“The primary, direct driver of default rates is not the yield on Treasury bonds but rather the business cycle.”

Martin Fridson, CFA

CIO of Lehmann, Livian, Fridson Advisors, LLC

At a conference in Chicago this week, following up on last week’s letter, Keep Dancing but with a Sharp Eye on the Tea Leaves, an advisor client asked me what my favorite “tea leaf” might be. When one of the greatest investors of our time, Ray Dalio, tells us to keep an eye on the exit door we should take note. But how? And when? There is no perfect indicator, but there are a few very good ones and it’s been my experience that simple is best and trend following works well.

Since we were talking about the economy and the stock market and since all the bad stuff in the stock market happens during recessions, my answer was to watch the trend in the high yield bond market. The players have a keen eye toward the economy and potential default risks in the bonds they own. Thus, in my view, high yield tends to be a pretty good “tea leaf.”

Watching the trends every day since the early 1990s has taught me that the high yield market generally leads the equity market by six months or so. It’s not exact, but in my 25 years of trading high yield, it’s been my observation (with real money on the line) that high yield is sensitive to the economy and tends to lead equities lower. I believe it is because high yield bond managers are razor-focused on changes in their underlying bond credits (default risks) and react just a bit faster than equity investors. More sellers than buyers drive prices lower.

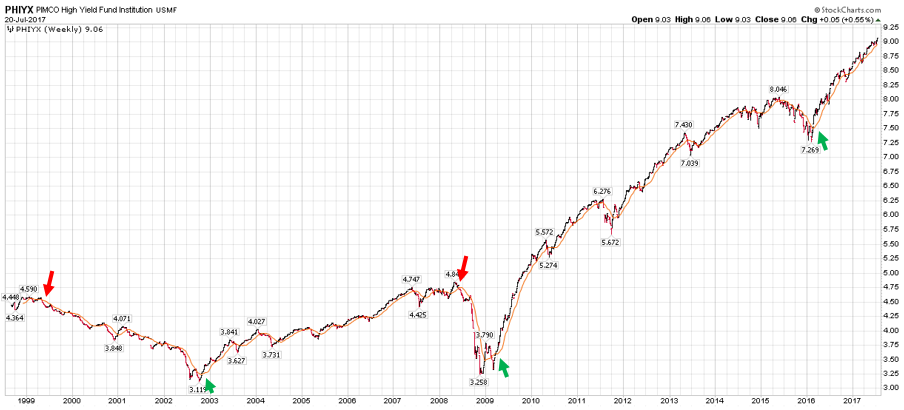

So how can you keep your eye on this? Following is a weekly chart of the PIMCO High Yield Fund going back 19 years to 1998. The chart shows weekly price data. The orange line is a simple 13-week smoothed moving average price trend line. When the current price drops below the smoothed trend line, a sell signal is triggered.

I remember taking a lot of heat from clients in 1999. High yield rolled over in 1998 while the tech bubble bubbled on. Then it broke. Avoided were the recessions in 1991, 2000-02 and 2008-09.

Here is the chart and how to read it:

- The data is weekly price data for the PIMCO High Yield Fund (PHIYX).

- The orange line is the 13-week moving average line. Think of it as a smoothed moving average of the trend in price over the preceding 13 weeks.

- When the price drops below its trend line, that’s a warning signal (red arrows).

- When the price moves above the trend line, it is a buy signal (green arrows).

- Note – arrows show only a few of the signals to give you a sense of how it works. More attention should be paid late in a business cycle (like today).

It’s important for me to say that we use a trend following process that triggers more quickly than the above for our high yield trading, but the point is that trend following can help you gauge turning points in the economy and the stock market. High yield is a leading indicator for both the economy and for equities. Experience has taught me it is a tea leaf worth watching. Of course, past performance does not predict, indicate or guarantee future results.

