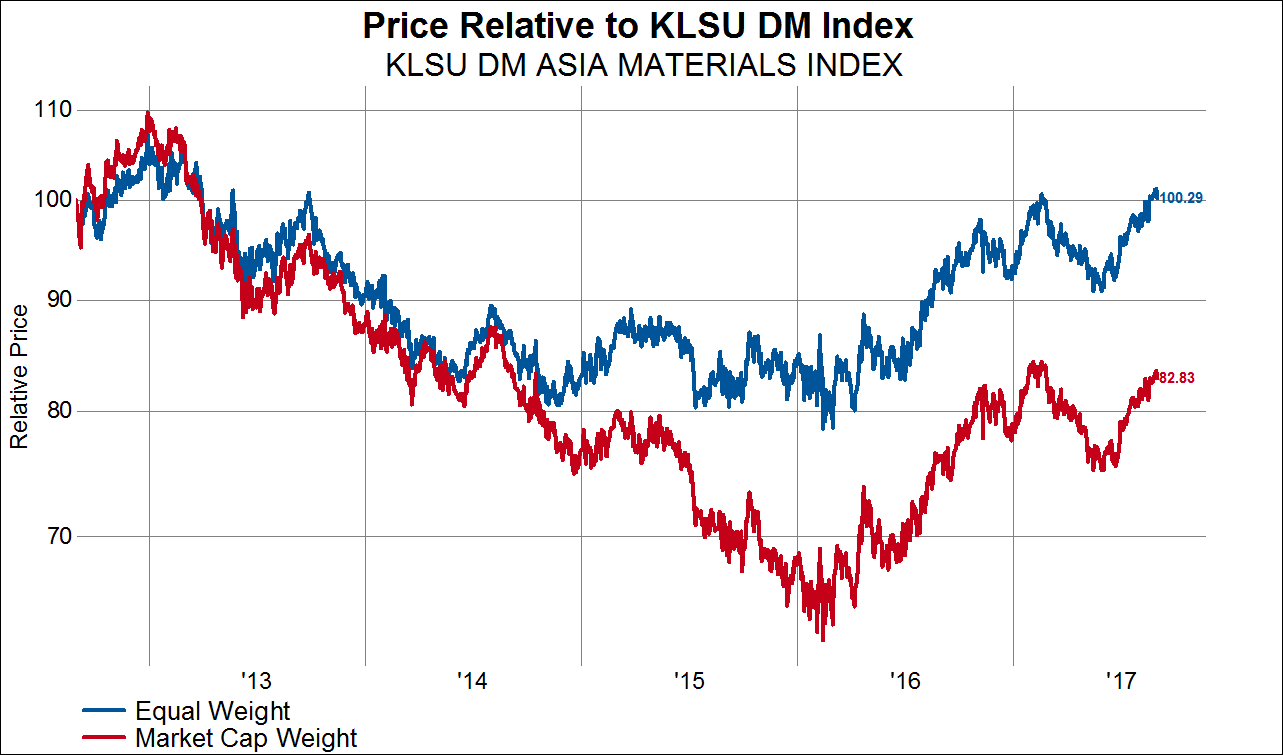

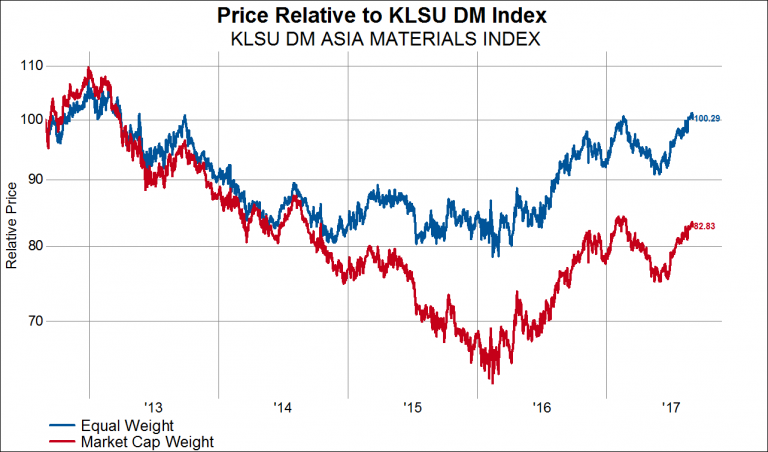

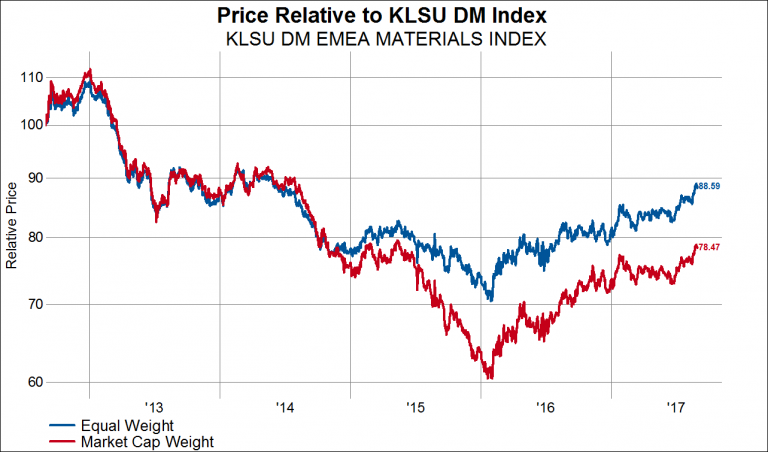

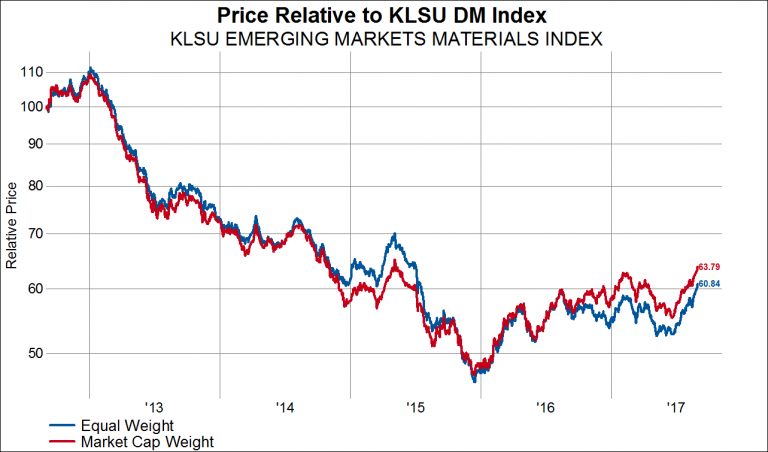

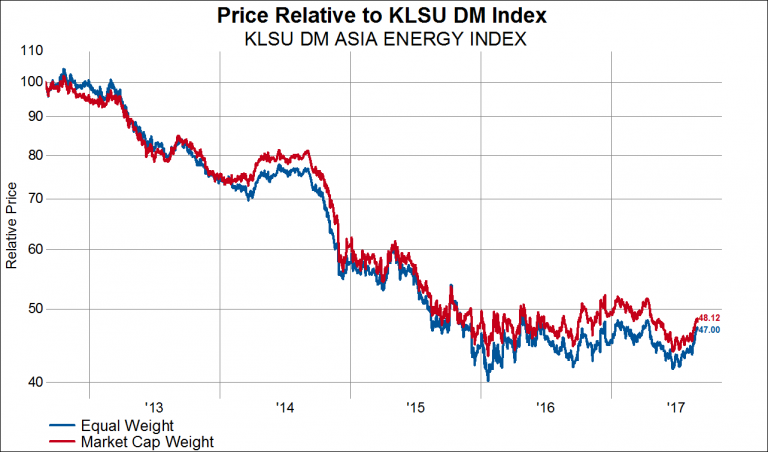

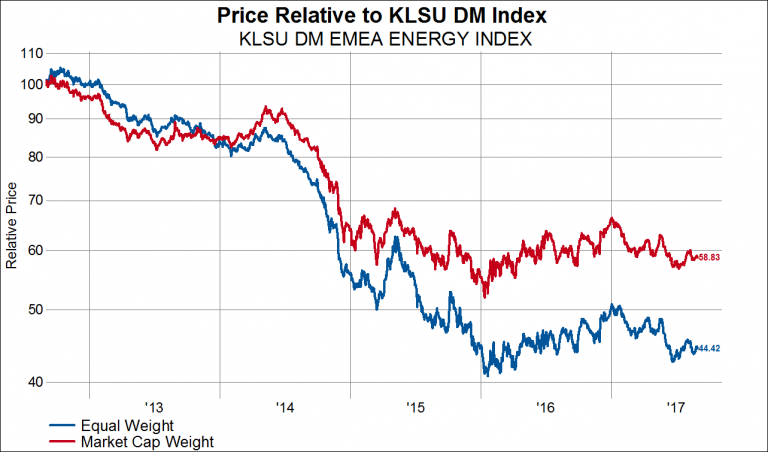

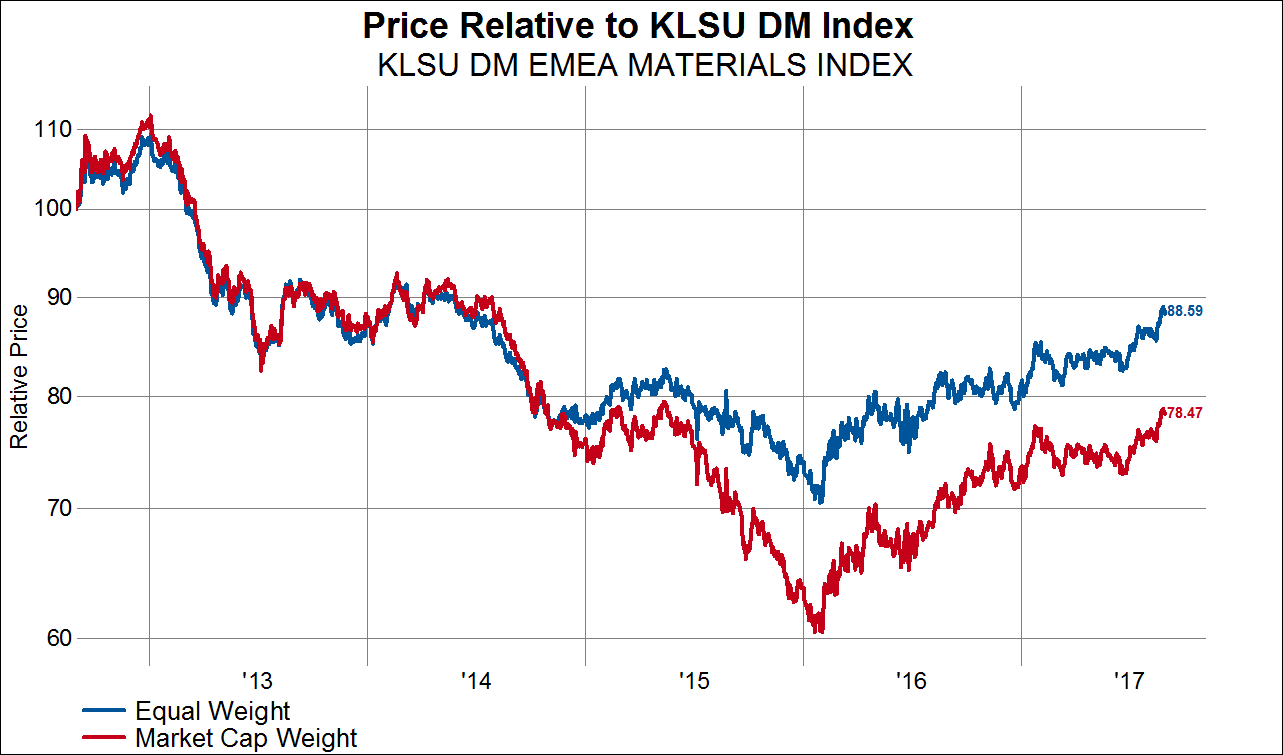

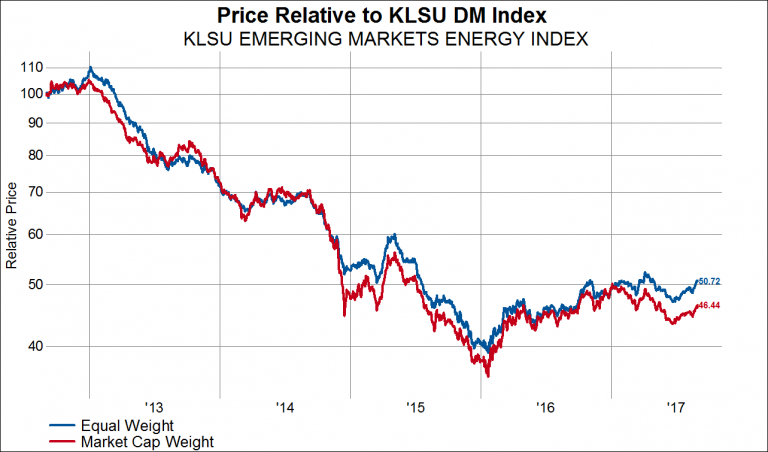

Investors Should Pay Attention to the Foreign Materials and Energy Sectors

We’ve been talking at length recently about the attractiveness of foreign, cyclical stocks. While foreign