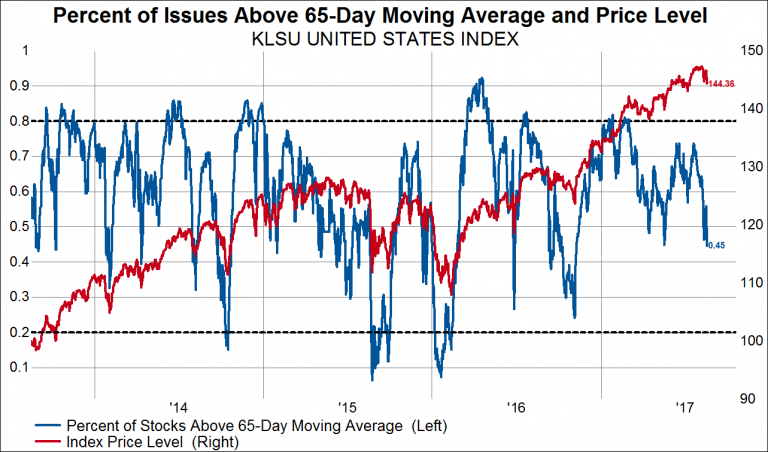

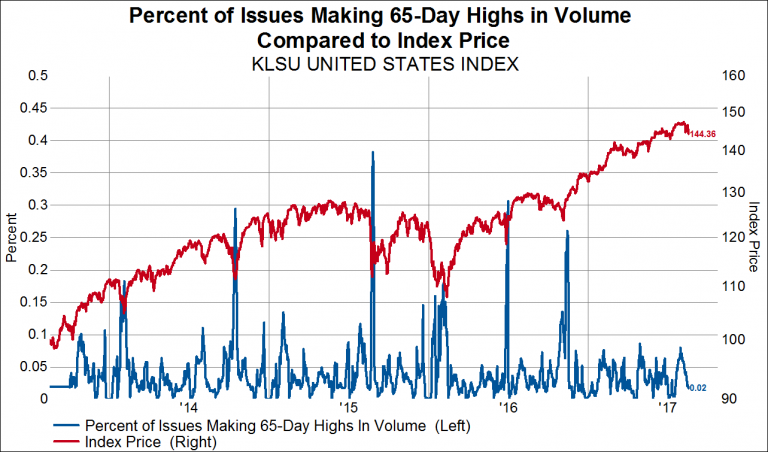

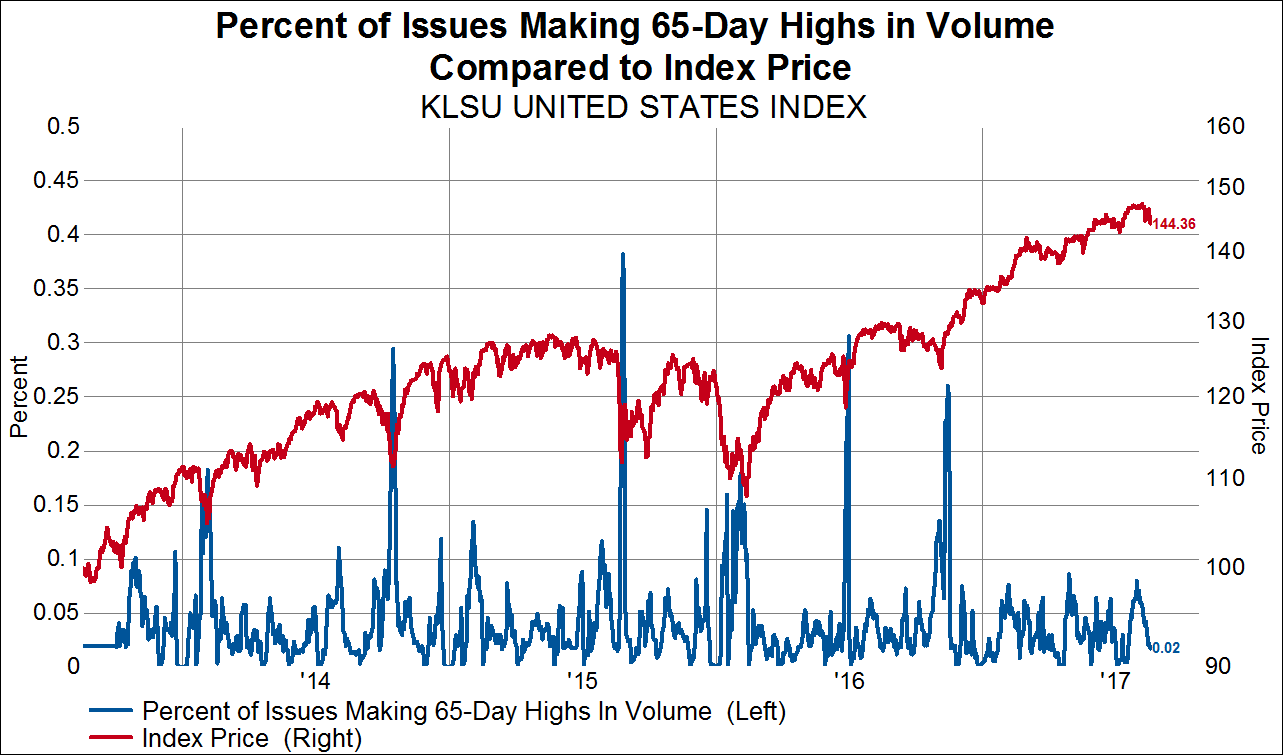

A Mini-Correction, but No Capitulation (Yet): Three Internal Indicators that Should Point to the Nex

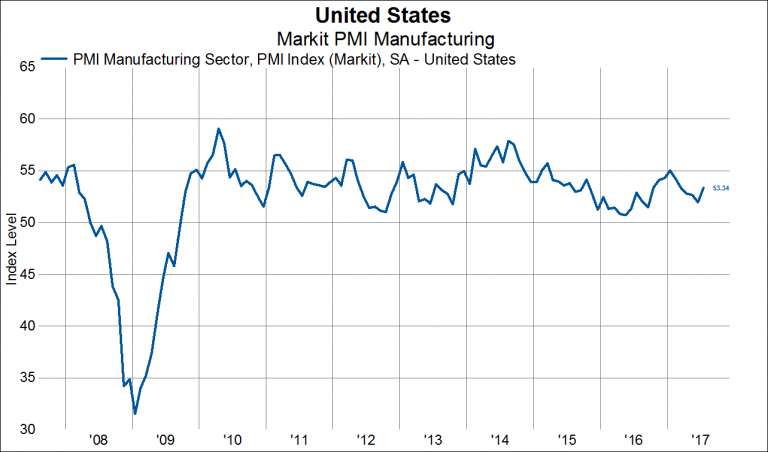

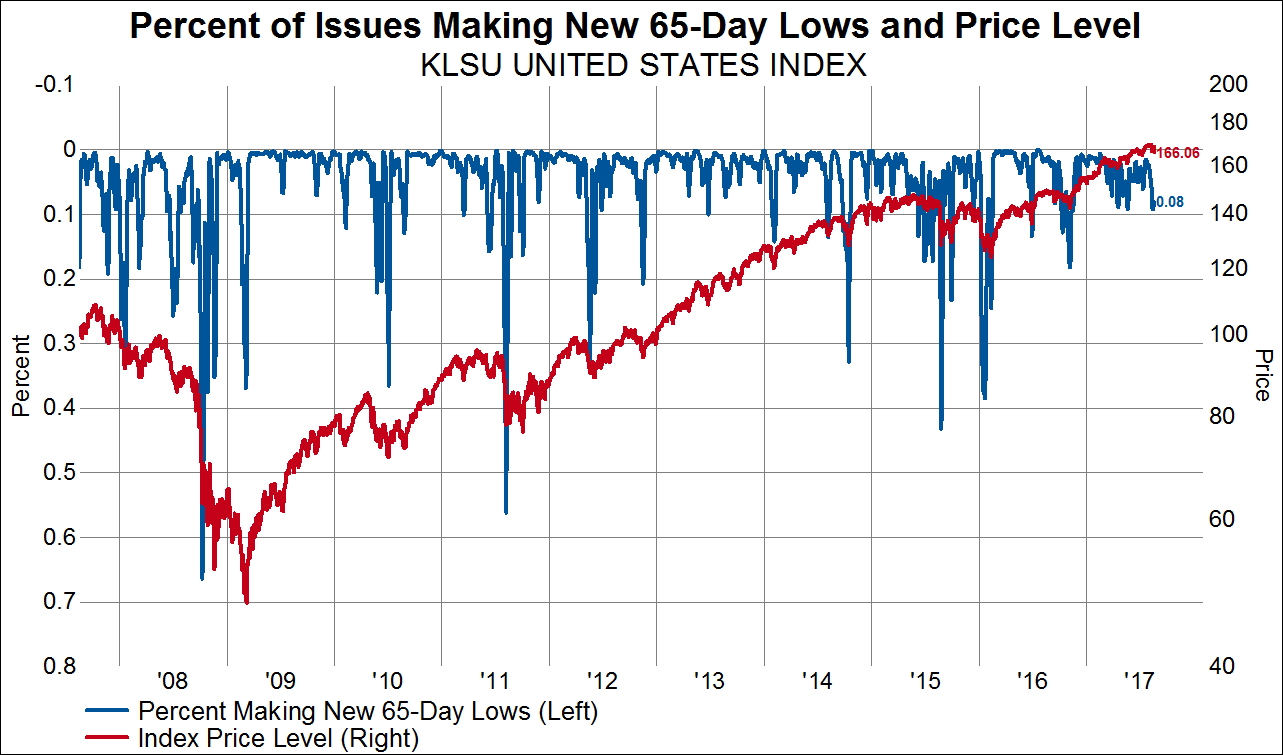

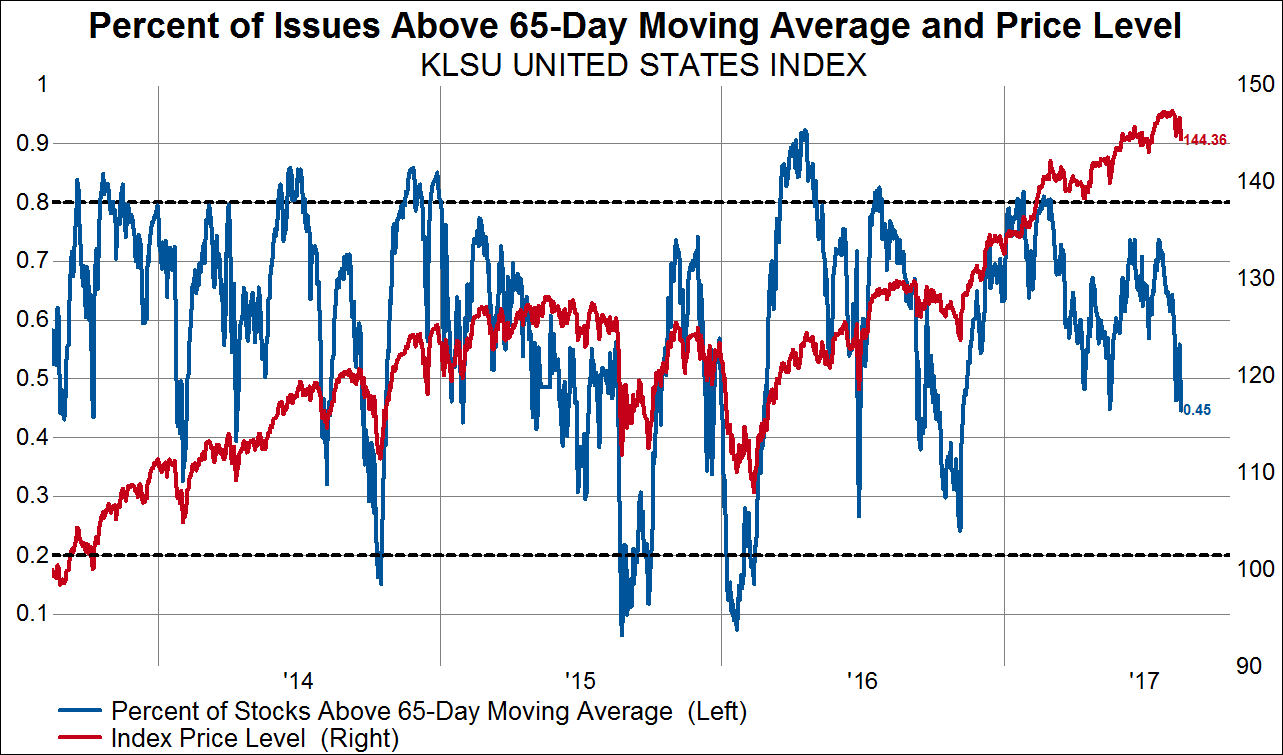

The last week has witnessed the return of multi-directional volatility in the equity markets for the first time since just before the election in the United States last November. At this point we have little reason to suspect the 2% mini correction in the S&P 500 will turn into a major downside swoon. After all, even though domestic and global politics remain unpredictable, high frequency economic indicators such as unemployment claims, consumer confidence, retail sales, and PMIs remain moderately strong and suggest the 2% real economic growth environment continues (charts 1-4 below). Furthermore, the loosening of financial conditions manifested through a weaker USD, falling rates, and contracting credit spreads should act as a boon to PMIs throughout the remainder of 2017. Even so, we wouldn’t be surprised in the least to see this correction go deeper to wash out some of the excessive optimism in the market. In this post we’ll highlight some of the things we’ll be watching for to help us gauge if market participants have capitulated, which would create an oversold condition to setup the next leg of this bull market.