The June 14 Fed policy decision was expected to overshadow the mid-month economic figures. Instead, the soft data reports contrasted with the relatively more upbeat central bank. Did the Fed make a mistake? Or are the financial markets placing too much emphasis on the short-term data?

The Consumer Price Index fell in May, reflecting a drop in gasoline prices (which, as expected, was amplified by the seasonal adjustment). However, core inflation was also below expectations, reflecting declines in communication, new vehicles, used vehicles, apparel, and alcoholic beverages. Bear in mind that the Fed’s 2% inflation goal is based on the PCE Price Index, which has been trending well below the CPI over the last several months. In her press conference, Chair Yellen noted that the March moderation in the year-over-year pace reflected a large “one-off” reduction in the price index for wireless telecom services – and one would expect the y/y pace to pop a little higher when the March 2017 figures rolls off the 12-month calculation. The CPI data continue to show a sharp divide between core consumer goods (-0.8% y/y), reflecting a continued trend of mild deflation, and non-energy services (+2.6% y/y), which has been led by higher shelter costs (+3.3%). Rent, 7.8% of the overall CPI, rose 3.8% y/y. Homeowners’ equivalent rent, nearly a quarter of the CPI, rose 3.3% y/y.

The Fed’s concern is future inflation, not past inflation. In the Summary of Economic Projections, the median forecast of senior Fed officials for 2017 PCE price inflation was revised down to 1.6% (from a 1.9% estimate in March), but officials continued to see that rising to 2% in 2018 and 2019. So, accounting for the drop in telecom wireless services, the Fed’s inflation outlook isn’t much different than in March. The more immediate concern for the Fed is the tightness in labor market conditions. The median forecast for the 4Q17 unemployment rate was revised down to 4.3% (from 4.5% in March).

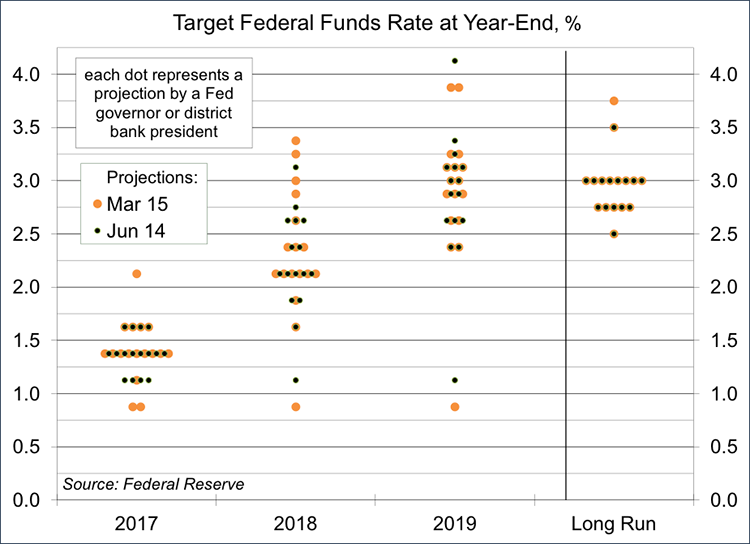

The dots in the dot plot (Fed officials’ projections of the appropriate year-end federal funds rate) did not change much from March. Half of senior Fed officials expect one more rate increase by year end, a quarter expect no further increases, and a quarter anticipate two increases. Note that only nine of those dots represent voting members of the FOMC – and those not voting may tend to be a little more hawkish.

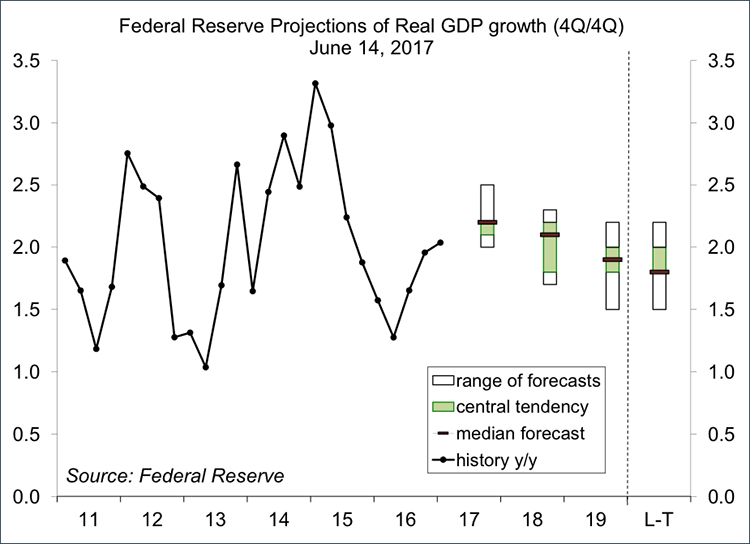

Fed officials still expect real GDP growth of a little over 2% this year, somewhat beyond a sustainable pace (given projected growth in the size of the labor force).

The FOMC indicated that it expects to begin reducing the balance sheet later this year, setting a cap for the monthly run-off (initially $10 billion, rising gradually to $50 billion). Note that the pace of run-off should be less important than the total amount of run-off, which is unknown. While the initial pace of run-off is relatively low and should not be unsettling for the markets, it’ll hit its full stride in a little more than a year – and at $600 billion per year, that pace seems likely to be too rapid.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James