developed markets are attractive, emerging markets are especially attractive from a valuation perspective and are also benefiting from what we think is just the beginning of a persistently weak US dollar environment. Indeed, EM economies tend to benefit from strong currencies for at least two reasons. First, EM companies tend to have USD denominated debt so their debt payments go down when the local currency strengthens against the USD. Second, in countries where inflation can run hot – which is a lot of them and for a variety of reasons – strong local currencies suppress inflation (a boon for the consumer) and allow local central banks to cut rates. Performance trends are starting to reflect this new dynamic, as we will see.

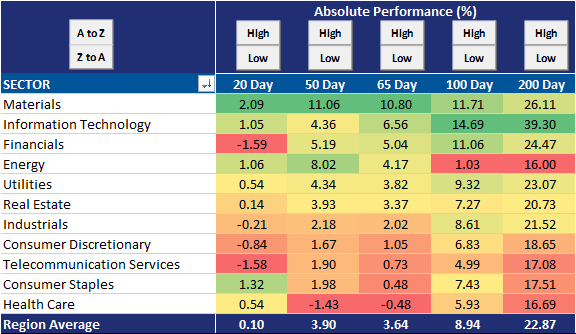

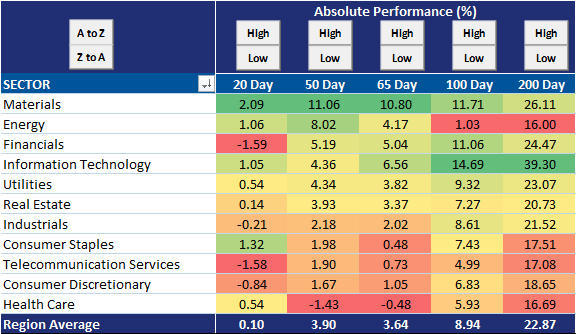

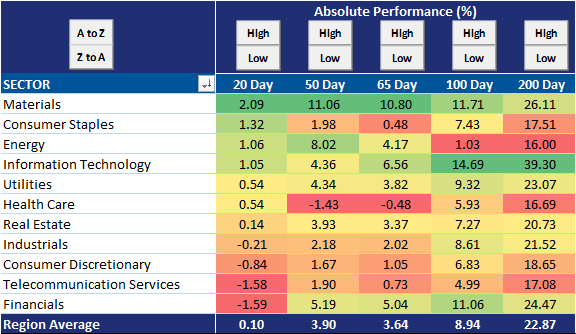

In the next four tables we show All Country ex US (so both DM and EM) sector performance on an equal weighted basis sorted by different time periods. Over the last 100 days (table 1) materials is the second best performing sector and energy is the worst. Over the last 65 days (table 2) materials is the best performing sector and energy is the fourth best performing. Over the last 50 days (table 3) materials is the best performing sector and energy is the second best performing. Over the last 20 days materials is the best performing sector and energy is the third best performing. The trend is that materials continues to be leadership and energy is gaining serious momentum.