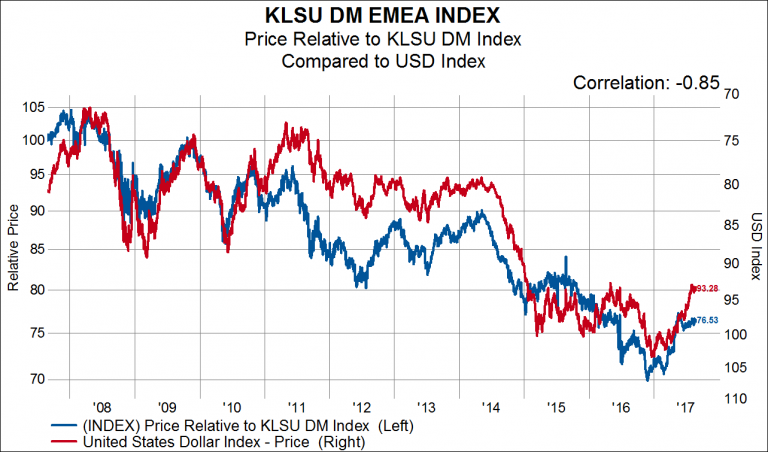

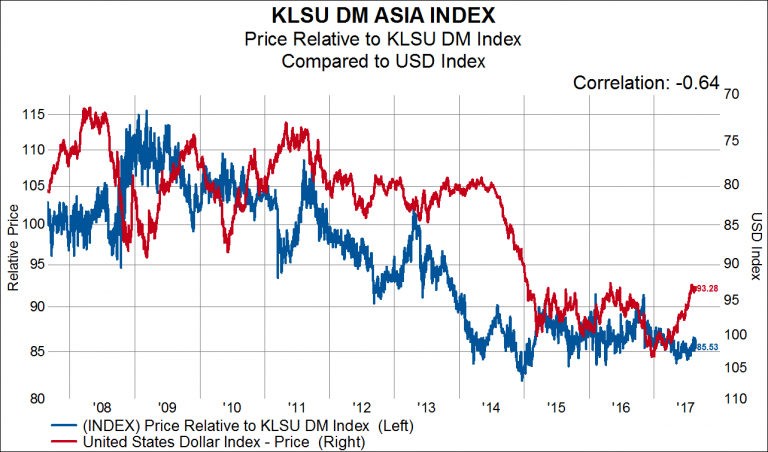

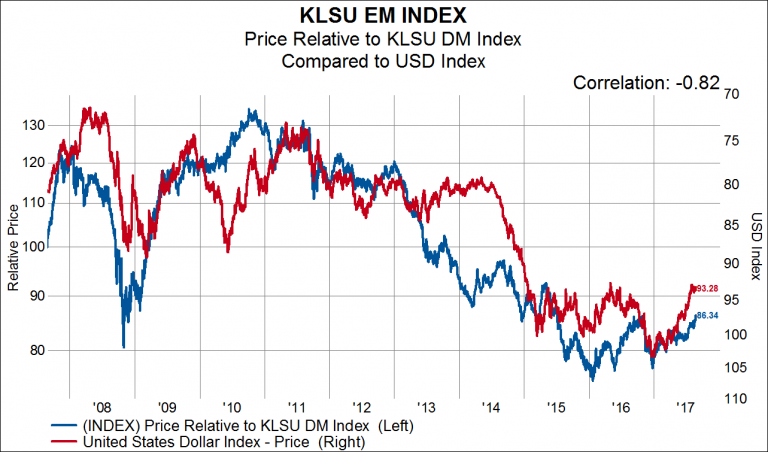

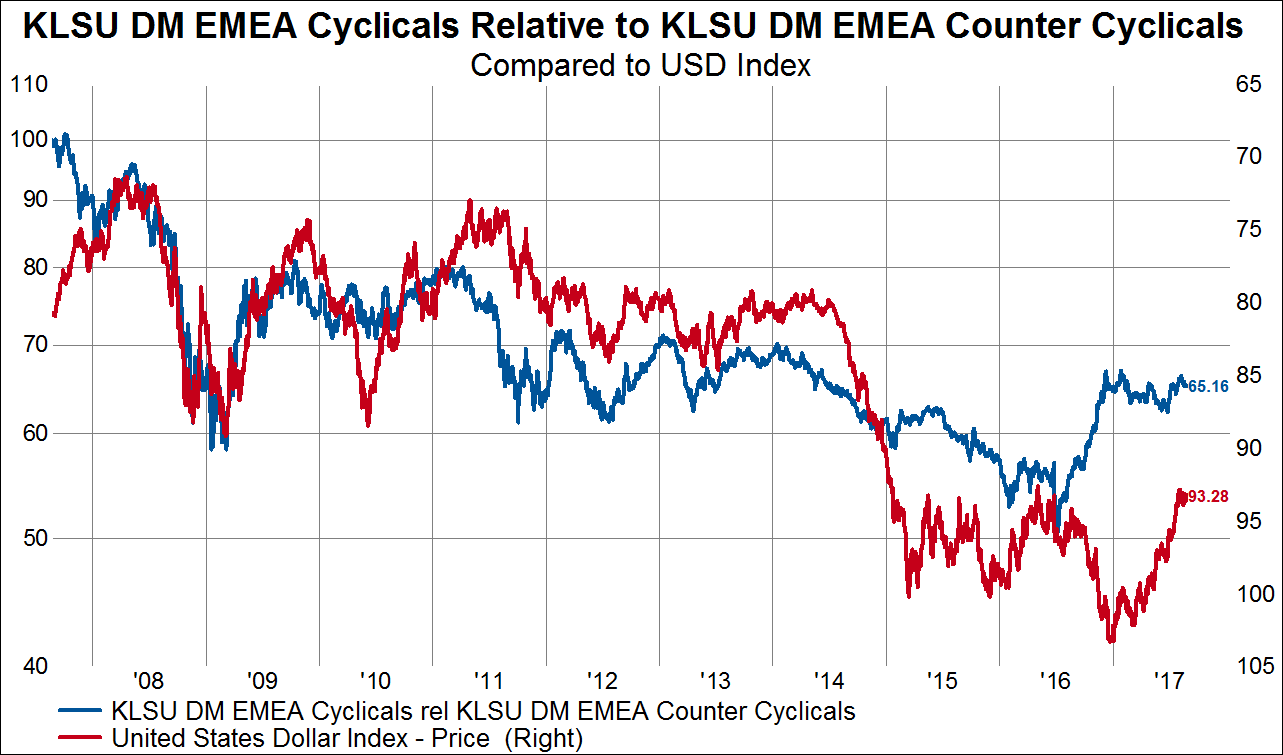

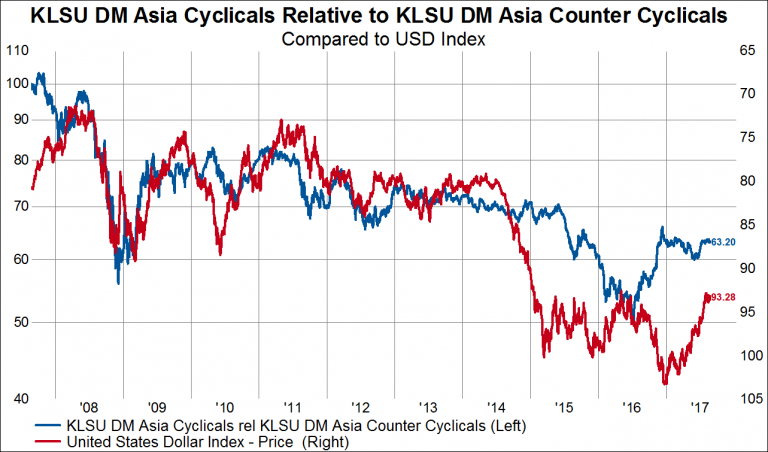

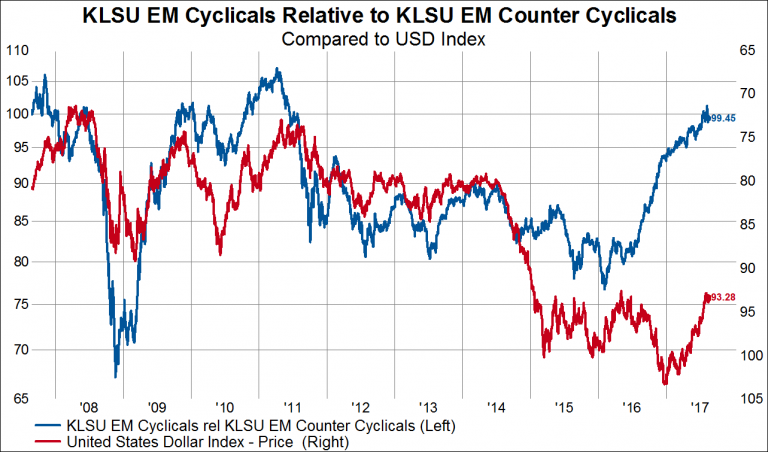

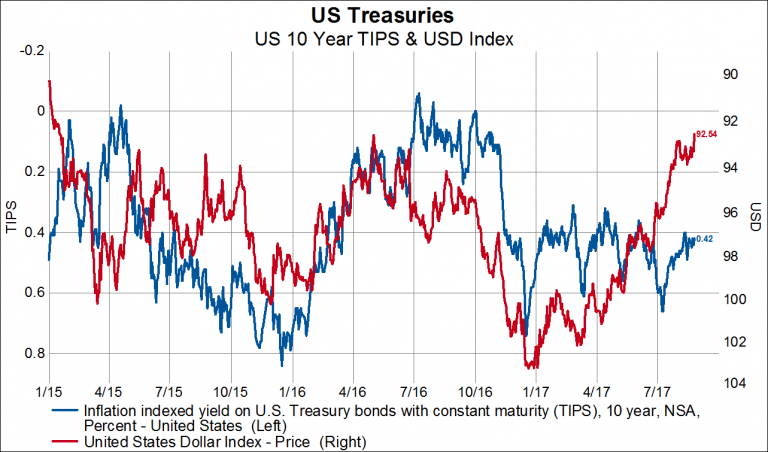

