On My Radar: Mark Yusko’s Ten Surprises — Notes from the 2017 SIC (Part 3)

Learn more about this firm“Your job as investors is to feel sick to your stomach.

Do not invest when you are excited and everything is great… go shopping when things go on sale.”

“We will have a recession sometime within the next 12 months. It is not going to be different this time.”

– Mark Yusko, Morgan Creek Capital Management

2017 Strategic Investment Conference

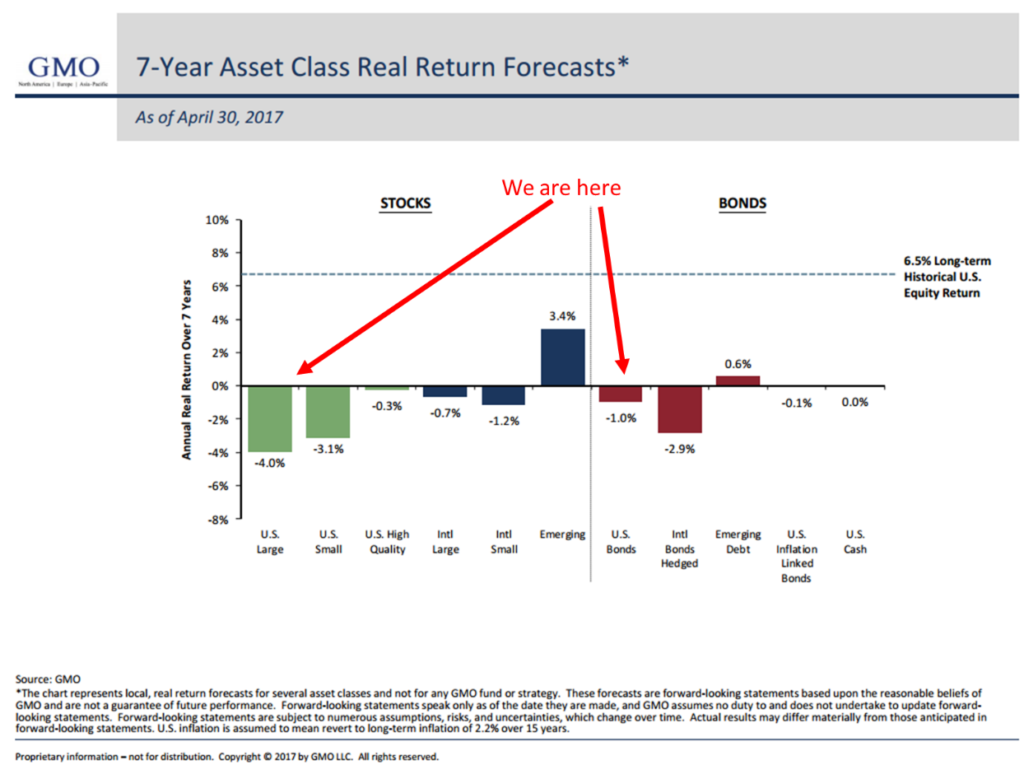

Today, you’ll find my high level notes from Mark Yusko’s presentation at the Mauldin Economics 2017 Strategic Investment Conference. It was outstanding and I hope you gain as much from the information as I did. By way of short introduction, in 1999, Mark Yusko, then CIO of the University of North Carolina’s endowment, recommended a significant reduction in the fund’s equity exposure to the board of directors. He advised that forward equity market returns would be a –1.90% over the coming seven years. Mark cited GMO’s famous 7-year Asset Class Real Return Forecast. One of the board members was irate and shouted, “I never want to hear those three letters ‘GMO’ again.”

The actual return achieved over the subsequent years was -3.5%. Mark and GMO were right. Even board members get emotional.

Source: GMO

Today, GMO is forecasting -4.0% real annualized returns (not a typo) over the next seven years (2017-2024). Compound that out and your $1,000,000 turns into $751,447. A loss of nearly 25%. One might think 7 x -4 = -28%; however, there is some benefit to how math compounds negatively. But negative it is.

By the way, GMO has been doing this same forecast each month for many years. CXO, LLC, a research advisory group, found “…correlation for these two series is 0.94, and the R-squared statistic is 0.88. The GMO forecasts tend to be high by less than 1%.”

Correlation is a statistical measure that indicates the extent to which two or more variables fluctuate together. A positive correlation indicates the extent to which those variables increase or decrease in parallel; a negative correlation indicates the extent to which one variable increases as the other decreases. R-squared is another measure of correlation. The score ranges from 0 to 1 with 1 being perfectly correlated. The CXO study shows a high degree of accuracy. Not perfect but not to be ignored.

Yusko’s point then and today is that your starting point conditions matter. Here is GMO’s most recent 7-Year forward return forecast.

Source: GMO

Today, you’ll find my summary notes from Mark Yusko’s presentation below. I enjoyed both his fast pace and fun personality. It will print long due to the many charts, but it is so worth your time.

Last week I shared with you my high level notes from Dr. Lacy Hunt’s SIC presentation. Lacy argued that recession is nearing and interest rates are headed even lower. He said that your starting point conditions matter when thinking about future returns and he shared the challenges facing us given today’s “initial conditions.”

Mark sees risks of a replay of the early 1930s legislative mistakes. He says not one incoming Republican president has avoided recession and a return to Hooverville is probable. He’s calling it Trumpville. “Beautiful” or “ugly?” Yikes… put Trumpville in the “ugly” outcome camp. My heart remains hopeful and focused on “beautiful.” But Yusko also sees opportunities in India, China and emerging markets.

If you haven’t heard of Mark before, here is a brief bio.

From 1993 to 1998, Yusko was a Senior Investment Director at the University of Notre Dame Investment Office. From 1998 to 2004, Yusko was founder and chief executive officer of UNC Management Company, Inc. Yusko left UNC to start Morgan Creek Capital Management in 2004.

Morgan Creek’s primary macroeconomic investment themes are forward looking and long term (5 to 10 years). They represent the synthesis of our global investment research, helping us determine where we can expect economic tailwinds in the markets and how we can best capitalize on the investment opportunities created by these long-term trends. OK – sharp guy.

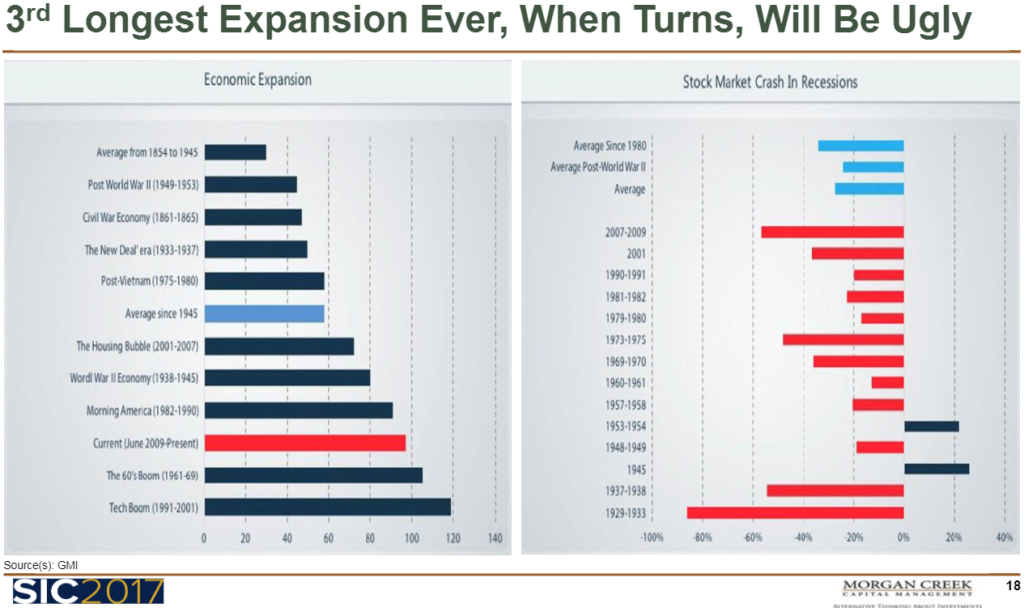

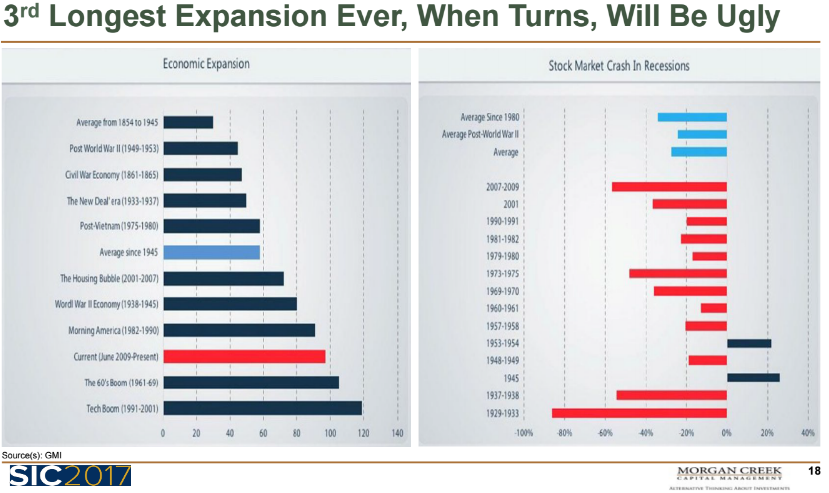

Speaking of “initial conditions,” one of the many charts Mark shared showed that we are in the third longest economic expansion ever (data 1845 to present). And he believes that, when it turns, it won’t be pretty.

Here is how you read the chart:

- Note on the right-hand side stock market performance in recessions.

- Note in the upper right (baby blue color) the summary of average declines since 1980, average post-war and the overall average. Call it -38% recession correction average since 1980.

- The left-hand side of the chart shows the various length in months of previous economic expansions (red bar is the current expansion).

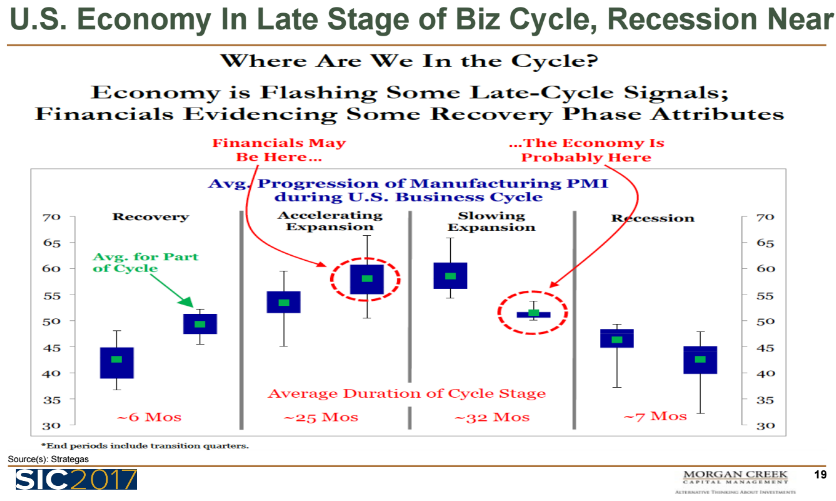

We are late in the business cycle. Note in red in this next chart: “…The Economy Is Probably Here.”

