No Matter How You Slice It, the Crude Oil Market is Coming into Balance

As the title suggests, any way we slice the data, it appears that the crude oil market is coming into balance to a greater extent than is generally recognized. This has broad asset allocation implications.

There are two basic ways we look at balance in the oil market: 1) purely from a supply standpoint, and 2) incorporating demand into the supply picture.

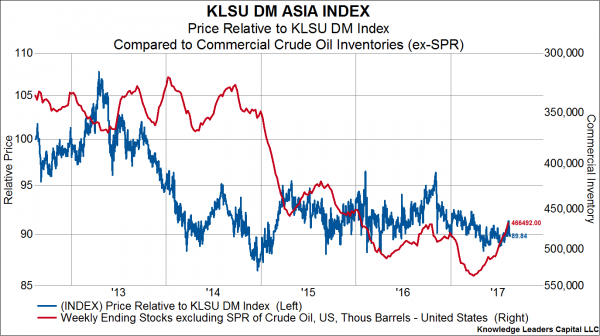

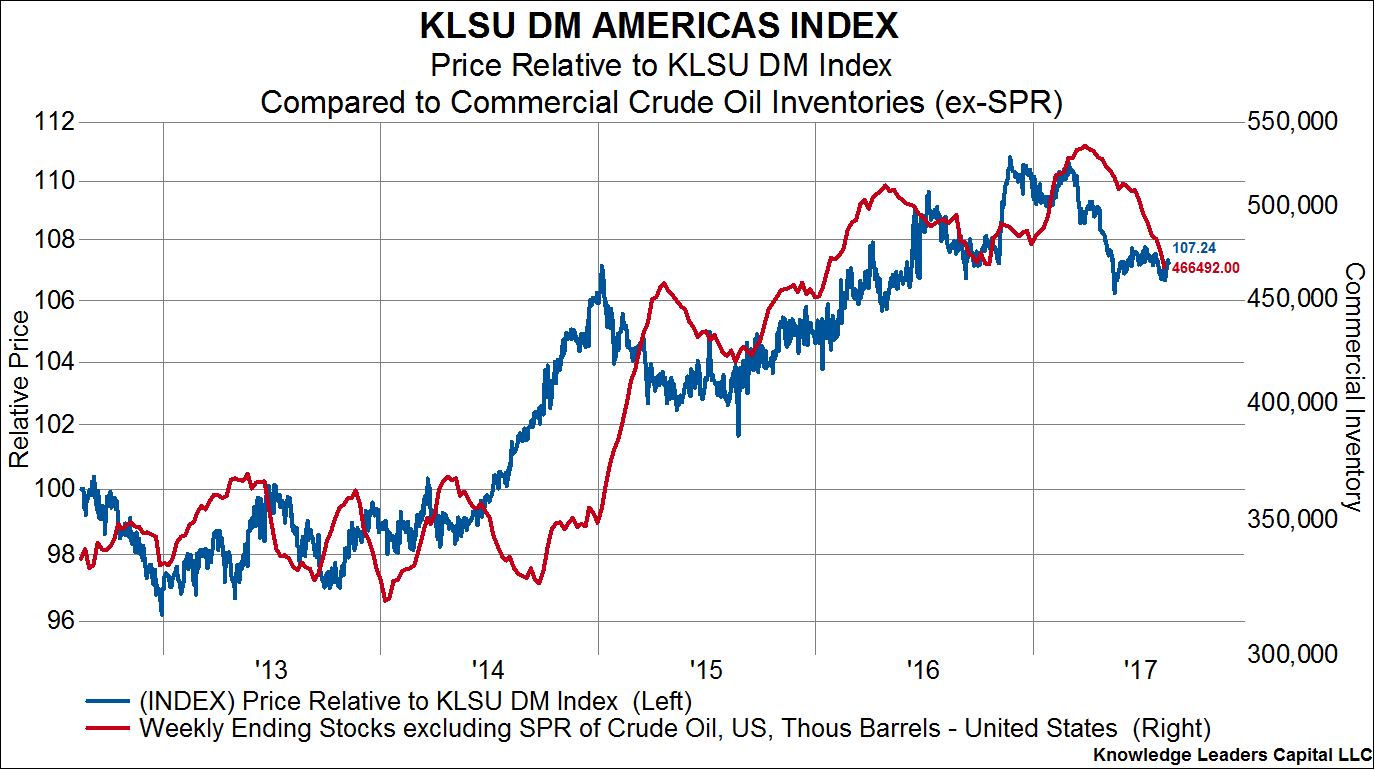

Let’s start with the commercial crude inventories as a pure measure of supply. Yesterday, the EIA reported that US commercial crude stocks fell to 466.49 million barrels. This is the first year-over-year decrease in crude stocks since January 2014. In the chart below, I overlay US commercial crude stocks (right scale) on the relative performance of our KLSU DM Americas Index (in USD) compared to the KLSU DM World Index (USD). As can be seen below, the relative performance of North American stocks has been highly correlated with crude oil supplies. A continued drop in supplies should correlate with the continued underperformance of North American equities.

