Anyone thinking that we may get a repeat of the spectacular 2001-2008 and 2009-2011 rallies in commodities may have to think again, at least that’s what’s being hinted at by many of the long-term technical indicators. You could say it depends on what the definition of the word “is” is, to quote a well-known Clintonian expression. In this case, it all depends on what the direction of the secular trend is, as we explain later.

What is the secular trend?

Since recorded history, which in the case of US commodities, began in the early nineteenth century, prices have swung in clearly definable very long-term or secular trends. These price movements have approximated between 18-20-years and embraced several business cycles. They arise because of huge swings in under and over capacity. Over capacity develops after many years of upward price pressures, that attract both new productive investment and the aggressive substitution of cheaper materials. This excess capacity does not suddenly appear, but takes several years to develop. Once on stream, it usually takes a couple of decades to work off. During that process, industrial commodity prices either decline, or experience a lengthy trading range.

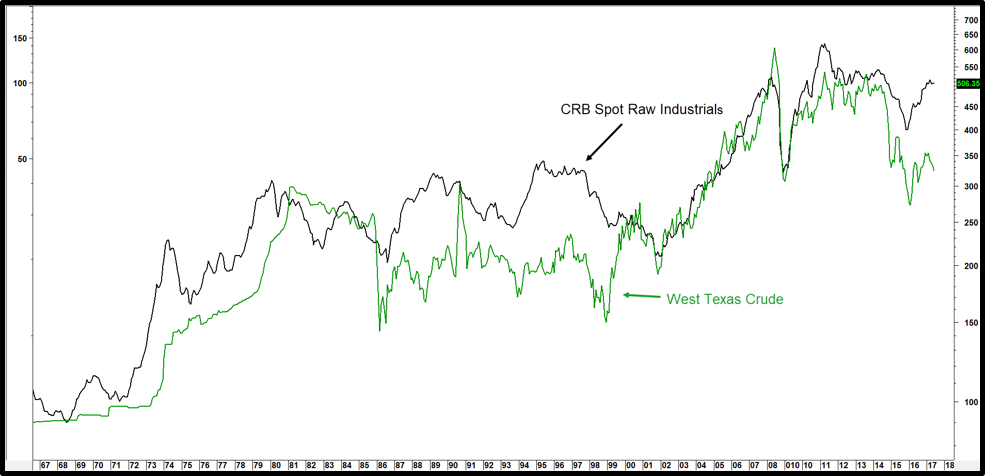

Recent history of the energy sector offers a great example. In the 2004 to 2008 period, supply constraints and growing demand for energy in China, drove up prices. OPEC also helped maintain them at an artificially elevated level. The market was eventually pressured, as those high prices naturally, incentivized greater conservation. From a supply aspect, high prices encouraged drilling, as the international rig count more than tripled between 1999 and 2012. Substitutes, in the form of renewables, also exploded, though admittedly from a small base. Fracking was the big elephant in the room. The technology that drove it, together with an improved regulatory environment in the US, will continue to bend its cost curve and cap prices. Oil, is just one commodity of course, but Chart 1 shows how closely its price is intertwined with other industrial commodities, especially since 2001.

Chart 1 Oil versus Industrial Commodities

Oil and industrial commodity price movements are linked.

Secular trends are not only important because of the giant swings in prices that they embrace. Equally significant, is the fact that the direction of the secular trend determines the characteristics of the business cycle price swings that fall under it. These primary trend movements generally range between 9-months -2-years. When the secular trend is rising, primary bull markets tend to last longer and are much stronger, whilst counter-cyclical. downtrends are generally contained. The opposite is true during a secular bear market, where rallies are limited in scope and price magnitude is on the downside. Alternatively, some secular “bears” take the form of a multi-year trading range.

There are two aspects to this. First, if the direction of the secular trend is known, we can on the lookout for momentum characteristics that are associated with that trend. Second, if a specific characteristic is spotted and that characteristic is typical bear market behavior, we have a piece of evidence that supports the idea that it actually is a bear market and vice versa. If it walks like a bear and quacks like a bear it probably is a bear!

