“Change of a long-term trend is usually gradual enough that it is obscured by the noise caused by short-term volatility. By the time secular trends are even acknowledged by the majority they are generally obvious and mature. In the early stages of a new secular paradigm, therefore, most are conditioned to hear only the short-term noise they have been conditioned to respond to by the prior existing condition. Moreover, in a shift of long-term significance, the markets will be adapting to a new set of rules while most market participants will be still playing by the old rules.”

* Robert Farrell, Former Chief Stock Market Analyst Merrill Lynch

I listened to Bob Farrell several times a week. Bob was the chief stock market analyst at Merrill Lynch. Do you remember those old “squawk boxes?” On my desk sat a small speaker box. It was the firm’s way of communicating to the thousands of brokers. I’d keep the volume low but when Farrell stepped to the mic, I’d turn the knob to the right. His deep monotone voice would fill my cubical and echo in the office around me. As a young broker, I had little idea as to the way of the financial world. I hung on his every word.

Bob was unique on Wall Street. Most firms pushed out product that had recently worked. Easier to sell, as you might imagine, but rarely worked as those gains were in the past. But Bob was different. He had the trust and the respect and a track record of success that enabled his superiors to let him speak his mind. Following his advice served broker and client well. We investors need to be forward looking. Unfortunately, most are not.

When your caddy is advising you to buy Facebook stock, as mine did recently; or when cab drivers are driving around with quote trek machines trading stocks, as they were in 1999; or when waiters and waitresses are flipping investment properties with access to no-doc mortgages, as they were in 2007, you can’t help but scratch your head knowing that this time isn’t different. Today we have debt and demographics issues. Asset prices most everywhere are overvalued.

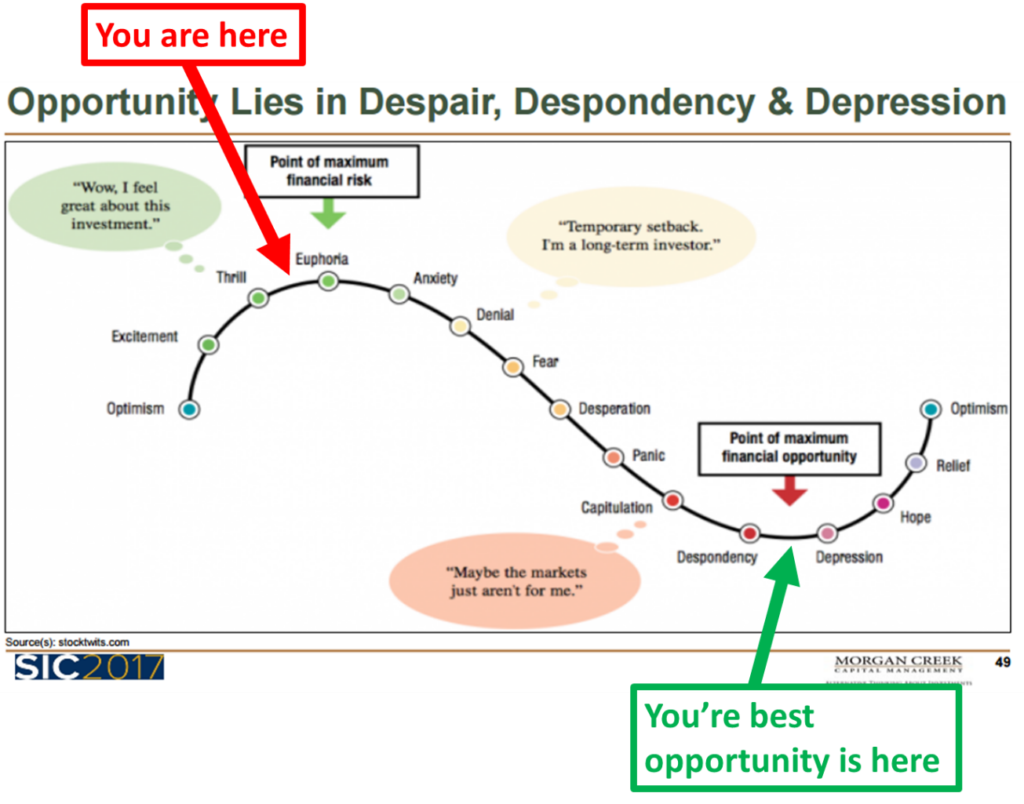

Buy low, sell high. Yep. Got it. Bob Farrell’s sage advice, if captured in a picture, might look like this:

Your starting point conditions matter. In 2009, forward return expectations were in the mid-teens. But really, who do you know that was buying. Certainly not the caddies and cabbies. They couldn’t click the sell button fast enough. It was pure panic.

