I continue to believe that the two most important issues receiving inadequate investor attention are productivity and the role of central bank liquidity in the performance of financial markets. Productivity is critical to both earnings improvement and a rising standard of living. Central bank liquidity has driven price earnings ratios higher and kept interest rates low. Productivity has been declining everywhere during the past decade compared to the 1996–2006 period, with the exception of China and India. This has placed the burden of profit growth either on existing customers spending more or on new products and new markets. Improving profitability is increasingly difficult in a slowly expanding business environment. The intention behind central bank balance sheet expansion has been to stimulate economic growth but, by my estimate, three quarters of the monetary accommodation over the past decade has gone into financial assets with only one quarter invested in the real economy.

A major reason for the weak productivity numbers is that no major technological innovation improving productivity has occurred since the Internet and the smartphone in the 1990s. The next major positive change will probably result from the introduction of the driverless car and truck. Unfortunately, almost any innovation that improves productivity has the concomitant characteristic of eliminating jobs, leading to human hardship and increasing government costs for social support programs.

Skeptics believe the productivity numbers are flawed because some improvements in worker output as a result of software applications and greater use of medical technology are hard to measure, but there seems to be little question that the productivity gains of the 1995–2005 Internet/smartphone period have slowed in the past decade. The Bank Credit Analyst has conducted a study which concludes that low productivity gains ultimately lead to higher inflation and interest rates. The emerging markets exemplify this. We will have to see if this model applies in the current cycle. The BCA economists conclude that low productivity keeps interest rates from rising at the outset but eventually leads to higher inflation and interest rates as savings are depleted. Some believe the large amount of time millennials spend on Instagram and Facebook actually detracts from productivity. The decline in mathematics proficiency for graduates of American public high schools could also be a contributing factor. Low investment in capital equipment has also lowered worker output per hour worked. There is also evidence of declining entrepreneurship. The birth rate of new companies has declined by 50% since the 1970s and now roughly equals the general business death rate. Despite these negatives, there is some hope that productivity will improve in the second half of 2017 with a stronger economy.

One aspect of the productivity issue is reflected dramatically in the U.S. equity market. Through the middle of June the so-called FAANG stocks (Facebook, Apple, Amazon, Netflix and Google, along with Microsoft) represented 13% of the capitalization of the Standard & Poor’s 500, but accounted for 33% of the appreciation. These companies were in the 90th percentile of all companies in the index, based on return on invested capital (close to a 100% return). The median was 20%. Investing in the companies with the highest return on invested capital and with the highest margins has paid off. It helps if they are in a dominant position in their respective industries and can maintain their market share. Looked at another way, Amazon and Walmart stocks were selling at about the same price in 2008. Since then, Amazon has soared and Walmart has stayed roughly flat. Today, Amazon has a market cap of $476 billion and Walmart’s is $230 billion. Amazon has 351,000 employees and Walmart has 2.3 million. Technology enables some businesses to build profits with a minimum of human capital and enjoy high margins as a result. That will be the shape of the future, with serious implications for the economy and the market.

