“Over the long term, what raises living standards is productivity—the amount that is produced per person—which increases

from coming up with new ideas and implementing ways of producing efficiently. Productivity evolves slowly,

so it doesn’t drive big economic and market moves, though it adds up to what matters most over the long run.”

– Ray Dalio

This is one of the more important pieces I’m sharing with you. It’s a candid look at where we are in the economic cycle and what that likely means for the global markets. Today, you’ll find Ray Dalio’s most recent “Observations” as shared by him in a recent LinkedIn post.

Dalio concludes that the “near term looks good but the long term looks scary.” He takes us on an economic/investment opportunity tour across much of the world. The significant problems are debt and low productivity. As he calls it, a “beautiful” debt deleveraging or an “ugly” deleveraging remains to be seen. I particularly like his direct and candid way. I also like that this information comes not from a Wall Street research department but from the largest hedge fund manager in the world. He has $150 billion of real skin in the game. To me, that’s a view I want to hear.

So, without further ado, let’s jump right in and see what Ray has to teach us. Grab a coffee and find your favorite chair. It’s to the point with supporting charts. I believe worth your time.

When you click through, you’ll find a link to Trade Signals and I conclude with a dad’s proud story about his son… “It’s All About Team.” I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- Ray Dalio — Big picture, the near term looks good and the longer term looks scary

- Charts of the Week — Recession Watch Charts

- Trade Signals — S&P 500 2,400, The Trend Remains Bullish for Stocks and Bonds

- Personal Note — It’s All About Team

Ray Dalio — Big Picture, The Near Term Looks Good and The Longer Term Looks Scary

Most of what Ray shared this past week in a LinkedIn post can be summed up in the title above. But I do encourage you to review the entire piece.

If you are not familiar with Ray Dalio, he runs the world’s largest hedge fund – Bridgewater Associates. He is a macro investment manager who looks for opportunities globally. Ray’s been on a mission to teach the world “How the Economic Machine Works.” It is the base template he has used to guide his investment decisions that has lead to his success. He is one of the brightest investment minds I know.

I recommend that your children click the link above and watch the short video. Then, ask them to forward it to their social studies or economics teachers. At the very least, they/we and our largely financially under-educated (said nicely) politicians should learn how the economic system works. Ok, enough preaching on my part… What follows is from Dalio’s LinkedIn post:

Near term looks good, longer term looks scary. That is because:

The economy is now at or near its best, and we see no major economic risks on the horizon for the next year or two.

1. There are significant long-term problems (e.g., high debt and non-debt obligations, limited abilities by central banks to stimulate, etc.) that are likely to create a squeeze,

2. Social and political conflicts are near their worst for the last number of decades, and

3. Conflicts get worse when economies worsen.

So while we have no near-term economic worries for the economy as a whole, we worry about what these conflicts will become like when the economy has its next downturn.

The next few pages go through our picture of the world as a whole, followed by a look at each of the major economies. We recommend that you read the first part on the world picture and look at the others on individual countries if you’re so inclined.

Where We Are Within Our Template

To help clarify, we will repeat our template (see www.economicprinciples.org) and put where we are within that context.

There are three big forces that drive economies: there’s the normal business/short-term debt cycle that typically takes 5 to 10 years, there’s the long-term debt cycle, and there’s productivity. There are two levers to control them: monetary policy and fiscal policy. And there are the risk premiums of assets that vary as a function of changes in monetary and fiscal policies to drive the wealth effect.

The major economies right now are in the middle of their short-term debt cycles, and growth rates are about average. In other words, the world economy is in the Goldilocks part of the cycle (i.e., neither too hot nor too cold). As a result, volatility is low now, as it typically is during such times. Regarding this cycle, we don’t see any classic storm clouds on the horizon. Unlike in 2007/08, we don’t now see big unsustainable debt flows or a lot of debts maturing that can’t be serviced, and we don’t see monetary policy as a threat. At most, there will be a little touching the brakes by the Fed to slow moderate growth a smidgen. So all looks good for the next year or two, barring some geopolitical shock.

At the same time, the longer-term picture is concerning because we have a lot of debt and a lot of non-debt obligations (pensions, healthcare entitlements, social security, etc.) coming due, which will increasingly create a “squeeze”; this squeeze will come gradually, not as a shock, and will hurt those who are now most in distress the hardest.

Central banks’ powers to rectify these problems are more limited than normal, which adds to the downside risks. Central banks’ powers to ease are less than normal because they have limited abilities to lower interest rates from where they are and because increased QE would be less effective than normal with risk premiums where they are. Similarly, effective fiscal policy help is more elusive because of political fragmentation.

So we fear that whatever the magnitude of the downturn that eventually comes, whenever it eventually comes, it will likely produce much greater social and political conflict than currently exists.

The “World” Picture in Charts

The following section fleshes out what was previously said by showing where the “world economy” is as a whole. It is followed by a section that shows the same charts for each of the major economies. These charts go back to both 1970 and 1920 in order to provide you with ample perspective.

