As our regular readers are aware, we’ve been pounding the table all year arguing that foreign stocks are in a position to structurally outperform domestic stocks. At the risk of sounding like a broken record, we thought we would – in one post – review the setup that makes foreign equities relatively attractive at this juncture.

1) US stocks have outperformed foreign stocks almost continually since 2008 – nothing lasts forever

In our world there are only three different kinds of trades:

- Momentum trades – trades that try to exploit price momentum and the herding behavior observed in markets

- Carry trades – trades that seek to capitalize on interest rate differentials between assets

- Return to the mean trades – trades that benefit from mean reversion of returns between assets

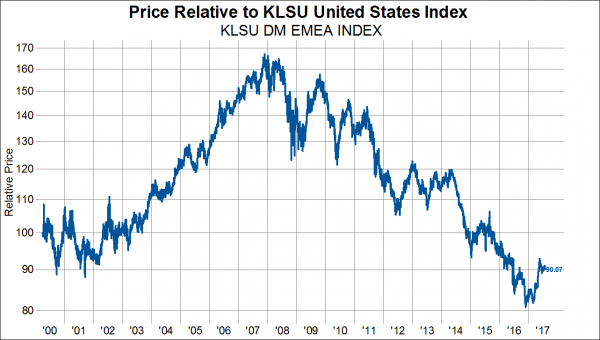

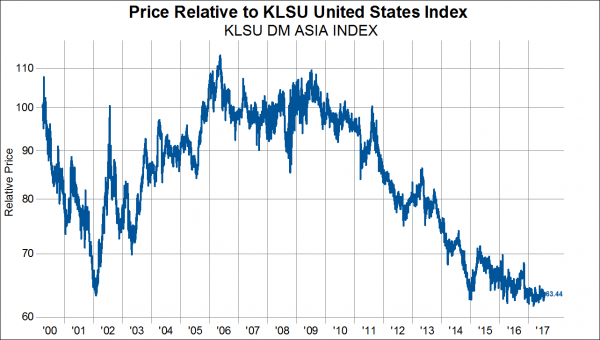

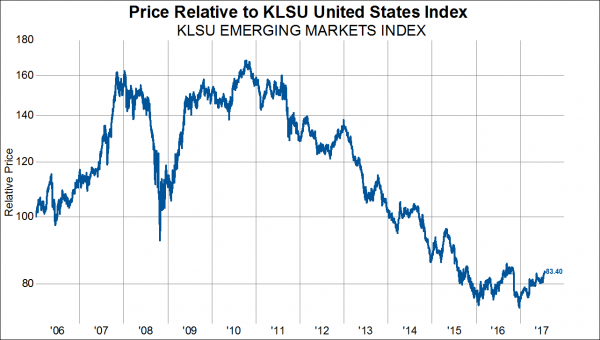

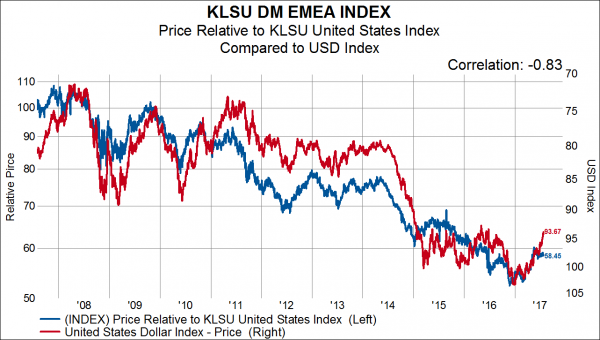

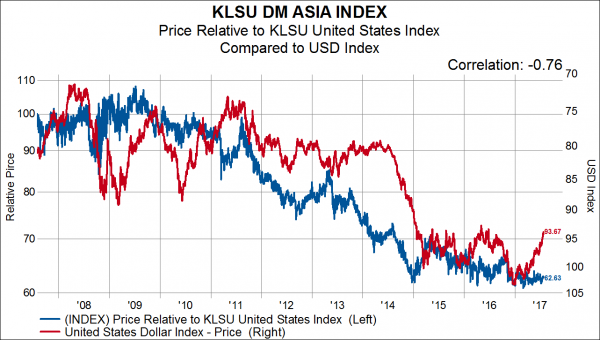

The opportunity for investors to increase their international equity exposure at the expense of domestic equity exposure is a return to the mean trade. The essence of a return to the mean trade is that in the fullness of time two similar assets should have a similar return. Since the end of 