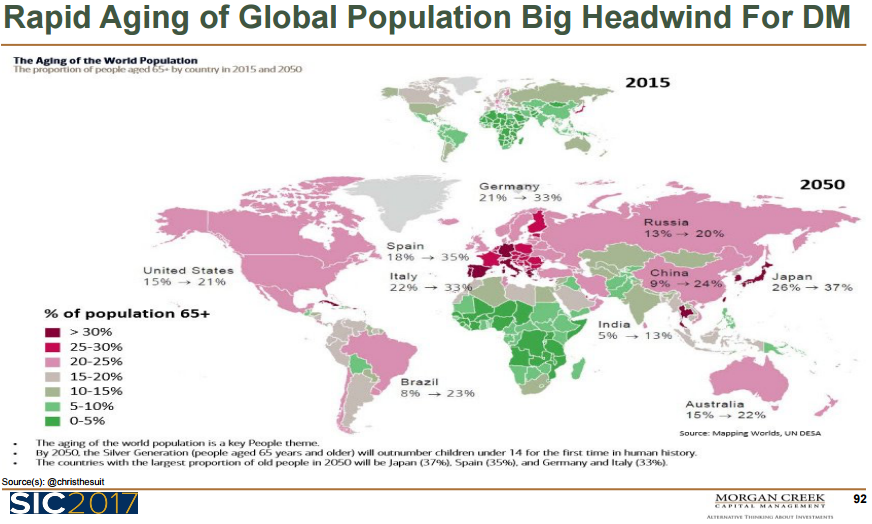

“Demographics is destiny,” Yusko said. You’ll find the same bullet point format again this week along with selected charts. His presentation was outstanding.

I hope you enjoy the notes as much as I enjoyed reviewing and processing the information. “Initial conditions” matter. I believe you’ll find some actionable ideas.

Grab that coffee and find your favorite chair – and jump in. And enjoy your weekend!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- Mark Yusko — Ten Surprises

- Trade Signals — S&P 500 Up 8.7% YTD; Trend Evidence Remains Bullish

- Personal Note

Mark Yusko – Ten Surprises

“Making predictions is hard, especially about the future….”

– Yogi Berra

Mark’s presentation lasted about 52 minutes. He sees low growth for the foreseeable future. 4% GDP growth is not going to happen. Also, he believes a recession is coming within a year, interest rates will remain on a path lower and that a stock market crash may occur this September/October.

Taken from his 2017 SIC presentation, following are my notes in bullet point format along with selected charts (note that the numbers on the actual charts do not match the chart numbers I give below. Mark’s presentation had over 130 charts. I’ve selected what to share with you along with corresponding notes):

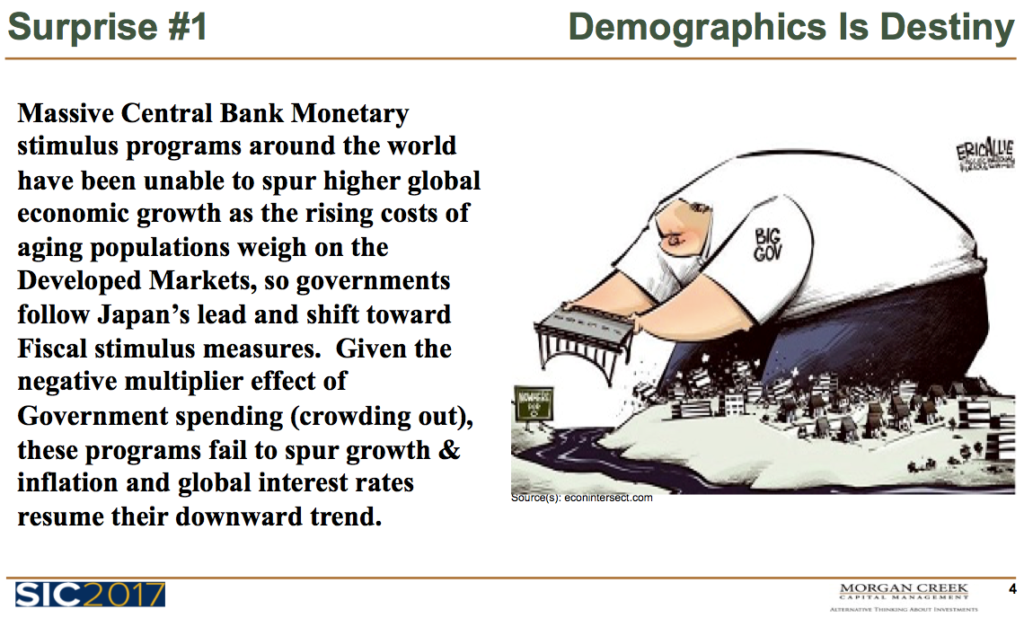

Surprise 1: Demographics Is Destiny

- When the big guy plants that bridge, it creates a whole bunch of crowding out. All the hopes on infrastructure spending and regulatory reform, while good; is not going to really make a difference.

- Mark said Lacy Hunt did a better job explaining why this is not going to work… and it is not going to work – (click here for last week’s notes on Lacy Hunt’s presentation to learn more).

- Mark’s major point is everyone is saying that because of the big man (federal government tax cuts and infrastructure spending) growth is going to suddenly be awesome in the United States… but it is not going to work.

- We are going to have low nominal GDP growth for a very long time due to poor demographics and productivity.

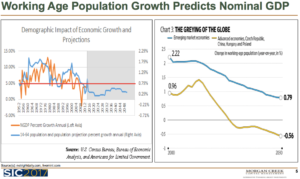

Working Age Population Growth Predicts Nominal GDP

Here is how you read the chart:

- Growth is really simple. Nominal GDP growth is the combination of two things: Population growth and

- Working age population growth, as you can see on the right-hand side of the next chart, is shrinking all around the world. You need 0.80% growth in population (red line on left-hand side of chart).

- It is well below 0.80% and will be for the next decade (light blue line in grey shaded area). Nothing we can do about it. Can’t make people older.

- You could add in immigration, but we are going the wrong way on that policy.

- We also know the second part of GDP growth is productivity: that is also sub 1% so we are going to have low GDP growth for a very long time.

- Call it 0.50% population growth and sub 1% productivity growth equals less than 1.5% nominal GDP growth.

Interest Rates

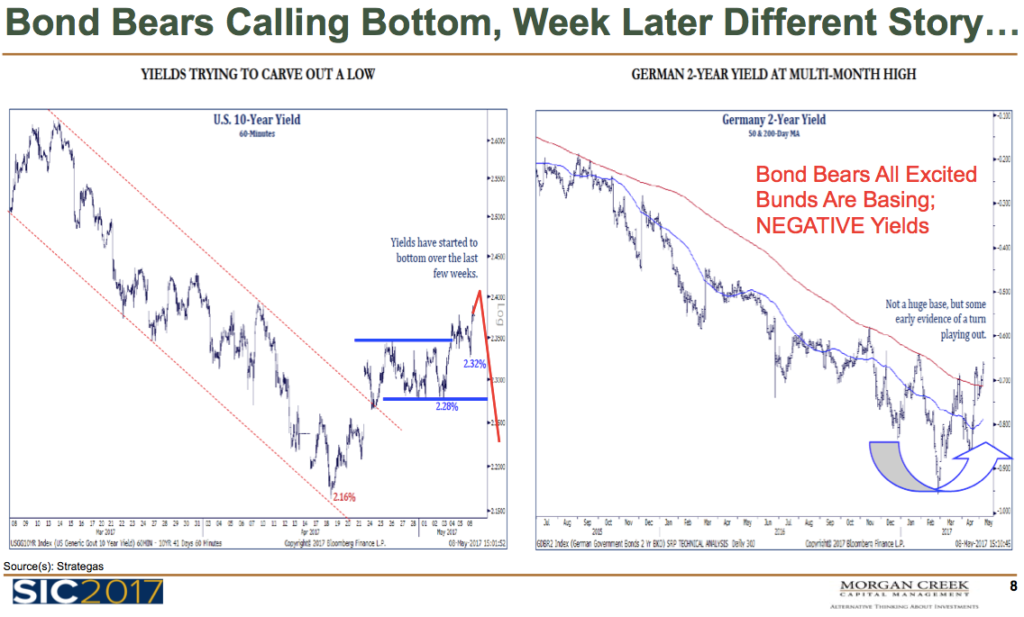

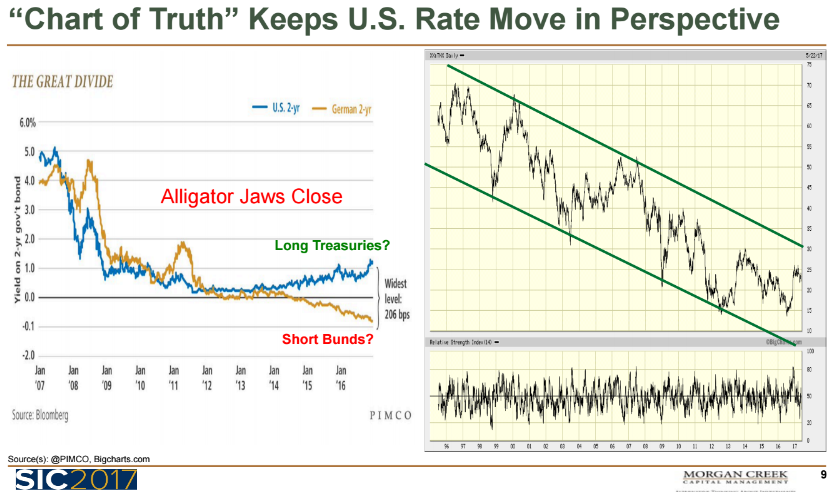

- Looking at interest rates (the 10-year Treasury yield) – the reflation “Trump” jump “hope” in rising interest rates has completely reversed.

- The administration has promised us 4% growth. We are not going to get 4% growth. Not going to happen.

- So… interest rates went up and they came right back down. And they are going to go lower.

- Everyone was short U.S. government bonds. The bond bears were calling for a bottom… A week later a different story…

- Bund yields are on the right in the above chart – that’s a negative 0.80% folks. That “sucks,” he said… “that’s a technical term.”

- Note in the above chart the “Alligator Jaws” (left-hand side: blue line is the U.S. two year yield, the orange line is the two year bund yield). T

- Alligator Jaws always close. A great trade may be to short German bunds and go long U.S. Treasury bonds.

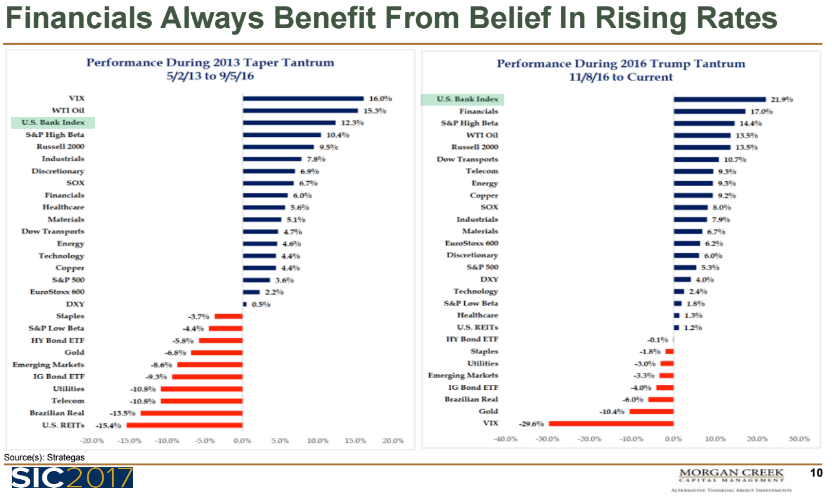

Financials Always Benefit from Belief in Rising Rates

- When everyone thinks rates are going to move up, they buy financials.