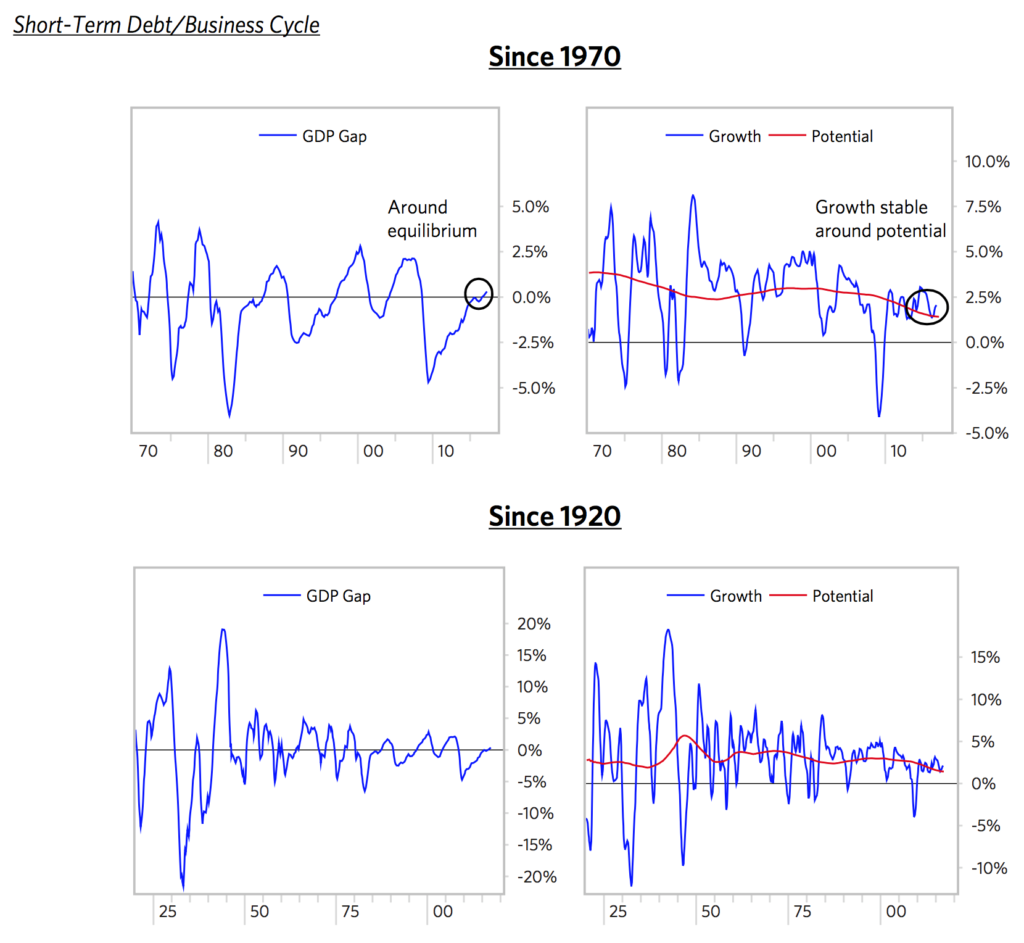

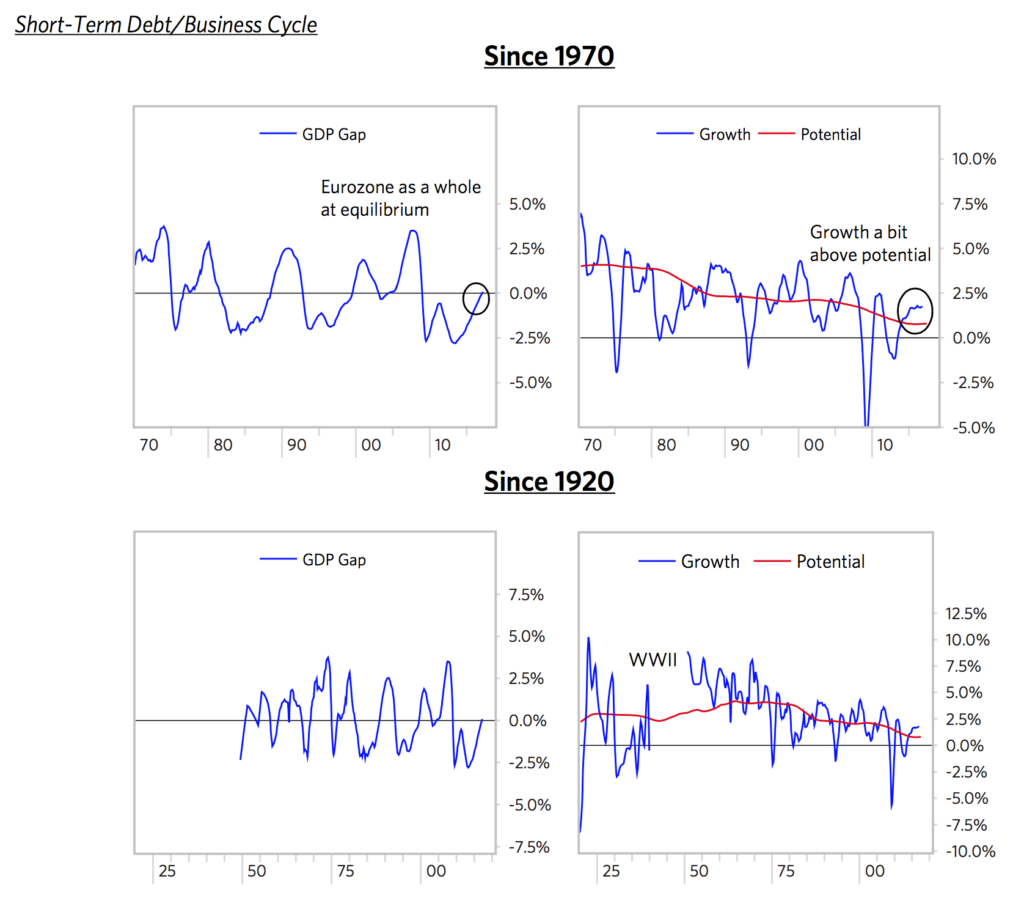

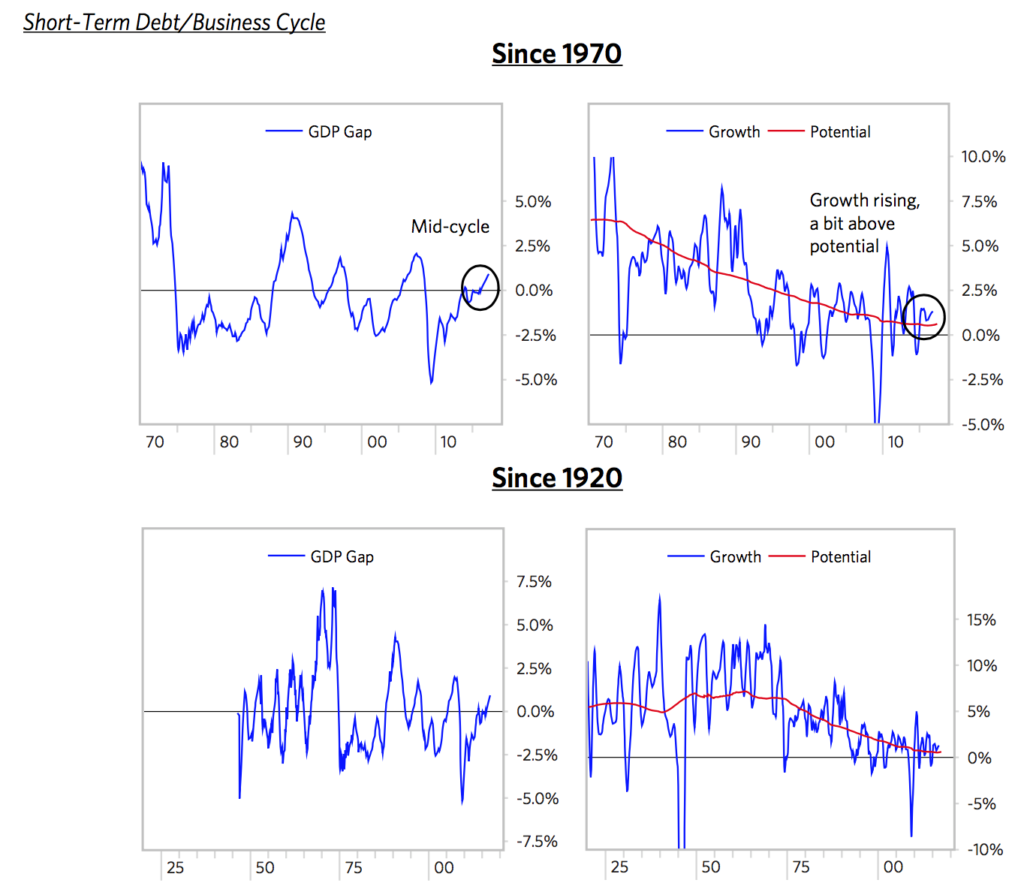

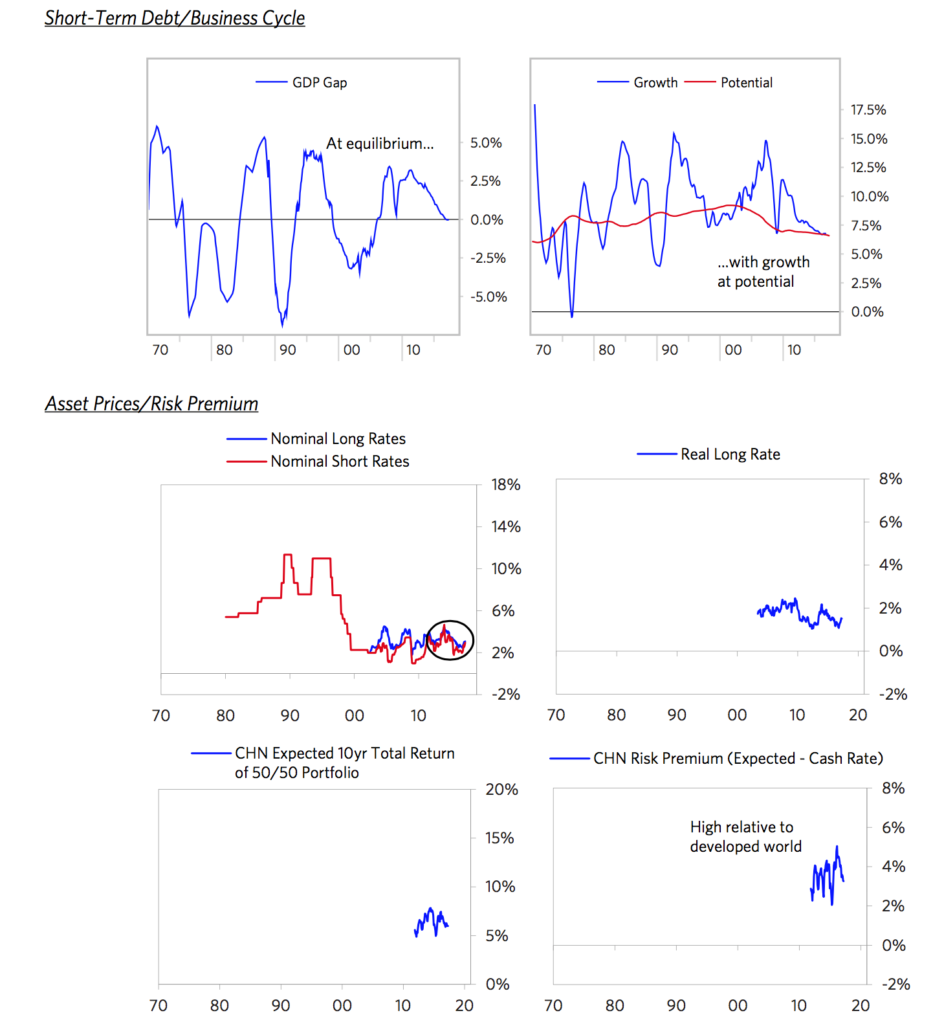

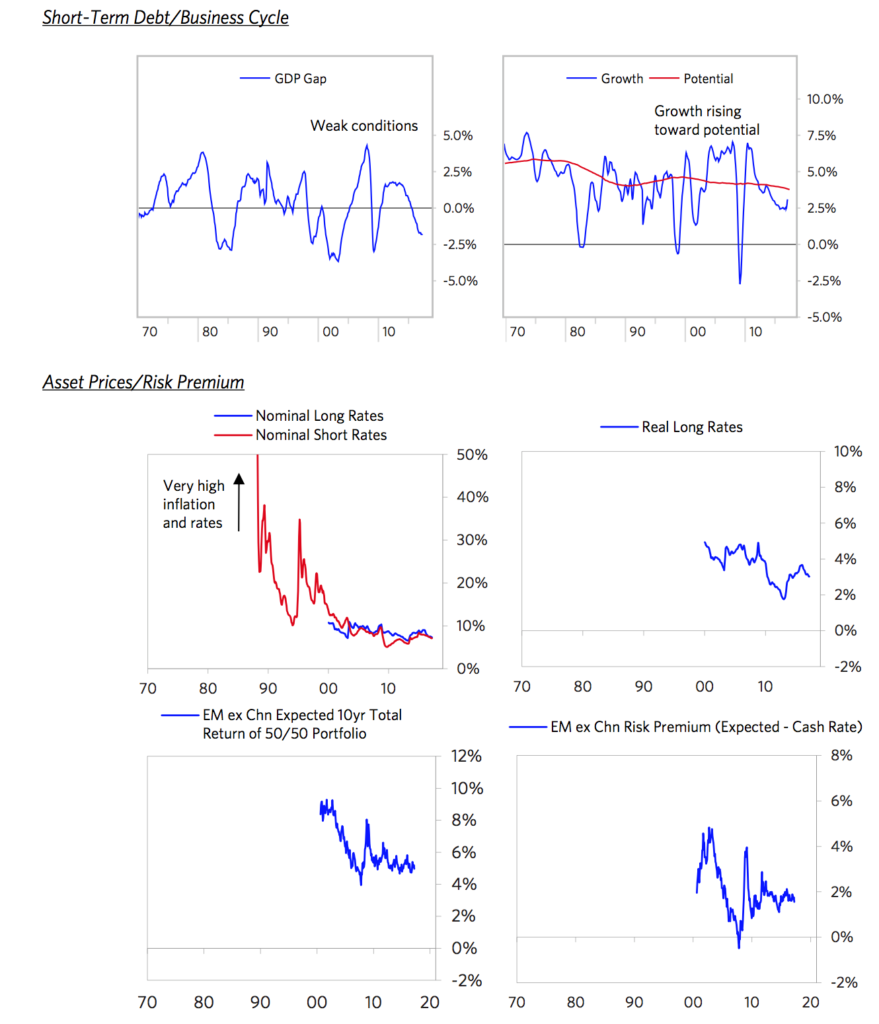

1) Short-Term Debt/Economic Conditions Are Good

As shown below, both the amount of slack in the world economy and the rate of growth in the world economy are as close as they get to normal levels. In other words, overall, the global economy is at equilibrium.