Forward 10-year equity market returns are in the low single digits. I’ll update those charts for you next week. There is no way that bonds can help your portfolio like they have over the last 35 years. Not a lot of get to be gotten from low 2.20% yields. We need to do our best to get our clients from “you are here” to “you’re best opportunity is here.”

On the way to that opportunity, keep in mind that “It’s all about the Fed and it’s always all about the Fed.” They’ve shifted gears… that wind is no longer at our backs. As a quick aside, Mauldin wrote a thoughtful piece last week titled, “Mad Hawk Disease Strikes Federal Reserve.” He writes,

While my rant last summer was about the Fed’s apparent willingness to embrace negative rates, we now face the opposite risk. Janet Yellen & Co. are asserting that inflation is such a serious threat that they must tighten policy with a two-pronged approach. They are already raising the federal funds rate and will soon begin reducing the massive bond portfolio accumulated in the QE years.

I don’t think these moves will create a crisis on their own. Rather, I think the mentality that they reveal may lead to much bigger mistakes when the next recession arrives. The mistakes may already be unfolding.

When our initial starting conditions are high valuations and low bond yields; well, Bob Farrell says it best, “…in a shift of long-term significance, the markets will be adapting to a new set of rules while most market participants will be still playing by the old rules.” It’s what happened in 1999 and again in 2007. It’s what’s happening again today.

Ok Steve, what do I do? First, it’s important to know that there are ways to make money in periods like 2000-2002 and 2008-09. One doesn’t have to sit on the tracks and get run over by the oncoming train. I have some ideas for you to consider. I advise you to do some research and set a clear game plan in place.

So today, let’s first look at some research in order to set the “you get from here to there in good shape” case and then I’ll share what I am personally doing with my portfolio. Hint: “Investors need risk management in bear markets, not in bull markets,” Ned Davis. Hint: Let the trend be your friend.

Grab that coffee and find that favorite chair. Hopefully, a beach chair. And do have a great holiday weekend.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- A Century of Evidence on Trend-Following Investing

- What I’m Personally Doing to Get From Here to There

- Trade Signals — Risk of U.S. Recession Low; Equity Cyclical Bull Market Intact; Bullish Signal on Bonds

- Concluding Thought

- Personal Note

A Century of Evidence on Trend-Following Investing

Let me begin this section by saying that I am biased. I’m a trend follower and have been since I founded my business in 1992. Maybe I was just optimistic when I started but many years and a track record I’m proud of tells me it works.

In recent years, there has been a proliferation of academic research that evidences the positive benefits of trend following. The reason is tied to our human behavioral tendencies as Bob Farrell taught me years ago. I’m not sure why but we humans seem to wash, rinse, repeat and in that is yours and my opportunity.

If you’d like to take the deep dive into the research paper by Brian Hurst, Yao Hua Ooi and Lasse Heje Pedersen, you can find the link here. I’ll try to save you some time and hit the high level points. If opportunity lies in despair not euphoria then how can we get to despair without being in despair ourselves. My point is there are times to play offense and times to play defense. And trend-following can help us both participate in up and protect in down.

My summary bullet points from A Century of Evidence on Trend-Following Investing:

Let’s begin with their conclusion:

- Trend-following investing has performed well in each decade over more than a century as far back as we can get reliable return data for several markets. Our analysis provides significant out-of-sample evidence across markets and asset classes beyond the substantial evidence already in literature. Further, we find that a trend-following strategy has performed relatively similarly across a variety of economic environments, and provided significant diversification benefits to a traditional allocation. This consistent long-term evidence suggests that trends are pervasive features of global markets.

Further, they find:

- In each decade since 1880, trend following has delivered positive average returns with low correlation to traditional asset classes.

