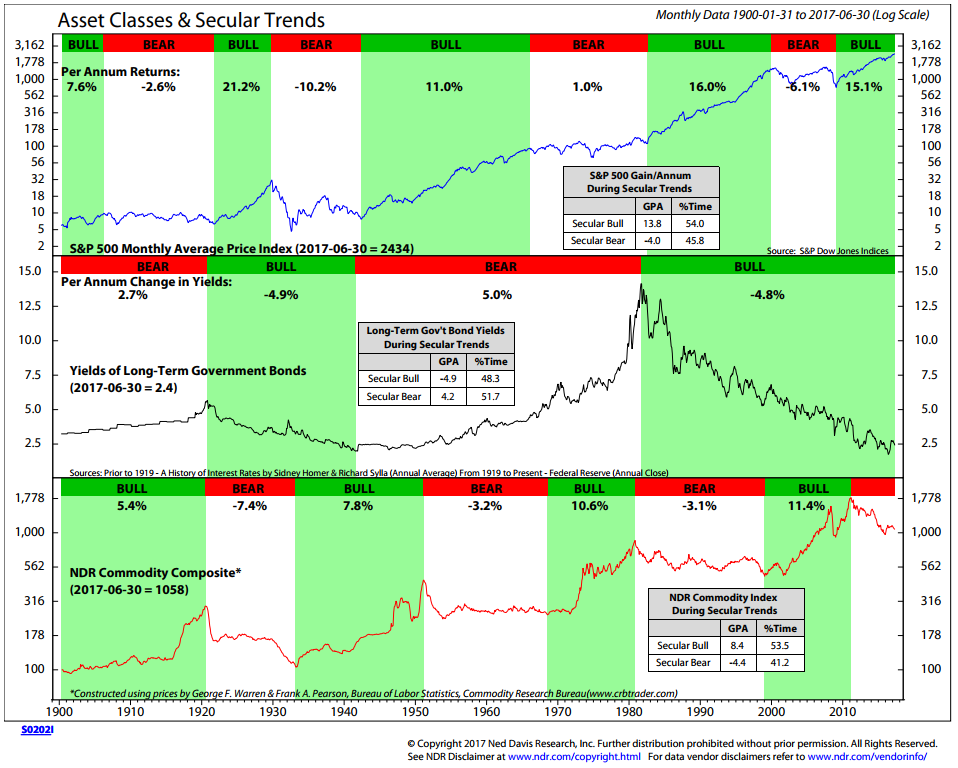

Few saw the bull market to come. Valuations were so low and forward return opportunity so high and with Treasury bonds yielding in the mid-teens, it was a beautiful set up for the 60-40 “buy-and-hold” mix. We are creatures of recent experience. Something the smart guys call “Recency Bias.”

As you can see in the next chart, the 1982-2000 equity bull market was pretty great. And the move since 2009 has been nothing short of spectacular; yet, who do you honestly know that was buying back then? It was pure panic.

Here’s the data:

One of the things that is easy for investors to lose sight of is the reality that both bull and bear markets exist. We know, behaviorally, it gets challenging for many investors after strong market periods and it is equally challenging after bear market corrections.

Kevin Malone from Greenrock Research visited me and my team this week. His firm partners with advisors and wealth managers, providing advice and an array of investment solutions. Before Kevin left he gave me a copy of a paper he wrote, “Think Twice.”