- This next chart compares the performance of financial stocks during the “Taper Tantrum” vs. the “Trump Tantrum.”

Here is how you read the chart:

- Highlighted in green is the U.S. Bank Index

- The left-hand side is the Taper Tantrum period from May 2013 to September 2013. The Fed was signaling higher interest rates.

- The right-hand side is November 2016 to current.

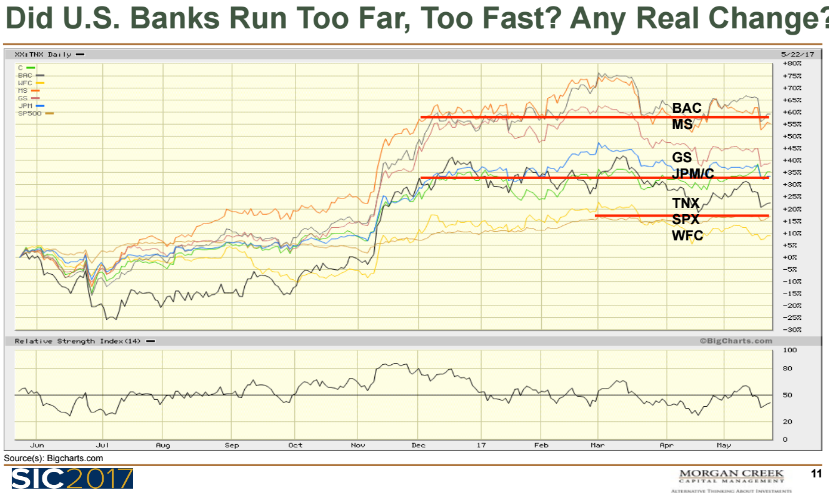

Did Bank Stocks Run Too Far Too Fast?

This next chart shows the November 2016 performance of select financial stocks.

Here is how to read the chart:

- Note, Bank of America and Morgan Stanley up about 60%. JP Morgan and Goldman Sachs up 30% to 40% and the S&P up about 20%.

- Mark says it’s been dead money (flat) since December and down since March 1.

- And here is his point:

- Financial stocks do well when rates rise.

- Rates are not moving higher.

- He doesn’t like financials.

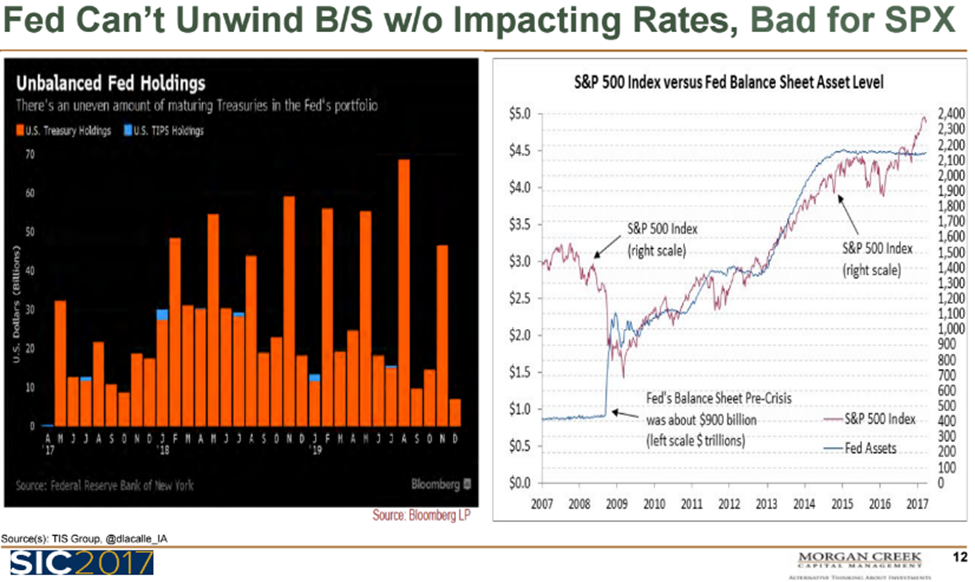

Fed Can’t Unwind B/S Without Impacting Rates, Bad for SPX

People seem to believe that the Fed is going to suddenly unwind their balance sheet and everything is going to be awesome. Not true.

Here is how to read the above chart:

- Note the high correlation with the Fed balance sheet and the S&P (right-hand side of chart).

- No chance they are going to unwind their balance sheet.

- And here’s why I know this — I don’t need to predict the future, we already know the future… everything that happens in Japan happens in the U.S. 11 years later.

- Their market peaked in 1989, our market peaked in 2000.

- Their bonds got downgraded from AAA, our bonds got downgraded from AAA 11 years later.

- We know that 11 years ago the Bank of Japan’s balance sheet was 26% of GDP, precisely where the Fed balance sheet is today.

- Today the BOJ’s balance sheet is 90% of GDP… That’s where we are going.

- There will be NO unwinding of the balance sheet.

- There will be NO selling of bonds. They are going to buy them all and then they are going to try to do (what was described the day before by several presenters) the “Jubilee.”

But here’s the problem, if it was as simple as printing money and handing it out to people, wouldn’t every country do it?

- If it were that simple, everyone would be rich…

- NO, we’d actually all be Zimbabwe.

- Mark said he actually has a one hundred trillion Zimbabwe dollar bill in his office and it wouldn’t buy a loaf of bread.

- So you can print all you want but eventually your currency becomes worthless.

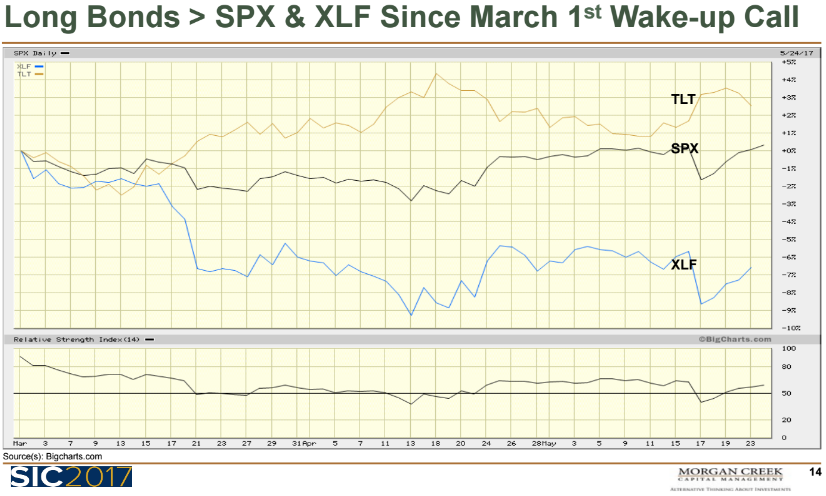

Trump is Not Going to Get Anything Done

On March 1, our day of reckoning and our little wakeup call when everyone realized holy crap, he’s not going to get anything done. HE’S NOT.

The Trump trifecta:

- Decreased taxes, decreased regulation, increased fiscal spending.

- Not happening — for that to happen you have to cooperate with the people in Congress, who he called rats in the swamp and he was going to get rid of them all.

- So they actually don’t want to work with him.

Long Bonds Greater Performance vs. S&P and Financials since March 1

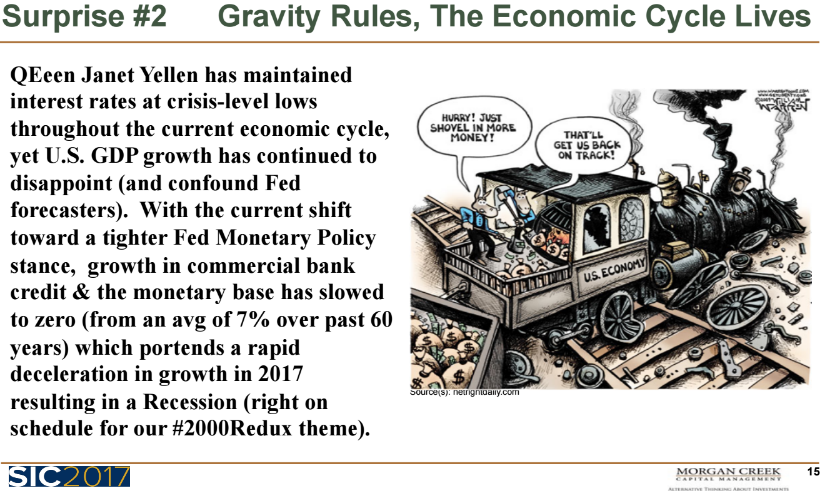

Surprise Number 2 – Decelerating Growth in 2017 = Recession

Just shovel in more money. That will get us back on track. The train is broken. Not going anywhere.

- Bottom line is that gravity rules. There is a business cycle.

- Lacy Hunt showed that bank lending and M2 money growth went negative last year.

- Negative growth in lending and money supply means that you are going to have low GDP growth.

- Do you remember in January when everyone thought GDP growth was going to be 3.5%? Everybody thought “awesome.” Except it came in at 0.70%.

- “0.70% sucks.” Why do we suddenly think if we get back to 2% growth, it’s ok. 2% is not OK.

- So we’ll throw more money in. Look at the train. “Just shovel in more money. That’ll get us back on track!”

- Do you think that train is going anywhere? No.

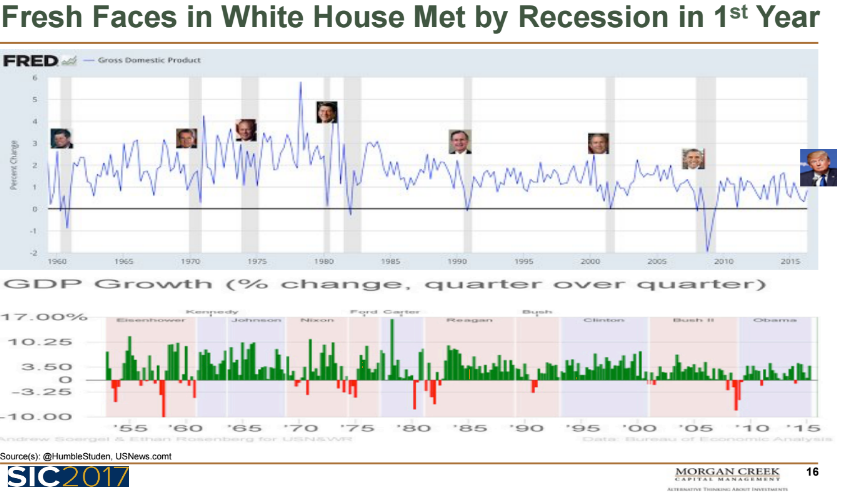

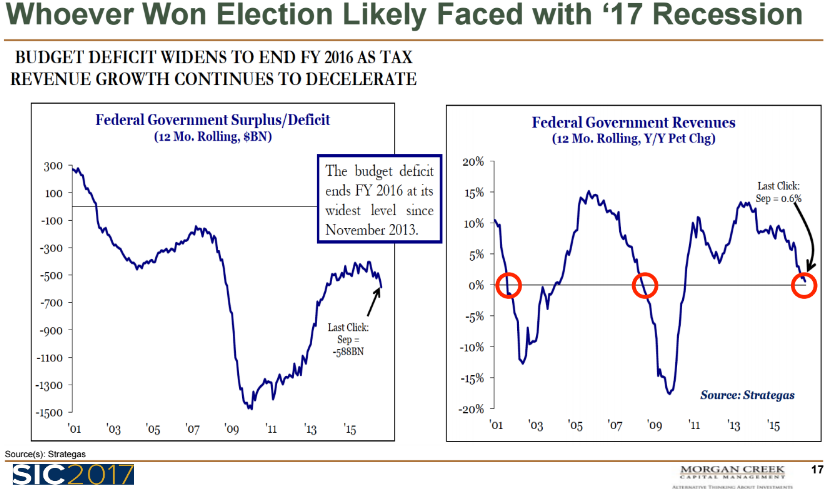

Presidents and Recession

Seven times a president has come in after an eight-year term and seven times we’ve had a recession. This eighth time is not going to be the first.

