On My Radar: Keep One Eye Focused on Growth and the Other on Capital Preservation

Learn more about this firm“[T]he big elephant in the room is the Fed.”

David Rosenberg

Chief Economist and Strategist, Gluskin Sheff + Associates

This week the Federal Reserve Bank of Kansas City is hosting its annual Economic Policy Symposium in Jackson Hole, Wyoming and a number of Fed officials have commented on “inflation.” Why is targeting inflation so important? Because rising inflationary pressures will cause the Federal Reserve to raise interest rates and such periods tend to prove challenging for the stock and bond markets.

In May, I shared the following on Fed tightening from David Rosenberg at the 2017 Strategic Investment Conference:

- [T]here’s never been a Fed tightening cycle that did not expose and expunge the bubble of the day, whether that’s in subprime autos, commercial real estate, leverage ETFs, take your pick.

- When the Fed is raising interest rates, these tightening cycles always start off benign but they never finish benign.

- And to get a sense of history, there have been 13 Fed tightening cycles in the post-World War II era, 10 landed us in an outright recession that the economists didn’t see coming ‘til we were knee-deep in it.

- There’s never been a Fed tightening cycle that left the economy stronger than what it was when they started.

If you missed last week’s post “Doesn’t Matter, Doesn’t Matter, Matters,” I shared my notes from a recent Bloomberg interview with Ray Dalio. There is an equilibrium in the capital market’s system where cash yields less than bonds and bonds have a lower return than stocks. There is an equilibrium that keeps working itself through the system; and monetary and fiscal policy are the tools we use as we work through short-term and long-term debt cycles.

So what our elected officials do in regards to fiscal policy (tax cuts and infrastructure spending are good and tariffs and trade restrictions are bad) and what the Fed does in regards to monetary policy (raise or lower interest rates, print and buy securities (“QE”) or unwind its balance sheet (“QT”)) impacts the economy and the markets in a powerful way.

How does this play out? We don’t yet know. Policymakers and central bankers will determine if the outcome will be beautiful or ugly. So we step forward and patiently watch.

Today I was a guest on Sirius XM’s “Behind the Markets” on Wharton’s Business Radio (Channel 111) with co-hosts Professor Jeremy Siegel and Jeremy D. Schwartz. Professor Siegel shared his outlook for equities, talked about valuations relative to low current interest rates and his belief that rates are headed lower. He sees another 10% to 15% advance likely for U.S. equities and interest rates lower for longer. He may be right.

Jeremy Schwartz added that we haven’t seen a period when both bonds and stocks sold off together in a material way. Meaning 2.16% 10-year Treasury yields just can’t help diversify a portfolio as they did in years past. That is true.

You can find the Wharton Business Radio podcast interview here.

Congress established three key objectives for monetary policy in the Federal Reserve Act: maximizing employment, stabilizing prices, and moderating long-term interest rates. The first two objectives are sometimes referred to as the Federal Reserve’s dual mandate. With the employment objective met, we know that the Fed is focused on a 2% inflation target. (I’ve herd that the Fed would be happy with 3% inflation.)

We know what QE and zero interest rate policy has done for asset prices. Asset prices have inflated beautifully since the great recession. In simple terms, lowering interest rates has been good for stocks and bond returns. We are in a tightening cycle (Fed raising interest rates) that began in December 2015. Raising interest rates is generally bad for asset prices, as Dalio explained last week.

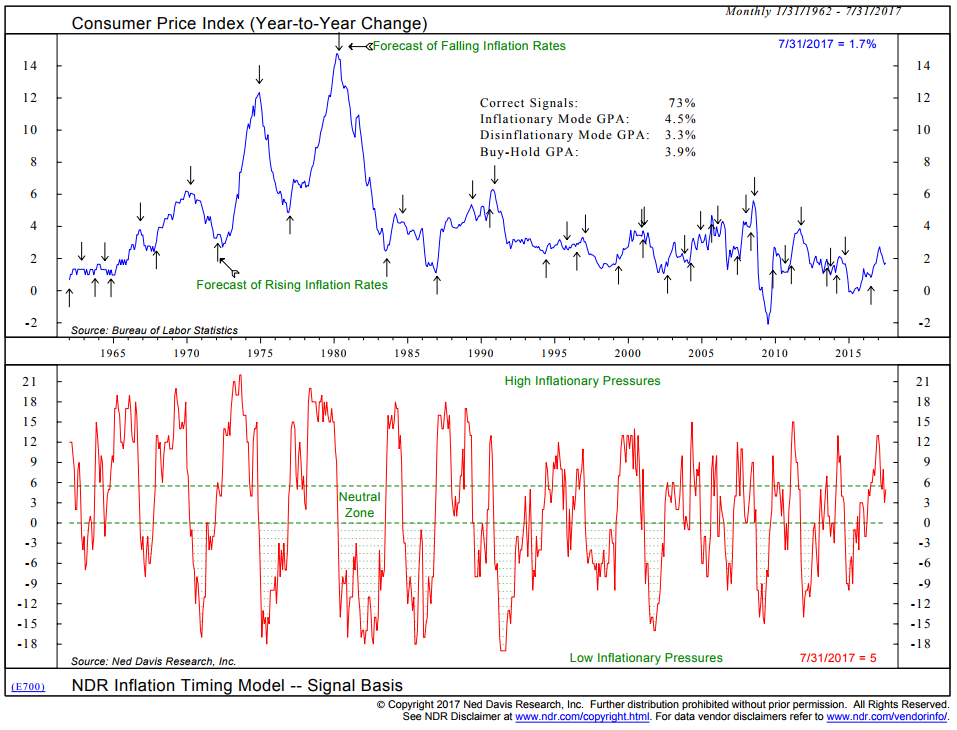

So it’s complicated, but there are important indicators we can watch. Since the Fed is targeting inflation, we can watch inflation to help us gauge their next move. My favorite inflation chart comes from Ned Davis Research (NDR). It is a model designed to signal inflation.

Here is how you read the chart:

- NDR’s Inflation Timing Model consists of 22 indicators that primarily measure the various rates of change of such indicators as commodity prices, consumer prices, producer prices, and industrial production.

- The model totals all the indicator readings and provides a score ranging from +22 (strong inflationary pressures) to -22 (strong disinflationary pressures).

- High inflationary pressures are signaled when the model rises to +6 or above. Low inflationary pressures are indicated when the model falls to zero or less.

- The bottom section (red line) details the model’s past and current reading of “5” as of 7-31-2017.

- NDR shows that economic growth, as measured by GDP, is stronger when the signal rises to +6 or above and slower when the signal falls to 0 or less.

I don’t use this indicator to tell me what GDP will be; I use it simply to measure inflationary pressures to determine what the Fed is likely to do. If there are high inflationary pressures, then they are likely to raise rates. If low, they will likely sit tight or lower rates. And since we are in a global economy and the U.S. is a significant part of global trade, I believe we can gain a lot by watching this chart.

Bottom line: right now it is telling us that inflationary pressures have rolled over from “High Inflationary Pressures” to the “Neutral Zone” (bottom section of chart, red line far right). However, the active signal, in place since mid-2016, is forecasting “Rising Inflation Rates.” This will likely keep the Fed on hold but leaning towards a rate increase in December. Stay tuned. I’ll continue to share this chart with you from time to time.

My overall two cents:

- The Fed is wed to the Phillips Curve. That’s why they’re raising interest rates and that’s where the policy mistakes that we’ve seen time and again is going to occur.

- We basically have never seen a situation going into a recession where measured rates of inflation and measured rates of nominal GDP growth were as low as they are today in any other prior situation.

- 10 of the 13 Fed tightening cycles since WWII have landed us in recession. Three have been soft landings. Global debt-to-GDP exceeds 325%. It’s 250% in the U.S. I believe this rate tightening cycle will land us in recession next year.

- But it’s not just the Fed. We must consider what the central bankers in Europe and Japan are doing as well. It will show up in inflation. It will show up in capital flows and those flows may flow to the U.S. Which is good for U.S. asset prices and economic expansion. So we need to keep our eyes on global capital flows.

The NDR Inflation Signal chart is a good tool. You can see what the Fed is looking at and why they began to raise rates. I can’t get that stellar post-WWII Fed/recession track record out of my mind. So we also watch for recession (you’ll find a few of my favorite recession watch charts below). Good news is recession remains at least six to nine months away.

As you’ll see in Trade Signals (link below), my favorite trend indicators remain bullish for both equities and bonds, but beware of August and September. August and September have been the two worst months of the year based on the mean monthly change during the past 29 years.

One last note on the mess in Washington. A client asked about the Trump trade and what I believe might happen given the leadership challenges Trump faces. I rarely talk about politics because I think Warren Buffett is right when he said, “If you mix your politics with your investment decisions, you’re making a big mistake.”

But I do wonder about the prospects for tax reform and whether the impressive market gains since the November election (the “Trump bump”) might be impacted should the Republicans fail to utilize the advantage that sits in their legislative hands. Congress must also act on the debt ceiling by October. Senator Mitch McConnell says there’s “zero chance” the U.S. fails to raise the debt ceiling.

I believe we should always be mindful of risk so keep one eye focused on growth and the other focused on capital preservation.

I hope you find this information helpful for you and your work with your clients. Grab that coffee and take a look at the charts below. And have a great weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- Charts of the Week — Recession Watch

- Trade Signals — August/September Seasonal Challenges Yet Trend Signals Bullish

- Personal Note

Charts of the Week — Recession Watch

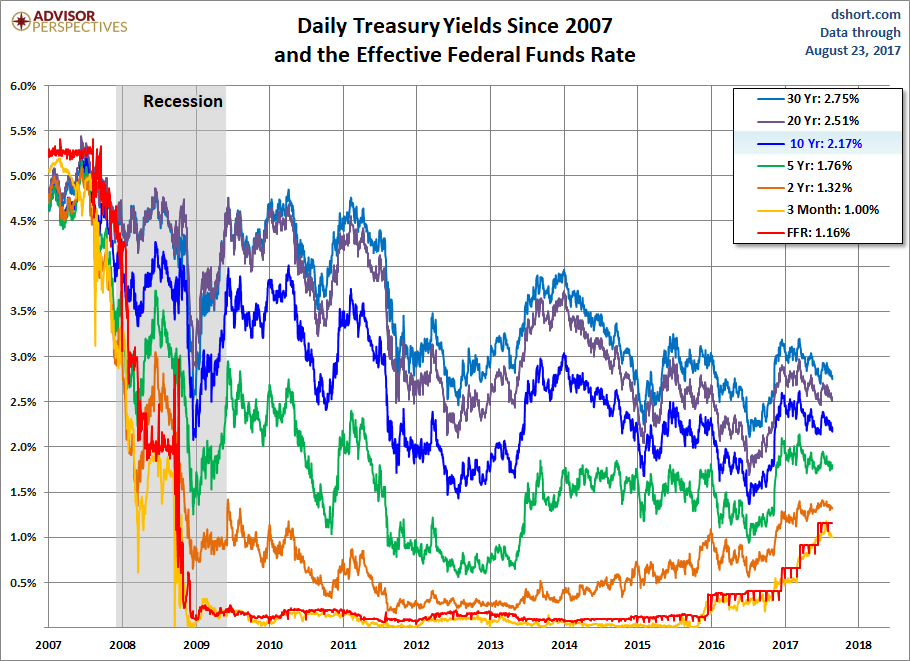

Charts 1 and 2: A Look at Treasury Yields Since 2007

The following charts show a snapshot of current yields from 2007 to present. The red line is the Fed Funds Rate. Note the movement from pre-recession levels in 2007 to zero interest rate policy coming out of the recession, to the move higher since December 2015 when the Fed began to raise rates.

One of the most accurate recession indicators (though past performance doesn’t guarantee future performance yet there are some tea leaves we must pay attention to) is the difference between the 10-year Treasury yield (currently 2.17%) and the 2-year Treasury yield (currently 1.32%).

Bottom line: it is currently 0.80% to the positive (the 10-year is yielding a higher yield than the 2-year). When it inverts or in other words goes negative, recession likely follows. So far, no sign of recession by this measure.

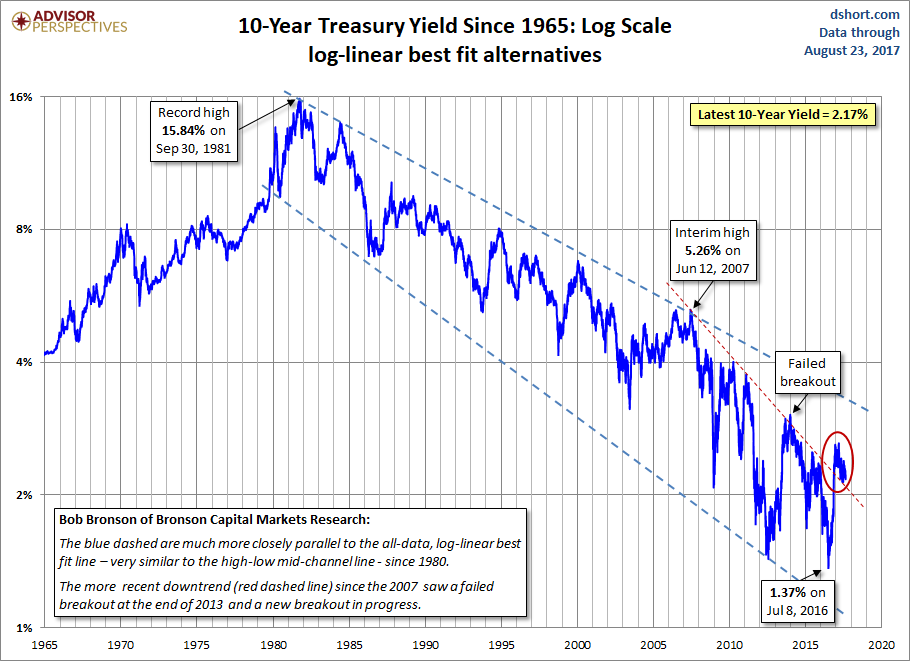

A Long-Term Look at the 10-Year Note Yield (1965 to Present)

A log-scale snapshot of the 10-year yield offers a more accurate view of the relative change over time. Here is a long look since 1965, starting well before the 1973 Oil Embargo that triggered the era of “stagflation” (economic stagnation with inflation). The blue trendlines connect the interim highs and lows following those stagflationary years. The red trendline starts in 2006, prior to the 2007 interim high and subsequent 2008 low. Note the 1987 closing high on the Friday before the notorious Black Monday market crash. The S&P 500 fell 5.16% that Friday and 20.47% on Black Monday.

Bottom line: 2.17% yields won’t do for you what 5.26% did for your portfolio. How about that 15.84% yield in 1981. The start of a great bull market for stocks and also for bonds. Then we had low valuations and ultra-high yields.

Today’s high valuations and low yields present us with a different opportunity. Expect low single-digit returns for equities and 2.17% from 10-year bond exposure.

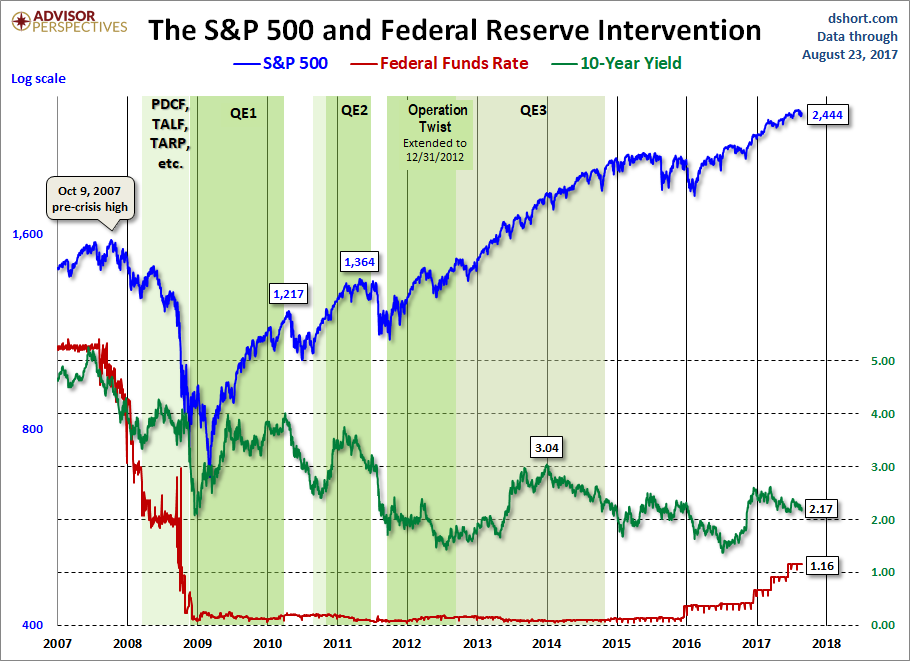

Chart 3: The S&P 500 Index and Federal Reserve Intervention

Here is how to read the chart:

- A simple reminder of the power of the Fed.

- More cookies please…

Bottom line:

- We just don’t yet know how the global central banks will respond to the next economic slowdown and/or next crisis.

- We don’t know how the other side of QE or Quantitative Tightening (“QT”) will look like.

- Keep your eye on the ECB, the JCB and the Fed.

- Keep your eye on legislative policy makers, i.e., what are the changes of a tax cut now? What about political unity in Europe? We just don’t yet know.

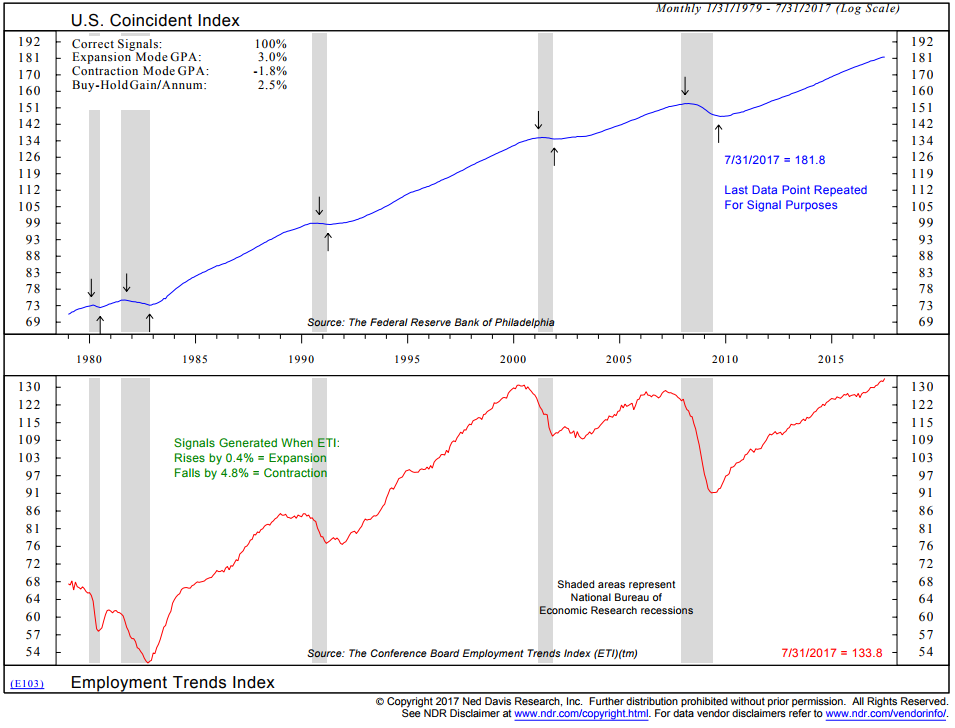

Charts 4, 5 and 6: My Favorite Recession Watch Charts

Here is how you read the chart:

- Up arrows signal expansion.

- Down arrows signal recession.

- 100% of past signals were correct signals.

- No current sign of recession.

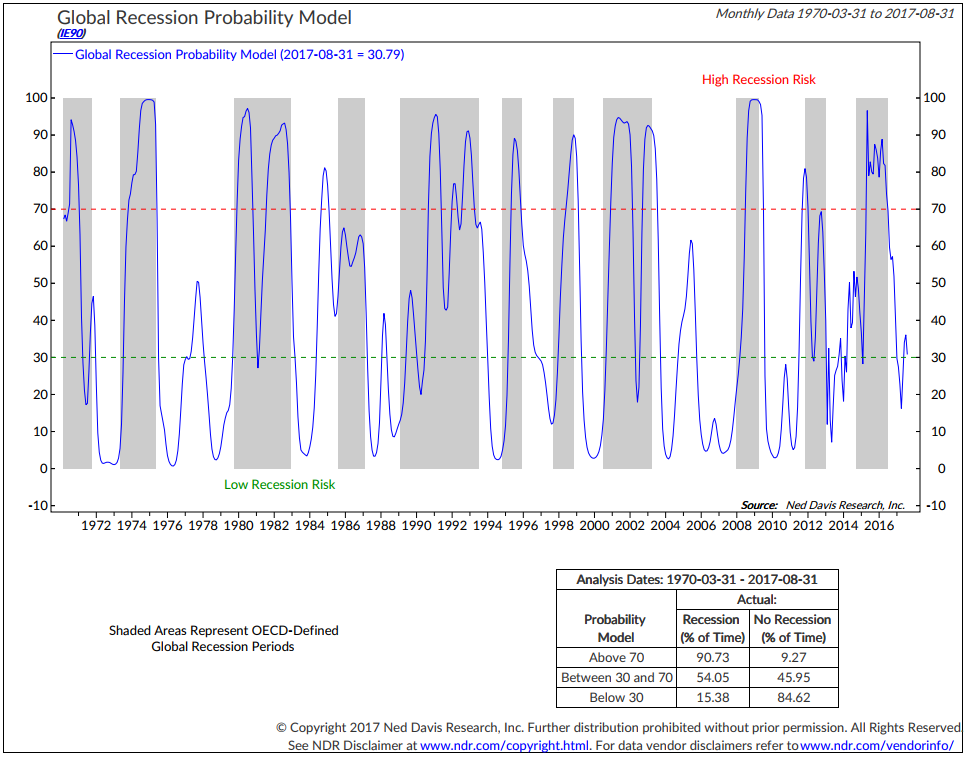

Chart 5 looks at the global economy. Here is how you read the next chart:

- High recession risk when the blue model line is above the dotted red line.

- Note the percentage of time recession has occurred when the model equity line was in each zone (data box bottom right of chart).

- Bottom line: modest global recession risk.

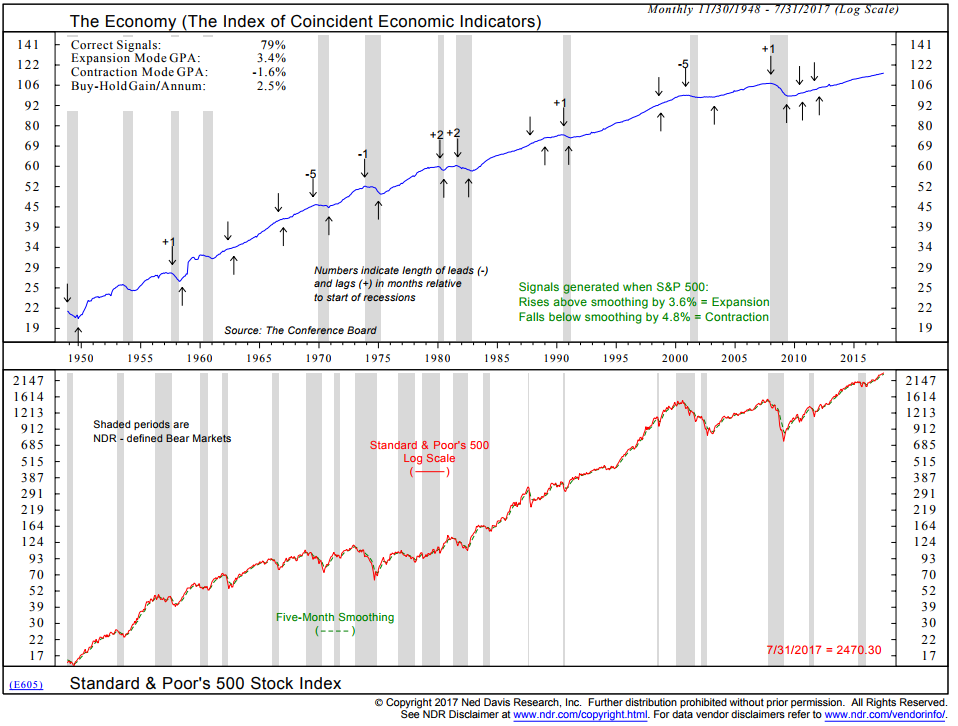

Chart 6 looks at the stock market as a leading economic indicator. One of my favorites.

Here is how you read the chart:

- When the S&P 500 Index moves above its 5-month smoothed moving average line by 3.6%, an economic expansion signal is generated.

- When it declines below its 5-month smoothing by 4.8%, an economic contraction signal is generated.

- Note the 79% correct signals.

- Note how well the down arrows have warned of recession (prior to or at the beginning of such periods).

- Not perfect but better to have a warning in advance than to get run ov

- er by the stock market declines that happen in recession.

- Bottom line: no current sign of recession.

Long-time readers know that I am a big fan of Ned Davis Research. I’ve been a client for years and value their service. If you’re interested in learning more about NDR, please call John P. Kornack Jr., Institutional Sales Manager, at (617) 279-4876. John’s email address is [email protected]. I am not compensated in any way by NDR. I’m just a big fan of their work.

Trade Signals — August/September Seasonal Challenges Yet Trend Signals Bullish

S&P 500 Index — 2,452 (8-23-2017)

Notable this week:

August and September have been the two worst months of the year based on the mean monthly change during the past 29 years. With global equities turning lower in recent days, we don’t think it’s time to take profits. The equity market uptrend remains in place as measured by the signals you see in this post. And, with the exception of the Fed, central banks remain friendly with real policy rates remaining negative.

No significant changes since last week’s post. Here is what I posted: As you’ll see in the following charts, the balance of evidence remains bullish for both equities, high quality fixed income and gold. Since last week’s post, our HY indicator has moved to a sell. I keep a close eye on HY, as junk bonds have historically been an early indicator for the trend in stocks and the economy. We typically get 4-5 signals a year.

I see no sign of recession over the next 6-9 months. Inflation remains a non-issue. The greatest risks are geopolitical (protectionism, trade, war), debt (specifically HY and foreign sovereign debt) and underfunded pensions (what will be required to fix the issue will be reduced benefits and higher taxes).

Given the developed world’s aging demographics, lower income and higher taxes are not good for economies. The risk of a 2018 recession is high. Yet for now, our recession watch indicators are signaling low recession risk and the overall trend evidence for stocks and high quality bonds remains bullish.

We continue to see a “risk on” positioning in the CMG Opportunistic All Asset Strategy with exposures favoring developed and emerging markets.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Click here for the latest Trade Signals.

Personal Note

The risks are asymmetric. Meaning raising rates will have a much greater impact on the markets than lower rates. QE is losing its punch. QT is the stronger opponent and the Fed is on that path.

While your clients may be looking at the last five years of stock market returns and projecting them forward, it’s important to understand what may happen to the market when the Fed reverses gear. To expect the same outcome is dangerous.

Dallas is up next on Monday. I’ll be attending the Morningstar ETF Conference on September 6 & 7 in Chicago and back to Dallas again for a Mauldin Solutions Advisor Meeting on September 20 & 21. To navigate the “Great Reset” period he sees ahead, John has combined four ETF strategists into one portfolio. We are privileged to be one of the four managers in his Mauldin Solutions Smart Core Strategy. The other managers are 3EDGE Asset Management (Steve Cucchiaro), Peak Capital Management and Tectonic Advisors.

All four managers will be presenting in Dallas in September and again in early October. If you are an advisor and interested in coming to Dallas to learn more, please send an email to [email protected]. You can also learn more here.

Wishing you a wonderful weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group