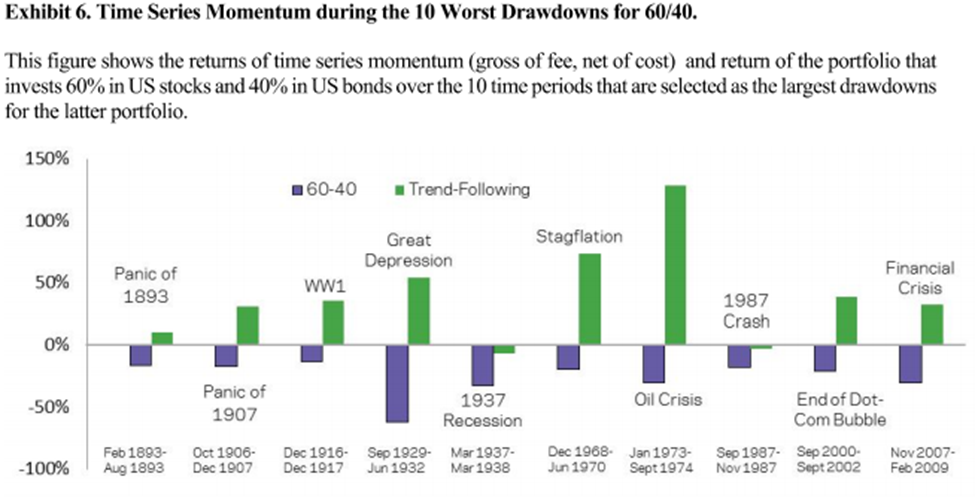

- Trend following has performed well in 8 out of 10 of the largest crisis periods over the century as defined as the largest drawdowns for a 60/40 stock/bond portfolio.

- Trend following has performed well across different macro environments, including recessions and booms, war and peacetime, high and low interest rate regimes and high and low inflation periods.

- As an investment style, trend following has existed for a very long time. Some 200 years ago, economist David Ricardo’s imperative to “cut short your losses” and “let your profits run on” suggests an attention to trends.

The most basic trend-following strategy is Time Series Momentum. Essentially that means:

- Going long markets with recent positive returns and shorting those with recent negative returns.

- Literature shows that time series momentum or trend following has been profitable on average since 1985 for nearly all equity index futures, fixed income futures, commodity futures and currency forwards.

- The authors find that trend following has been consistently profitable throughout the past 137 years.

Here is what the authors studied:

- The analysis used monthly returns for 67 markets across four major asset classes: 29 commodities, 11 equity indices, 15 bond markets and 12 currency pairs.

- They combined a large number of existing data sets and hand-collected new data that has not been previously studied (transcribing data from the “Annual Report of the Trade and Commerce of the Chicago Board of Trade” dating back to 1877.)

- For the study, they used end of month prices and returns.

Base study:

- They created a simple time series momentum strategy that added to the work of Moskowitz, Ooi and Pedersen [2012] and Hurst, Ooi and Pedersen [2013].

- What’s important is that they add to that prior evidence by taking the same rules and applying the trading rules to periods farther back in time than was previously studied.

- For quant geeks this is called “out-of-sample” testing of those prior papers.

Strategy rules:

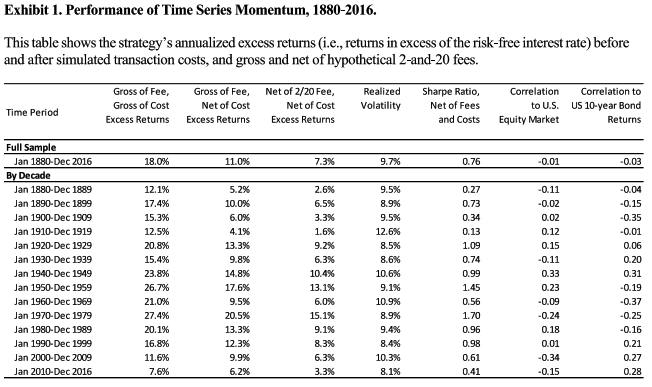

- The authors construct an equal weighted combination of 1-month, 3-month and 12-month time series momentum strategies for the 67 markets cited above from 1880 through December 2016.

- For each of the three measurement periods (1, 3 and 12 months), the position taken in each market is determined by assessing the past return in the market over the 1, 3 and 12 month look back measurement periods.

- A positive past excess return is considered an “up” trend and leads to a long position.

- A negative past excess return is considered a “down” trend and leads to a short position.

- Therefore, each strategy holds one long position and a short position in every market. Move forward a month, run the momentum again and reposition in the strongest price trend and short the weakest price trend.

- They do some volatility scaling to target a 10% vol target. This is done to target a consistent amount of risk over time, regardless of the number of markets that are traded at each point in time. (Don’t get too hung up on what this means – we can discuss at a later time.)

- Finally, the authors subtract transaction costs and fees. Meaning they report the hypothetical performance net of a hedge fund like 2% (base fee) and 20% (incentive fee) and they deduct what they feel might be reasonable trading costs.

Performance:

- Exhibit 1. Performance of Time Series Momentum, 1880 – 2016

- Next is a look at the 10 worst drawdowns for 60/40 and how the simple time series momentum process the authors used in their study compared:

Every single recession in the last 100 years has been lead with a Fed tightening cycle. We are four rate hikes into the current cycle.

When you think about how to invest for the period ahead, simply know that there are a number of ways to navigate the waters. And hopefully profit. Let’s end this section where we began:

- Trend-following investing has performed well in each decade over more than a century as far back as we can get reliable return data for several markets. Our analysis provides significant out-of-sample evidence across markets and asset classes beyond the substantial evidence already in literature. Further, we find that a trend-following strategy has performed relatively similarly across a variety of economic environments, and provided significant diversification benefits to a traditional allocation. This consistent long-term evidence suggests that trends are pervasive features of global markets.

Next, I share a few ideas.

What I’m Personally Doing to Get from Here to There

“The biggest unknowable is that you have the illusion of liquidity. You have people who promise overnight liquidity that have taken quite illiquid positions, particularly lending to various entities. As long as the party continues that’s fine, but should this liquidity be tested it’s not going to be as deep as people think.” – Mohamed El-Erian

My personal goal is to get from this side, what Mauldin has termed, “The Great Reset”, to the other side. I’m 56 years old and though I have most of my wealth in my business, I do have my and Susan’s personal assets.

I believe there are times to play more defense than offense and times to play more offense than defense. I believe in broad asset class diversification. To which end, I think in terms of three asset buckets – equities, fixed income and liquid alternatives.

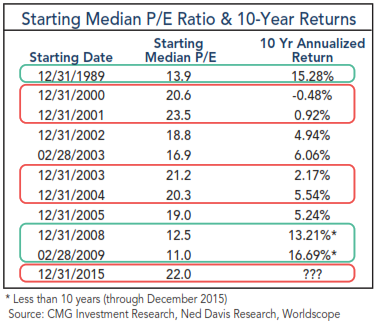

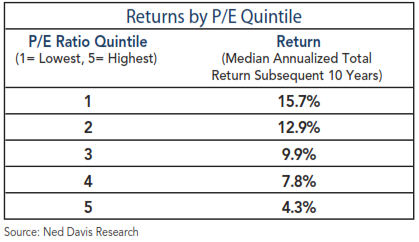

I also believe that your initial starting conditions matter. By this I mean, that I’d rather be overweight long equities when valuations are attractive. For example, here is a look at starting point valuations and what the subsequent 10-year annualized nominal returns turned out to be:

If you sorted all Median PEs into quintiles, most attractive to least attractive, it looks like this (data 1926 to present):

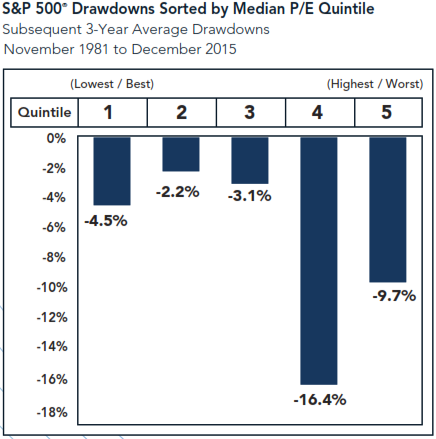

The problem is, and I believe will be again this next recession, that the really big declines come when the market is most expensively prices (Quintiles 4 and 5). Unfortunately, we sit firmly in Quintile 5 today:

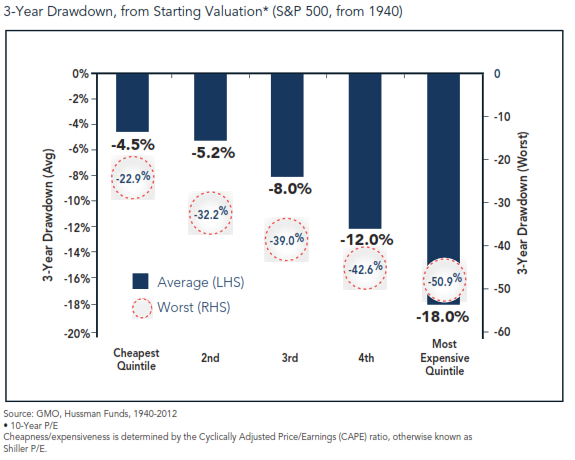

Here is another look but this time using Shiller PE data:

So my strategy is to overweight equities when, as Warren Buffet has said, “the hamburgers are cheap.” That’s when we can buy a lot for our money. And underweight equity exposure when they are expensive.

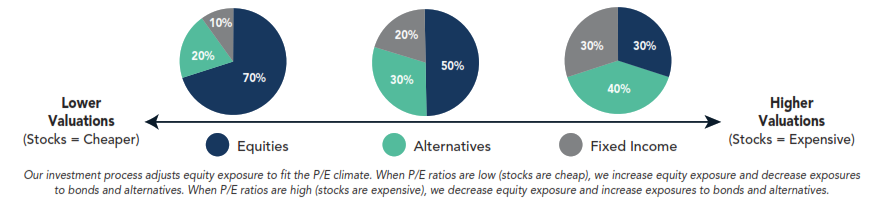

But valuations tell us little about timing. A bull market may run longer than what our personal views might suggest so I favor rules-based “trend following” processes to do my best to both participate and protect. Nothing is perfect in this business so I diversify to different trading strategies.

I favor a rules-based game plan that decreases my equity exposure when valuations are high (right hand side of the next chart) and gets me overweight equities when the getting gets good again (and it will). It looks like this:

My current portfolio is 30% equities, 30% fixed income and 40% to liquid ETF trading strategies. Every component is tactically managed utilizing liquid funds and ETFs with the intention to participate in growth and protect downside. It looks like this:

30% Equities

- 10% NDR CMG U.S. Large Cap Long/Flat Strategy (U.S. large cap exposure)

- 10% CMG Tactical Equity Strategy (U.S. and global exposures via ETFs)

- 10% CMG Beta Rotation Strategy (Vanguard Total Stock ETF or Utility ETF)

30% Fixed Income

- 10% CMG Managed HY Bond Program (trend following, HY or cash)

- 20% CMG Tactical Fixed Income Strategy (currently holding Treasury bonds and Muni bonds)

40% Liquid Alternatives (ETF trading strategies)

- 25% Mauldin Solutions Core Strategy (global tactical – broad assets classes)

- 10% CMG Tactical All Asset Strategy (global tactical – broad assets classes)

- 5% Gold ETF

Each week I post a number of our indicators in Trade Signals. Despite my overvalued, overbought, over leveraged watch out for the Fed view, the markets may continue higher. I want to participate yet protect. Well researched rules based investment processes may help. One has to have deep confidence in the processes and I do. I write about risk each week in On My Radar but it is the risk managed processes I stick to that has kept me invested in equities, global equities and even fixed income when the majority of analysts have been calling for higher interest rates. Of course, some strategies have performed better than others. But collectively I believe this diversified process can help get me to the next exceedingly attractive equity market buying opportunity. I will adjust my mix and significantly overweight to more traditional long equities then.

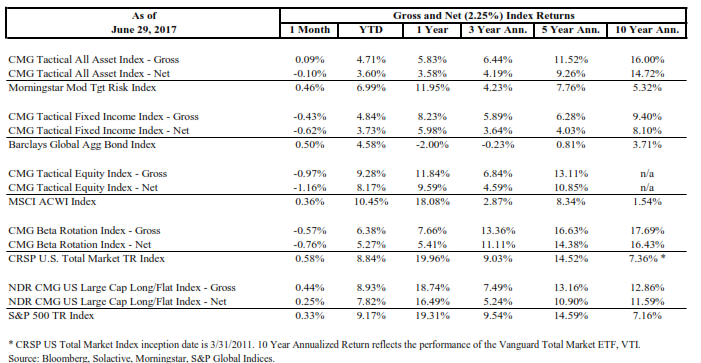

Here is a look at the most recent index performance:

If I were smart enough to know, I should have gone 100% to the NDR CMG U.S. Large Cap Long/Flat Strategy and I would have done better over the last year than any of the other strategies performed. I’m thrilled with how the CMG Tactical Fixed Income Strategy performed over the last year in comparison to the bond market in general. Plus 8.23% gross vs. -2.00% gross.

There are more aggressive ways to generate return. For example, I could allocate only to the three equity strategies. Much depends on the risk one is willing to take. I put my money in the same things I recommend to my clients. I believe in the processes and I believe it is the right thing to do. I diversify because I just don’t know what strategy will outperform and when.

The above are hypothetical index-based returns shown both gross and net of a max fee. Past performance cannot predict or guarantee future performance. All investing involves risk. You can follow the NDR CMG U.S. Large Cap Long/Flat Index, independently calculated by S&P Dow Jones Indices here. You can follow all of the other indices calculated by Solactive here. And you can learn more about some of the processes in the Trade Signals section next. See important disclosures below.

I believe Ned Davis said it best. You have to invest differently in bear markets than you do in bull markets. Knowing when can be challenging. Valuations can tell us a lot about coming 10-year returns and right now they don’t look so good. GMO is projecting -4% real annualized returns over the coming seven years. This bull will end but no one can tell you when. I have put forward what I believe is the best way for me to get from here to the next great buying opportunity. There are, of course, many ways to invest. Find something you believe in and can stick to.

Trade Signals — Risk of U.S. Recession Low; Equity Cyclical Bull Market Intact; Bullish Signals on Bonds

S&P 500 Index — 2,419 (6-28-2017)

Notable this week:

The short-term Gold Model moved to a sell. The longer-term trend remains bullish. The Ned Davis Research CMG U.S. Large Cap Long/Flat Index remains in a partial sell signal moving from 100% S&P 500 Index exposure to 80% S&P 500 Index exposure (with the 20% balance in T-Bills) on Tuesday, June 13, 2017.

80% exposure is bullish, yet there is reason to take note. The Index is signaling weakening market momentum (trend) and market breadth. Bonds remain in a buy signal. The Zweig Bond Model remains in a buy signal and the High Yield trend model remains bearish. The CMG Tactical Fixed Income Strategy is equally allocated to Treasury bonds and Muni bonds.

Inflationary pressures are high. Risk of recessions in the U.S. is low. Global recession risk is now neutral.

Click here for the charts and explanations.

Concluding Thoughts

“Bull markets are born in pessimism, they rise on skepticism, they mature in optimism and they die on euphoria.”

— Sir John Templeton

In 1985, my Merrill Lynch office manager tapped me on the shoulder and told me he needed me to go to a lunch seminar at the Union League in Philadelphia to hear a presentation by Sir John Templeton. I wasn’t happy as I walked the few short blocks as I had many cold calls to make.

Here is one more last look at the behavior chart. I can see Sir John nodding his head and saying, “the secret to my success is I buy when everyone else is selling and sell when everyone else is buying.”

As I noted last week, we have reached euphoria. Red is bad, green is good. Perhaps the early stage but euphoria nonetheless. I wonder what Sir John might make of all the money racing into passive index funds. Bubble?

Personal Note

Today’s my wedding anniversary and Susan and I are heading out to dinner. She’s mending well post-knee surgery and starting to feel like herself again. I’m crazy about her. My gift to her (and me) is a long weekend getaway to a quiet island. Date to be determined.

There is a soccer tournament for her youngest son, Kieran, in Virginia this weekend and golf plans for me with my best friend on the 4th. The bottom end of the table Philadelphia Union has a home game Sunday evening. So peanuts and a cold IPA are in my future and hopefully a win.

Travel is picking up again in July. I was in Austin this past Tuesday meeting with a fixed income ETF manager who is doing some interesting work and visited with an advisor. I like what I saw especially given the challenges of ultra-low bond yields. I’m in Dallas July 8, in Omaha July 11-12, Dallas July 18-19 and from there a direct flight to Chicago for an annual advisor conference. I’m looking forward to seeing some good friends.

Then it’s, as the say in Philly, “down the shore.” Susan, I and the kids are heading to Stone Harbor, New Jersey from August 5-12 for our annual week at the beach. I see some beach volley ball, a good book and Springers ice cream in my near future.

Have a great 4th of July weekend. Celebrate!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group