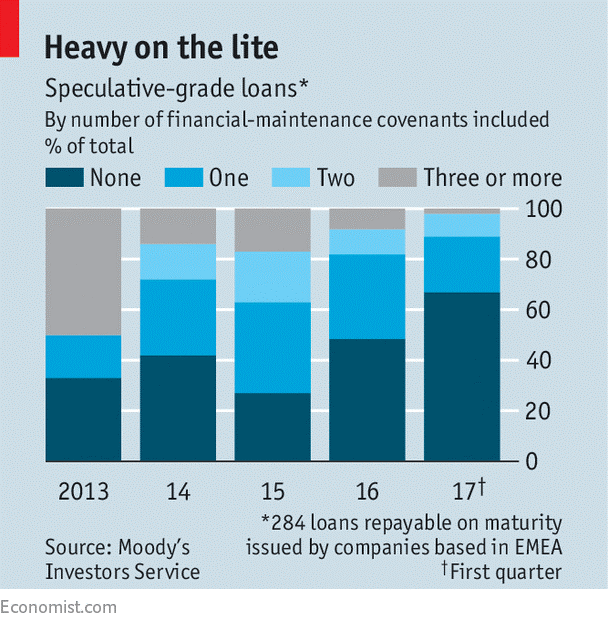

PJ Grzywacz, CMG’s president, sent me the following Economist article a few weeks ago. “Alarm grows about over-exuberance in corporate lending.” Here is the bottom line, the chase for yield has led to really junky junk bonds. Remember those mortgage pools, subprime, CDOs and slices and dices of synthetically packaged AAA-rated garbage. Well, it’s happening again.

Investors are willing to accept such terms because they are desperate to earn some kind of yield on their assets. In the past eight years, central banks in developed economies have pushed interest rates close to zero. Government bond yields have also been at historic lows and some have even been negative.

When low-risk assets offer a poor return, investors are willing to take more of a chance. At times like this, Wall Street always has a suitable set of initials to flog. This time, it is the collateralized loan obligation (CLO), which bundles loans together into a diversified portfolio. As with subprime mortgages a decade ago, these portfolios are then divided into different tranches to offer higher returns (at higher risk). CLO issuance so far this year is double the amount raised in the same period of 2016, according to Wells Fargo Bank.

The cycle has turned again. Analysis by Moody’s, a ratings agency, shows that the proportion of the loan market that is “covenant-lite” has risen from 27% in 2015 to more than two-thirds in the first quarter of this year (see chart). Some loans even contain restrictions on the lender, not just the borrower.

The good news is that any shakeout in the market should be more contained than it was in the days of Bear Stearns and Lehman Brothers, whose collapse precipitated the 2008 crisis. The financial system is not as fragile as it was a decade ago; banks have more capital and are probably carrying less of this speculative debt on their own balance sheets.

Nevertheless, it is hard to escape the feeling that the market is being kept aloft by the actions of central banks.

So the risk is building. This from Investing.com:

According to Moody’s Covenant Quality Index, US and Canadian bonds issued during the month of June had a quality rating of 4.48, weakening from 4.26 in May and only four basis points of the record worst 4.52 set in August 2015.

SB here: 1 is best rating quality, 5 is the worst.

Further, ““HY-Lite bonds represented a record 60% of June’s single month issuance and a record 47% of bonds included in the June Covenant Quality Index.”

SB again: Big appetite for the riskiest bonds.

Tea leaves indeed. Keep the high yield price trend on your radar. For now, the trend is higher, so breathe easy and carry on. As you’ll see when you click through to Trade Signals (link below), the equity and bond market trend indicators remain bullish as well.

This week’s post is short. I hope you find the charts I share with you interesting. Grab a coffee, jump in and have an outstanding weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Follow me on Twitter @SBlumenthalCMG.

Included in this week’s On My Radar:

- Charts of the Week

- Trade Signals — Cyclical Bull Trend Persists

- Personal Note

Charts of the Week

Following are several charts I found interesting this week.

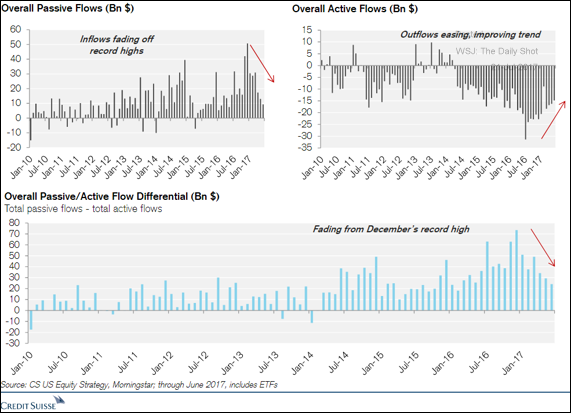

Chart 1: Fund flows show further rotation from passive to active funds. When correlations are low (as they are currently), stock/sector picking becomes more important.

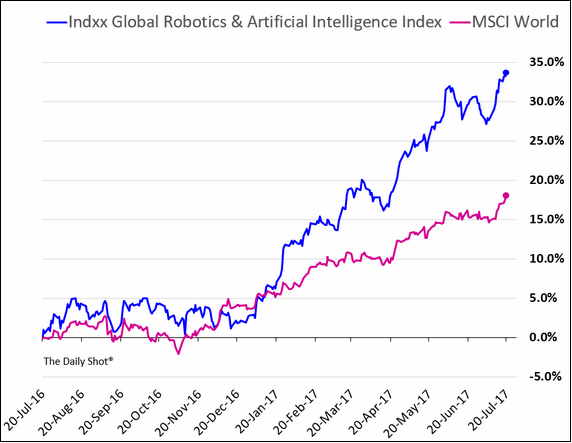

Chart 2: Stocks of companies focusing on robotics and artificial intelligence have dramatically outperformed broad global indices this year.

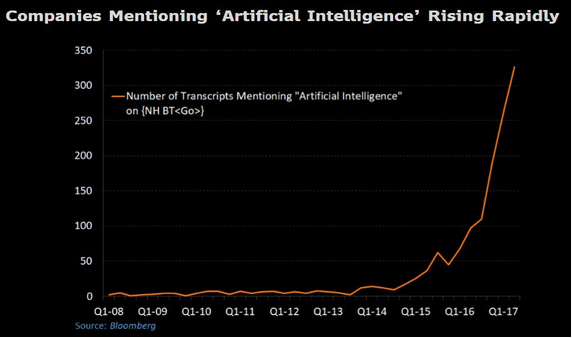

Chart 3: This chart shows the number of companies mentioning “artificial intelligence” in their reports.

Think about the artificial intelligence that scanned the transcripts to produce that data. Awesome times… and perhaps a bit concerning. We are on an unstoppable robotics path. What might this mean to future jobs? Complex in its societal impact. We’ll just have to figure it out.

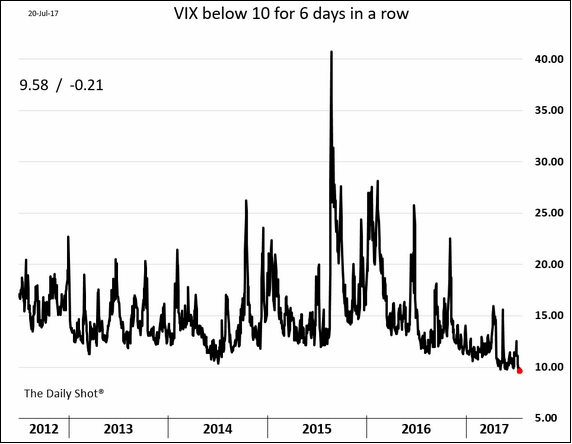

Chart 4: VIX closed below 10 for six straight days. A record low. Complacency equals high risk in my book.

Downside risk protection is cheap!

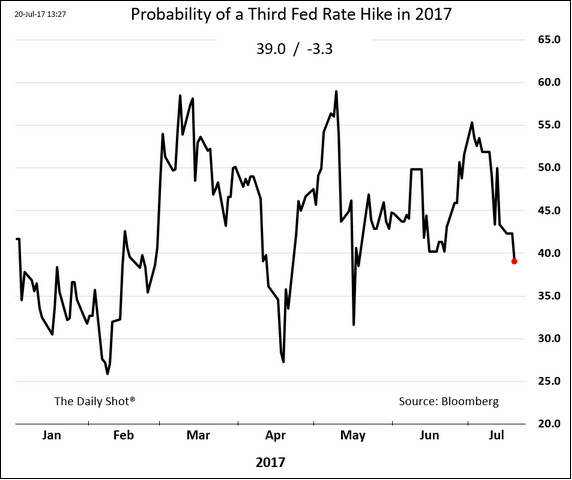

Chart 5: Probability of a third rate hike is declining.

Chart 6: This is cute.

Source: @LorcanRK

The ECB is getting concerned about the euro’s strength because this trend is negating the central bank’s easing efforts. The ongoing euro appreciation could begin dampening the recovery (by pressuring exporters) and further depressing inflation (which is already way below the ECB’s target).

Chart 7: The U.S. dollar. The dollar continues to weaken amid softer economic data in the U.S. and more hawkish central banks around the world.

Chart 8: The euro continues to rally relative to the dollar. Thus the humor in the above Mario Draghi-Alexis Tsipras photo. Draghi is the head of the ECB and Alexis Tsipras is the Prime Minister of Greece.

The currency games are “full on” whether by choice or circumstance. The lower dollar favors U.S. exports. The higher euro puts Europe at a trade disadvantage.

All of the above charts are from the WSJ’s Daily Shot. To receive the Daily Shot newsletter in your inbox, sign up at Email Center. I believe it requires a subscription to the Wall Street Journal.

Finally, here are three outstanding minutes with Richard Fisher on CNBC. His views on asset bubbles, the Fed and Gary Cohn. Click on the picture. Worth the watch… It’s all about that Fed.

Source: CNBC

Trade Signals — Cyclical Bull Trend Persists

S&P 500 Index — 2,466 (7-19-2017)

Notable this week:

No changes since last week’s post. Aged, overvalued and in a state of euphoria (yes, all true); yet, the equity market trend signals remain bullish. You’ll find more information, charts and explanations here.

Personal Note

Numbers stick like glue in my mind and I can mentally map my way, but try to tell my wife the names of the roads along the path and I struggle. Quickly recall names? A struggle for me. I came across an email from Lumosity giving a few pointers on time-tested memory techniques and, if you are like me, I hope you find them helpful.

- Build your own “memory palace”

Used by the ancient Greeks, the “memory palace” technique is based on the fact that people have a far better memory for the tangible (physical spaces, images) than the abstract (numbers, words, ideas).

To create your own memory palace, pick a familiar space and populate it with vivid representations of whatever you want to remember. The odder these images, the better.

Let’s say you need to buy a bag of oranges, then pick up a dog at the pound. Picture walking into your house. Now picture an orange-skinned man standing on your TV wearing a bag as a hat (that’s your bag of oranges). Then mentally travel to your bathroom, where you see a tiny one-pound dog sitting on a scale. You’ve now created a “memory palace” that will make your to-do list very hard to forget.

- Break information into bite-sized chunks

In 1955, psychologist George Miller discovered that most people can only hold about seven “chunks” of information in their head at once. While the precise number varies depending on the context and the individual, scientists agree that the number is relatively small.

Get the most out of your available memory chunks by grouping information intelligently. Let’s say you’re given the numbers “7 4 7 6.” Instead of storing them as four separate chunks, you can transform them into one memorable date: July 4, 1776. Keep doing this, and you’ll be amazed by how much information you can string together.

I know I need the help but I’m not so sure about the orange-skinned man.

When this letter hits your inbox, I’ll have made my way to Penn State and will be playing golf with my son, Matthew, on my childhood course. Dad was a member of Centre Hills Country Club and I played as often as I could. On more than one occasion, I’d be finishing the last hole in the dark with mom waiting in the parking lot. Well, actually she was leaning hard on that old Fiat horn.

I caddied as a kid. $5 a bag. The shoulder straps were thin leather and the old-timers seemed obsessed on keeping a large stash of golf balls in the bag. But $10 for four hours of work was the going rate and I’d listen and learn from the businessmen.

Speaking of memory, I can picture every part of the course in my head. I remember the best shot I hit on a particular hole (not enough of them.) And the time my dad made a 30-foot putt to put us in the championship playoff… and the $750 we each won in pro shop credits. Maybe the highest I’ve ever seen him jump. It’s been years since I’ve been back and haven’t played Centre Hills since dad’s passing. We step forward and now it’s time with Matt. And I can’t wait to play golf with my boy.

NYC is up next early next week. Ned Davis Research and CMG have co-licensed the Ned Davis Research CMG U.S. Large Cap Long/Flat Index to VanEck. We will be doing a video interview to help explain the Index and process. More on this soon.

The economic gathering at Camp Kotok in Maine follows August 3-6. It is an annual fishing trip that brings together some of the brightest investment and economic minds in the business. It is nicknamed the “Shadow Fed” so you might imagine the direction the conversations will go. I hope to be able to share what I learn with you. I’m not sure of the ground rules just yet. Family vacation immediately follows and some needed down time is in order.

I hope you, too, have some vacation time in your immediate future!

Thanks for reading. Have a great weekend!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group