Fed Chair Janet Yellen covered no new ground in her monetary policy testimony to Congress, but that didn’t stop financial market participants from trying. While the CPI report drew a closer focus, past inflation figures don’t tell us a lot about future inflation. Retail sales for June disappointed, but inflation-adjusted wage growth is picking up, which should provide some support in the near term. Fed policy will remain data-dependent, and there’s not enough evidence to suggest that the expectation of moderate growth will prove wrong.

“The [FOMC] continues to expect that the evolution of the economy will warrant gradual increases in the federal funds rate over time to achieve and maintain maximum employment and stable prices. That expectation is based on our view that the federal funds rate remains somewhat below its neutral level – that is, the level of the federal funds rate that is neither expansionary nor contractionary and keeps the economy operating on an even keel. Because the neutral rate is currently quite low by historical standards, the federal funds rate would not have to rise all that much further to get to a neutral policy stance. But because we also anticipate that the factors that are currently holding down the neutral rate will diminish somewhat over time, additional gradual rate hikes are likely to be appropriate over the next few years to sustain the economic expansion and return inflation to our 2% goal. Even so, the Committee continues to anticipate that the longer-run neutral level of the federal funds rate is likely to remain below levels that prevailed in previous decades.” – Janet Yellen, July 12

Monetary policy is currently accommodative, but the federal funds target rate is not far from what one would consider to be a neutral rate. However, the Fed expects the neutral rate to rise over time, compelling policymakers to chase it gradually higher over the next few years (to remain near neutral).

In the first quarter, the year-over-year change in the core CPI was trending over 2%, leading some to believe that the Fed was perhaps “falling behind the curve,” but inflation figures are often misleading at the start of the year. The core CPI is now up 1.7% from a year ago, leading some to believe that the Fed is “failing on its inflation goal.” Chair Yellen and other Fed officials have pointed to “transitory factors” keeping the inflation figure low. Notably, wireless telecom services, which account for just 1.5% of the overall CPI, have fallen sharply – and if excluded, year-over-year core inflation would be trending closer to the Fed’s 2% goal. Hence, the Fed’s expectations that inflation will move toward the 2% goal still appear to be valid.

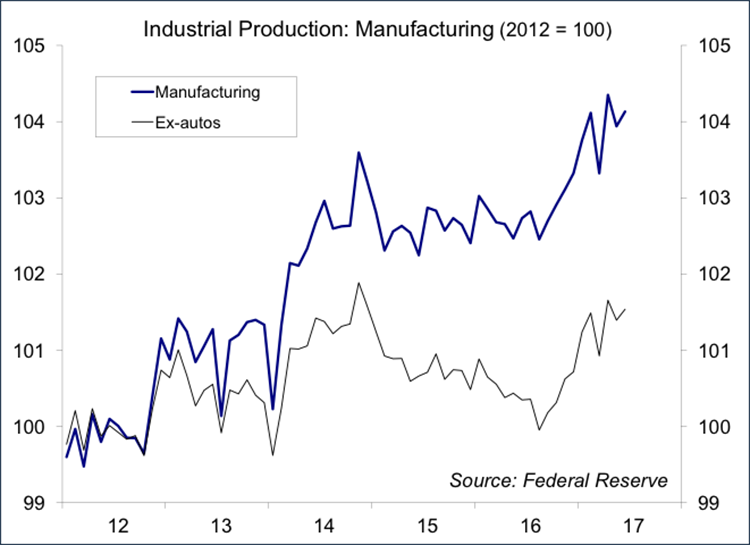

Retail sales were expected to have risen meagerly in June, but the report showed a decline. Unit auto sales had already been reported to have fallen further in June – the pace likely settling to a sustainable level, with some tightening of credit at the low end of the scale. Higher gasoline prices reduced consumer purchasing power in the first few months of the year. However, inflation-adjusted wage growth has picked up (+0.8% y/y).

The current economic expansion has now entered its ninth year. The likelihood of a recession does not depend on the length of the expansion. We are never “due” for a downturn. Economic expansions typically end with efforts to curtail excessive growth in credit. That does not describe the current situation, but there is some risk that the Fed may overdo it in raising short-term rates in the months and quarters ahead.