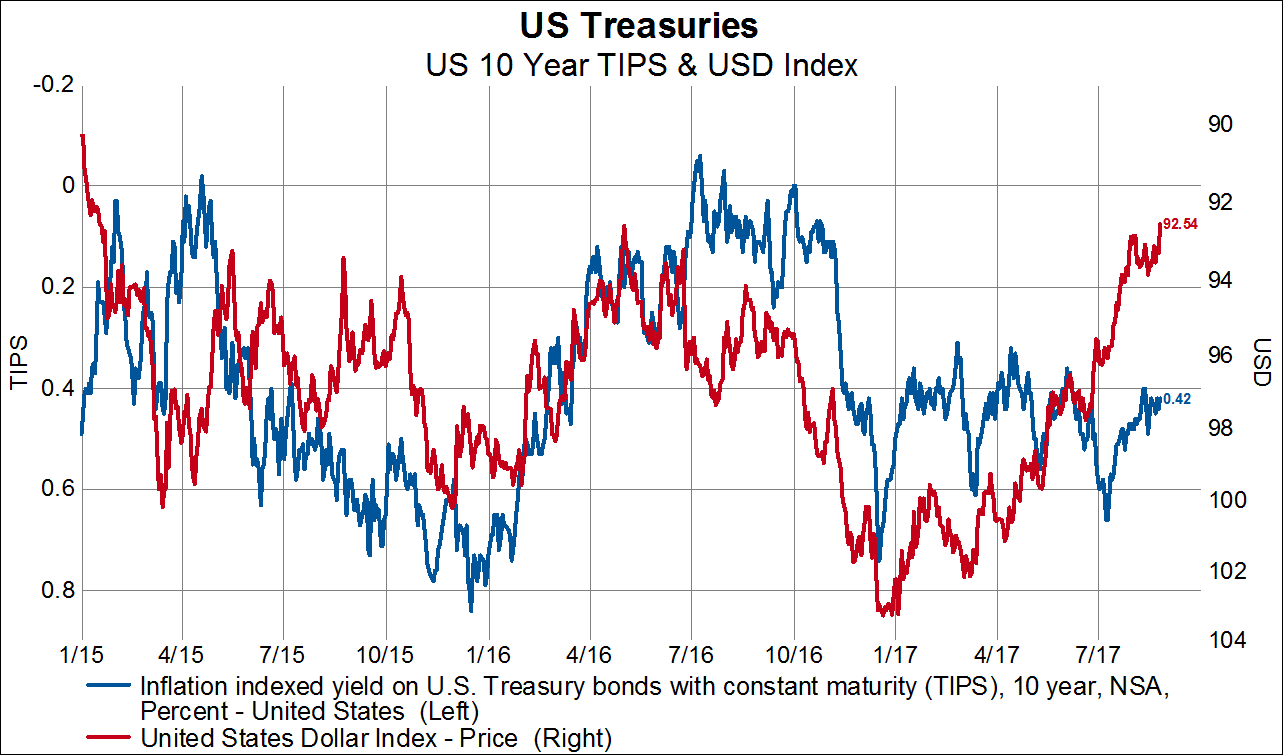

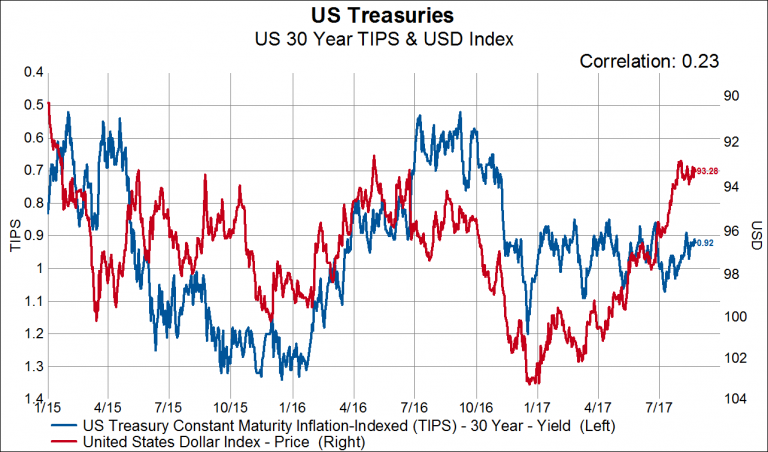

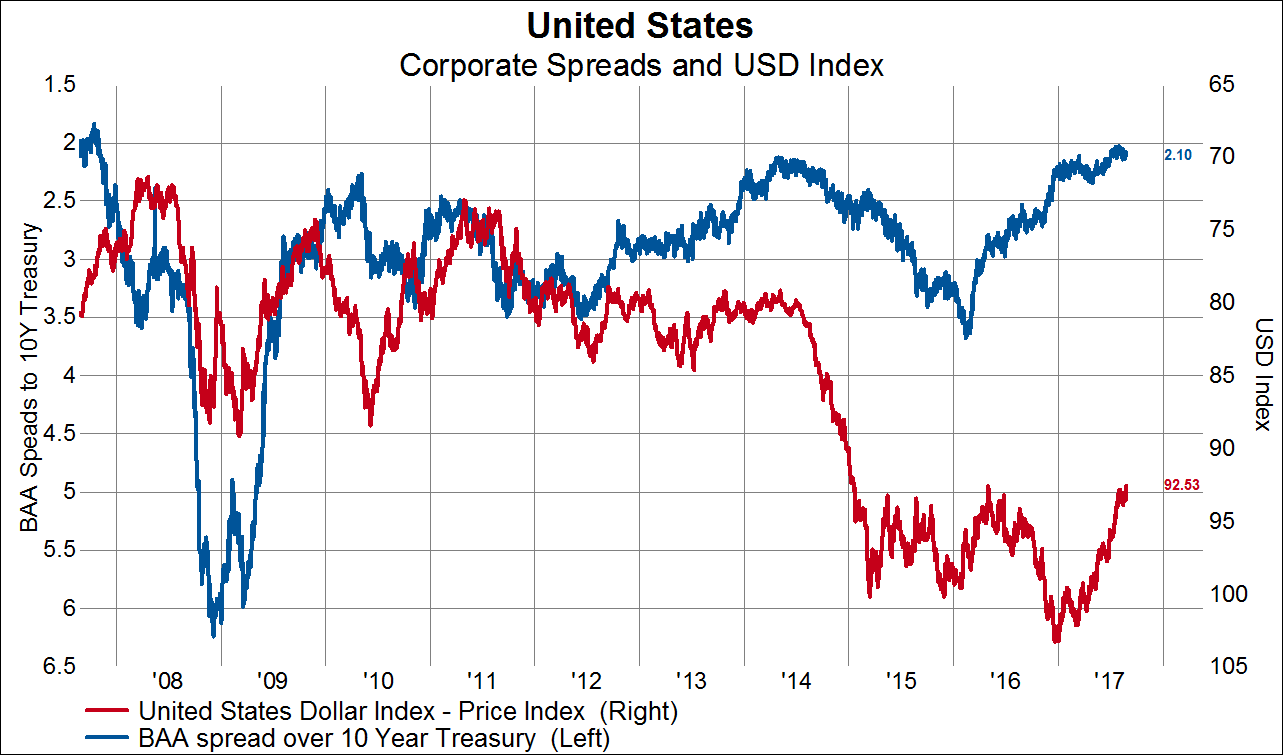

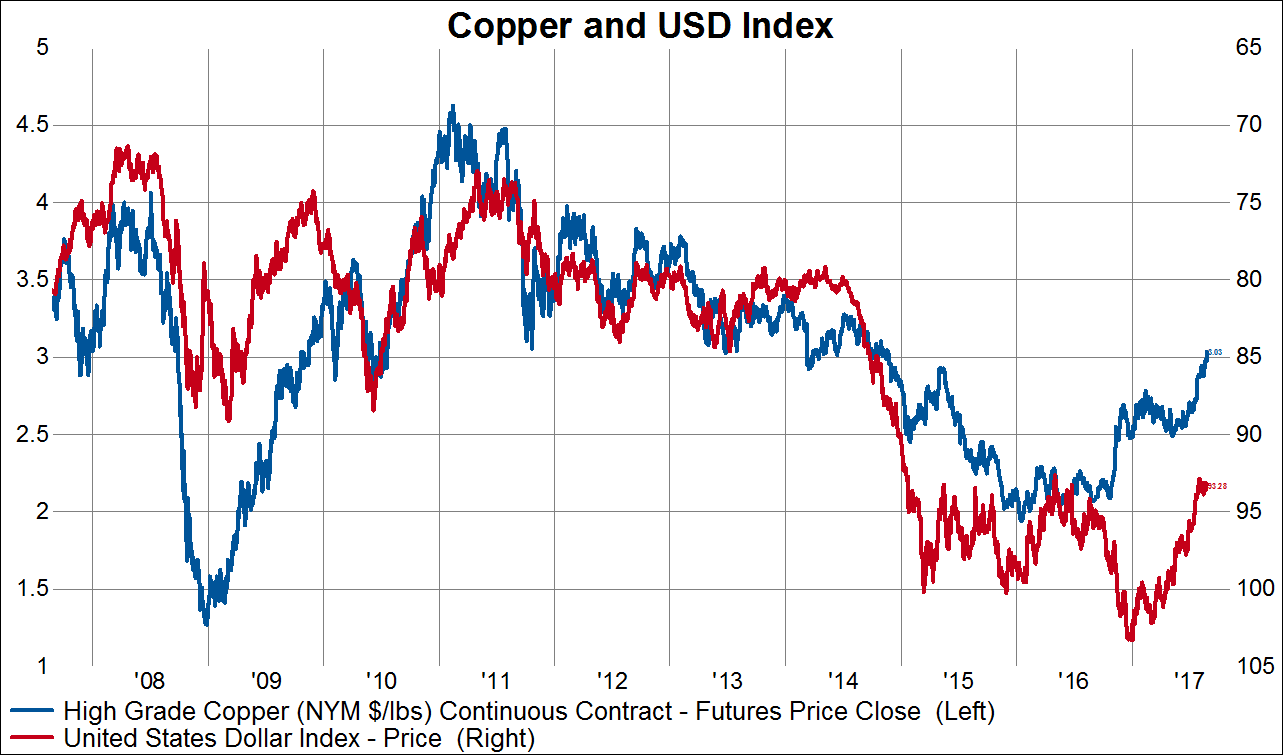

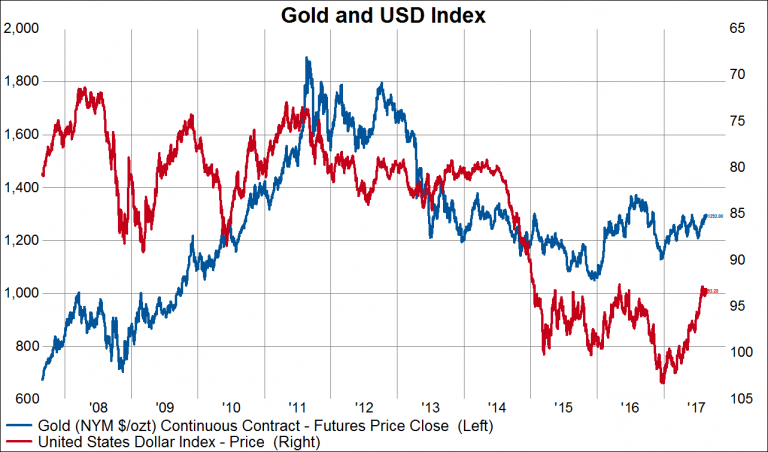

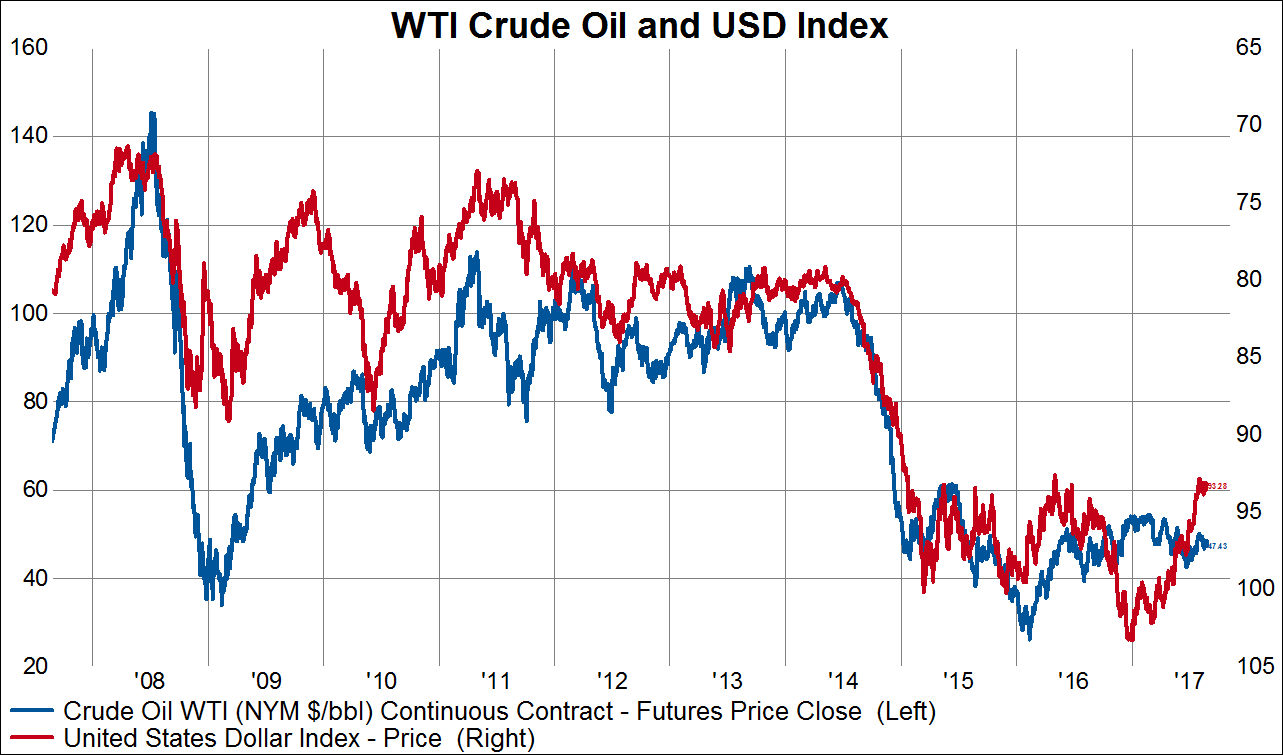