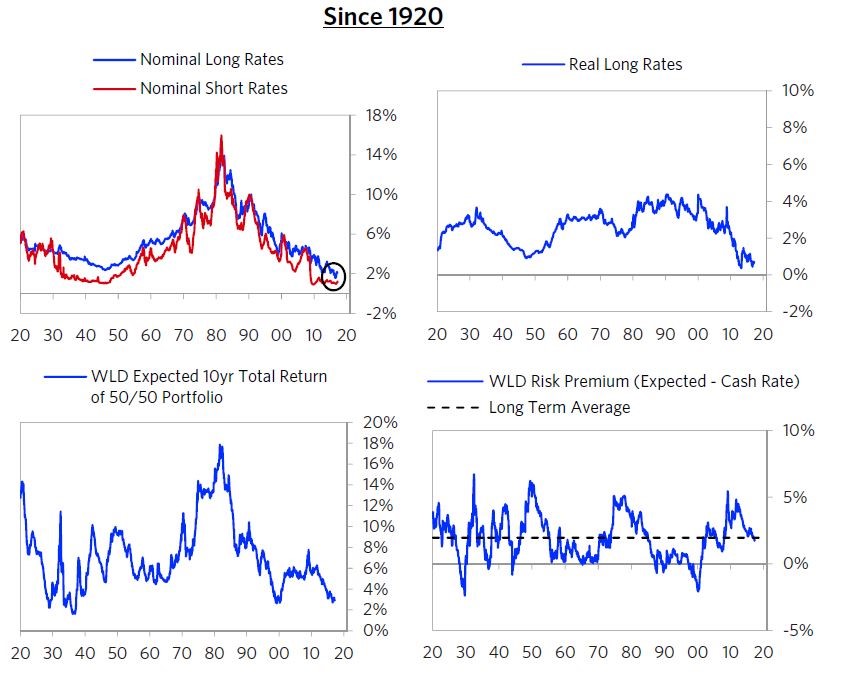

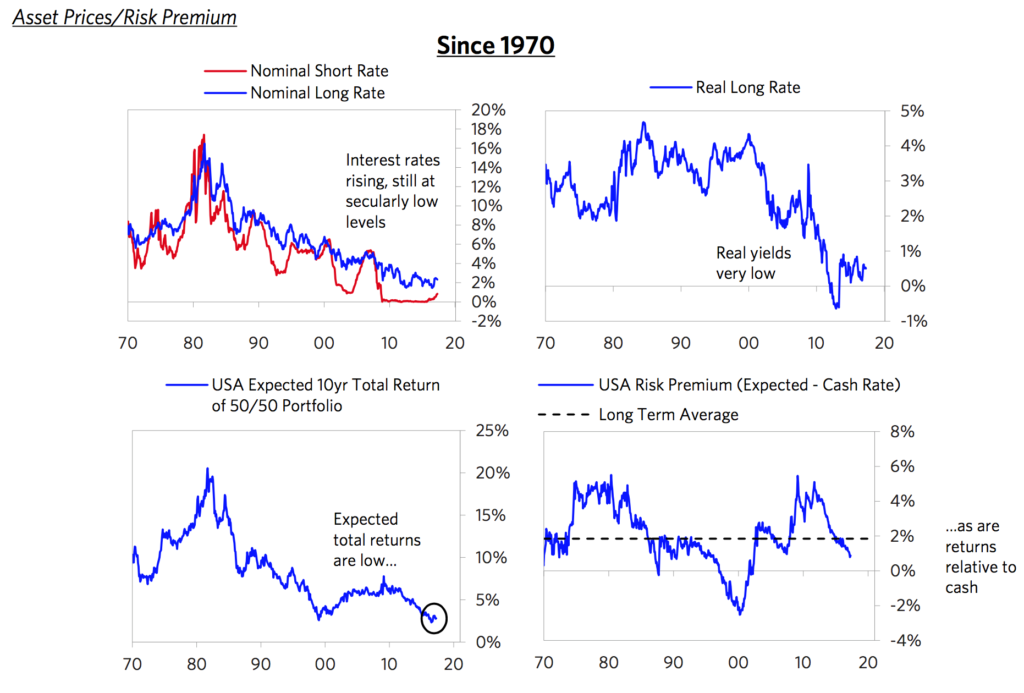

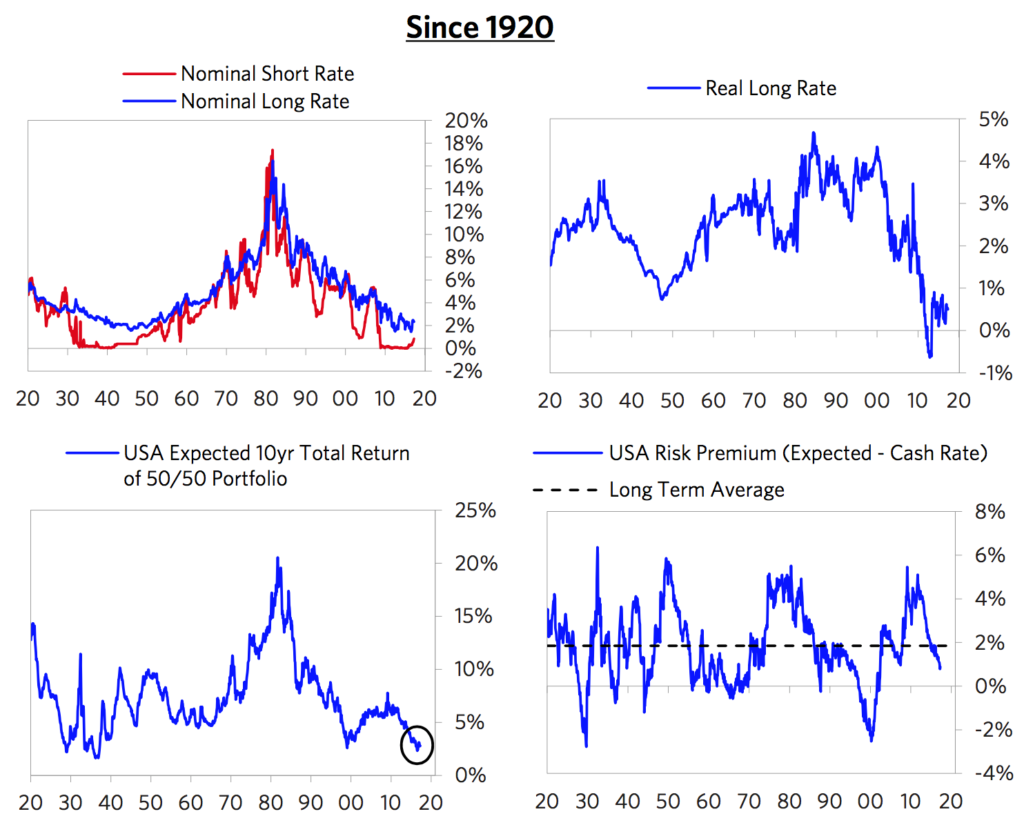

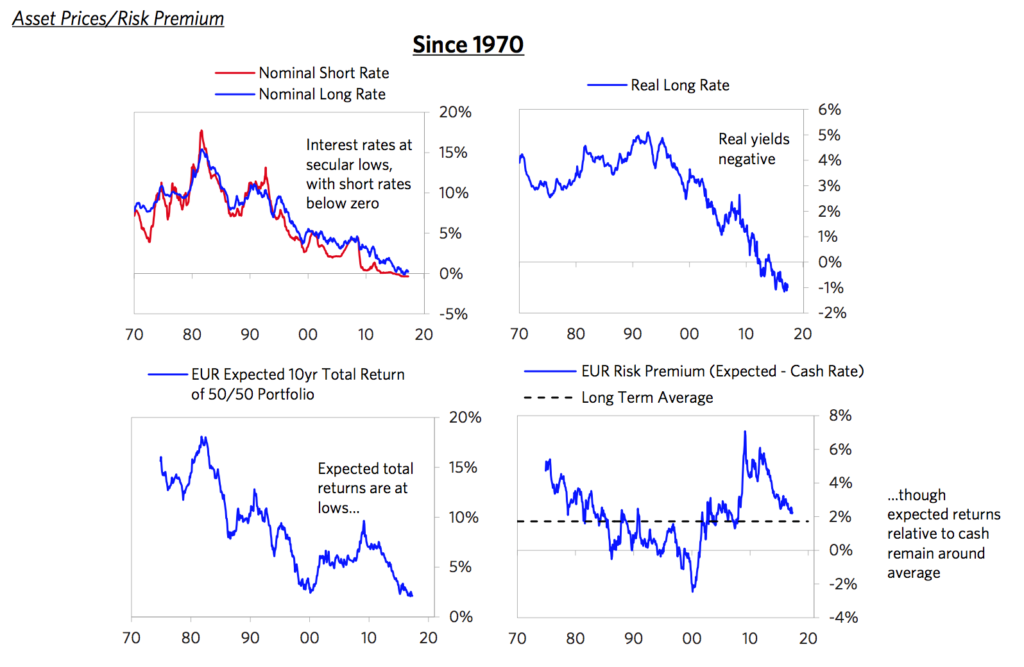

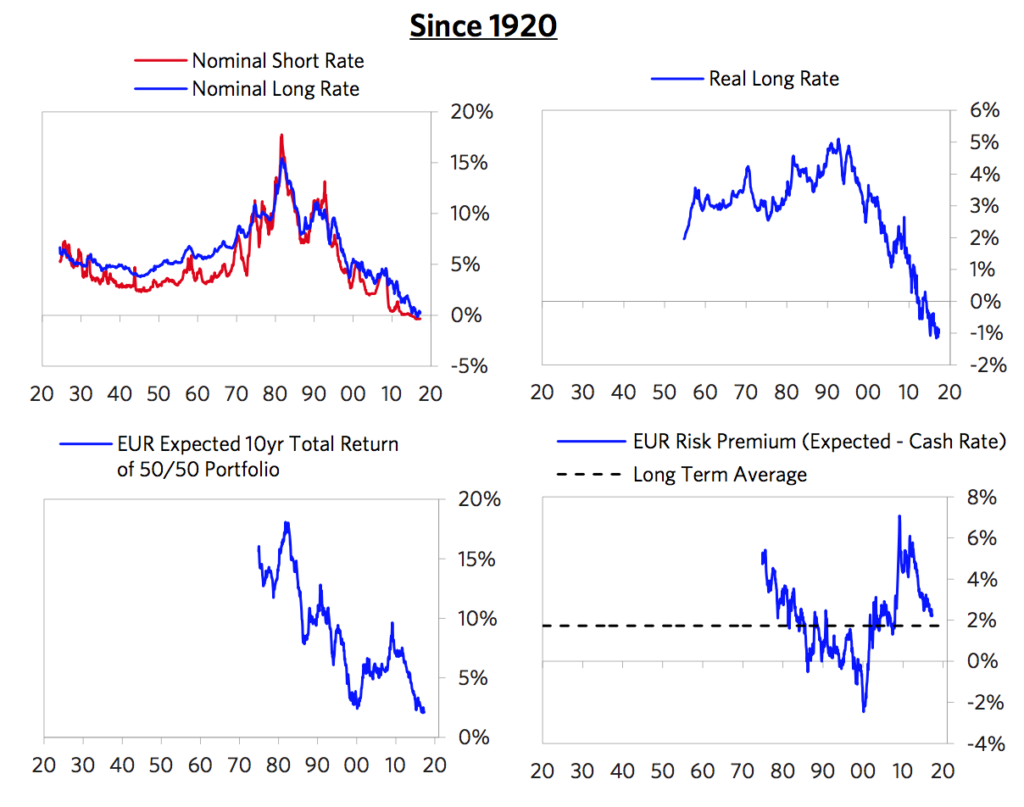

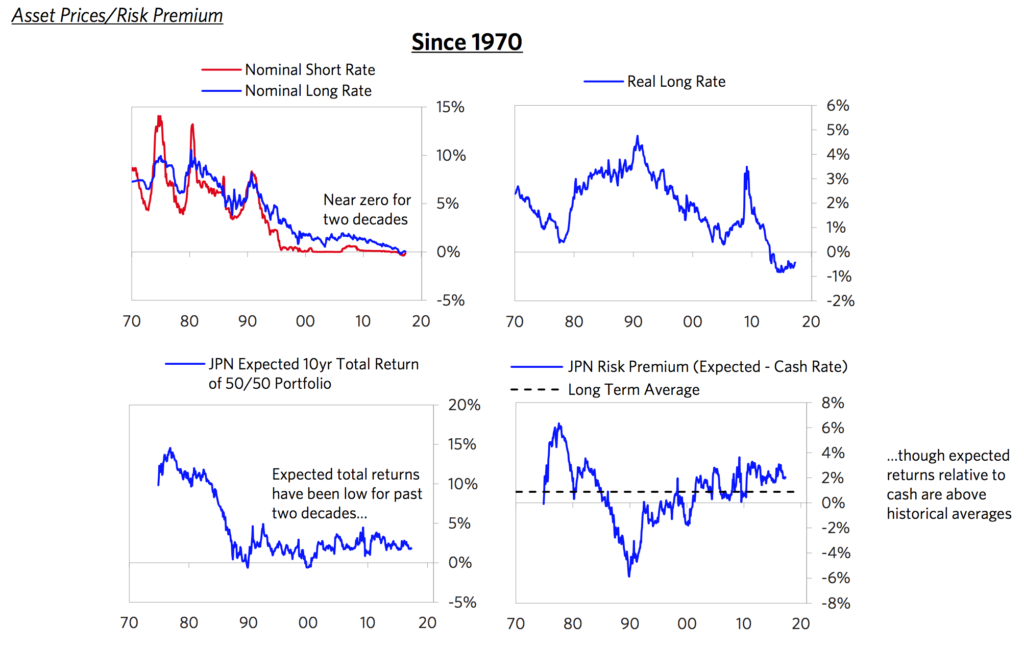

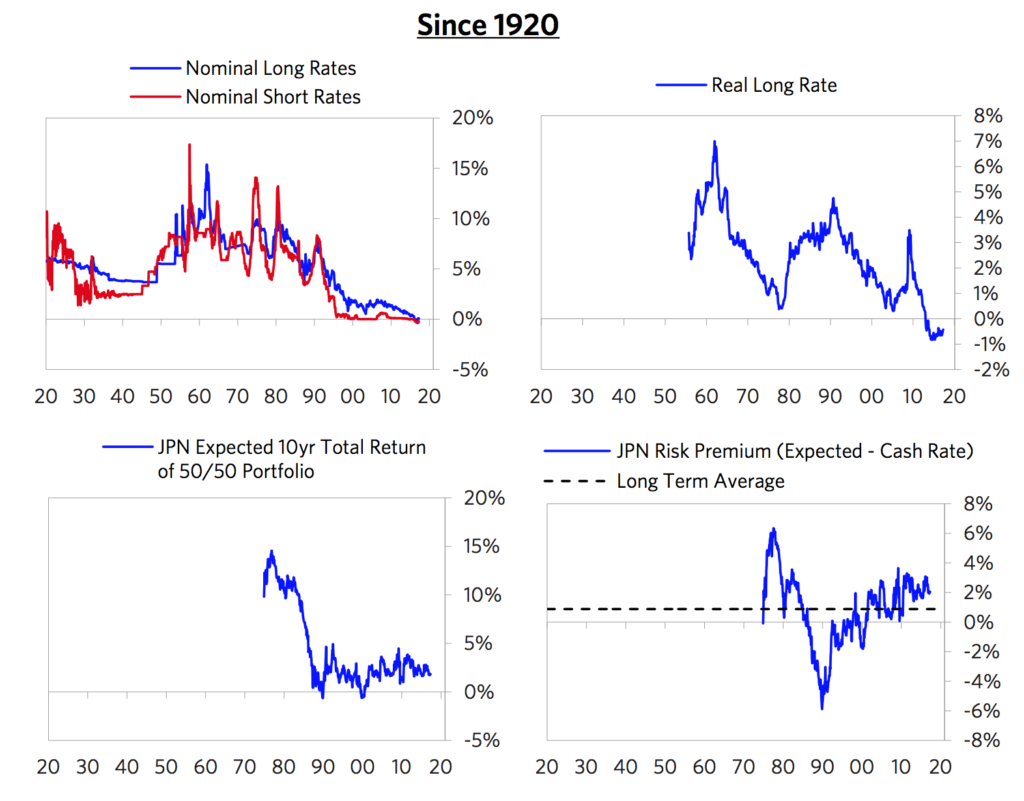

2) Assets Are Pricing In About Average Risk Premiums (Returns Above Cash), Though They Will Provide Low Total Returns

Liquidity is abundant. Real and nominal interest rates are low—as they should be given where we are in the long-term debt cycle. At the same time, risk premiums of assets (i.e., their expected returns above cash) are normal, and there are no debt crises on the horizon.

Since all investments compete with each other, all investment assets’ projected real and nominal returns are low, though not unusually low in relation to cash rates. The charts below show our expectations for asset returns (of a global 50/50 stock/bond portfolio). While those returns are low, they’re not low relative to cash rates.

Relative to cash, the ‘risk premiums’ of assets are about normal compared to the long-term average. So, both the short-term/business cycle and the pricing of assets look about right to us.

