One (more) Reason to Expect the USD to Continue to Fall

The USD is weak again today and plunging lows not seen for 15 months. The “obvious” reasons for the USD weakness include converging foreign economic activity, more hawkish foreign monetary policies, and a general overvaluation of USD. All of those reasons we outlined here. Yet, another less obvious catalyst for USD weakness is taking shape right here at home: the ballooning US government budget deficit.

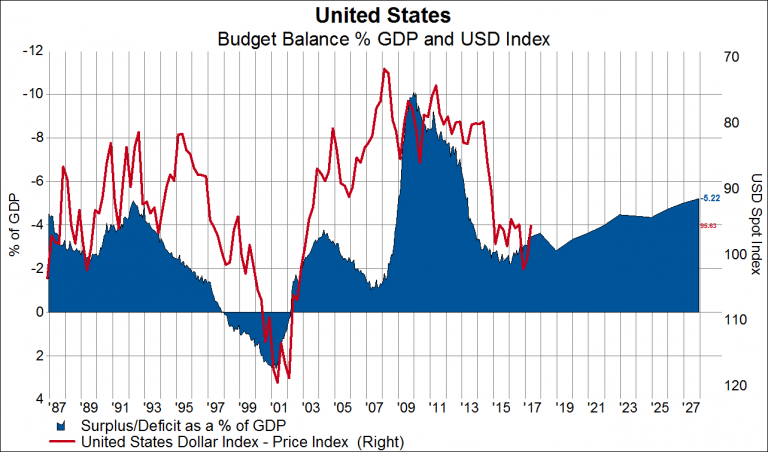

The Congressional Budget Office (CBO) released in June new estimates for GDP and the budget balance through 2027. The estimates were based on current law, meaning that health care and tax reform were not considered. With health care reform all but dead as of today, a big variable is removed from the equation. Taxes are still a bogie and may or may not increase the budget deficit (tax reform as it’s being proposed is unlikely to reduce it). But, the main takeaway from the estimates is that the budget deficit is on track to increase to 5.2% of GDP over the next ten years compared to about 3.4% today. Importantly, the CBO does not forecast recessions and we are eight years into this expansion, making it one of the longest in US history. A recession would be accompanied by fiscal policy expansion, not contraction, and thus would necessarily increase the budget deficit relative to current projections.

So why all this talk about the budget deficit? The US fiscal position is highly correlated to the level of the US dollar index. If history is a guide, an expanding budget deficit would likely be accompanied by a falling USD. In the chart below we plot the US budget deficit/surplus (blue area, left axis, inverted) against the USD spot index (red line, right axis, inverted). We can see that over long periods of time this relationship holds quite closely.