No matter who won, the federal government surplus/deficit was increasing and federal government tax revenues were going negative.

- When tax revenues are negative, it means people are doing less well.

- When people are doing less well, you can’t just paper over it.

- It means we have a problem.

Third Longest Expansion Ever, Recession Near

When recession comes, the market will go down 38%. That’s what they do (upper right – light blue – average since 1980).

Where are we in the business cycle today? We are somewhere between 50 and 57 on the ISM. That means we are in the late stages. Almost in recession.

He also noted that earnings were down 20%. There was a small spike in inflation along with the oil price rebound, but oil prices are declining again and the direction is lower. That spike was transitory.

- Inflation is going to go back down below 2% and ultimately sub 1% because we are in “deflation” not “inflation.” There is no inflation.

- There is deflation everywhere you look. Because of technology, because of productivity and as it turns out, age 65 to age 85 people don’t buy as much stuff as 45 to 65 year old people.

- And every day, 10,000 people turn 65.

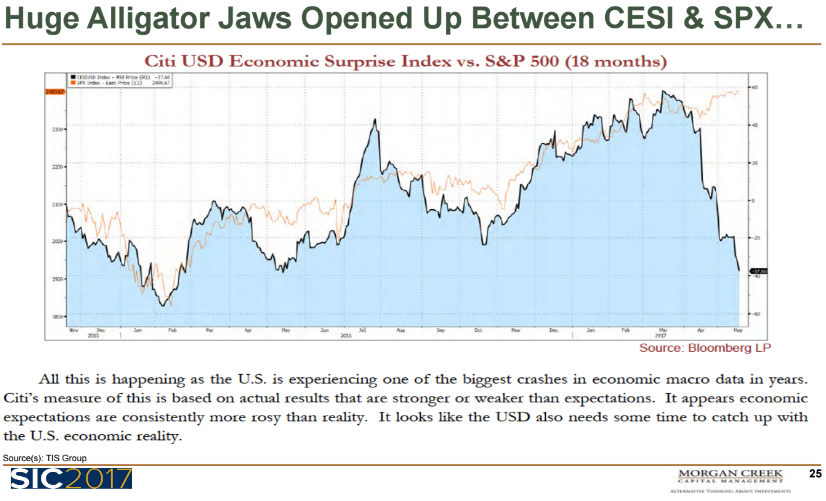

Next chart shows the Citibank economic surprise index has fallen off a cliff.

Here’s how you read the chart:

- Citi Economic Surprise Index (black line – blue shaded area).

- S&P 500 Index (yellow line).

- Note the high degree of correlation.

- Note the divergence early March 2017.

- Expect the “Alligator Jaws” to close (he is expecting the S&P to correct).

But everyone is saying employment is awesome. Of course, employment is awesome, but is it always awesome at the beginning of the cycle or at the end a cycle. It is always awesome at the end of a cycle.

(SB here: This is an important point. The press will point to this as proof the market is going higher. It’s opposite, as many things are in investing. Don’t bite, as most others do, on that head fake.)

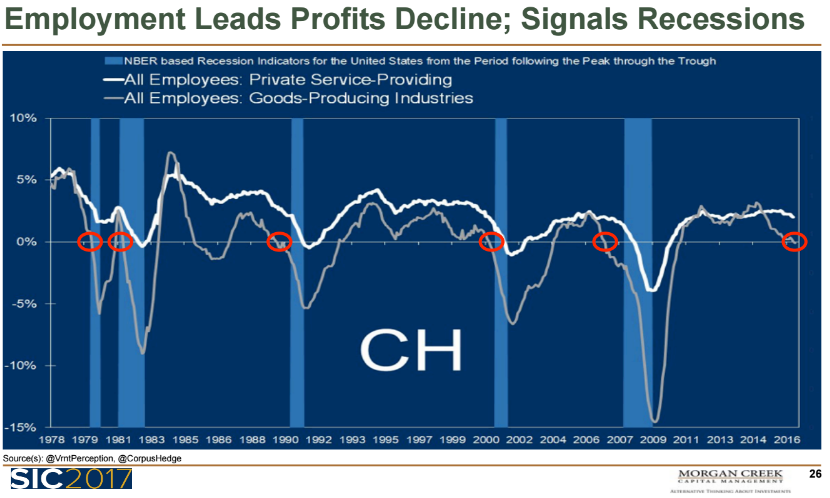

Here’s the chart:

Recession:

- Every time the rate of growth goes below zero, we have a recession (red circles).

- Note far right red circle – just went below zero.

- We will have a recession sometime within the next 12 months. It is not going to be different this time.

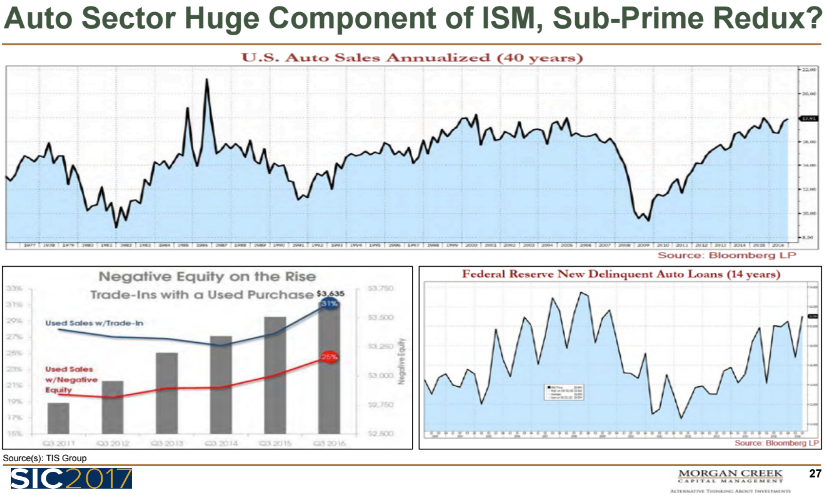

Auto Loans

Auto loans:

- 38% of new car loans have negative equity rolled into the loans.

- So you are starting with a loan to value of 115%… of a depreciating asset.

- This is subprime 2.0.

- This ends so badly. If you are not short the auto lenders and the auto manufacturers, you’re missing a big opportunity.

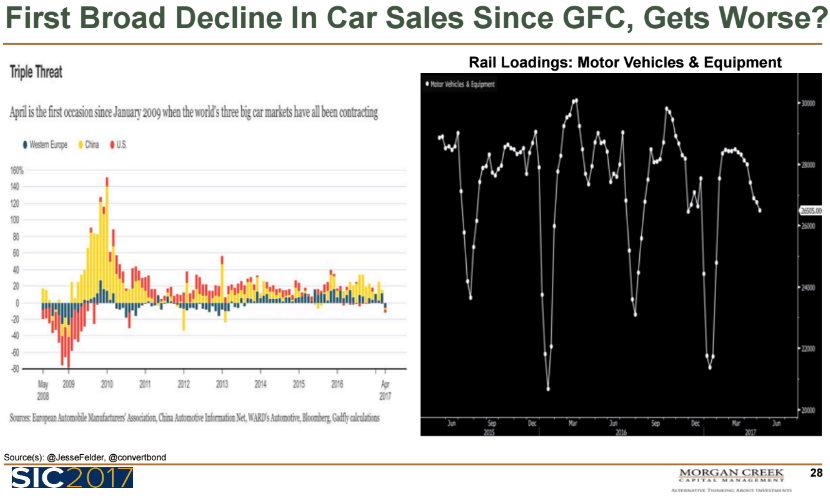

Here is how to read the above chart:

- Note the drop in sales (left side) – April is the first time since January 2009 when the world’s big three car markets have declined.

- And we know what sales are going to be because cars are shipped on rails. And we know how many are being stacked up in inventory. We track them with satellite pictures. They are packaged in shrink wrap but they are counted as sold because they left the GM plant.

There is one spoiler in this recession outlook. Material oil price declines could give the consumer a financial boost. If this happens, it could push out the recession for maybe 18 months.

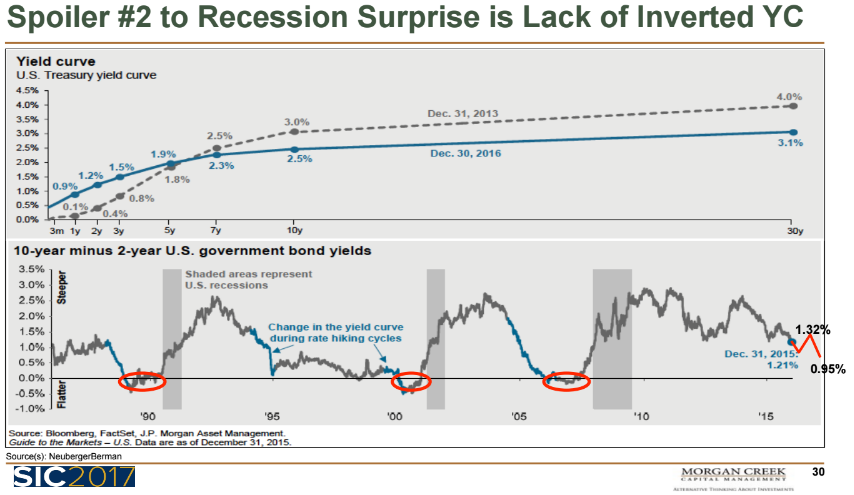

Inverted Yield Curve

But people are arguing that we are getting a recession because the yield curve is not inverted (one of the best predictors of recession is an inverted yield curve where the short end of the curve, two-year Treasury yields, are higher than longer-term 10-year yields).

Past inverted instances are circled in red below:

- Mark noted that the yield curve is not inverted because the Fed has artificially suppressed the short end.

- If the short end yields were where they should be, which is equivalent to nominal GDP growth, which it has been for 100 years, the yield curve would be inverted and this indicator would be signaling recession.

- There were only two periods like this one and the other was in the 1930s (interesting). Then, too, rates were artificially suppressed.

Surprise #3 – Kurve it Like Kuroda

- If you can make the yen go down, you can make Japanese equities rally.

- That is their only way out. That’s what Kuroda is doing.