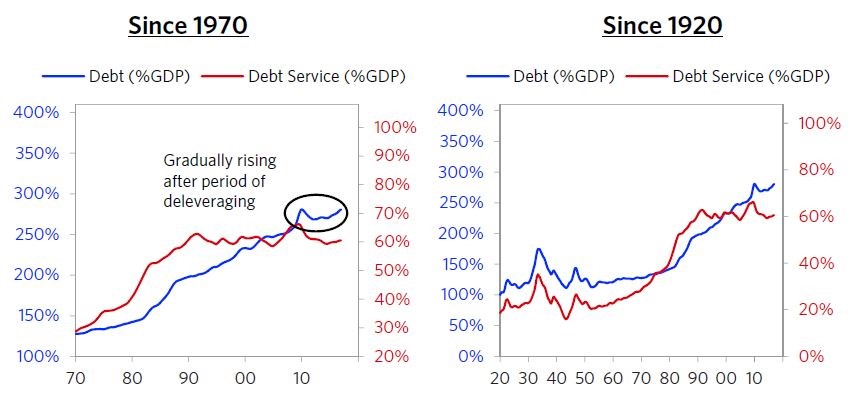

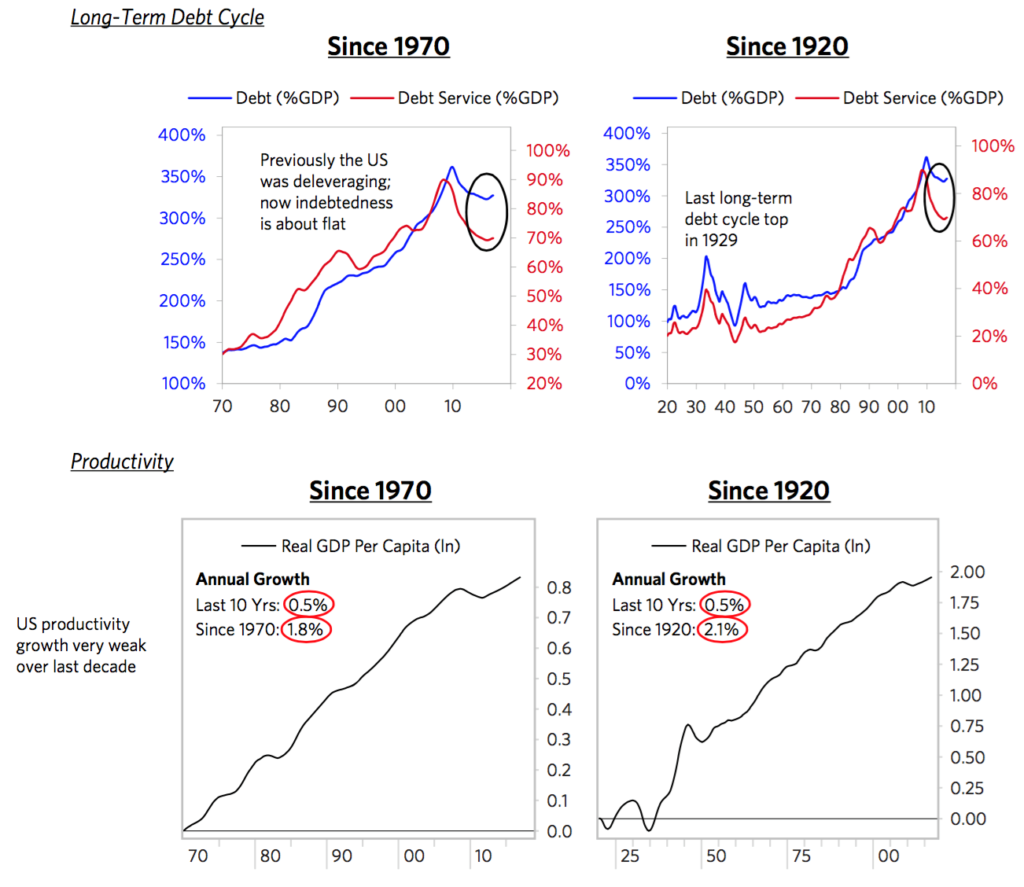

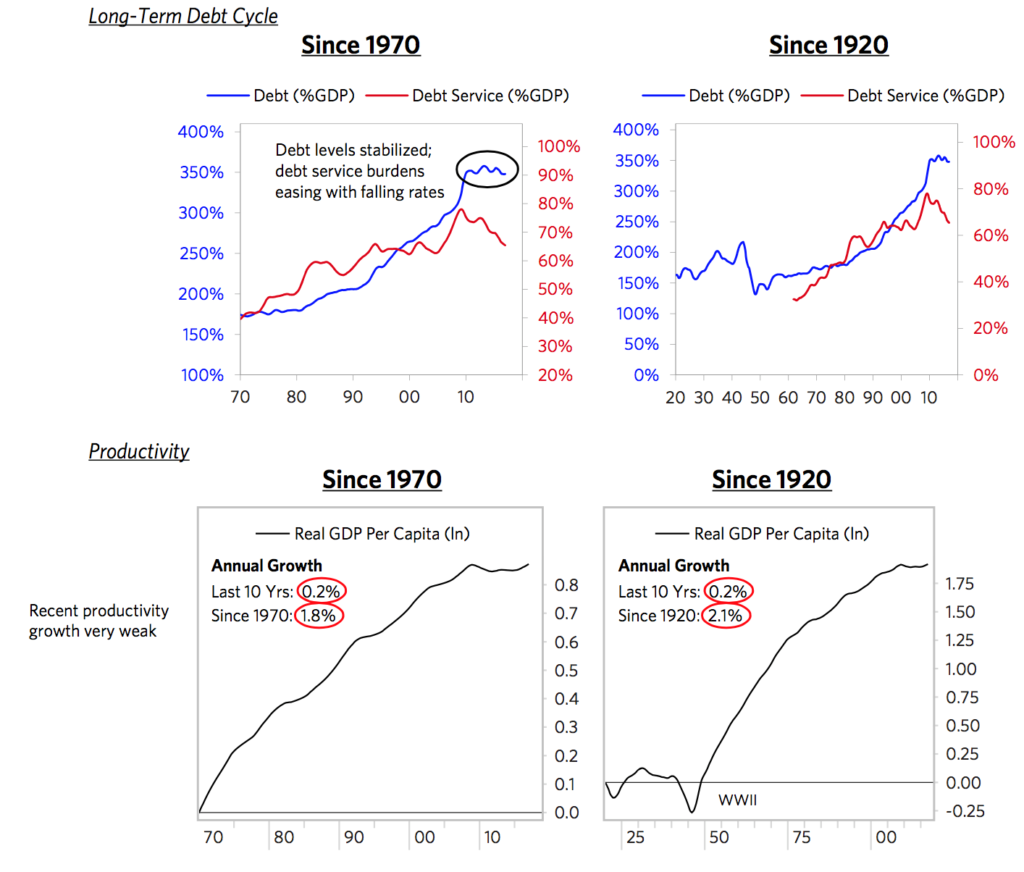

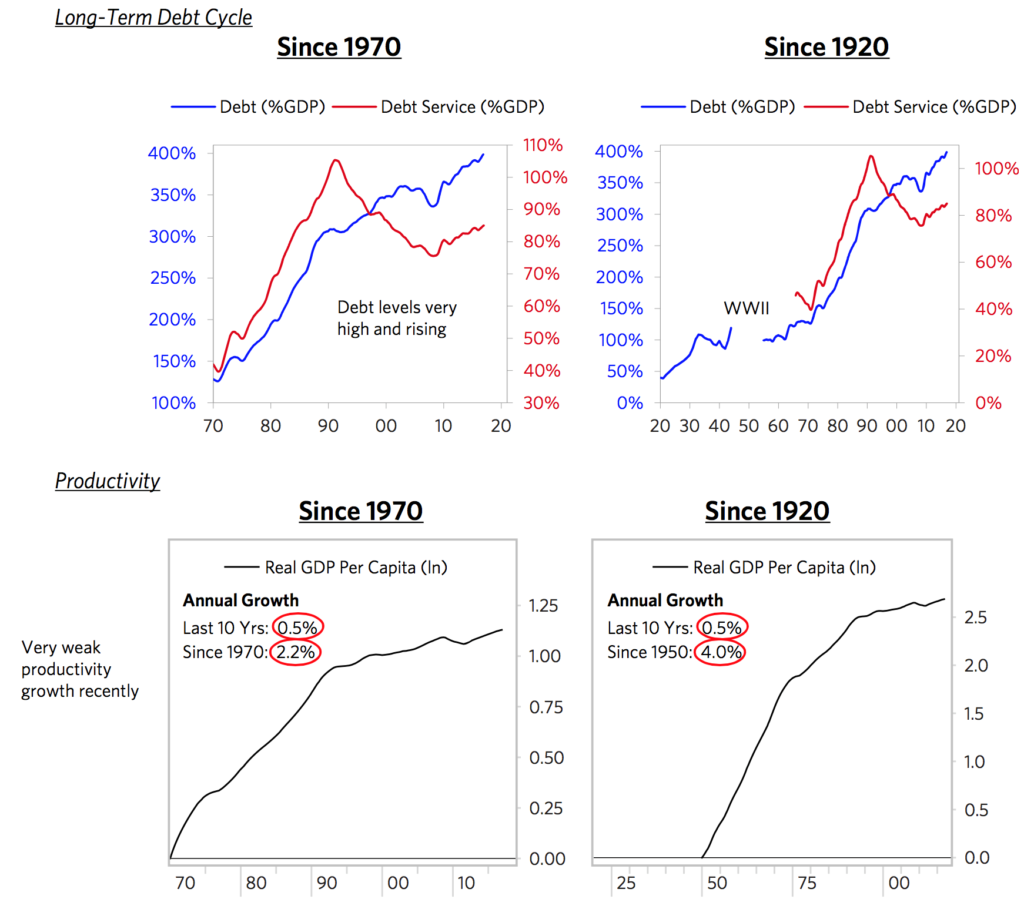

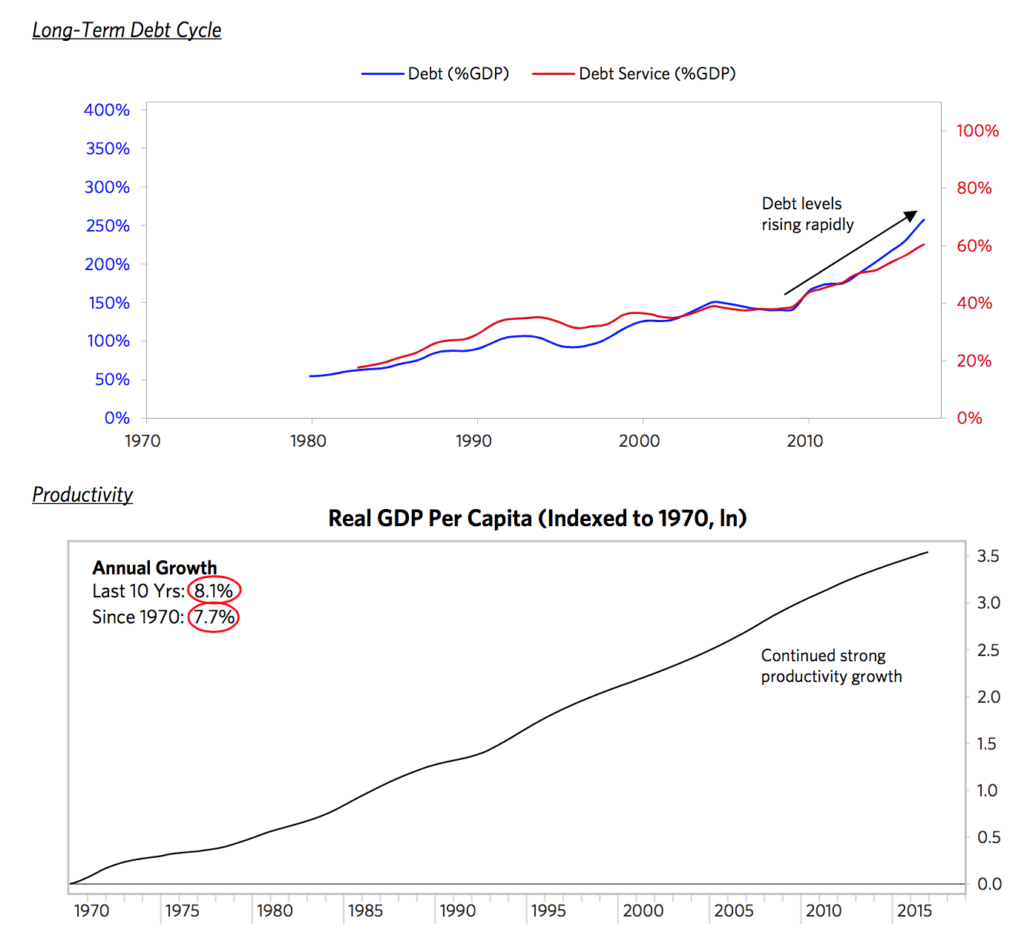

