The June Employment Report was about as much as stock market participants could have hoped for. Nonfarm payrolls rose more than expected, helping to offset fears that the economy is weakening. However, job growth was not too strong and wage inflation remained moderate, reducing fears that the Fed might be forced to raise short-term interest rates more aggressively. If this moderate-growth backdrop sounds familiar, that’s because we’ve lived with it for some time now, and that’s been a relatively good environment for investors.

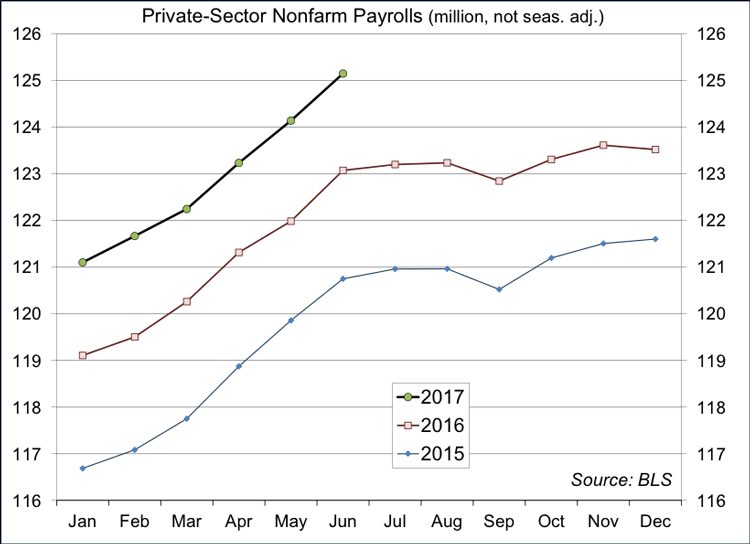

Nonfarm payrolls rose by 222,000 in June, more than anticipated, with a net revision of +47,000 to April and May. The June surprise was partly due to a 35,000 gain in government jobs (mostly local, and surprisingly, not education). Note that, prior to seasonal adjustment, the economy lost 952,000 education jobs (public and private-sector) in June and added 1.551 million non-education jobs – roughly in line with what we saw in June 2016. Private-sector (adjusted) payrolls rose by 187,000, not far from the median forecast (+172,000), leaving the first-half average at +171,000 (vs. a +170,000 average for all of 2016). Retail payrolls rose by a lackluster 8,100, but that followed four consecutive months of declines (up 0.1% y/y).

We need less than 100,000 payrolls gains per month to be consistent with the growth in the working-age population. We can run higher than that now because we are still working off the slack created during the Great Recession. How much slack remains in the job market is difficult to determine, as demographic changes (an aging population) have reduced labor force participation. As the job market picks up, we normally see individuals come back into the labor force, but that ought to be limited (again, due to the demographics). The degree of underemployment is also difficult to gauge. Involuntary part-time unemployment has been trending lower.

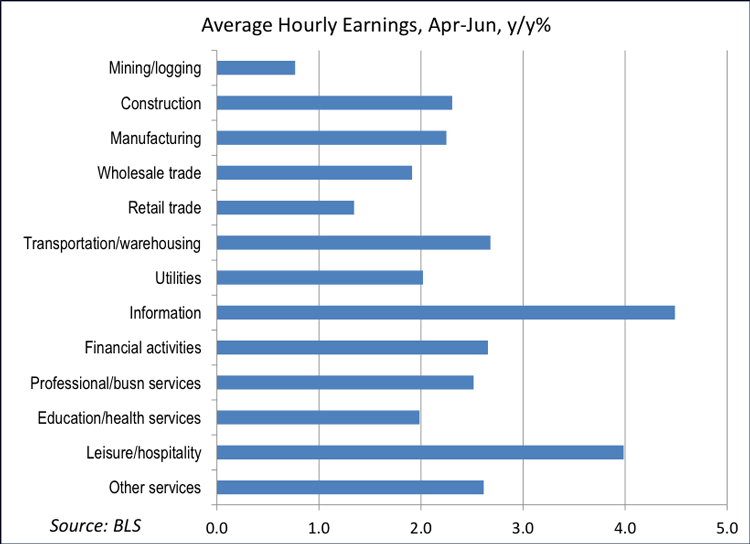

Tighter job market conditions should eventually lead to higher wage inflation. Average hourly earnings are now trending at 2.5% year-over-year – good, but not especially strong, and somewhat surprising given the low unemployment rate (4.4%). That could be due to better job growth in lower-paying industries. The AHE figure is subject to shifts in the composition of jobs, but the Employment Cost Index (2Q data due July 28) is not. As expected, 2Q17-over-2Q16 wage growth is elevated in the information sector and weak in the retail sector, but mixed otherwise (what’s up with leisure and hospitality?).

There are a number of possible explanations for why wage growth has been limited. Firms continue to emphasize cost containment and aren’t giving away wage hikes much beyond consumer price inflation, unless the employee has one foot out the door. Workers may be accepting lower salary increases to keep their health insurance. The Fed believe that wage growth may have been held down by the weak pace of productivity growth. Whatever the case, the near-term economic backdrop remains favorable: continued growth, but not too strong.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.