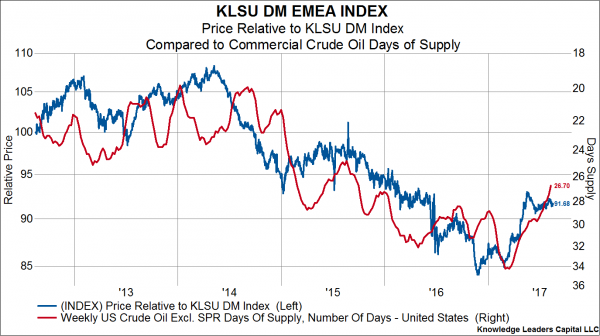

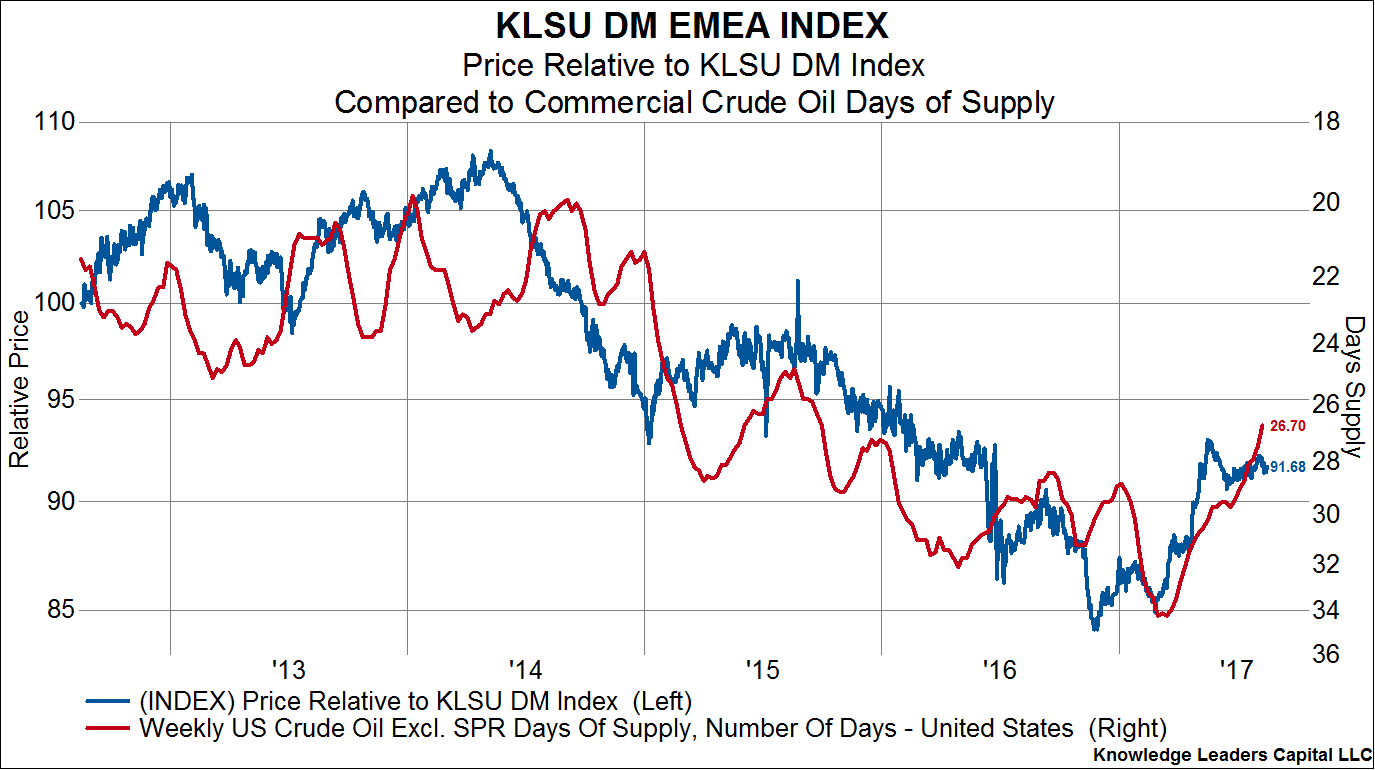

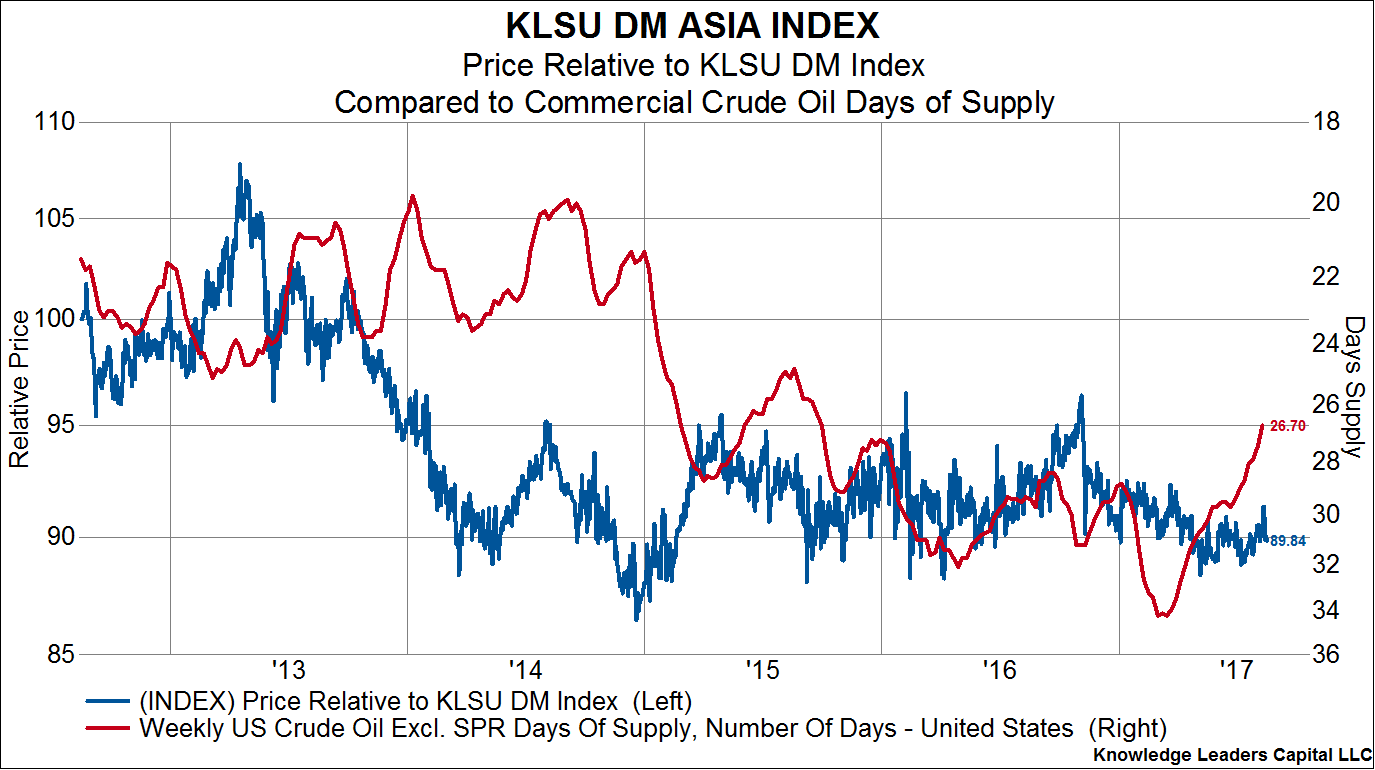

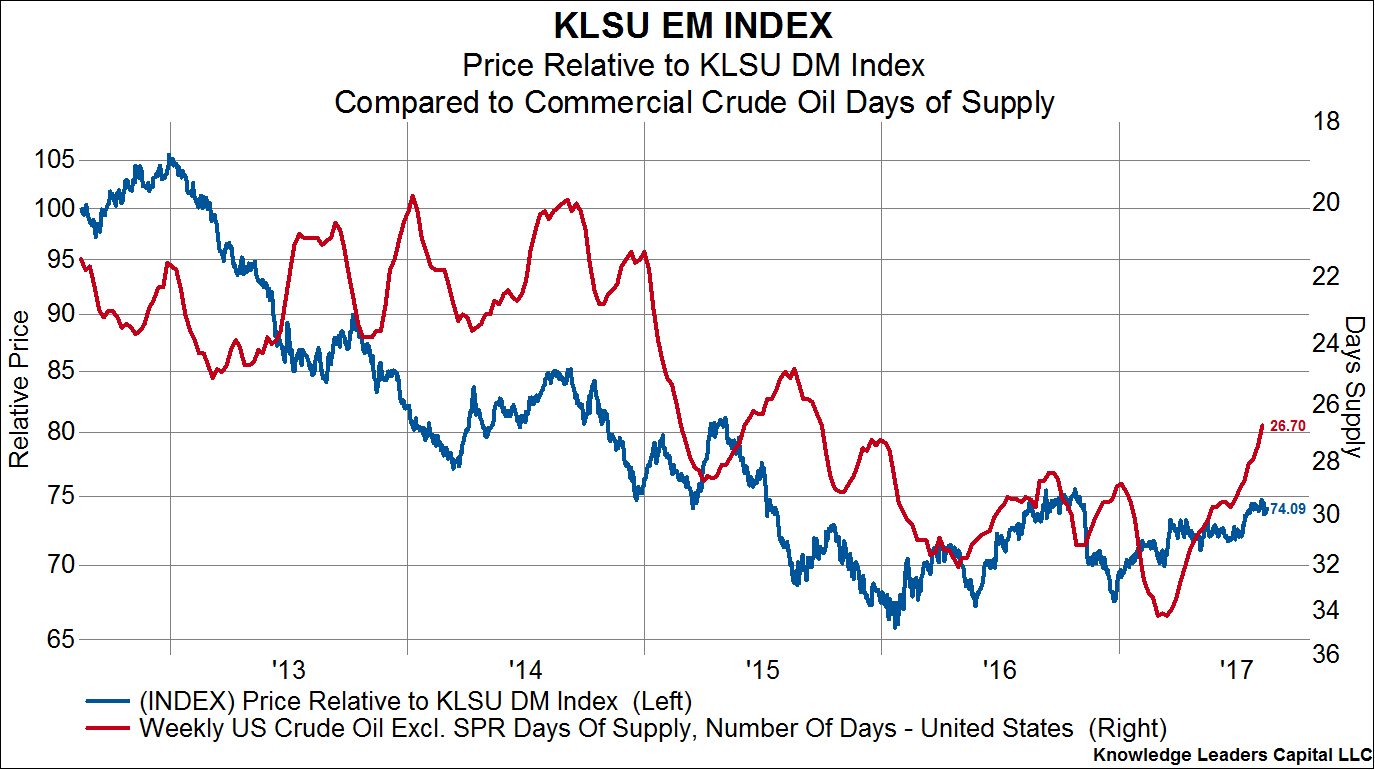

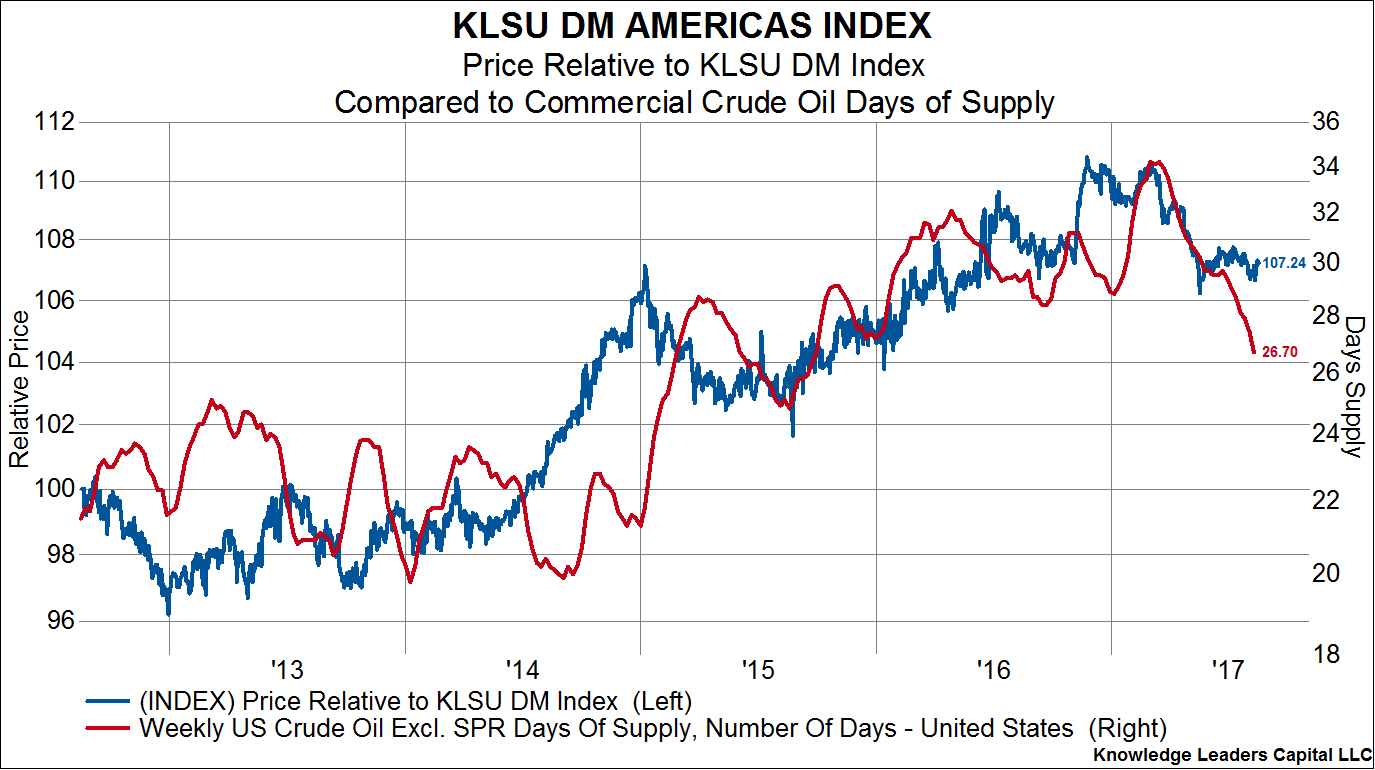

Next, incorporating demand into the equation, we look at the EIA’s measure of days of supply of crude oil. Since beginning the year over 34 days of supply, we are now under 27 days. In the chart below I overlay crude days of supply (ex. SPR) on the relative performance of North American equities. Here again, we are experiencing the first year-over-year drop in days of supply since January 2014. These shrinking inventory figures again suggest another period of underperformance by US equities broadly.

