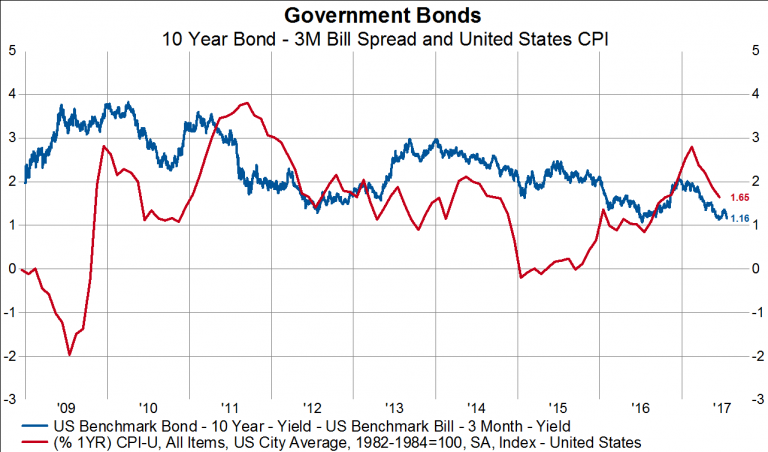

Can Financials be Leadership with a Flattening Yield Curve?

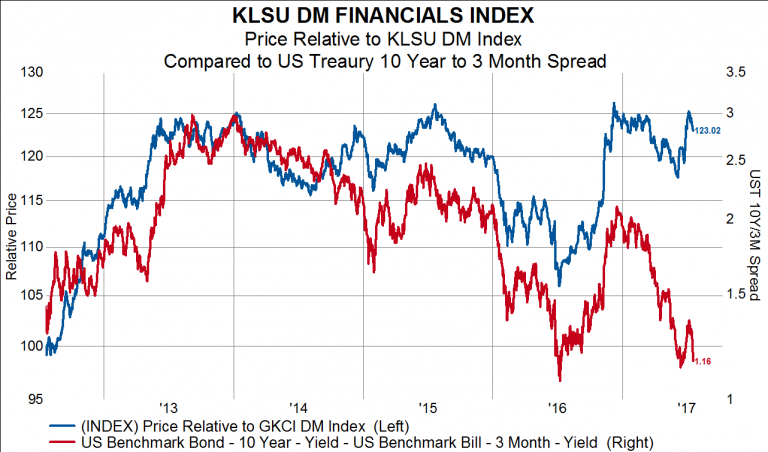

The financial sector has been getting a lot of attention recently with earnings announcements so we thought we’d weigh in on one aspect of financial stock relative performance that is making it difficult for financials to truly lead this market higher: the flattening yield curve. As most of our readers are aware, one way financials in general and banks in particular make money is by capturing the spread between short-term funding costs and long-term lending returns. A nice proxy for the margin that is earned is the 10-year minus 3-month US Treasury yield spread. When the spread is expanding (curve steepening) it implies bumper times for financials and vice versa when it is contracting (curve flattening). Well, after the brief steepening episode that occurred between the middle and end of 2016, the yield curve is back to the flattest it’s been all cycle, and flattening still further. That has, so far in 2017, been an impediment to financial stock relative performance and has kept the group from breaking out of its range-bound trend (chart 1).

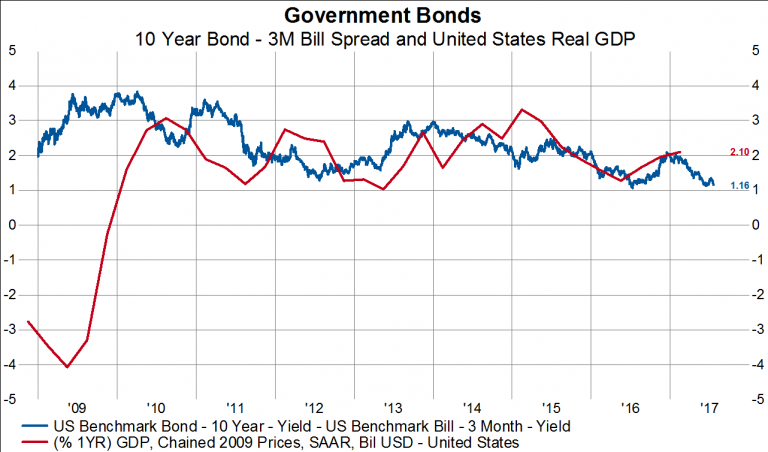

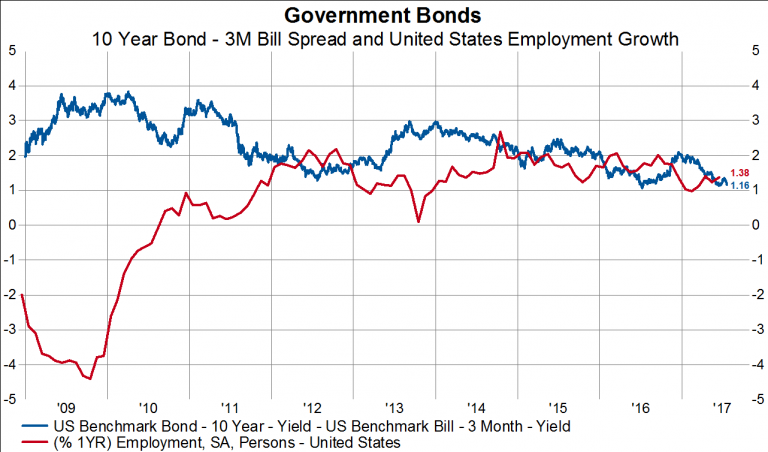

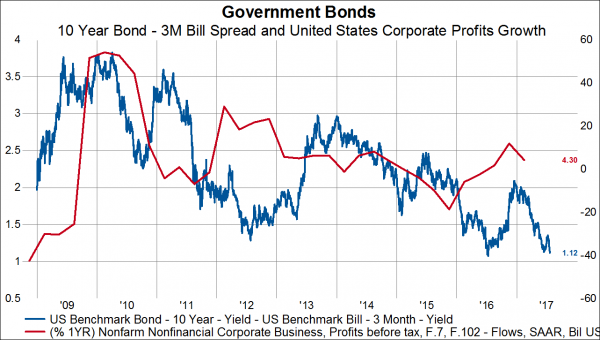

So the obvious question for financial stock bulls is what would it take to get a steeper yield curve? At this stage in the cycle a steeper yield curve could be generate by the economy producing higher inflation or higher real growth. As charts 2 and 3 demonstrate, the there is a tight relationship between both inflation and real GDP growth and the yield curve. Inflation has been trending lower since 2011 and real GDP growth has been trending lower since 1Q15. Unfortunately, we don’t think that is about to change. Indeed, employment (one important component of output) has been trending lower on a year over year basis since the end of 2014, and corporate profit growth (one component of employment) remains weak and looks to be headed lower. These things should keep a lid on the yield curve, and may thus impeded financials from sustainably leading this bull market.