By many measures, the stock and bond markets have rarely been more expensive and more stable, and that has me worried. High-yield bonds and mortgage-backed securities are both trading near their narrowest-ever spreads relative to Treasurys, and they have been hovering around these levels for months. At the same time, U.S. stock market indexes are continuing to make new highs while the Chicago Board Options Exchange Volatility Index (VIX), which measures option-implied S&P 500 volatility, is near its lowest level since 1993. The amount of complacency built into the markets argues for caution.

Plenty of events clustered around this summer and fall could potentially spell disappointment for the markets. In Europe, Emmanuel Macron may have handily won the presidential election in France, but there remains the French parliamentary elections next week. These elections may result in what the French call “cohabitation,” a term that describes when the president and the majority of the members of the French parliament represent two different parties, which has not happened in France since the 1997 election. Meanwhile, the U.K. election results have hobbled Theresa May’s mandate and created a cloud of uncertainty over the timing and direction of Brexit negotiations. German federal elections, due to take place in September, will test Angela Merkel’s conservative bloc.

In Washington, the focus is on the Senate version of the healthcare bill, which is unlikely to be finalized before the August recess. This delay could push back the timeline for enacting tax reform to 2018. This says nothing of the political uncertainty in Russia, North Korea, or in the Middle East.

As this realization settles in, I think some of the hope underpinning the markets will slowly erode this summer. History suggests that there is a high likelihood we will get some sort of shock in the second half of the year, which would lead to tightening financial conditions and widening credit spreads. I have seen it happen a number of times in my career: The stock market crash of 1987 and the Asian crisis in 1998 were both unexpected events late in a lengthy economic expansion that led to a brief but violent repricing of risk assets. Both events, however, were followed by at least two more years of an expanding economy.

Today we are on pace to set a record for the longest expansion in U.S. history, thanks in large part to the slow post-crisis recovery and accommodative monetary policy. The current upward slope of the yield curve offers no indication that it will end soon, but eventually it will, given the Federal Reserve’s indications that further tightening is needed. I believe we will see two more rate hikes in 2017, the next one occurring later this month, and at least three increases in 2018. I also expect that the Fed will announce in September a change to its balance sheet strategy that will involve a gradual tapering of reinvestments in 2018. This should put upward pressure on yields at the short end and the belly of the curve, where most of the new Treasury issuance is likely to come.

Even as conditions call for a healthy dose of caution, there is no need to panic longer term. There is still significant ongoing stimulus coming from the European Central Bank and the Bank of Japan.

The combination of these conditions argues for taking certain near-term portfolio actions. Investors should consider upgrading credit quality whenever possible while reducing exposure to high-yield bonds and stocks. Holding some dry powder* for opportunities that should arise amid a pickup in volatility later this year would be a wise move. With spreads near record tights, fixed-income investors simply are not being compensated for the risk they incur in the hunt for yield. Investors should remain disciplined and not chase returns now. It may not be the most exciting message, but no one ever took a loss by booking a gain.

As I see more life left in this economic expansion, I believe there will be opportunities later in the year to make up for any near-term underperformance. The coming correction might not happen tomorrow, but current conditions bring to mind the legendary response of Baron Rothschild, who, when asked the secret of his great wealth, said he made his fortune by selling early. It might be wise to follow Baron Rothschild’s example and take some chips off the table.

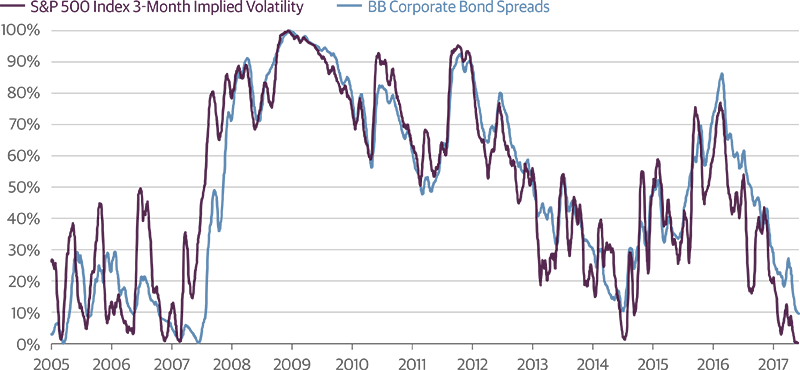

Risky Assets Set for a Pullback

Stock market volatility and high-yield corporate bond spreads are at their lowest levels since 2005, represented by the zero percentile. Both measures have returned to levels last observed ahead of a shock that caused a major pullback. The catalyst for this cycle’s pullback is unknown, but history tells us to be cautious when valuations are stretched and markets are complacent.

Source: Bloomberg, Bank of America Merrill Lynch, Guggenheim Investments. Data from 1.3.2005–6.6.2017. Based on a 20 trading day moving average of 3-month SPX Index put options struck at the money and BB-rated corporate bond spreads, both shown in percentile, which indicates in percentage terms the time over the period that levels have been below the closing level. Example: The 60th percentile for high-yield spreads indicates that spreads have been tighter in 60 percent of observations over the period.

Important Notices and Disclosures

*“Dry powder” refers to highly liquid assets, such as cash or money market instruments, that can be invested when more attractive investment opportunities arise.

This article is distributed for informational purposes only and should not be considered as investing advice or a recommendation of any particular security, strategy or investment product. This article contains opinions of the author but not necessarily those of Guggenheim Partners or its subsidiaries. The author’s opinions are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. ©2017, Guggenheim Partners. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.