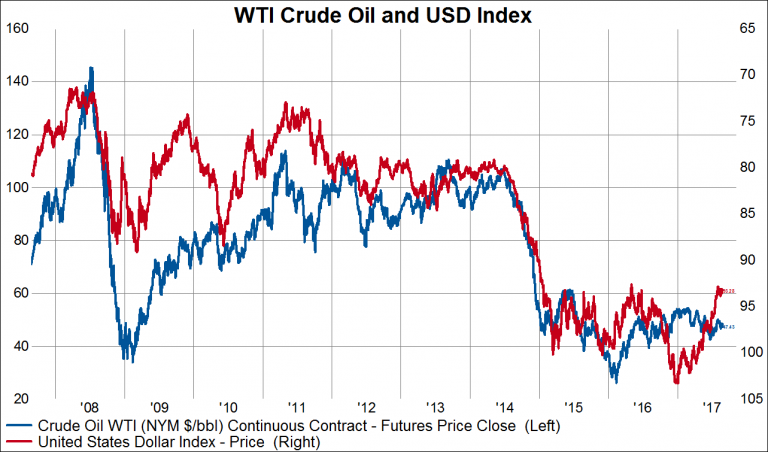

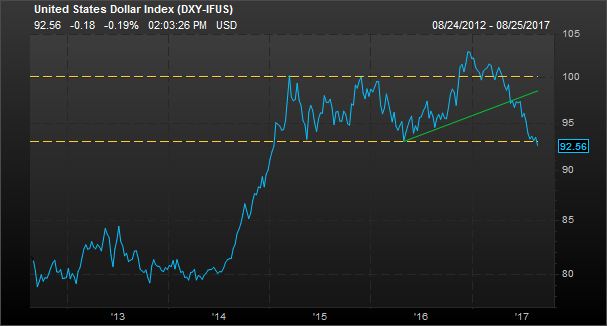

What Are the Asset Allocation Implications of a Persistently Weak USD?

We’ve been arguing since the end of 2016 that markets could be in for a sustained period of USD weakness and so far in 2017 they delivered just that. Indeed, even with the USD having its worst start to the year since 1985, the following items all argue for continued weakness in the USD: 1) baked-in higher budget deficits, 2) US economic underperformance, 3) a USD that is still overvalued against all the major currencies, 4) the heightened prospect of a deficit expanding tax cut instead of revenue neutral tax reform (i.e. the “easy” tax solution) and 5) newly introduced political risk. On top of that, the USD is today breaking through the bottom of a multi-year trading range with absolutely no technical support in the vicinity. As such, this is a great opportunity to revisit the asset allocation implications of a multi-year weak USD environment, should it come to pass. In all the charts below the USD index is the red line plotted on the right, inverted axis.

Foreign developed and emerging market stocks outperform US stocks when the USD goes down. In the below charts, the blue line on the left axis represents the relative performance of each region compared to our developed market index covering 85% of the investable market cap of each country: