“Anything that has happened economically, has happened over and over again.”

– Ray Dalio

Founder, Bridgewater Associates, in Bloomberg Interview

My thinking is impatient and mostly critical as I sift through research each week. I’m sure my “get to the point” personality frustrates my co-workers and I’m sure at times my beautiful wife. It’s a personality flaw, I know; but hey, I’m just not sure any amount of therapy can help.

As I sift through research, my head clicks doesn’t matter, doesn’t matter… matters! Last week I wrote about Camp Kotok. There were some important “matters” moments. For example, there was an interesting moment when Bloomberg’s Mike McKee fired hard questions at the panel of economists and former Fed insiders.

Stress test very bright thinkers on stage with their peers and you get to watch their body language as you listen to their answers. Further, you get to watch the movements and facial expressions of others in the room. The panelists debated what the Fed will do next.

The most important takeaway from camp was confirmation of my view that the Fed, at the highest level, is heavily reliant on, if not married to, a limited equation called the Phillips Curve. The Fed’s goals are to keep employment strong and inflation in check.

The Phillips Curve is a single-equation empirical model, named after William Phillips, describing a historical inverse relationship between rates of unemployment and corresponding rates of inflation that result within an economy.

The Phillips Curve assumes that high levels of employment will pressure wages, increase incomes, increase spending and drive inflation higher. And that is true in the short-term debt (or business cycles) we move through over time, but is it always true? In my view, the answer is no.

I argued they need to consider where we are in terms of both the short-term and the long-term debt cycle. A retired senior Fed economist said to me, “Until someone comes up with a better model, it’s the best we’ve got.” At this moment in time, they are looking at the wrong thing. “Matters!”

Put “how the Fed will likely react” in the matters category. Put the Phillips Curve in the matters category simply because it is what the Fed is focused on and not because it is the right metric and put, as I mentioned last week, the understanding of short-term and long-term debt cycles and where we are within those cycles in the matters most category.

Bottom line: We sit at the end of a long-term debt cycle. One very few of us have ever seen before yet one that has happened many times over hundreds of years. The data exists. The Phillips Curve doesn’t see it.

I wrote last week, “… the Fed is Focused on the Obvious and the Unimportant.” That is important for us to know. But then, what should the central bankers and you and I be focused on? Let’s take a look at that today and see if we can gain a better understanding.

Meeting Bloomberg’s chief global economist Mike McKee at Camp Kotok was a real treat for me. If you have listened to Bloomberg radio over the years, you’ll know him as Tom Keene’s co-host. So how will the next few years play out? What does it mean in terms of the returns you are likely to receive? In the matters category, I believe this is what you and I need to know most.

Following are my abbreviated notes from a recent Keene-McKee-Ray Dalio video interview to better understand how the economic machine works and how Bridgewater uses this understanding to invest their clients’ money.

There are three main factors. There is productivity which produces income. You can spend at the end of the day what you earn. And what you earn is a function of your productivity. For a country it is the same as for individuals. You can be more productive if you work harder and you can be more productive if you are creative.

Over a short period of time you can spend more money than what you earn. That’s because we have debt. So we have debt cycles. There are two major debt cycles. There is a short-term debt cycle which we are used to (it’s called the business cycle). We have recession and the Fed eases. What they do is reduce interest rates and as a result, money and credit goes out into the system.

It first bids up asset prices and then the lower borrowing costs enable business to make items that are cheaper because interest rates go down… so we have that business cycle. When that cycle gets past a certain mid-point in the cycle, there is a tightening of monetary policy as you get to the later part of the cycle (Fed raises interest rates) as you start to have inflation. It then gets too tight and the economy starts to go down. And that’s the business cycle. We are all used to this cycle.

So when we look at every country, we can see where we are in that cycle. We are in the mid-part of that cycle and hence we are having the conversation we are having about the Federal Reserve.

And then there is a long-term debt cycle because these cycles add up. In a long-term debt cycle, imagine you start off with no debt. Think of low debt-GDP ratios. Say you’re earning $100,000 a year and you have no debt. You borrow $10,000 so you can spend $110,000. Your spending is somebody else’s income. They are earning more so they can spend more. And it becomes self-reinforcing until you get to the point where debts rise too high relative to the income (like a balance sheet, at some point you can’t borrow anymore because you owe too much relative to what you can make, your income).

Central banks, all central banks, are in the business of helping this process go along. They lower interest rates, and lower again until rates hit 0% and we then come to a dilemma. We reach an end of monetary policy as we traditionally have it and as a result, you can’t keep that cycle going.

At this point the Fed puts money into the system. There is a difference between debt and money. With debt, for example, you go into a store and buy a suit, you put down your credit card and you later have to pay back money to settle the transaction. So the central banks can’t create credit because we’ve reached a point of too much debt so they put money in the system. They do this by buying financial assets.

When they buy bonds, the seller of those bonds takes the cash and he does something else with that cash. As a result of this, it causes longer-term yields to fall as the buying drives asset prices to rise.

So there are three equilibriums we have longer term:

1. The first equilibrium is debt can’t rise faster than your income for long.

2. The second equilibrium is that the operating rate in the economy can’t be too loose or too tight.

3. The third equilibrium is that in the capital markets structure. In other words, cash is going to have a lower yield than bonds which is going to have a lower return than equities and so on.

And there is an equilibrium that keeps working itself through this system and monetary and fiscal policy are the tools we use as we work through short-term and long-term debt cycles.

Tom Keene asks, “…we’ve enjoyed the last seven years. Where are we now within that equilibrium?” Dalio answered,

The United States is in the mid-point of its short-term debt cycle so as a result central banks are talking about whether we should tighten or not. That’s what central banks do in the middle of the short-term cycle and we are near the end of a long-term debt cycle. (Emphasis mine.)

- You have interest rates going to zero. You have spreads that have come down (spreads are the difference between the yield you get on short-term bonds vs. the yield you get on long-term bonds).

- So spreads that have come down mean that asset prices have gone up.

- So now the expected return of asset classes (cash, stocks, bonds) are all very low.

- We know that 1-year Treasury bonds are 2.25%. So you know that’s what you are going to get for the next ten years.

- The equity price premiums look like 3½% or 4%.

- So all of the asset classes now are aligned (returns on cash, fixed income and equities). As is normally the case.

- If interest rates rise, then it will cause all of those assets to decline in value.

Tom Keene asks, “Within the framework of your economic machine, do you presume a jump condition (a jump up in rates) as central banks come out of this or can they manage it with smooth glide paths?” Ray answered,

I don’t believe they can raise rates faster than is discounted in the curve. In other words, the rate at which it is discounted to rise which is built into the interest rate curve (the curve is the different yields you get for short-term Treasury Bills to long-term Treasury Bonds). This is built into all asset prices.

So if you raise rates much more than is discounted in the curve, I think that is going to cause asset prices to go down. Because all things being equal, all assets sell at the present value of discounted cash flow. All assets are subject to this so if you raise rates faster than what is discounted in the curve, all things being equal, it will produce a downward pressure on all asset prices.

And that’s a dangerous situation because the capacity of the central banks to ease has never been less in our lifetimes. So we have a very limited ability of central banks to be effective in easing monetary policy.

Mike McKee asks, “What does a central bank do when you are at the end of a long-term debt cycle? When the Fed is at the zero bound (meaning a Fed Funds rate yielding 0%)?”

Ray believes the pressure on the central banks will be on easing monetary policy (lowering rates) vs. tightening (raising rates).

Ray said, “We are in an asymmetrical world where the risks of raising rates is far greater than lowering rates (this is due to where we sit in the long-term debt cycle including emerging market U.S. dollar denominated debt, commodity producing dollar denominated debts, Japan, Europe and China debts relative to GDP or their collective income).”

Meaning if you raise rates, it affects the dollar and it affects foreign dollar dominated debt. So the risks on the downside are totally different than the risks on the upside.

Ray suggests that the next big Fed move will be to ease and provide more QE.

McKee asks, “Do you think QE works anymore?”

Ray said, “It will work a lot less than it did last time. Just like each time it worked a lot less.” He’s saying we can’t have a big rate rise because of the amount of debt, because of what it will do to the dollar, because of the disinflation it will cause and we will have a downturn.

And the downturn should be particularly concerning because we don’t have the same return potential with asset prices richly priced, so each series of QE cannot provide the same bump. You reach a point where QE is simply pushing on a string. You get nothing.

McKee asked if we are there yet.

Ray responded, “No, we are not there yet, but we are close. Some countries are there. Europe is there. What are you going to buy in a negative interest rate world? Japan is there. The effectiveness of monetary policy then comes through the currency (SB here: currency devaluation makes your goods cheaper to buy than my goods).”

(SB here: QE creates money out of thin air and central banks use that money to buy assets. That money buys bonds from you and you then have money in your account to put to work. What will you then buy? Which country might you choose to invest?)

Ray said, “If you look at us (the U.S.), we have very high rates in comparison to those in Europe and Japan. So it comes through the currency. If you can’t have interest rate moves (like in Europe) it comes through the currency.” Countries need to get their currencies lower to compete and drive growth. Can you see the mess that debt gets us into and the challenges reached at the end of long-term debt cycles?)

I’m going to conclude my notes from the Bloomberg interview with this last comment from Ray:

If you can’t have interest rate moves, you’ve got to have currency moves. And that’s the environment we are in.

You’ll find the full interview below.

OK, my friend, I believe the Fed should be studying history. As I mentioned last week, they do talk with the likes of Bridgewater but it stops short of the top. I believe the Fed should be looking at what happens at periods in time when debt had reached, like today, ridiculous debt-to-GDP levels. That’s the road map. That’s the seminal issue. There are other important issues, of course, but I believe this one matters most. What I gained from my time at Camp Kotok was that the Fed is not reviewing history. They are not considering the dynamics of were we are in the long-term debt cycle. They are wed to the Phillips Curve. “Matters!”

How we reset the debt via a combination of monetary policy and fiscal policy will dictate a beautiful or ugly outcome. Risks are high because asset prices are significantly overvalued. Participate yes but have processes in place that protect. I believe the U.S. looks most favorable relative to the rest of the world and we will likely see more QE. I believe the Phillips Curve and the Fed’s desire to normalize rates (to put them in a better position to deal with the next cycle) will prove to be a mistake. As Ray said, “The risks are asymmetric.” The current rate hike period will be halted and more QE will follow.

What happens between now and then? Don’t know. I suspect a shock followed by more global QE. The current state favors a stronger dollar and a strong U.S. equity market especially if there is a sovereign debt crisis in Europe. So yep… there’s that. Participate and protect and tighten your seat belt. Likely to be bumpy.

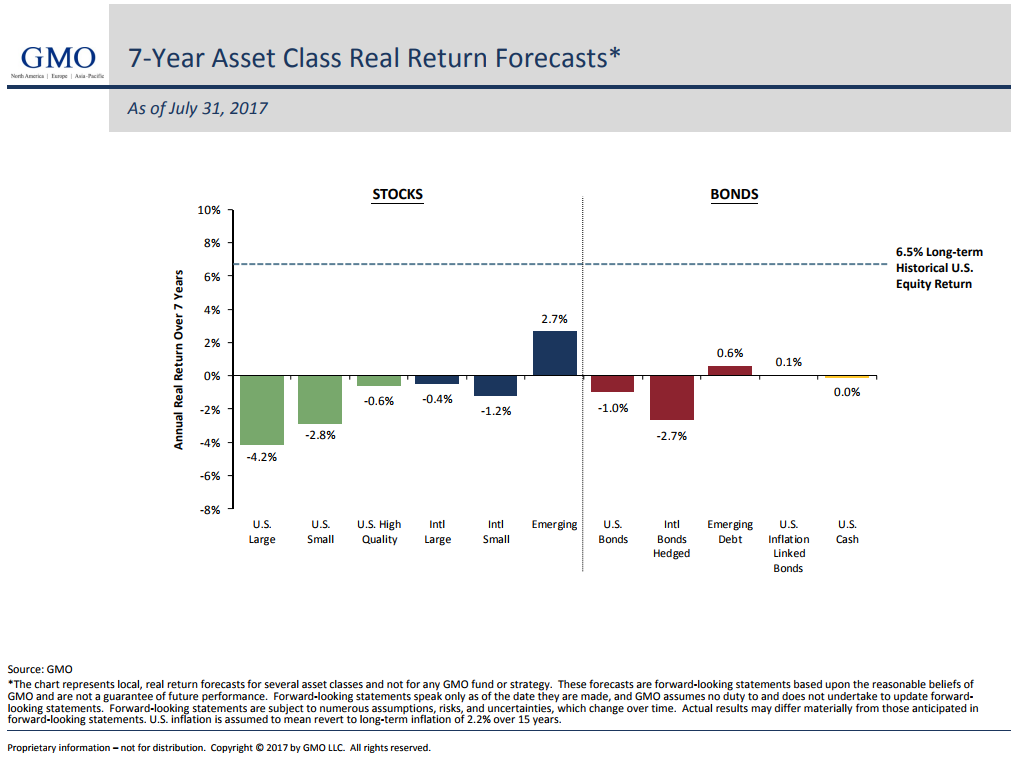

Grab a coffee. There was a great piece from GMO titled, “The S&P 500: Just Say No.” It highlights how GMO comes to their 7-Year Real Asset Return Forecast. One that is currently predicting a -4.20% annualized real return over the coming seven years. As in a loss of nearly 4% per year. If true, expect every $100,000 of your wealth to equal $70,945 seven years from now. Ultimately, valuations do matter. So yep… that too.

GMO has posted its forecast for many years. It is updated monthly. The accuracy rate has been excellent. Meaning the correlation to what they predicted to what returns turned out to be is very high. Not a guarantee, but put it too on your matters list. You can follow it here.

You’ll find a few interesting charts. Thanks for reading. I hope you find this information helpful for you and your work with your clients. Have a great weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- “The S&P 500: Just Say No”

- Charts of the Week

- Trade Signals — August 16, 2017

- Personal Note

“The S&P 500: Just Say No”

Each month I share with you my favorite valuation charts. They can tell us little about timing tops and bottoms, but they can tell us a great deal about coming forward returns.

James Montier from GMO along with his colleague, Matt Kadnar, put out an excellent piece this week. They explain how GMO gets to the -4.2% annualized real return forecast for U.S. Large Cap stocks.

With everyone herding into passive index funds, James and Matt begin by addressing what you are probably hearing from your clients. “U.S. stocks have outperformed for the last number of years, so I see no reason why that should not continue.”

Yes, but not likely. Here is a look at their forward return estimates for various asset classes.

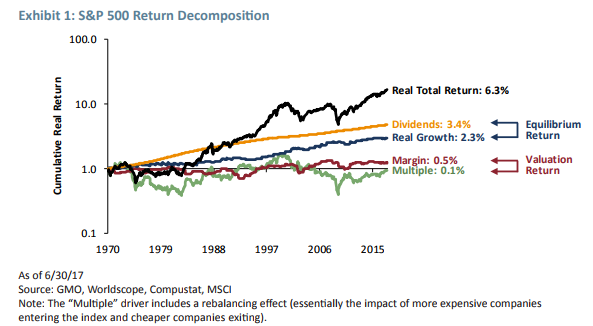

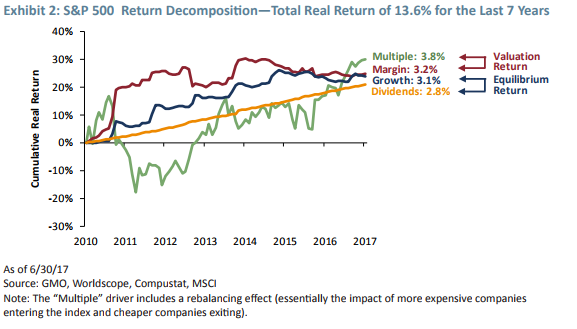

I particularly like how they decomposed returns and then show what the return drivers have been over the last seven years. Simply, don’t expect a repeat from here. Expect a reversion back to the mean. They conclude, expect -4.20% per year for seven years.

They conclude: If earnings and dividends are remarkably stable (and they are), to believe that the S&P 500 will continue delivering the wonderful returns we have experienced over the last seven years is to believe that P/Es and margins will continue to expand just as they have over the last seven years. The historical record for this assumption is quite thin, to put it kindly. It is remarkably easy to assume that the recent past should continue indefinitely, but it is an extremely dangerous assumption when it comes to asset markets. Particularly expensive ones, as the S&P 500 appears to be.

I encourage you to read (and show your clients) the full piece. You can find it here.

Charts of the Week

Just a few charts of interest to share.

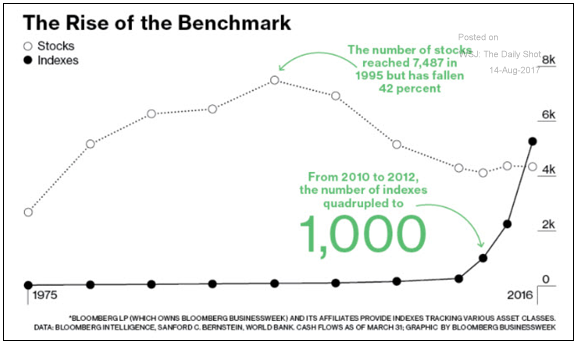

Chart 1:

There are now more index benchmarks than there are stocks. A passive index bubble? It sure looks like one to me.

Source: The Daily Shot, Bloomberg.com, Skënderbeg Alternative Investments. (Full article)

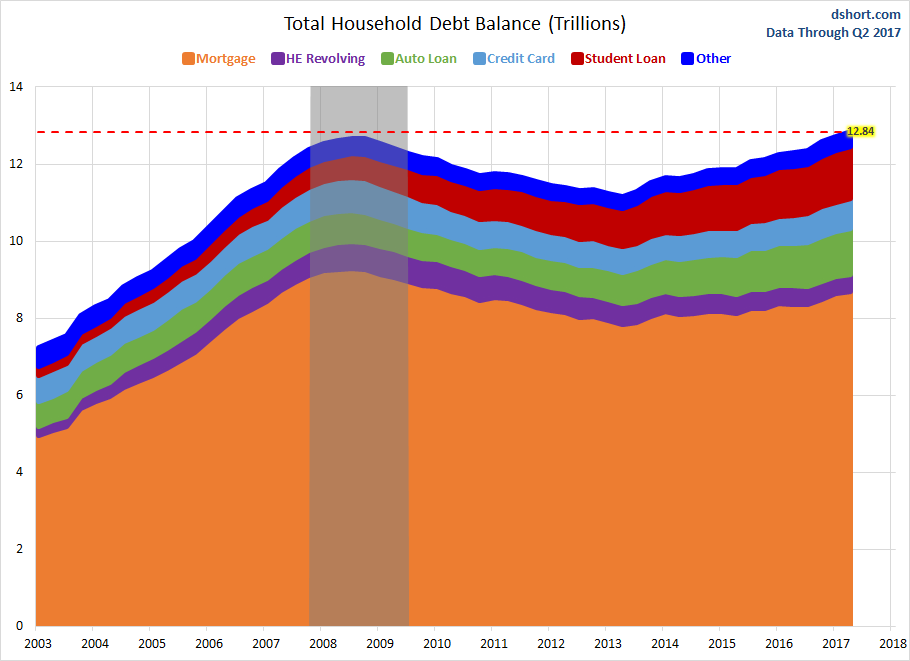

Chart 2: Deja vu all over again – Consumer Debt Exceeds 2008 High

Here is how to read the chart:

- The chart below shows total debt balance nationwide by composition in trillions of dollars. The current total is $12.84T, well exceeding the 2008 peak. Notice that even though the current Total Household Debt is greater than its 2008 high, mortgage debt is still currently lower than during the recession.