- Mark is bullish on Japanese equities. He thinks Kuroda will get back on the hamster wheel and weaken the yen some more.

Surprise #4 When OPEC Freezes Over…

Several comments on oil:

- Idea is that they were trying to crush the shale producers.

- Shale guys figured out how to produce for even less. Didn’t work.

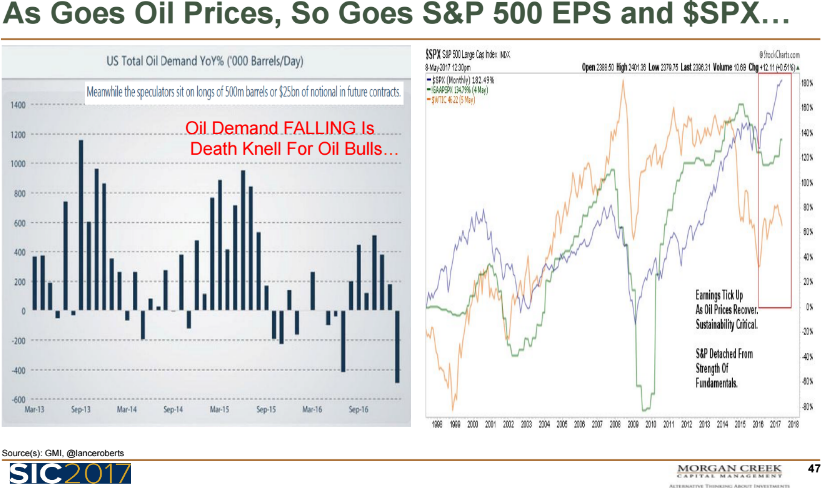

- If demand for oil actually falls (which on the left-hand side in this next chart it actually is falling, that is the death knell for oil prices).

- And as goes oil, so goes the earnings for oil companies and so goes the direction of the S&P (right-hand side of above chart).

- The overall trend in S&P 500 company earnings remains flat to down.

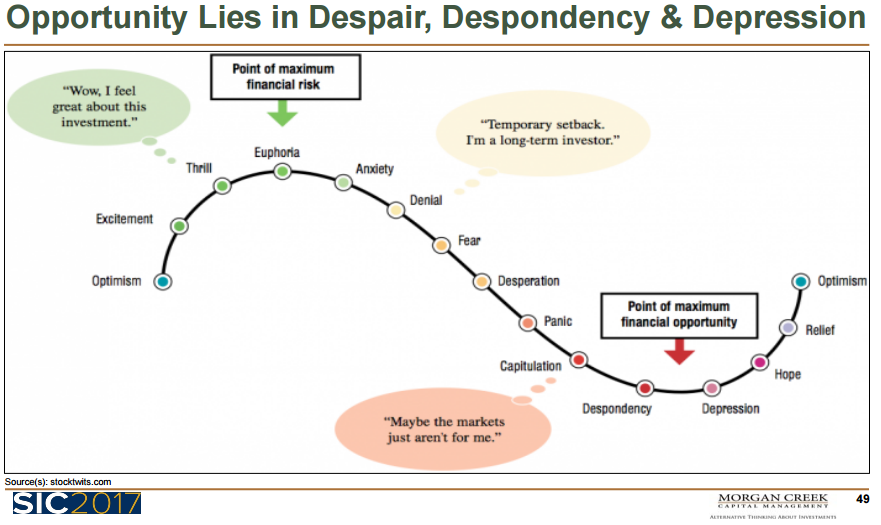

Surprise 5 – Italy & Opportunity Lies in Despair, Despondency & Depression

I loved this particular quote: Mark said, “Your job as investors is to feel sick to your stomach. Do not invest when you are excited and everything is great… go shopping when things go on sale.”

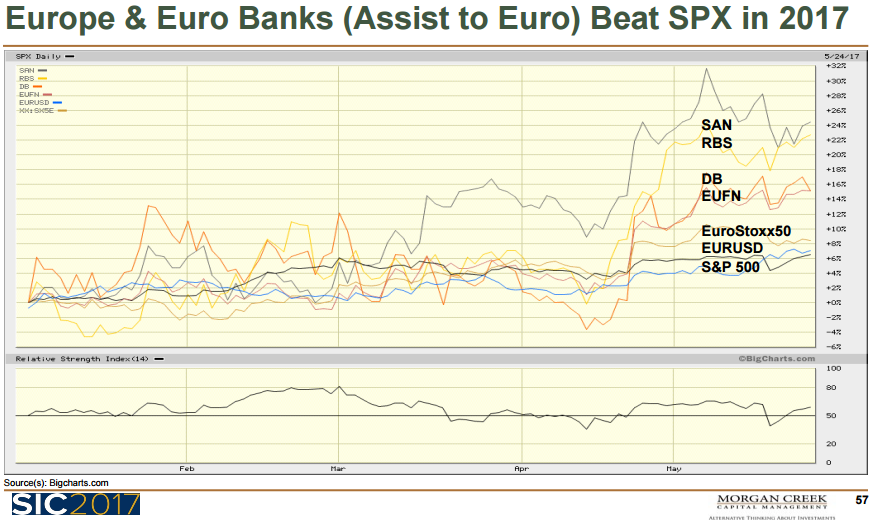

Mark said, “Banks look attractive globally, particularly so in Europe.” He noted for example, the Italian Banks are up 45% since the Italian Referendum. “Euro banks as a group are doing better than what you are reading in the press.” Keep in the back of your mind that “negative press sells.”

Europe and Euro Banks since January 1, 2017:

SB here – I just can’t get myself to add Euro Bank stocks to my shopping list – yet. Maybe in the next crisis. I see a real risk of a sovereign debt crisis coming out of Europe. The banks own much of the debt. I’m expecting to see “Despondency and Depression.” Not so sure we’ve seen those emotions yet.

Surprise #6: One Belt, One Road, Multiple Bull Markets

Xi is one of the most amazing leaders we have ever seen.

One Belt, One Road is the greatest construction program of all time. The center of the universe is moving to China and that is where it will be the next 100 years.

They are cutting interest rates when the rest of the world is raising interest rates.

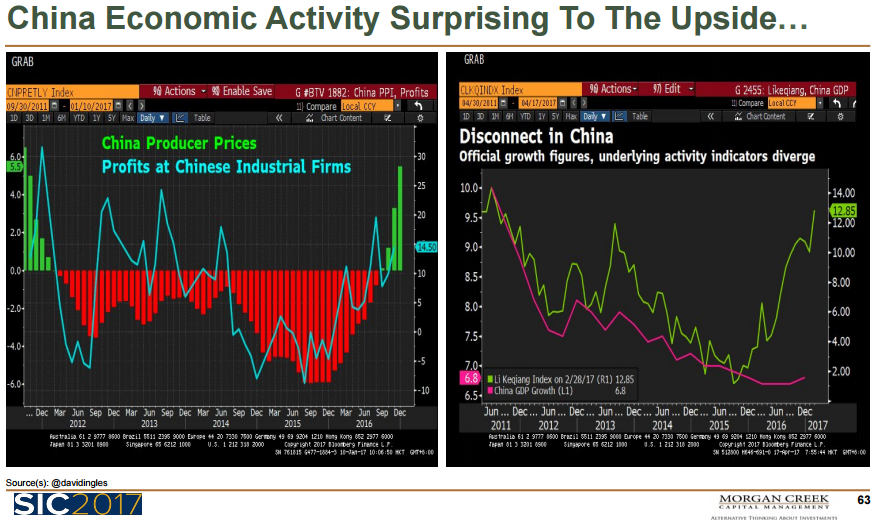

Leading economic indicators are telling us they are way better than what is being reported in the news. Everyone says China is cooking the books.

A U.S. company tried to prove that China was cooking their books (overstating their actual GDP growth). What they found is that China is cooking the books, except that opposite of what everyone thinks. They are under-reporting their true growth not over-reporting growth.

The green line at bottom right is the researched number and the red line is what China is reporting. Far better growth than what people think.

The current real risk is that China might actually be tightening right now (raising rates). Mark doesn’t see the currency risk others are talking about. Especially short term with the 19th Congress meeting later this year. No chance of a devaluation prior to it.

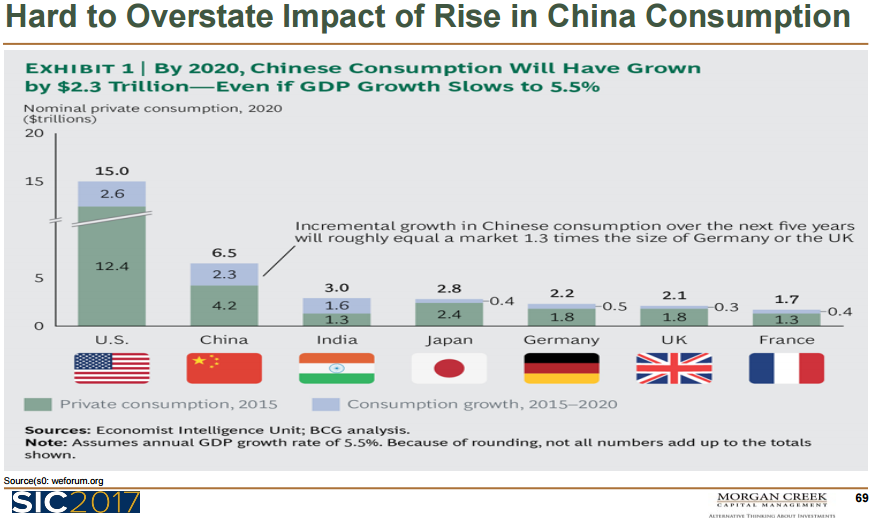

It’s hard to over-state the impact of the rise in Chinese consumption. The increase over the next five years is larger than all of the consumption in Germany and the U.K. (re-read that last sentence).

750 million people in China bought something with their mobile phone last year. 250 million people in the United States did. (SB here – wow!)

- Mark also mentioned Momo (a live broadcasting content company, which is up 140% this year, a $900 million cash flow positive business) and Tencent.

- Mark noted that Mark Faber said the day before, “If spending half of your time thinking about China, you are wasting your time.”

SB here: A year ago I mentioned two stocks I have yet to personally buy (they remain on my want-to-buy-in-crisis list). One is Alibaba (it’s up a lot) and the other is China Mobile. Available in ADR’s. I walked away from Mark’s presentation wondering if I should step up my thinking. (Note – not a recommendation for you to buy or sell any stock. Please talk to your advisor regarding suitability.)

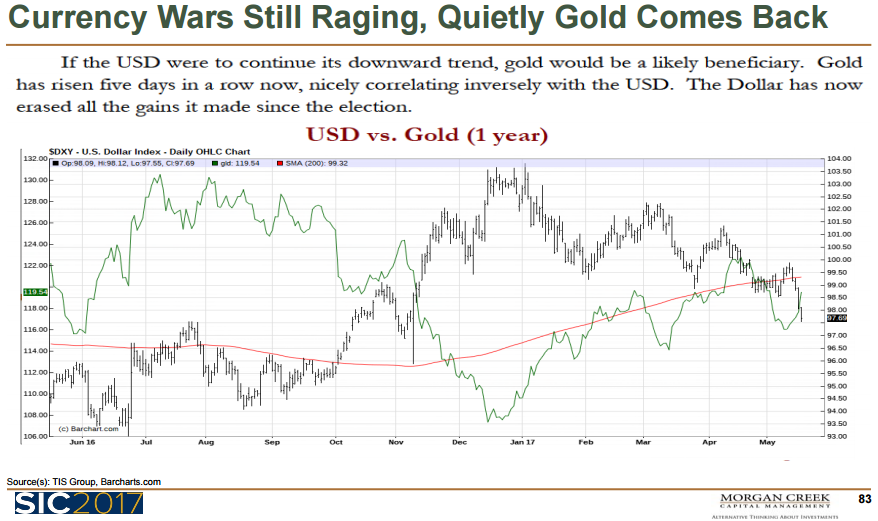

Surprise #7: King Dollar is in a Secular Decline

- When 85% of the people think the dollar is going to rise, it is not going to rise. That’s why it’s down 8%. It’s below L/T support, so it is going to go down more.