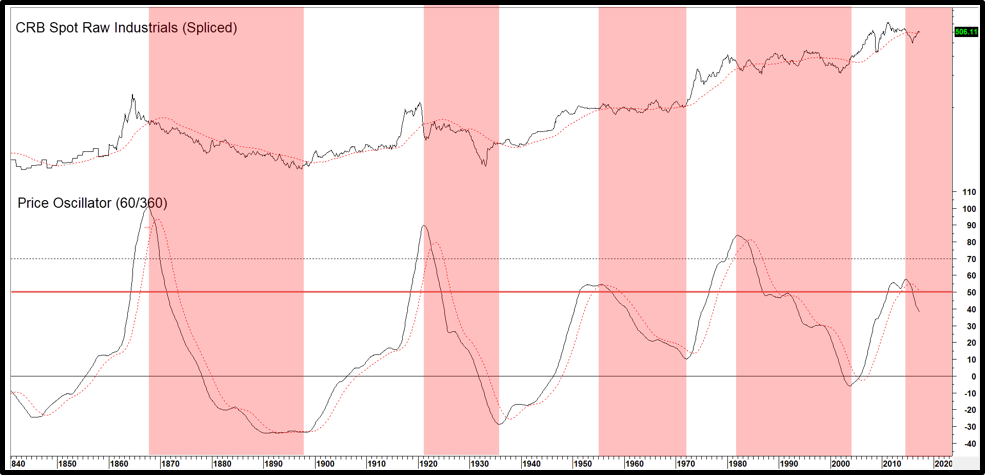

No indicator is perfect, and attempting to identify long-term trends means that most signals are triggered several years after the actual turning point. Bearing that in mind, the lower panel of Chart 2 features our “secular oscillator”. This is a measure of long-term momentum that compares two moving averages, a 60-month divided by a 360-month. When it is above its (red) 48-month MA it is signaling a secular bull market and vice versa. The first thing to note, is that all previous secular peaks were signaled when the oscillator rallied above the red horizontal line and started to reverse. At that point, price action indicates that sufficient time has elapsed from which a condition of long-term overcapacity has been generated. Four instances occurred between 1860 and 1980. Two were followed by a bear market, and two by a multi-decade trading range. A fifth signal, developed in 2012. If that bear trend ended in 2016 it would be the shortest in history, well below the 18-20-year average. Based on that metric alone it would seem that there is more corrective action to come.

Chart 2 CRB Spot Raw Industrials versus a Secular Momentum Indicator

When the indicator peaks from a reading above +50% a secular commodity bear is signaled.

The oscillator is also useful in objectively identifying the status of the prevailing secular trend by observing its direction. In this respect, the pink shaded areas flag secular bear markets. These have been demarcated with the benefit of hindsight by taking the periods between the approximate oscillator peaks and troughs. Since it is currently declining, the trend, by this measure, is bearish.

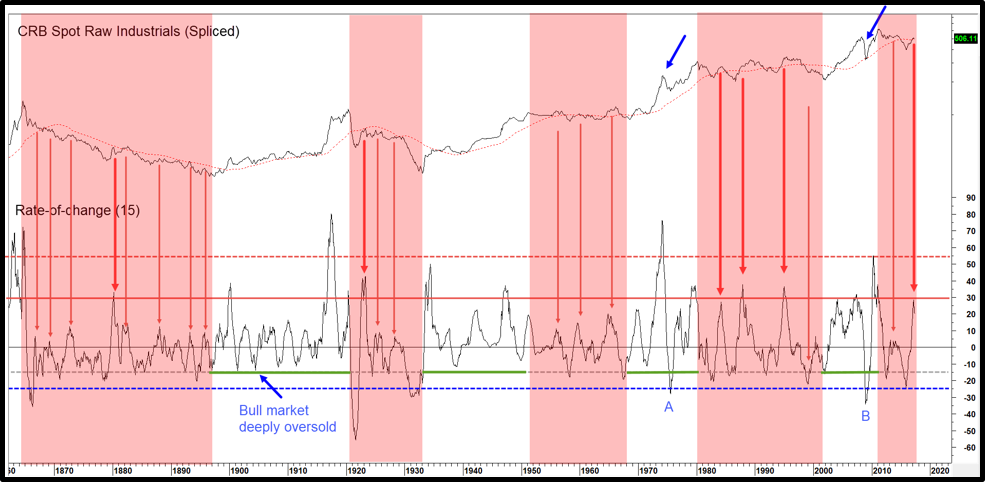

Chart 3 substitutes a 15-month rate of change (ROC) of the CRB Spot Raw Industrials in place of the price oscillator. The first thing to notice is that four of the previous five secular peaks were signaled by the ROC reversing from at or above the (dashed) red horizontal line at +55%. Second, on most occasions when this indicator has fallen to or below the deeply oversold blue dashed line at-25%, as was the case in 2016, the secular trend was bearish. There were two exceptions at points A and B, but these developed as shakeout moves following a strong advance, when the oscillator in Chart 2, was in a bullish mode, not bearish as it is now. Third, the behavior of the ROC under a secular bear market environment is also revealing. That’s because counter-cyclical rallies have generally been unable to record readings much above the +30% barrier. When they did, the initial upside penetration signaled, that for all intents and purposes, the advance was over. These instances have been flagged by the six thick red arrows. The thin red ones, tell us that in most situations, ROC rallies amount to very little in terms of magnitude when the secular trend is bearish.

Chart 3 CRB Spot Raw Industrials versus a 15-month Rate of Change

When the ROC reaches +30% in a secular bear that’s usually the end of the primary bull market.

Since the price oscillator in Chart 2, is still overstretched and well below its 48-month MA, there is a better than even chance that the secular bear market is still in force. If past is prolog, that means that the primary or cyclical commodity bull market that began in October 2015 is either over, or very close to it. In other words, the most likely outcome as the year unfolds, is for a new leg down in the secular bear market. Alternatively, we could see a probing of the 2016 low, as part of a multi-decade trading range.

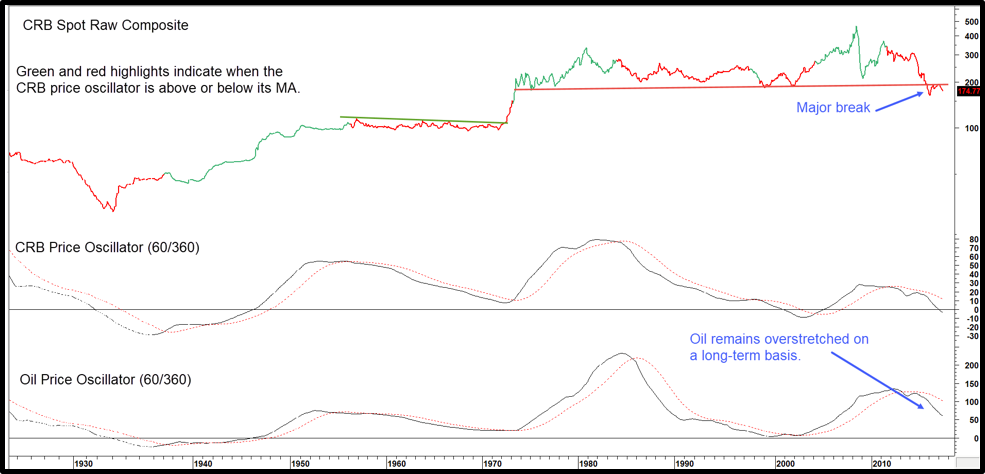

Chart 4 tells us that the secular bear is not solely confined to industrial commodities as a similar oscillator for the more broadly based CRB Composite is also in a declining mode. Note, that a secular oscillator for West Texas Crude (bottom window), is also in a negative trend and at an overstretched reading. The CRB Composite itself has violated a multi-decade support trendline, which has now reversed its role to one of resistance. The Index has so far failed in two attempts to rally back above it. This further hints that the cyclical recovery rally may be over.

Chart 4 CRB Composite versus The West Texas Crude

The CRB Composite and oil are both in secular bear markets.

Conclusion

If the longer-term indicators are accurate in their identification of a secular bear market or trading range for commodities, any upside potential for the current primary bull market is probably limited. It seems more likely though, prices may have already peaked. For those concerned about equities, history shows that a gentle decline in commodity prices is generally bullish. On the other hand, severe commodity price drops are quite negative. Right now, most global leading economic indicators continue to edge higher. That means, that if our analysis of the commodity picture is valid, any expected weakness will be contained, therefore enabling equities to extend their upward march.

Martin J. Pring

July 3 2017

Disclosure: The views expressed in this article are those of the author and do not necessarily reflect the position or opinion of Pring Turner Capital Group or its affiliates.

© Pring Turner Capital Group

© Pring Turner Capital Group

Read more commentaries by Pring Turner Capital Group