2007 the United States has outperformed DM EMEA by 45%, DM Asia by 38%, and EMs by 48%. One can argue that there were structural reasons for the lopsided returns over the last decade, but even structural divergences don’t last forever. And indeed, it looks like foreign markets have stopped underperforming. Relative performance for DM EMEA and EMs stopped making new lows at the end of 2016 while DM Asia stopped making new relative lows at the end of 2014. The first three charts below show the relative performance of the three regional equity indexes compared to the United States index.

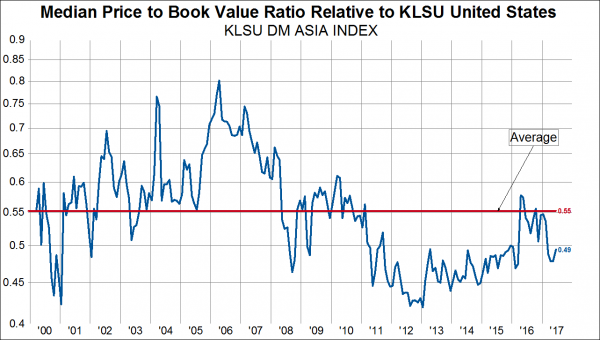

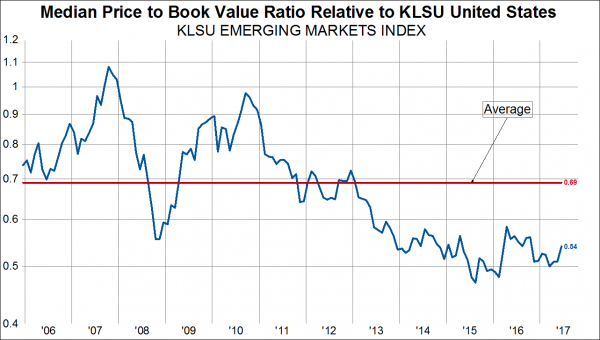

2) Relative valuations favor foreign equities, except in Europe

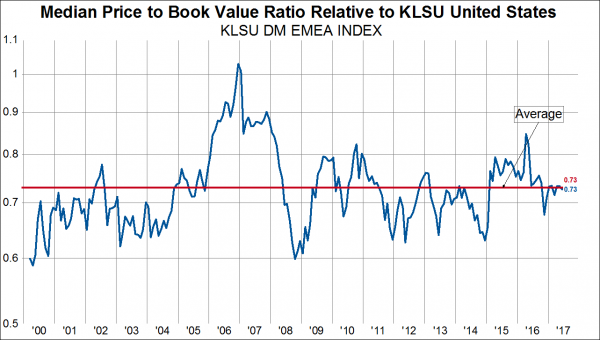

The substantial outperformance of US stocks has come with substantial relative valuation expansion, especially in developed Asia and the emerging markets. Higher valuations necessarily imply lower prospective returns, and vice versa. The charts below show the median price to book value ratio for stocks in each region compared to the median price to book value of US stocks. By this measure, relative valuations are right on the mean for DM EMEA, 11% below average for DM Asia and 22% below average for the EMs.