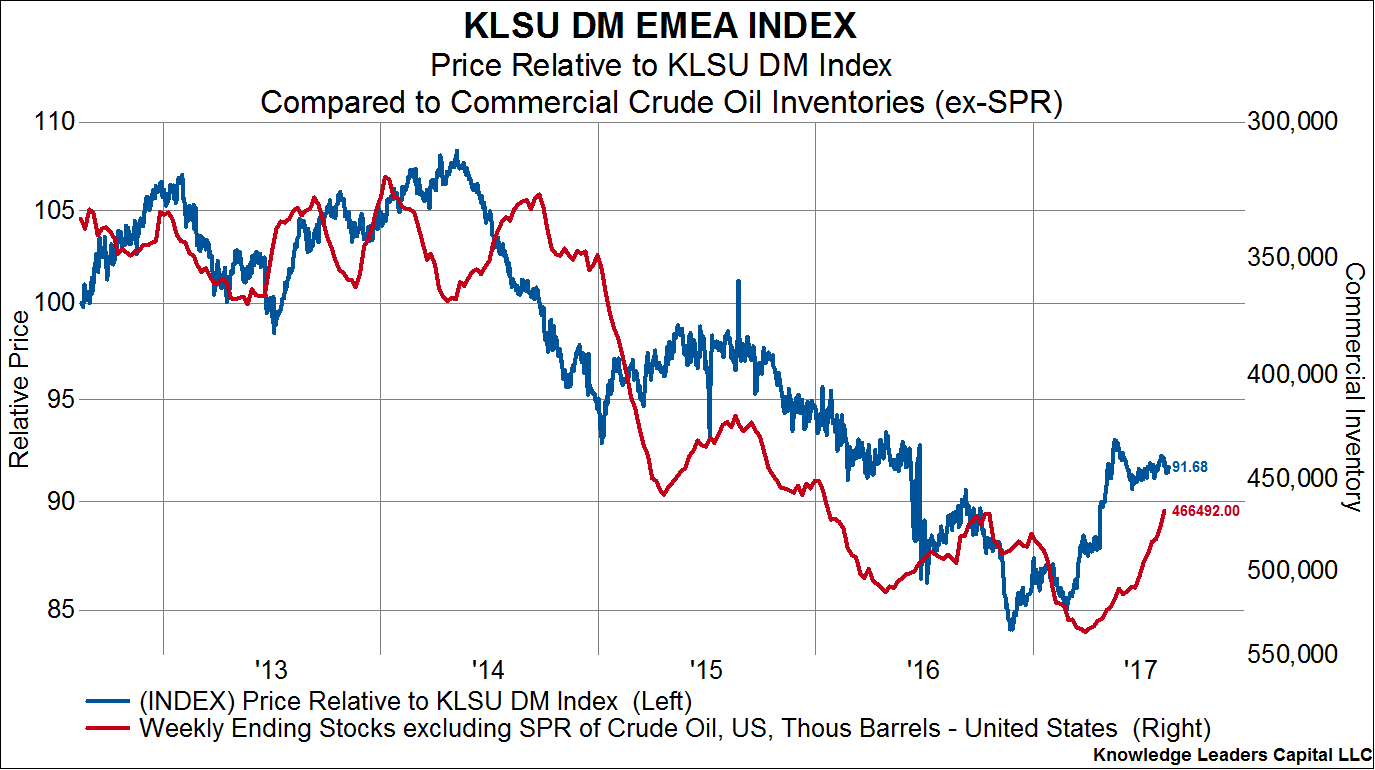

The flip side of this equation is what these shrinking energy inventories mean for foreign stocks. Let’s start with Europe. As can be seen below, where we invert the inventory data (right axis), the relative performance of European equities is negatively correlated with inventories; so, if crude supplies continue to fall, we would expect Europe to continue to outperform.