The advance GDP report for 2Q17 contained few surprises. Growth was largely in line with expectations, leaving growth for the first half of the year at a 1.9% annual rate. Recent reports suggest some loss of momentum for the consumer, but rising real wages ought to provide support. The second half outlook should come into better view as the July data begin to arrive. While the growth outlook may be disappointing relative to earlier expectations, it’s still a good backdrop for the markets.

Click here to enlarge

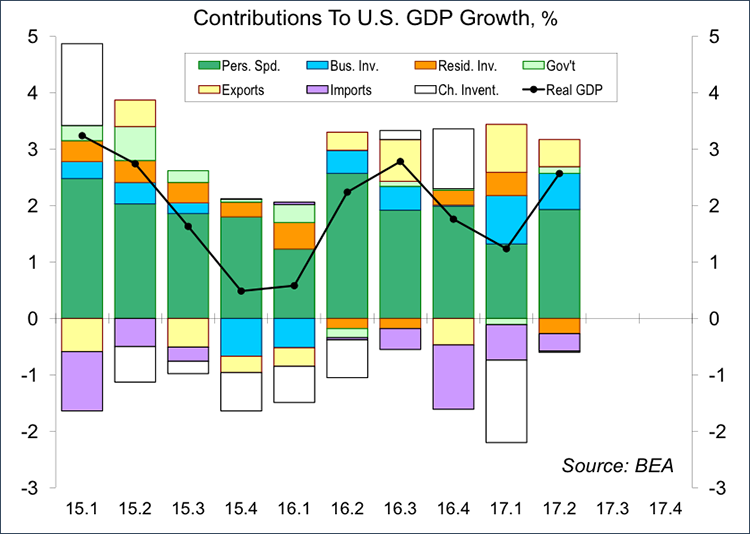

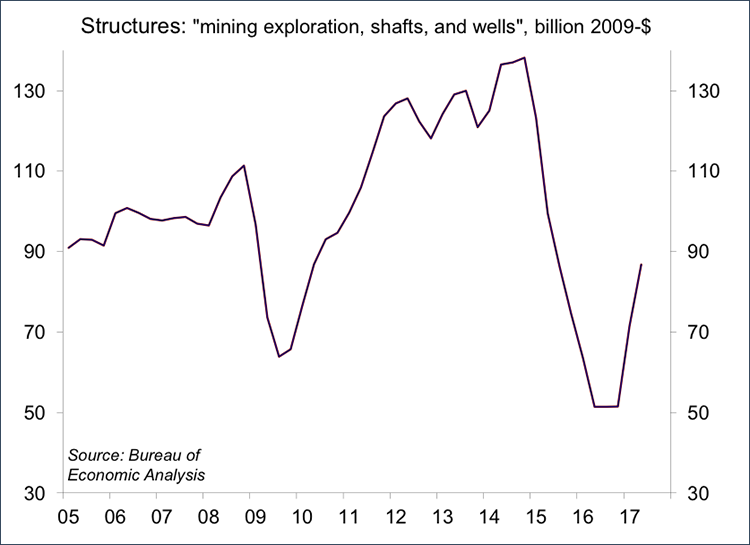

Consumer spending, which accounts for 69% of Gross Domestic Product, picked up in the second quarter, while the annual benchmark revisions appear to have shifted some strength from 4Q16 into 1Q17. Business fixed investment remained strong, although not quite as robust as in the first quarter. While business optimism has been supportive, nearly half of this year’s growth in business fixed investment has been concentrated in energy exploration. Residential homebuilding weakened in the second quarter, but that followed weather-related strength in 1Q17. Slower inventory growth subtracted nearly 1.5 percentage points from headline GDP growth in the first quarter. Economists had expected an inventory rebuild to add significantly to GDP growth in 2Q17. That didn’t happen (at least in the advance data). None of this tells us much about the growth prospects for the second half of the year.

While the 2Q17 consumer spending data show improvement relative to the first quarter, monthly figures point to a lack of momentum heading into 3Q17. We’ll get a better idea following Tuesday’s release of personal income and spending figures for June (which will include annual benchmark revisions). Job growth has certainly been supportive. Nominal wage growth has been moderate, but the rise in gasoline prices (relative to a year ago) was a sharp restraint on real wage growth. That appears to be changing, and improvement in real wages ought to support consumer spending growth in the second half.

The recovery in oil and gas well drilling appears to have more room to run, helping to fuel growth in business fixed investment in the second half of the year. Global growth has picked up, which should aid U.S. exporters. The Border Adjustment Tax appears to be dead, but many firms are still worried about the possibility of a trade war. Developing and securing alternative supply chains is costly, but this may contribute a little to domestic capital spending. Business optimism, elevated at the start of the year, is likely to ebb, but remain relatively high.

Click here to enlarge

Residential homebuilding, which accounts for about 3.8% of nominal GDP, is cyclically sensitive – rising in expansion and falling sharply in recessions. The sector remains constrained by higher costs and affordability issues, but we should see moderate strength in the second half of the year.

In their growth outlooks for this year, economists were divided largely by differences of opinion regarding the timing, magnitude, and characterization of fiscal stimulus. At this point, the more optimistic have become less enthusiastic. Despite, improved business sentiment, GDP growth is likely to be closer to 2% in the second half of the year than to 3% – and we could easily see growth edging below 2%.

The Fed still expects to continue gradually raising short-term interest rates over the next couple of year. Consumer price inflation has remained low, and if one factors out the sharp drop in telecom services we had in March, the trend is largely in line with what Fed officials had expected. Still, while low inflation figures won’t prevent the central bank from tightening further, they ought to keep the pace very gradual. It’s widely expected that the Fed will wait until the mid-December meeting to raise rates again, setting a smooth backdrop for the start of balance sheet unwinding in October (provided the economy evolves in line with expectations). Moderate GDP growth isn’t bad – in fact, it’s been a great environment for stock market investors.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James