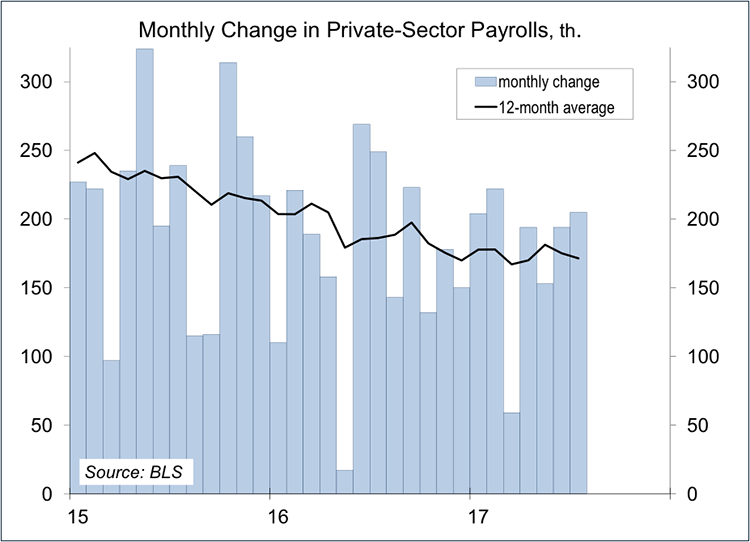

There’s a fair amount of noise in the monthly employment data, but July figures remained consistent with expectations of moderately strong growth in the near term. One glaring weakness remained. That was in retail payrolls (up modestly, but down significantly since January). Job growth should be supportive for spending. Real wage growth, weak in early 2017, appears to be picking up, and that is a good sign.

Nonfarm payrolls rose by 209,000 in the initial estimate for July. The monthly change is reported accurate to ±120,000, meaning that there is about a 90% change, or level of confidence, that the true monthly change was between +89,000 and +329,000. So why do financial market participants put so much weight on the figure? In addition to statistical noise, seasonal adjustment can be tricky (unadjusted payrolls fell by 1.039 million in July, reflecting the end of the school year). Looking at longer-term averages reduces (but does not eliminate) much of the noise in the payroll data. Private-sector payrolls appear to be trending at about the same pace as last year, which is still beyond a long-term sustainable rate. We know that because the unemployment rate continues to trend lower.

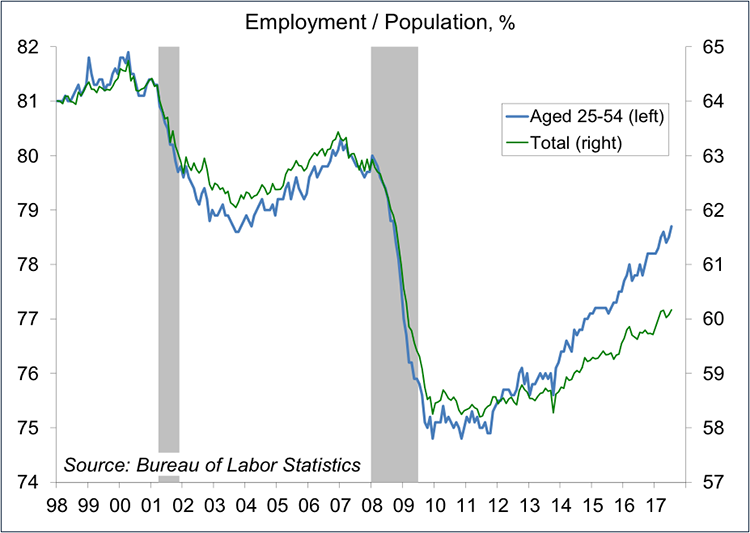

The unemployment rate edged back down to 4.3% in July, about even with May’s 16-year low. Labor force participation remains well below its pre-recession level, but that’s largely due to the demographics (an aging population). The employment-to-population ratio for prime-age workers (those aged 25-54) is trending higher and is near where it was before the recession.

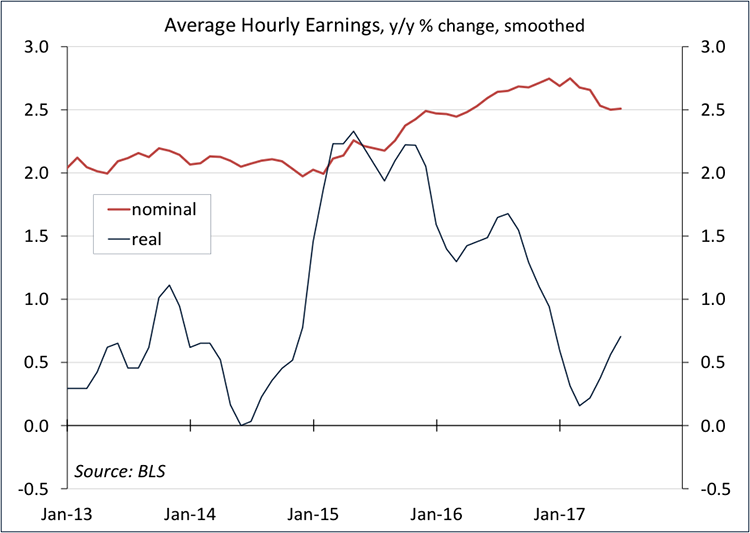

So where is the wage growth? Average hourly earnings are trending +2.5% year-over-year – good, but not where we’d expect to be given the unemployment rate. Anecdotally, firms are reporting higher wages offers for certain skilled positions, but we haven’t reached a point of broad wage acceleration. A large part of that may be explained by reduced bargaining power (lower union membership, a higher concentration of large firms). Low productivity growth is also a possible explanation, as is the low trend in inflation (workers typically get annual cost of living increases tied to the CPI).

Job growth has certainly been supportive for consumer spending growth, but purchasing power was restrained in early 2017, reflecting year-over-year increases in gasoline prices. While nominal wage growth has been trending at a moderate pace, inflation-adjusted wage growth appears to be picking up.

There are other constraints on household budgets. Rents have been rising faster than overall inflation (and wages). The Affordable Care Act has led to increased out-of-pocket spending on healthcare. In addition, many firms now have health insurance plans with large deductibles that have to be reached before coverage kicks in. These deductibles reset once a year, leaving households with less fuel for discretionary spending.

Real wage gains and fading strains from health insurance should help to support consumer spending growth in the near term, but don’t expect a sharp boom in the second half.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James