- EM currencies are strengthening, not weakening, because that’s where all of the growth is.

- Gold is outperforming most currencies. Gold is a currency and has been a store of value for 4,000 years.

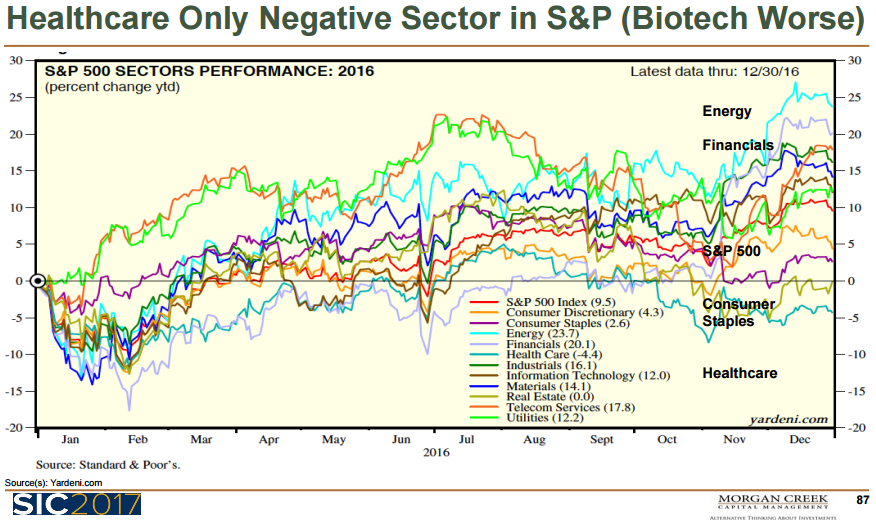

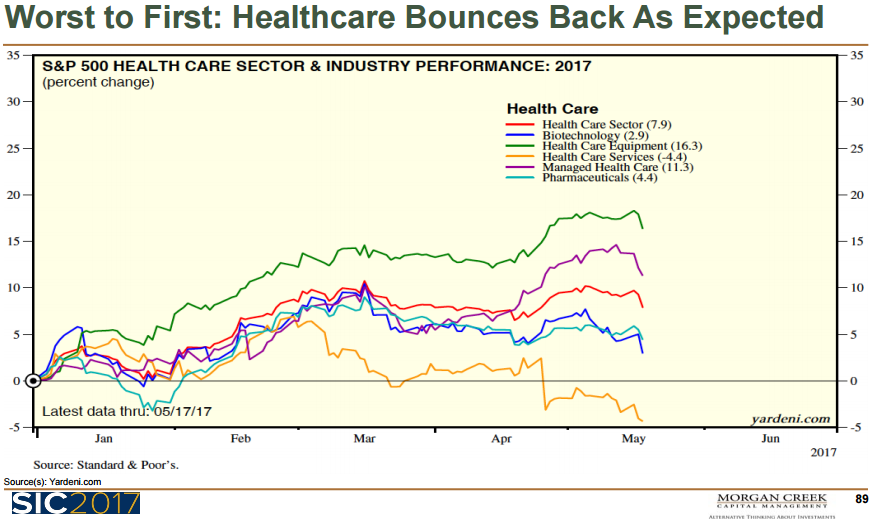

Surprise #8: Healthcare Gets Discharged

- Everybody hates healthcare. Since the Hillary tweet and the Donald saying I hate the high drug prices too.

- The reality is that Republicans control Congress. Republicans are funded by Pharma. They are not going to pass anything to hurt drug prices. Not going to happen.

- So when Clinton was projected to win, healthcare tumbled. The only sector that was negative last year was HC. One of the best performers this year is HC.

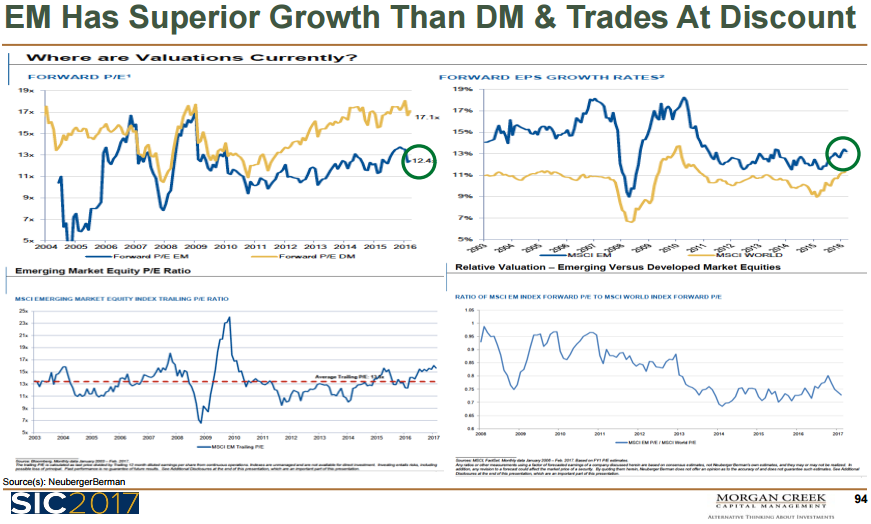

Surprise #9: Willy Sutton Was Right

- EM will continue to outperform in the coming years. That is where the growth is.

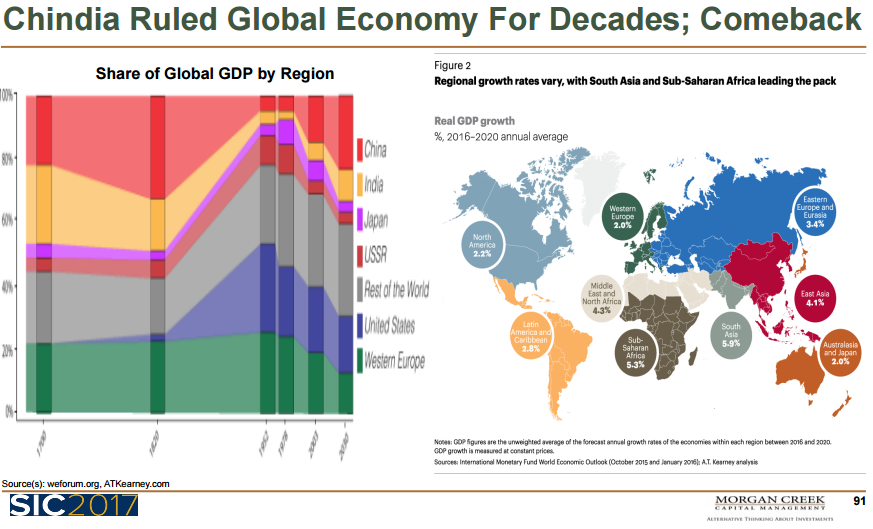

For 2,000 years, Chinda (China and India) ruled the world. Except for the last 200. Now it is coming back. All of the growth is in EM.

- Every day, 10,000 people turn 65 years of age in the U.S. and Europe.

- They don’t spend as much and they buy bonds.

- EM has better growth and lower prices (better valuations).

- People are still afraid of EM.

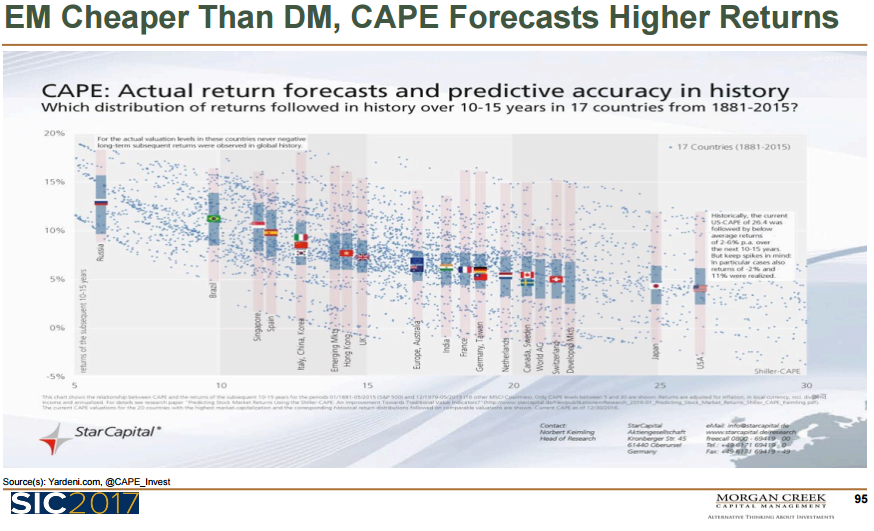

CAPE

- A horrible short-term indicator, but it is perfect long-term.

Here’s how you read this chart:

- Far right is USA.

- Horizontal axis is the Cyclically Adjusted Price Earnings Ratio or CAPE.

- Note how high it is on the chart (actually it is near 30 today).

- Left axis are the 10-15 year return histories. Look at USA, then look left and you’ll see a 4% expected forward return for the coming 10-15 years.

- Do the same for the other countries.

- Expect double-digit returns for the next few decades from EM and low single-digit for the U.S. and Japan.

- When you buy things that are cheap, you make money. When you buy things that are expensive, you lose money.

- If China does tighten, then expect a dip. Mark is going to want to buy the dip.

Aadhar – learn about Aadhar. It makes India one of the greatest investment opportunities of our time.

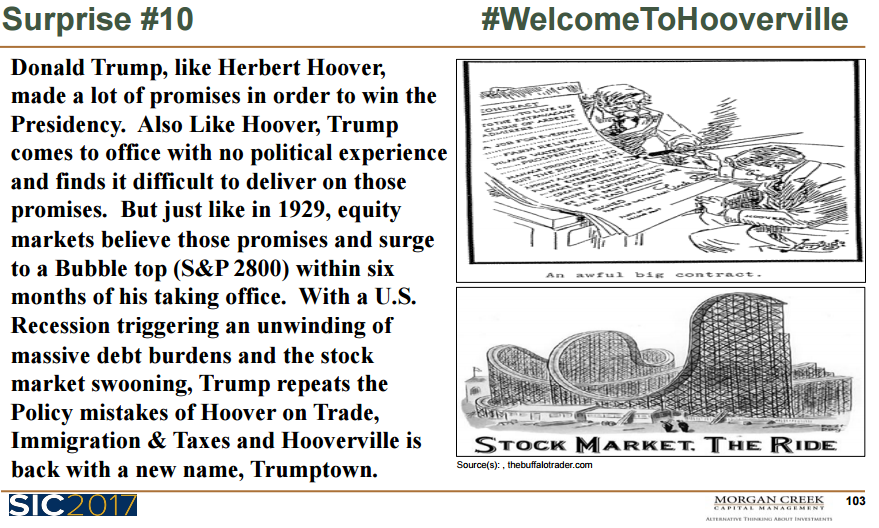

Surprise #10: Welcome to Hooverville

- Donald Trump has no political experience. He’s not going to get anything done.