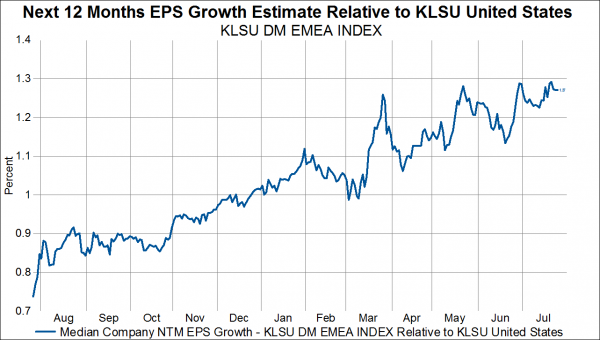

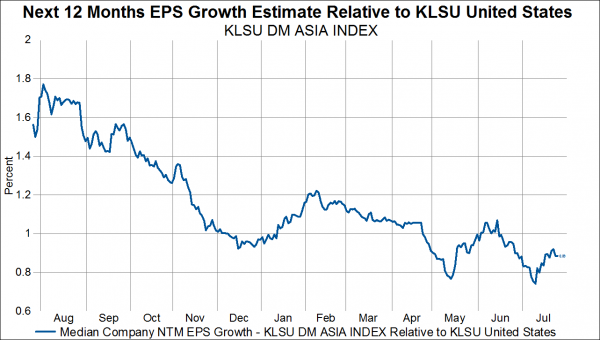

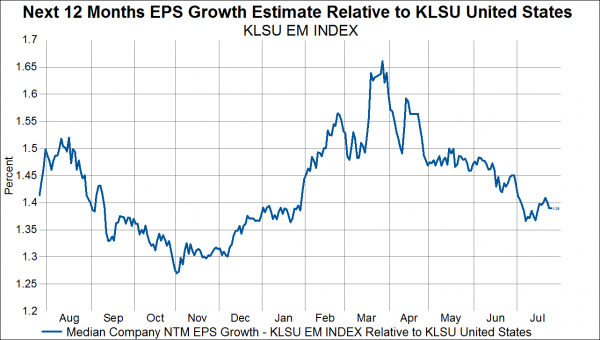

3) The analyst community is starting to expect relatively higher earnings growth in some foreign markets

The next three charts show the median company’s next twelve months earnings growth estimates for stocks in each region compared to the next twelve months earnings growth expectations for the median US stock. Essentially, this is a comparison of relative earnings growth estimates. Analysts have consistently rerated their expectations of European company earnings growth compared to US companies. Meanwhile, estimates for DM Asia have stopped deteriorating relative to the US. Relative growth expectations for EMs troughed last November and may have started to turn higher over these last several weeks.

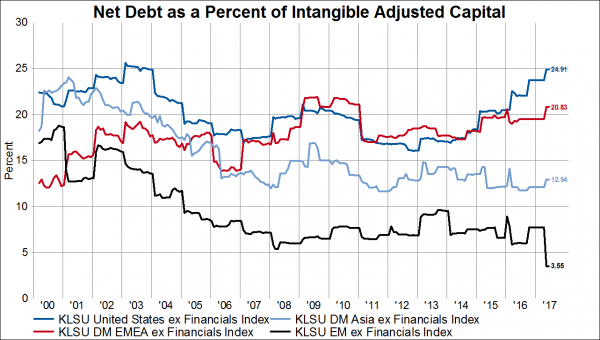

4) Balance sheets are stronger outside of the US

The chart below shows the aggregate net debt as a percent of intangible adjusted capital for all non-financial stocks in the United States and the three other regions. Since 2012 we’ve witnessed a disturbing trend of higher net debt levels among US companies (dark blue line). Companies in the DM EMEA region (red line) have increased net debt modestly, but are still below cycle highs. Companies in DM Asia (light blue line) and the EMs (black line) have been reducing net debt since 2001 and are at or near cycle lows.