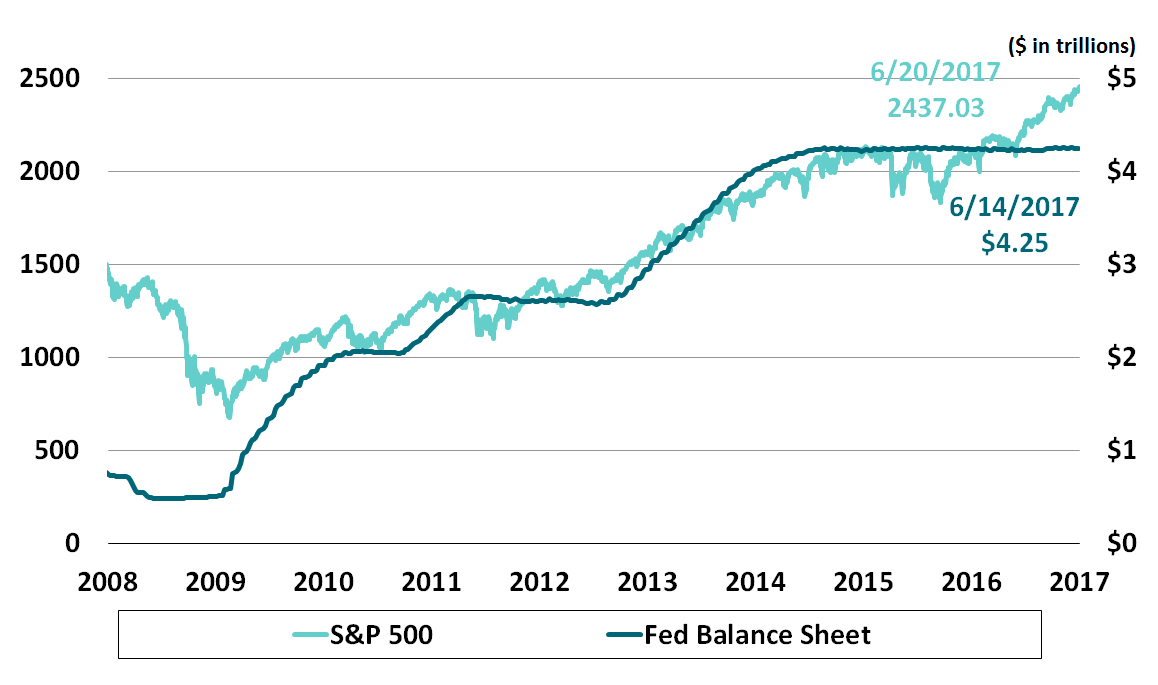

As for central bank liquidity, it has increased 13% year-on-year for the four major industrial regions – the Federal Reserve, the European Central Bank, the Bank of England and the Bank of Japan. The total of the balance sheets of those four is $12.8 trillion today compared with $3 trillion in 2008 before the financial crisis. We know, however, that the Federal Reserve is tightening its posture, having increased short-term rates twice this year with the promise of further increases to come later. The Fed is also planning to slowly shrink its $4.5 trillion balance sheet by letting maturing bonds be redeemed without buying replacements in the open market. This has the effect of reducing the supply of money in the economic system with bearish implications. The European Central Bank under Mario Draghi is also considering switching to a less accommodative stance. Draghi is going to the Jackson Hole economic conference at the end of the summer where he may announce a change in European Central Bank policy. If the Fed chooses to become more aggressive in its tightening process, Janet Yellen may use Jackson Hole as an opportunity to announce that change to the world as well.

Fortunately, earnings are coming in better than expected. After several years of modest increases, primarily because of poor performance in the energy industry, S&P 500 earnings are expected to break out and be up 10% this year to close to $130, or possibly even higher. Earnings improvements in the financial services industry will also help increase 2017 profits for the index. Continued double-digit earnings increases should not be expected, but I could see S&P 500 earnings exceeding $150 by the end of the decade if no recession takes place. While the current expansion is more than eight years old, few excesses are apparent and I am optimistic that the next serious downturn is several years away. If a recession should occur before then, determining what policy steps could be taken to get us out of it will be difficult. With interest rates already so low, the Fed has little room to create stimulus by dropping the Fed funds rate. Also, a Republican Congress is unlikely to pass bills providing significant fiscal stimulus. As a result, the best policy course is one that attempts to defer the next recession for as long as possible.

During the past few weeks, the yield on the 10-year Treasury has increased from 2.19% to 2.31%, and many observers are concerned that the yield is finally headed to 3% or higher. At the beginning of the year, the consensus was that higher interest rates would be encountered during 2017, but that view was largely based on Donald Trump getting his pro-growth agenda passed in Congress, and that has not happened. The big financial surprise of the year has been the decline in intermediate-term rates, but the recent rise suggests that trend may be reversing. At the level of 2.5% or below on the 10-year Treasury, my dividend discount model (which is designed to determine when stocks and bonds are equally attractive) indicates that the S&P 500 equilibrium point is above 3000, so stocks at present level of 2460 would appear to be very attractive. If the 10-year Treasury yield climbs above 3%, the index at present levels would be overpriced based on the model. While the model has the appearance of precision, it is actually a somewhat crude estimator. Until now, interest rates have not played much of a role in the performance of the equity market. One of the reasons the market may be consolidating recently could be that investors are apprehensive about the possibility of rising yields providing bond market competition for stocks.