- Just like Herbert Hoover in the 1920s.

- The markets are going to roll over and then the President and Congress are going to make stupid decisions, just like they did in the 20s, and then we are going to have Hooverville all over again.

- Which we will nickname Trumpville.

We know that no president other than George W. Bush came into power with a higher valued stock market and strong economic conditions.

- We know that when Republicans sweep, bad things happen.

- It is because they try to do things that in the short run are bad for the economy.

- They try to increase deficits by reducing taxes and they do all these other things that don’t actually happen for a while like regulatory changes. There is a lag so the market collapses as it did under Reagan and under Bush.

- And it is going to happen again under Trump.

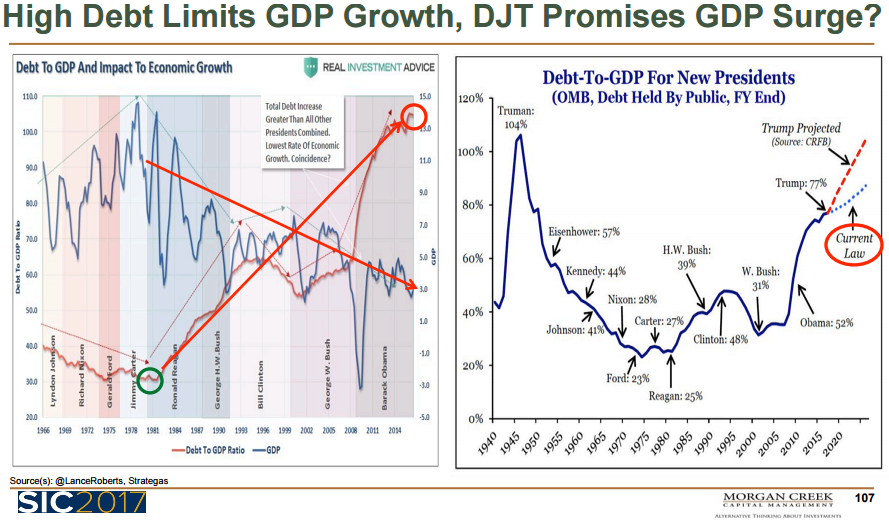

High debt actually limits growth. Trump’s a debt guy. More debt won’t do it.

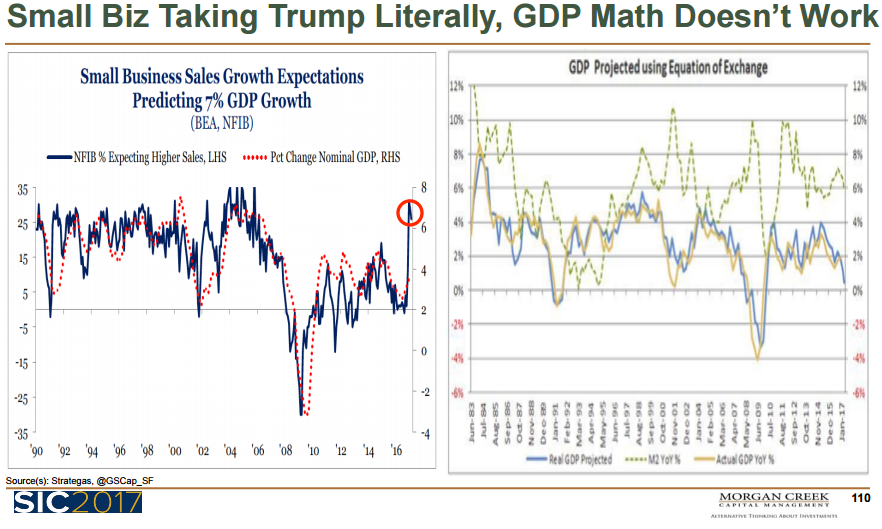

Small business expecting 7% GDP growth. Won’t happen!

The Trump Trifecta – Tax Cuts, Regulatory Reform and Fiscal Spending

- So far we have the Nofecta.

- We’ve had the second best stock market rally post-election since Hoover.

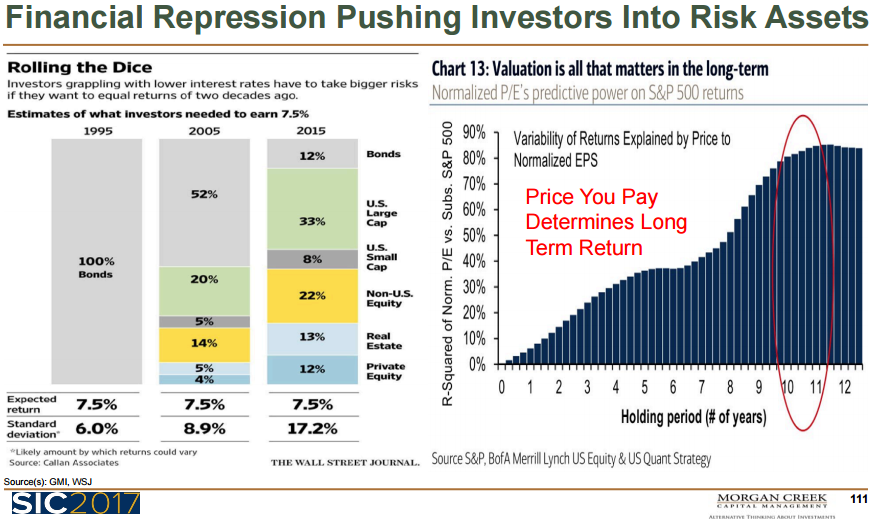

Financial repression forcing people into riskier assets.

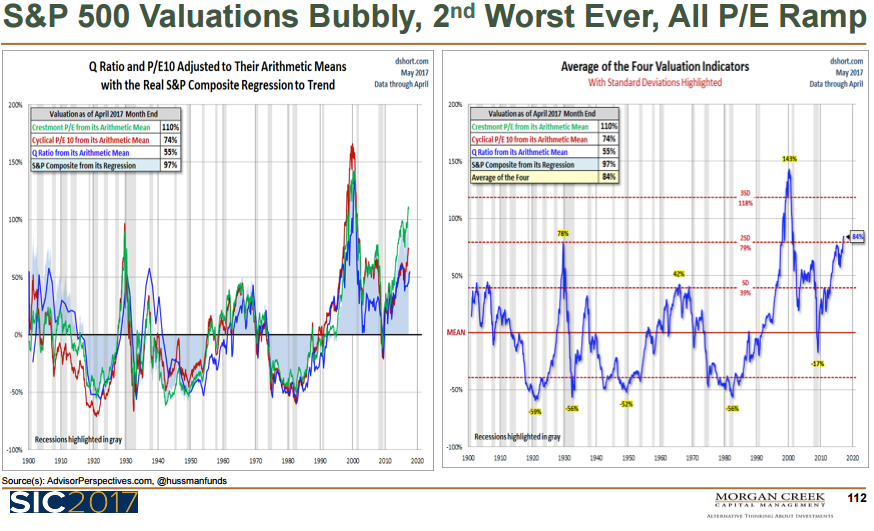

But wrong time to do so. We are at the second worst valuation level ever.

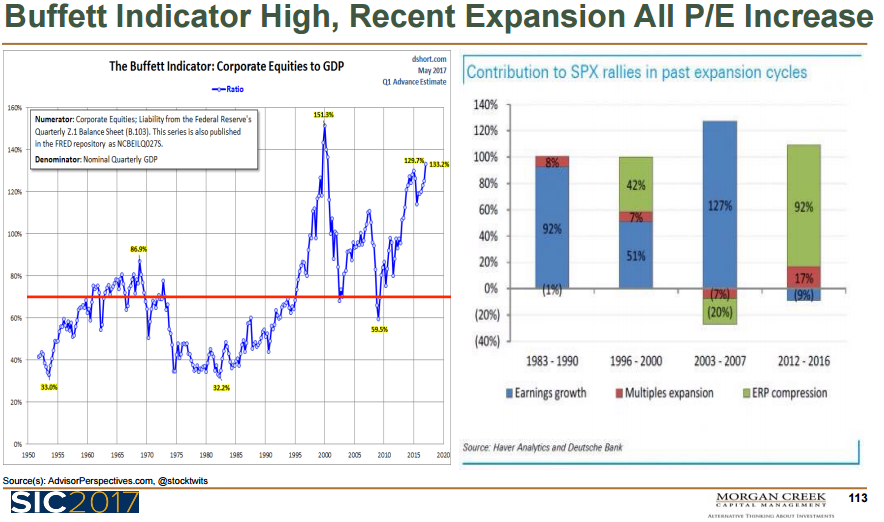

Since 2012, no growth in earnings. Just price expansion.

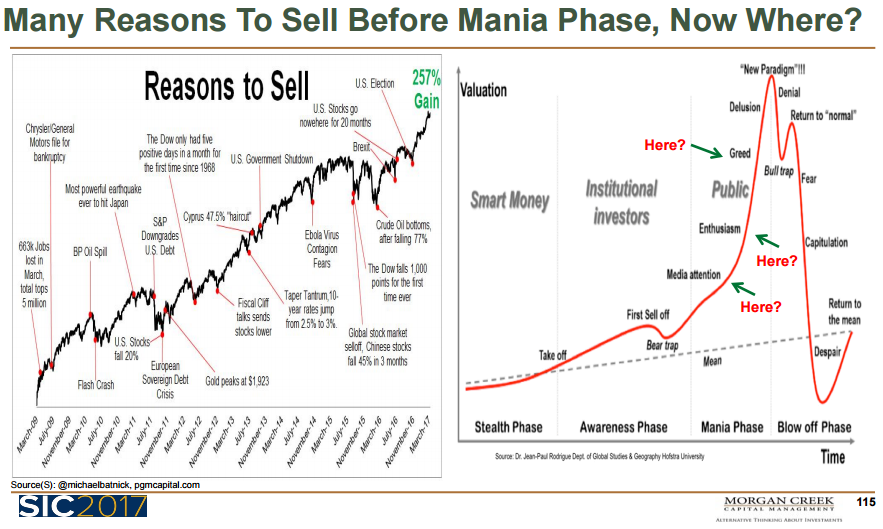

We are “Here.” Note green arrow on right-hand side. This suggests a little more room to run in stocks.

And this is where we are emotionally. SB here – The great Sir John Templeton comes to mind, “Sell when everyone else is buying.”