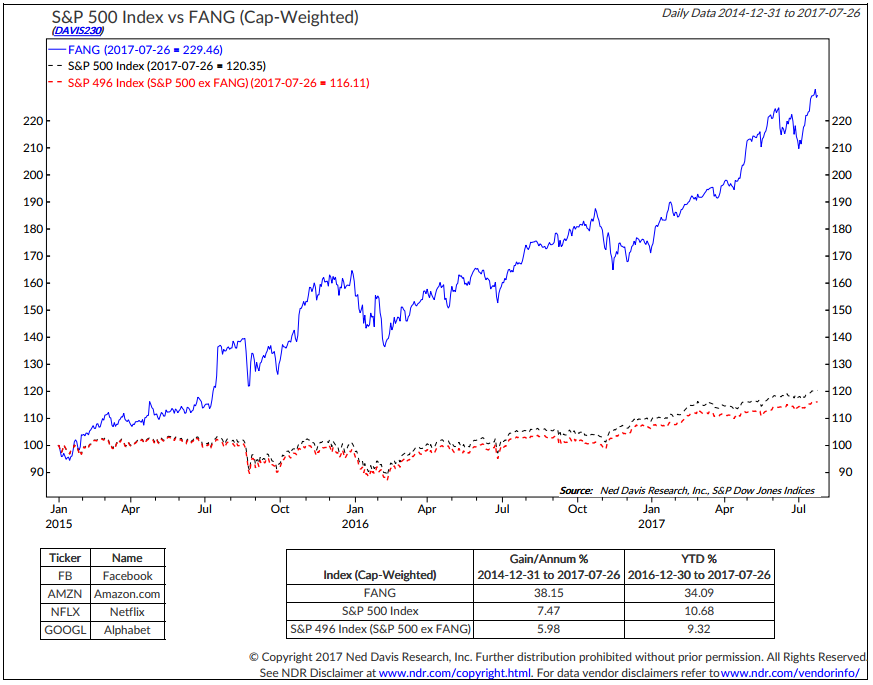

In 1998, the top 12 stocks contributed all the return of the S&P 500 Index. In other words, the S&P 500 was up 28.6% while the S&P 488 was flat. We thought that performance couldn’t be sustained until we saw what happened in 1999 when the total return of the S&P 500 came from the top 7 stocks.

Unfortunately, this is normal behavior after long rises in stock prices. The same phenomenon existed in the later 1960s and early 1970s with a group of stocks called the Nifty Fifty. These were supposed to be one-decision investments: one could safely hold them for decades. The problem was that 1973 and 1974 saw the Nifty Fifty fall more than the market, just as the top 12 and 7 stocks from 1998 and 1999 fell in the 2000-2002 period.

The poster child for this one-decision investing phenomenon in the 1998-1999 period was Microsoft, a great company. Our job, though, is not to identify great companies but great investments. If one bought Microsoft on the first trading day of 1998, the price was $16 per share and by the end of the next year, 1999, the price was $48. Investors were euphoric, but here is the problem. Microsoft peaked at the end of 1999 at $48 and one had to wait until September 30, 2015 to reach $48 again. That was 15 years and 9 months of no appreciation.

Today, the craze is FANG (Facebook, Amazon, Netflix and Google) stocks. And it looks like this:

Is it any wonder investors are crowding into these four stocks? Seems like periods past.

Ned Davis said, “Over the years I have seen scores of very bright investment advisors turn into hugely successful gurus who blaze into the investment business with spectacular forecasts. Yet, I’ve watched each and every one of them crash back to earth when a big subsequent forecast inevitably proved wrong.”

The reason I shared that intro quote is that all too often I see investors jump from one hot hand to another. My point is that I don’t believe that works in the long run.

Be mindful of risk… at all times. This is not a game of perfect. Everyone makes mistakes but you have to avoid the really big mistakes. If you are young and have many investment years and little need to touch your savings, then dollar-cost average and simply buy and hold. Your additional savings and ongoing rebalancing will get you to a very good place. Save more… borrow less.

But if you are a pre-retiree or retiree, like me, unfortunately you don’t have the time required to overcome significant loss. Like Microsoft in the late 1990s, resist the urge to herd. As Kevin suggests – Think Twice.

Below you’ll find a great chart on long-term buy-and-hold. I think about my daughter, Brianna, and see this as a good investment plan for her. And you’ll also see that the weight of evidence, as posted in this week’s Trade Signals (link below), remains bullish.

FANG stocks, gigabytes and terabytes. The amount of data that is available at our fingertips is simply amazing. We can be really thankful for that. Read on and have a great weekend!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

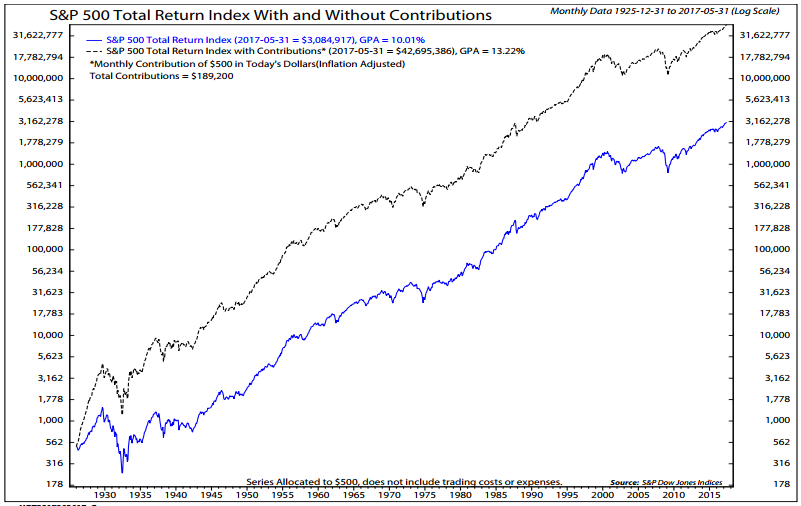

- S&P 500 Total Return Index With and Without Contributions — 1926 to May 31, 2017

- “Think Twice,” by Greenrock Research

- Trade Signals — Trend Trumps Sentiment

- Personal Note

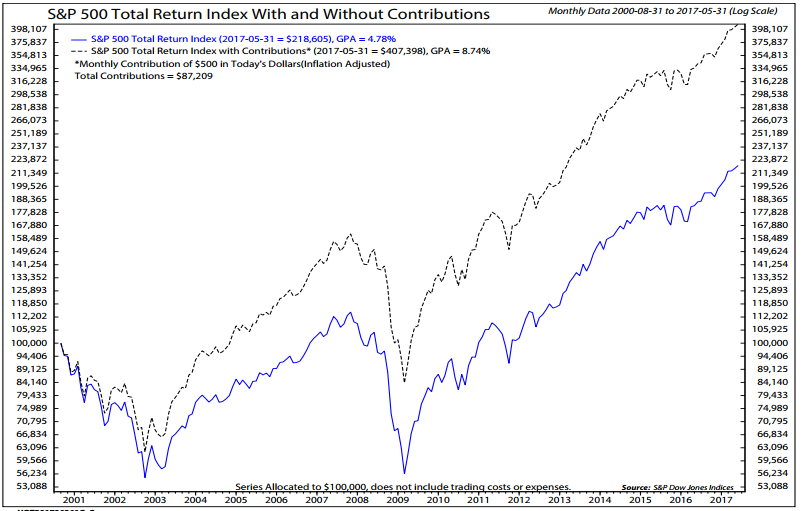

S&P 500 Total Return Index With and Without Contributions — 1926 to May 31, 2017

Here is how to read the chart:

- Start date: 12-31-1925

- $500 monthly contribution

- Black line shows the results of dollar-cost averaging starting with $500 in 1926 (in today’s dollars adjusted for inflation or the equivilent of $37 in 1926) and adding the inflation adjusted equivalent of $500 per month

- The dollar-cost averaging took the return up to 13.2% from 10% (blue line). That’s really good.

The problem is in one’s ability to stick to the plan. If you can dollar-cost average the indices, reinvest the dividends over the long run and stay the course during the big declines, then this type of investment process is a really good plan. One that is more suitable to the young and ultra-wealthy.

Here is a look since August 2000 to give you a feel of what this investment strategy looked like through two bear market declines of 50%.

But real life experience tells me to question just how many people can continue to buy when prices are crashing. I believe few can truly stick to the process. And that’s the point, find a process that suits your psyche.

“Think Twice” by Greenrock Research

Here is the link to a thoughtful piece from Greenrock Research. A special thank you to Kevin Malone for allowing me to share it with you. Kevin and his firm work with hundreds of individual investment advisors.

“If you go to the dictionary to get an understanding of the term ‘Think Twice’, you will find theses definitions,

- To consider carefully whether one should do something.

- To be cautious about doing something.

- To weigh something carefully.

- To review one’s options.”

Kevin believes, “Thinking twice and considering reasonable timeframes are critical to investment success. So why do investors get caught up in the wrong timeframe?”

It may be the amount of information or investment sound bites. When investors hear that the market is up 8%, but EAFE is up 14% for the first half of 2017, they feel they missed out. It becomes too easy to stray from a long-term game plan.

Your job is not an easy one. Hope material such as this helps you keep your clients focused on 10 years and not eight months. And post-Trump’s election, what an eight months it has been.

Click here for the full piece. It is short and well worth the read.

Trade Signals — Trend Trumps Sentiment

S&P 500 Index — 2,477 (7-26-2017)

Notable this week:

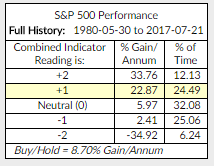

It’s Fed day [last Wednesday], so let’s take a look at one of my favorite indicators: Ned Davis Research’s Don’t Fight the Tape or the Fed. The indicator looks at the NDR’s Big Mo Multi-Cap Composite and the 10-year Treasury yield percentage. Big Mo measures the overall breadth of the marketing across many sectors. The Treasury yield looks at where the current yield is relative to its recent trend to define periods of rising rates, flat rates or declining rates.

Each indicator can score +1, 0 or -1. A +2 (bullish) score is given if both the composite and 10-year yield are bullish. A -2 when both indicators are bearish. The current reading is +1. The composite reading is neutral and the 10-year Treasury yield is bullish. When used together they can be a historically strong indicator as indicated by the model results reflected in the following chart. We want to “watch out for minus 2.”

Overall, the balance of evidence remains bullish for both equities and fixed income. Both the short-term and intermediate-term gold indicators are bullish. Investor sentiment has been excessively optimistic suggesting short-term caution. Trend trumps sentiment in my view.

You’ll find more information, charts and explanations here.

Long-time readers know that I am a big fan of Ned Davis Research. I’ve been a client for years and value their service. If you’re interested in learning more about NDR, please call John P. Kornack Jr., Institutional Sales Manager, at (617) 279-4876. John’s email address is [email protected]. I am not compensated in any way by NDR. I’m just a fan of their work.

Personal Note

Some vacation is in my near future and I hope yours as well. Susan and I, along with our children, are heading to Lake George to visit family this weekend. Everyone is really excited. It’s going to be tough to surpass last year’s wine-induced Karaoke session where we passed the pepper shaker (microphone prop). Only later to discover, thanks to video recording captured on our kids’ iPhones, we just didn’t sound as good as we thought we did in the moment. Oh, but what fun.

John Mauldin is flying to Philadelphia next Wednesday and we head out the following morning to Maine for an economic and investment brainstorming session of sorts at the annual Camp Kotok “Shadow Fed” get-together. I’m not sure what I’ll be able to share but I’m really looking forward to those few days.

If you missed John’s recent post titled, “Three Black Swans” you can find it here. John writes,

I am concerned that another major crisis will ensue by the end of 2018 – though it is possible that a salutary combination of events, aided by complacency, could let us muddle through for another few years. But there is another recession in our future (there is always another recession), and it’s going to be at least as bad as the last one was, in terms of the global pain it causes. The recovery is going to take much longer than the current one has, because our massive debt build-up is a huge drag on growth. I hope I’m wrong. But I would rather write these words now and risk eating them in my 2020 year-end letter than leave you unwarned and unprepared.

Black Swan #1: Yellen Overshoots

Black Swan #2: ECB Runs Out of Bullets

Black Swan #3: Chinese Debt Meltdown

I look forward to stress testing his thinking on a lake in Maine with fishing rod in hand. I then fly home on August 6 and head straight, as they say here in Philadelphia, “down the shore.” Susan and I have rented a house in Stone Harbor, New Jersey for the week. Kyle will be coming home from camp and five of our six kids will be with us. Can’t wait.

If you have any great book recommendations, please let me know. Something non-financial. I don’t think I can stuff any more terabytes in my hard drive.

Thanks for reading. Have a wonderful weekend!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group

Read more commentaries by CMG Capital Management Group