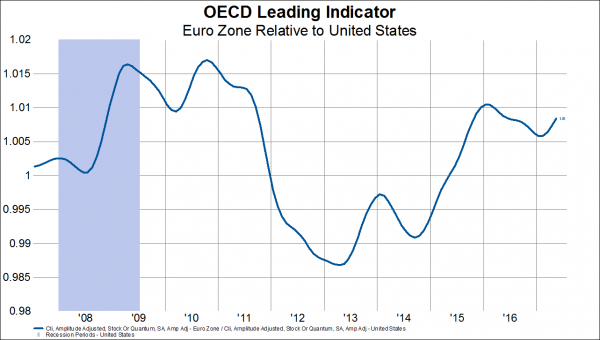

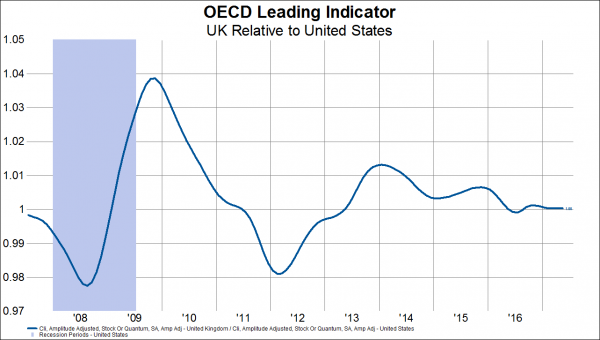

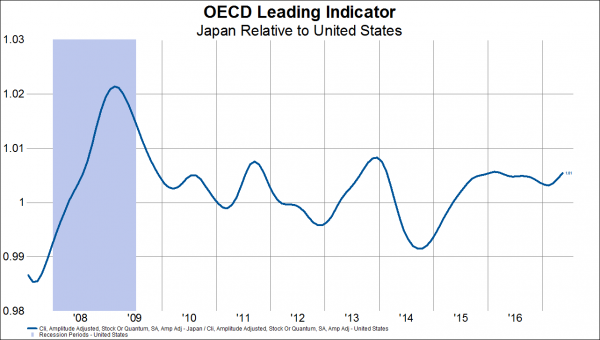

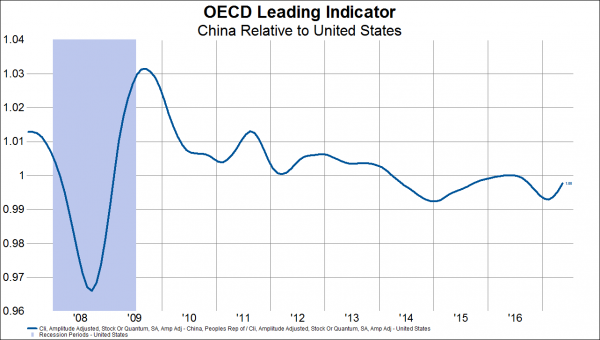

5) Economic growth prospects are improving in foreign markets relative to the US

2017 has so far been a catch-up year for foreign economies relative to the United States and some indications suggest the convergence will continue. One such metric is the OECD’s leading economic indicator (LEI). In the next four charts below we show each region’s LEI relative to the LEI of the United States. For almost all of 2017 the LEIs in the Eurozone, Japan and China have been increasing compared to the US LEI. Even the UK LEI has kept pace with the US LEI. Furthermore, the Eurozone LEI troughed back in 2013 and Japan’s LEI troughed in 2014, suggesting the worst relative performance may be behind these economies for the time being.