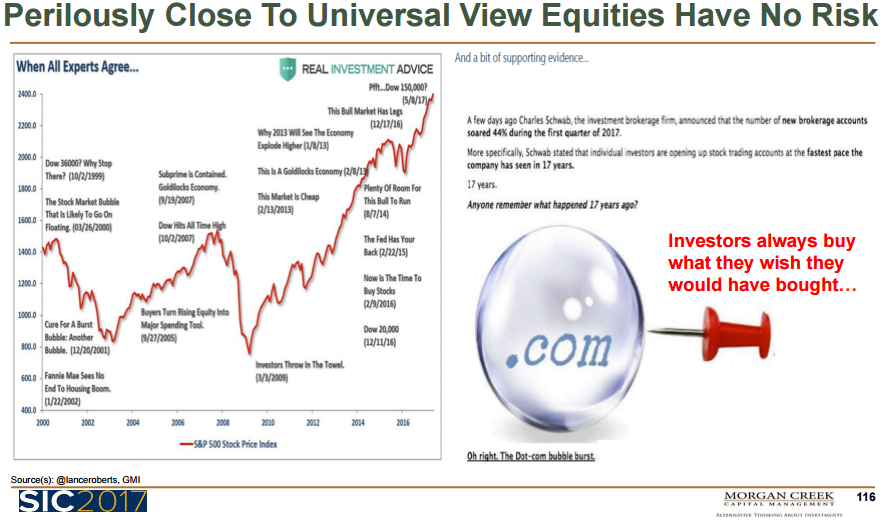

- Charles Schwab has had the highest number of new accounts opened since the month of March 2000. The month the greatest bull market of all time peaked. YIKES!

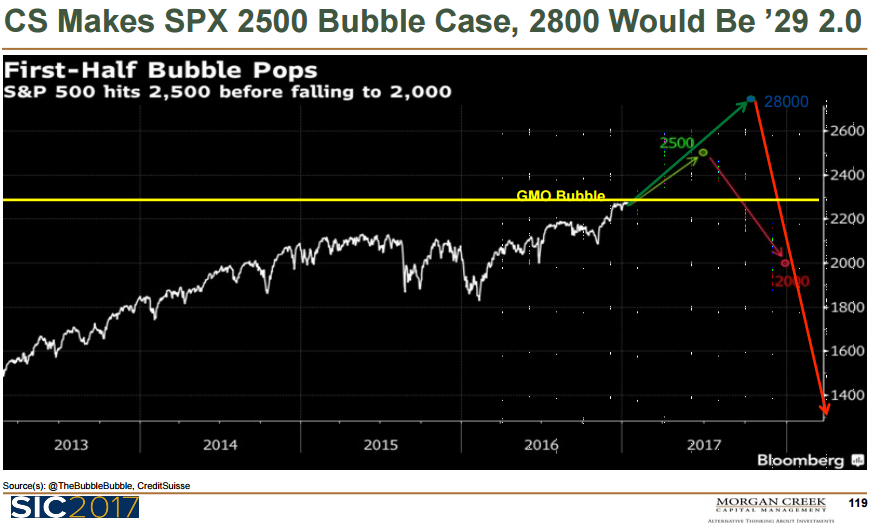

If we are to repeat the roaring 1920s, the Dow will go to 28,000 and the S&P will go to 2,500 according the Credit Suisse. Mark thinks the S&P will go to 2,800 and then we fall hard. Really hard.

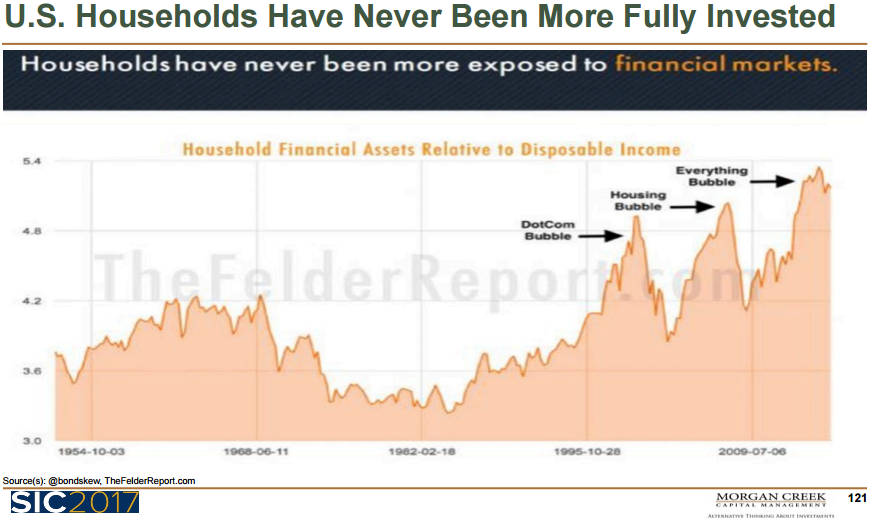

Everyone says this is the most hated bull market. That households are not in. Not true. We have the highest level of individual investor assets relative to their income… ever. Worse than just prior to the dot-com bust.

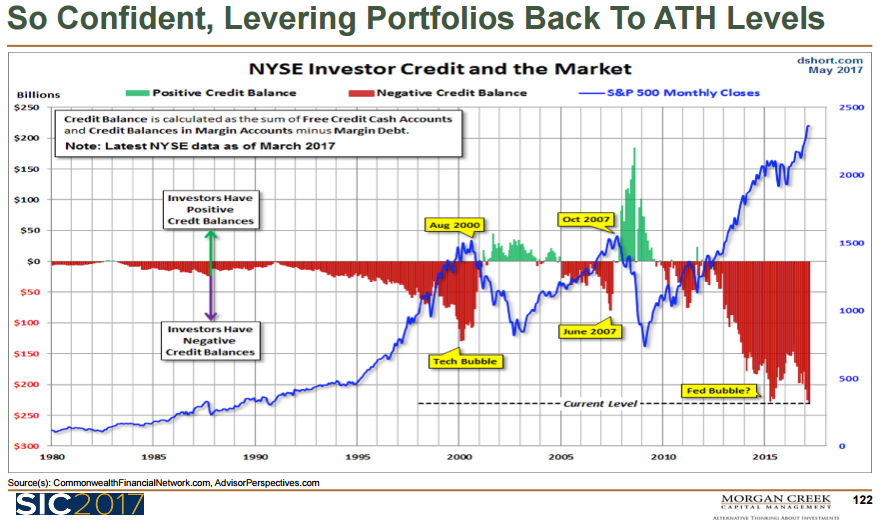

And we are borrowing money to buy overvalued assets. Margin debt highest ever.

We’ve seen this movie before. Mark concludes, “I’m telling you right now. We are going to have a crash and it is going to be terrific. I don’t know when it is going to be. I think maybe in September or October, but it is going to happen. And if we do what they did in the 1930s, if they impose tariffs to try to help our jobs, if they export foreigners, we are going to turn a recession into a depression. We are going to have a deflationary bust. When you put up tariffs, do you think that other countries just sit back and take it? No. Our exports went down 35% in the 30s. Because they put up higher tariffs than we did. Because they fight back. We act like we are just going to do this to the rest of the world.

U.S. markets have never been calmer. It is when we usually have crashes. May not happen this time but…

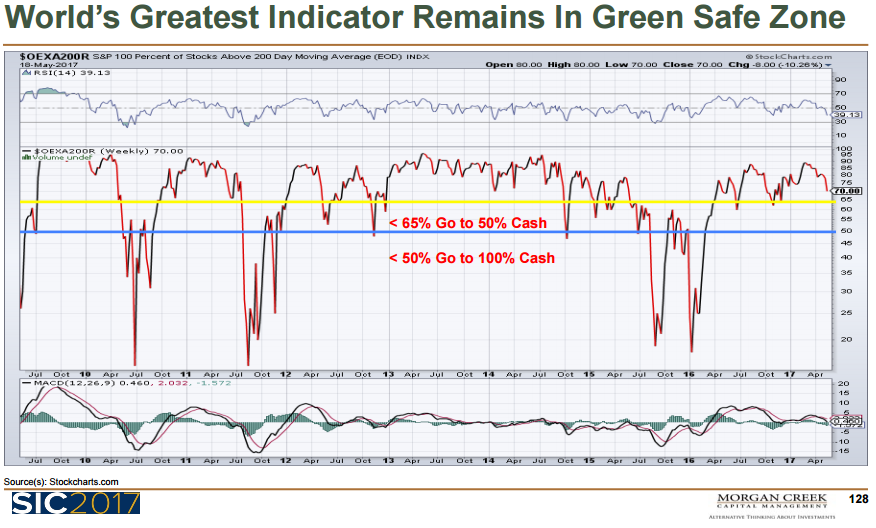

Mark offered up what he said is the greatest stock market indicator:

Here is how you read the chart:

- When the percentage of S&P 100 stocks above their 200-day moving averages declines below 65%, move 50% of your U.S. stock exposure to cash. When more than 50% of the stocks decline below their 200-day MAs, move 100% of your U.S. stock exposure to cash.

SB here – I keep saying, “Trend following works!” and I like Mark’s take on how to use trend following to help you with your risk management.

So there you have Mark Yusko’s presentation. Long and lots of charts. I found a number of actionable ideas. If I can leave you with one thought: see the opportunity and not the fear. There are things you can do to risk protect and enable you to navigate to the next opportunity. It’s coming, and as Trump might say, it is going to be “huge.”

Trade Signals — Cyclical Bull Signals on Equities and Fixed Income

S&P 500 Index — 2,429 (6-7-2017)

Notable this week: No changes since last week’s post. Despite all of the negative chatter about the Fed, including mine, the Ned Davis Research (NDR) “Don’t Fight the Tape or the Fed” indicator continues to suggest a bullish environment for stocks. The NDR CMG U.S. Large Cap Long/Flat Index remains bullish and there remains more buyers than sellers as measured by the Volume Demand vs. Volume Supply indicator. As for bonds, the Zweig Bond Model remains in a buy signal, our High Yield trend model is bullish and our Tactical Fixed Income Strategy remains invested in HY and muni bonds.

The short-term gold trend indicator remains in a buy signal, suggesting some portfolio exposure to gold. Investor sentiment is Extremely Optimistic, which is S/T bearish for equities but, while that suggests caution, the major cyclical trend for equities remains bullish. Inflationary pressures are neither high nor low.

Click here for the charts and explanations.

Personal Note

“True heroism is remarkably sober, very undramatic.

It is not the urge to surpass all others at whatever cost, but the urge to serve others at whatever cost.”

— Arthur Ashe

In addition to the Yusko presentation, I intended to share with you my summary notes from both David Rosenberg and Raoul Pal’s presentations. But you’d be reading today’s piece into early next week, so let’s save those comments for next week.

If you missed this last week, I’d like to share it with you again. Following is my recent interview by Shaun Wurzbach from S&P Dow Jones Indices. Click on the photo to watch the short interview.

My son, Matthew, graduated from high school today. As you receive this email, Susan and I will be celebrating with Matt, his sister Brie, brothers Kyle, Tyler, Conner and Kieran and our extended family and friends. Matt’s heading to Penn State with determination to make the golf team. He’s working hard to which dad has benefited (more golf for dad). My money is on Matt. Literally.

And Grandma Pat is in town. Grateful for the family I have. As I’m sure you are of yours… Here’s the gang:

The next two weeks are going to be challenging. Susan is having knee replacement surgery on Monday. I’ll be taking some time off and staying close to home. We understand the first few weeks are pretty rough, but she’s so mentally strong and ready to have a working knee again. Years of sports and wear and tear has left little cartilage but, as my father always used to say, “The prize is worth the price.” To which Susan agrees.

Come on medical science, invent some synthetic cartilage of some sort. I see billions in that business.

Hope you have some fun plans in your weekend. Enjoy your family and raise a glass to the wonderful journey you are on. Let’s celebrate life!

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Capital Management Group