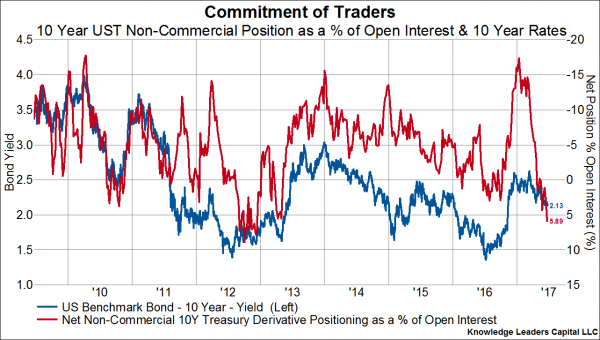

The last six months has seen one of the most incredible changes in investor positioning in 10-year US treasury bonds in recent history. Back in early January, around the time rates peaked, non-commercial traders (AKA speculators) were net short 10-year options and futures contracts by a whopping 17% of open interest. Fast forward to today and speculators are net long 10-year options and futures contracts by a relatively large 6% of open interest. In other words, the net positioning of speculators betting on 10-year rates has undergone a 23% change over the trailing six months. Speculator positioning is useful to analyze because as a group they are often positioned incorrectly at major inflection points. That is to say, by the time all the speculators are on one side of the boat, the move in the subject asset is largely over.

The recent sharp change in positioning is similar to that which occurred between April-October 2010. Over that period speculators moved from a net short 18% of open interest to a net long 4% of open interest (a change of 22%) as rates fell from 4% to 2.4%. The longest speculators have been of 10-year treasury derivatives this cycle was in October 2012 when they were net long about 9% of open interest. Subsequently, the Taper Tantrum helped take rates from 1.4% to 3% and speculator positioning back to 16% short.

We are not exactly bond bears (actually, quite the opposite, as over the next 18-24 months we look towards the culmination of this late cycle environment with an inevitable recession), but the positioning in the derivatives market has our antennae piqued for a tactical trough in rates which may be coinciding with a short-term trough in economic performance.