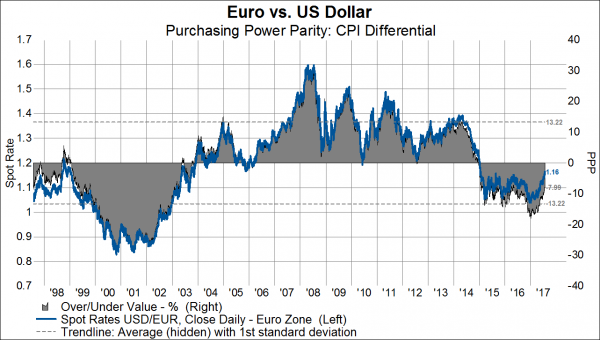

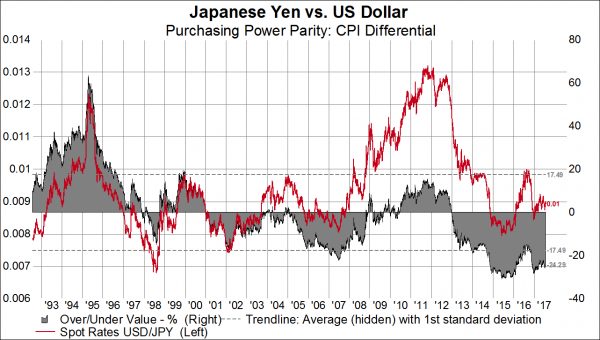

6) The US dollar has more room to fall and a falling US dollar is supportive of foreign equity outperformance

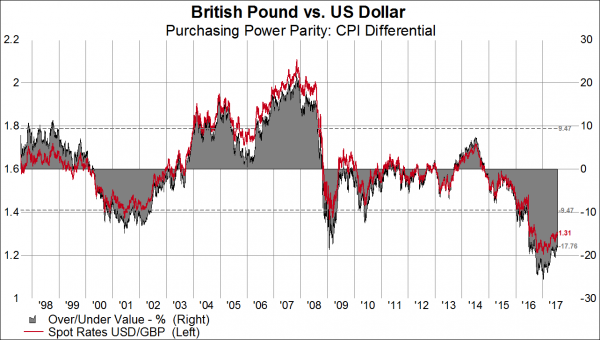

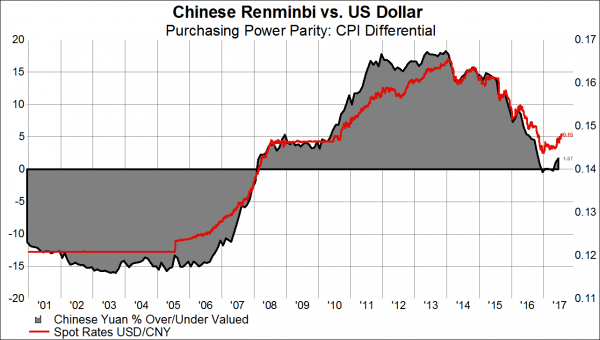

The USD has been going nowhere but down recently and is certainly due for a near term reversal or consolidation. However, the fundamentals driving the weakness in the USD persist, namely: monetary policy convergence (or slowing of divergences), relative US economic underperformance, and higher budget deficits in the US. Furthermore, according to our purchasing power parity (PPP) model, which takes into account price differentials between economies, the USD is still 7% overvalued against the euro, 24% overvalued against the yen, 18% overvalued versus the pound, and is sitting right at fair value relative to the yuan. Given that currencies almost always overshoot their fair value PPP level, the USD could conceivably fall substantially further if it were to reach the other extreme.

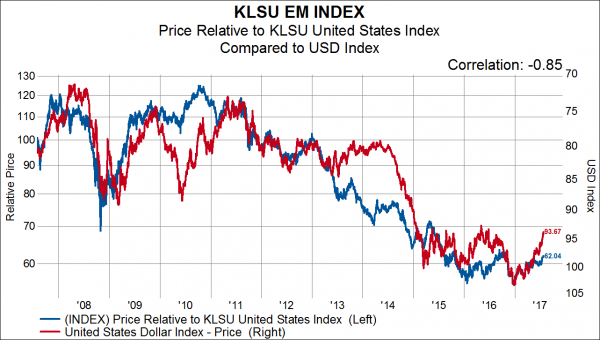

The prospect of a falling USD is important because foreign equities outperform US equities when the USD is falling. In the final three charts below we plot the performance of each regional index relative to the US index (blue line, left axis) and then overlay the USD spot index (red line, right axis, inverted). We obvserve extremely high negative correlations between the level of the USD and the relative performance of regions outside of the US. In other words, for European stocks, Asian stocks and emerging market stocks, a falling USD is associated with those markets outperforming the United States.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital