The July CPI data were a bit softer than anticipated, due partly to a drop in the price index for lodging away from home. Granted, if you exclude everything that went down, the CPI always looks higher, but the underlying trend is not far from the Fed’s earlier expectations (of a gradual move toward the 2% goal). The Fed is more focused on future inflation than past inflation. How the new normal fits into the inflation outlook ought to be a primary consideration for Fed policy.

Inflation figures are often uneven over the course of a year. Higher numbers in January and February led to calls that the Fed had “fallen behind the curve.” The more recent soft figures have led to calls that the Fed has overdone it. Go figure.

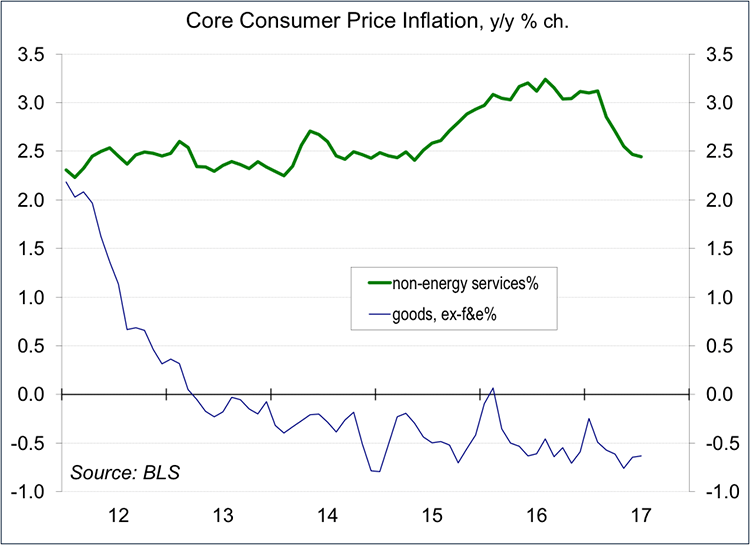

Diving into the details, one sees some odd things. Ex-food & energy, the price index for consumer goods (18.9% of the CPI) is still showing a trend of mild deflation (-0.6% y/y). Inflation in non-energy services, buoyed over the last year by rising rents, appears to have moderated somewhat.

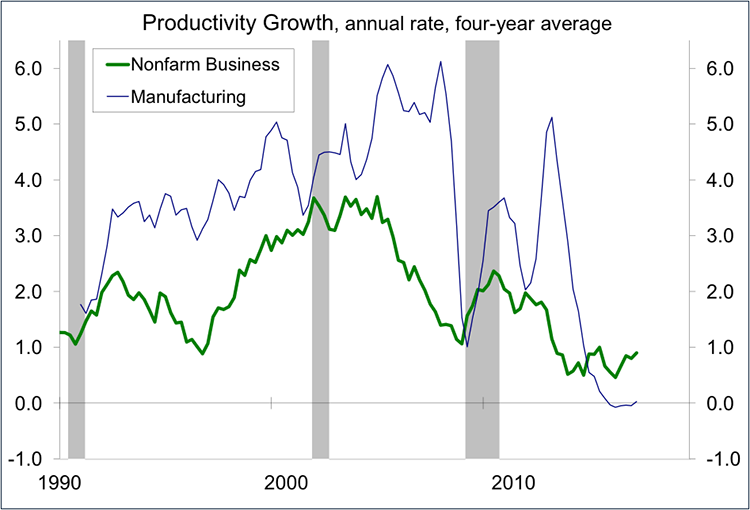

Inflation in services is thought to be driven more by labor costs, but wage growth has been moderate. Note that there is a chicken-or-egg component here. Firms typically peg annual wage gains to the CPI. Firms generally complain that they can’t find qualified workers. A simple solution would be to offer better wages, but that may mean paying more to those already on the payroll. One possible explanation for slow wage growth is the low trend in productivity. Quarterly figures bounce around, but the noise washes out over longer trends. Over the last four years, productivity growth has averaged 0.9% per year for nonfarm business and 0.0% for manufacturing.

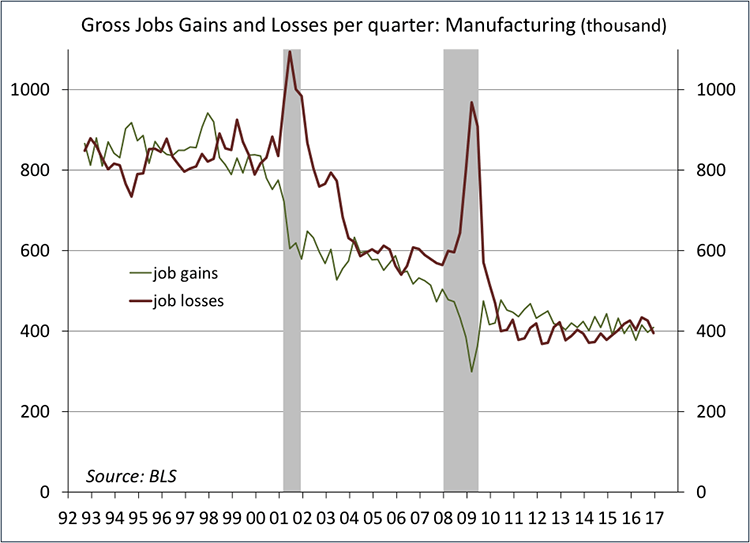

The aging of the population means that there is less job hopping than in past decades. The turnover in factory jobs is half of what it was a couple of decades ago. The economy is less dynamic and there may not be much policy can do about that.

Given the demographic story, the new normal is characterized by slower economic growth, lower inflation, and lower interest rates. In the months ahead, Fed policymakers will wrestle with the questions of how slow and how low. They aren’t alone. Other countries will be experiencing a similar challenge.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James