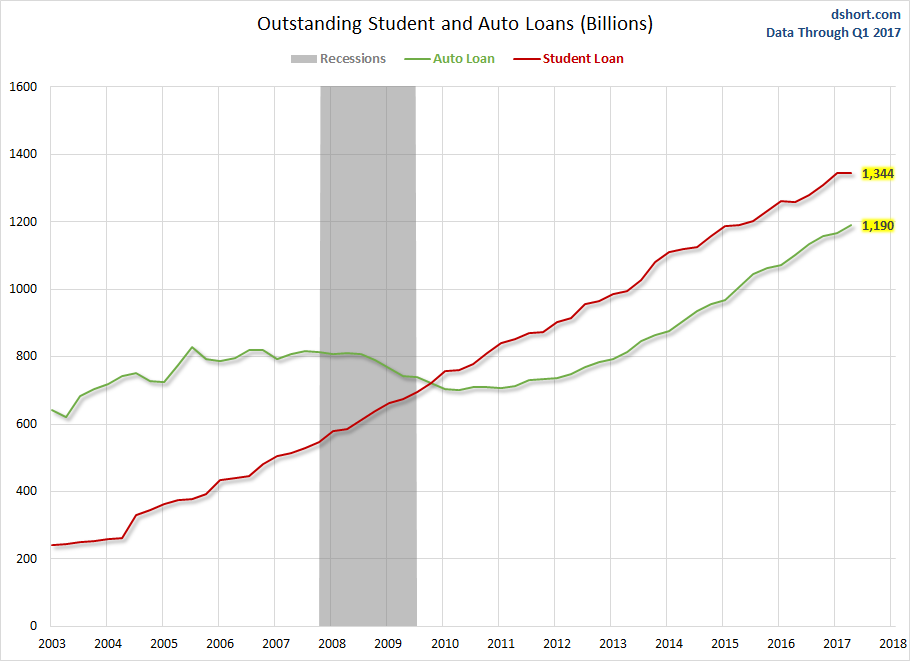

Chart 3: Student Loans and Auto Debt

The next chart drills down into student loan debt and auto loans. It’s no surprise the Student Loans have been on the rise.

Source: Advisors Perspectives – Jill Mislinski, 8/15/17

Trade Signals — Cyclical Trend, Daily Investor Sentiment, Zweig Bond Model, Gold Signals Bullish

S&P 500 Index — 2,469 (8-16-2017)

Notable this week:

As you’ll see in this week’s charts, the balance of evidence remains bullish for both equities, high quality fixed income and gold. Since last week’s post, our HY indicator has moved to a sell. I keep a close eye on HY, as junk bonds have historically been an early indicator for the trend in stocks and the economy. We typically get 4-5 signals a year.

I see no sign of recession over the next 6-9 months. Inflation remains a non-issue. The greatest risks are geopolitical (protectionism, trade, war), debt (specifically HY and foreign sovereign debt) and underfunded pensions (what will be required to fix the issue will be reduced benefits and higher taxes).

Given the developed world’s aging demographics, lower income and higher taxes are not good for economies. The risk of a 2018 recession is high. Yet for now, our recession watch indicators are signaling low recession risk and the overall trend evidence for stocks and high quality bonds remains bullish.

We continue to see a “risk on” positioning in the CMG Opportunistic All Asset Strategy with exposures favoring developed and emerging markets.

Click here for the current Trade Signals.

Personal Note

As a quick aside, you can follow @RayDalio on Twitter and read his “Observations” in LinkedIn. Here is link to a recent tweet. Click on it to read the “Risks Are Rising While Low Risks Are Discounted:”

I use Twitter to send out links to what I feel “matters.” Of course, no guarantees. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn here.

This past week was full of mixed emotions. I lost my brother to a heart attack. We are all shocked and numb. My brother was smart with a witty, fun sense of humor. We are celebrating his life on Monday. He leaves behind the most important person in his life, his daughter, Ashley. I pray my Mom and Dad are holding him.

The high for the week was golf Wednesday afternoon with two business partners, Adam (CMG’s head trader) and my son, Matt. Personally, I needed the distraction. Though I did lose another $15 to Matt. A 10-foot par save followed by two consecutive birdies sunk the old man. Two down with one to play. Birdies are worth $5 extra each. It was nice to be with friends and my son. Four of the five of us were rooting for Matt. I was happy to add more money to the “Matt continues to beat dad” fund.

Susan’s mother is coming to visit next week. We are really looking forward to that. She is an avid golfer so I may try to sneak away from work and get out to Stonewall. That will be fun. She’s an awesome Grandma!

Thanks for reading. Hug your family… I’ll be holding a glass high and toasting my brother. Welcome home, Mike. You are loved.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group