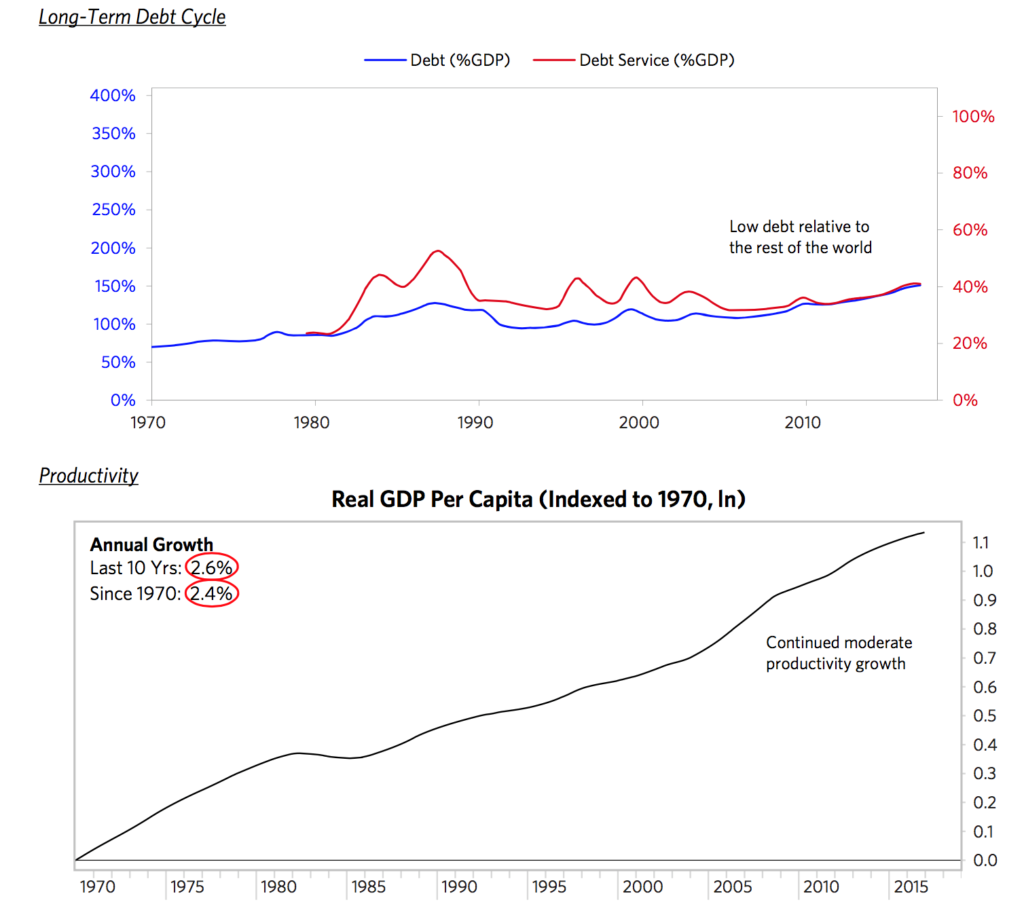

3) The Longer-Term Debt Cycle Is a Negative

Debt and non-debt obligations (e.g., for pensions, healthcare entitlements, social security, etc.) are high.

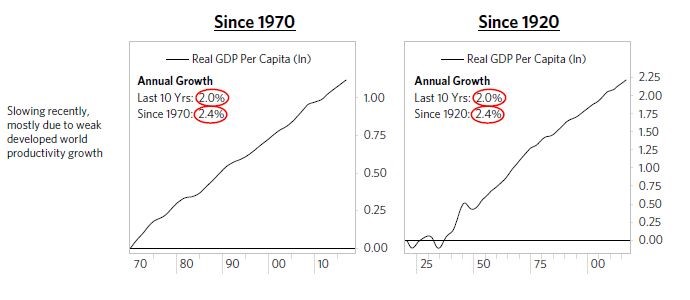

4) Productivity Growth Is Low

Over the long term, what raises living standards is productivity—the amount that is produced per person—which increases from coming up with new ideas and implementing ways of producing efficiently. Productivity evolves slowly, so it doesn’t drive big economic and market moves, though it adds up to what matters most over the long run. Here are charts of productivity as measured by real GDP per capita.

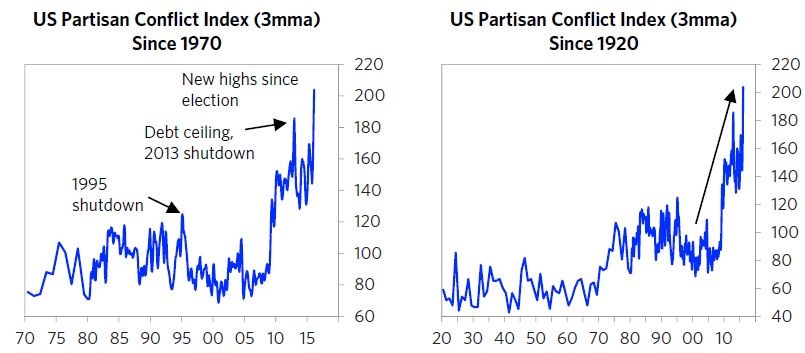

5) Economic, Political, and Social Fragmentation Is Bad and Worsening

There are big differences in wealth and opportunity that have led to social and political tensions that are significantly greater than normal, and are increasing. Since such tensions are normally correlated with overall economic conditions, it is unusual for social and political tensions to be so bad when overall economic and market conditions are so good. So we can’t help but worry what the social and political fragmentation will be like in the next downturn, which, by the way, we see no reason to happen over the next year or two.

Below we show a gauge maintained by the Federal Reserve Bank of Philadelphia that attempts to measure political conflict in the US by looking at the share of newspaper articles that cover political conflict from a few continuously running newspapers (NYT, WSJ, etc.). By this measure, conflict is now at highs and rising. The idea of conflicts getting even worse in a downturn is scary.

Downturns always come. When the next downturn comes, it’s probably going to be bad.

Below, we go through different countries/regions, one by one.

Looking at the Individual Economic Blocs

United States

As shown below, the US is around equilibrium in the mid-to-late stages of the short-term debt cycle (i.e., the “in between” years), and growth remains moderately strong. Secularly, the US is at the end of the long-term debt cycle. Debt levels are high and have leveled off after a period of deleveraging. The Fed has started to tighten gradually, but interest rates remain low, so the Fed has limited room to ease in the event of a downturn. And as we’ve covered in prior Observations (so won’t go into here), the US is in a period of exceptional political uncertainty as the new administration’s policies continue to take shape.

Eurozone

While there are two Europes within Europe, we will talk about the Eurozone as a whole (as we have covered the different parts in other Observations). The region is around cyclical equilibrium, but this masks significant divergences between depressed periphery countries and Germany, where the economy is running hot. In response to ECB stimulation, growth has picked up a bit, but inflation is still very weak and below the ECB target. Secularly, Europe is also at the end of the long-term debt cycle. Debt levels are high and haven’t fallen much. Nominal interest rates on both the short and the long end are around zero and are priced to stay low for years. We won’t go into detail here, but Europe also faces one of the most challenging political backdrops due to the growing support for populism.

Japan

In Japan, policy makers are trying to reverse decades of ugly deflationary deleveraging and shift to a beautiful deleveraging. As shown below, over the last several years, the BoJ’s policies have produced a cyclical upswing and eased deflation. Japan is now around its cyclical equilibrium, growth rates have picked up a bit, and inflation is still very low but the economy is no longer in deflation. Secularly, Japan is at the end of the long-term debt cycle, with the highest debt levels in the developed world (which the BoJ is monetizing at the fastest rate). Debt is still rising, driven by government borrowing. Interest rates have been around zero for two decades and are priced to stay there.

China

We’ve previously described that China faces four big economic challenges (debt restructuring; economic restructuring; capital markets restructuring; and the balance of payments/currency issue) that are being well managed. We won’t go into these challenges here other than to emphasize that they are an important backdrop for the perspective shown below. Cyclically, overall levels of activity in China are neither too high nor too low; growth has accelerated and is now strong; and while inflation has picked up some, it remains modest. Debt levels are high and growing rapidly. Interest rates remain relatively low, though these have risen some recently. Under the hood, these aggregate conditions are the net of “two economies” that look very different: a slowing, heavily indebted “old economy” with pockets of excess capacity, and a steadily expanding “new economy” driven by higher-end industries and household consumption.

Emerging Markets ex-China

Obviously, this category aggregates many countries with many different sets of circumstances, which we won’t get into here. Overall, cyclical conditions in EM ex-China are a bit weaker than in the developed world, reflecting, that several of the largest countries (e.g., Brazil, Russia) are now recovering from balance of payments adjustments. But the longer-term picture is comparatively stronger. These EM countries haven’t yet seen much of a productivity slowdown akin to what the developed world has seen, and debt burdens remain low.

Article by Ray Dalio, LinkedIn

SBB here: I hope that gives you some footing for state of where we are within the economic cycle in the U.S., the developed world and the emerging markets.

Overall, debt remains the significant issue and it is showing up in low productivity, which ultimately hurts long-term growth.

I like how Ray gets right to the point. No wasted moves. I hope you found his insights as helpful as I did.

As I sat with a good friend and advisor client in Dallas this week, he shared the following Dalio piece with me. “Founder of world’s largest hedge fund says ‘magnitude’ of next downturn will be epic.” (Source)

Let’s not get “tech wrecked” or “gfc’d” (great financial crisis) on the way to that opportunity. And let’s help as many people as we can.

My two cents: Show Dalio’s piece to your clients. Advise them to be careful not to buy into the long-term buy-and-hold passive investment trap. It can work for the rich and wealthy over 30 years, like past cycle tops; it will not work for most. The vast majority of people are prone to allow fear to rule reason. Investor behavior is well documented. It’s not good.

This time, most of the money is in the self-directed hands of pre-retirees and retirees. This group can least afford to take the hit. The group that doesn’t have the 10 to 15 years it may take just to get back to even. The math of loss and time needed to recover simply doesn’t work.

Debt and demographics are choking productivity. The fix remains in the future. It requires a political solution. That looks unlikely. Like 2008, I believe it will take a crisis to get our elected officials moving. Keep an eye on the recession indicators (posted below). Overall, participate and protect… play defense now so you can play offense later.

Let trend following, risk managed processes help you seek growth, reduce volatility and limit your downside loss. That’s what I mean by defense. And get mentally prepared to be a buyer when everyone else is a seller. “Good near term, scary long term… epic decline.” In this is a great opportunity for your business. Most importantly, it is a great opportunity for your clients and their retirement futures.

Charts of the Week — Favorite Recession Charts

You’re probably all “charted” out from Ray Dalio’s insights… long but important. So let’s keep this week’s “Charts” section short.

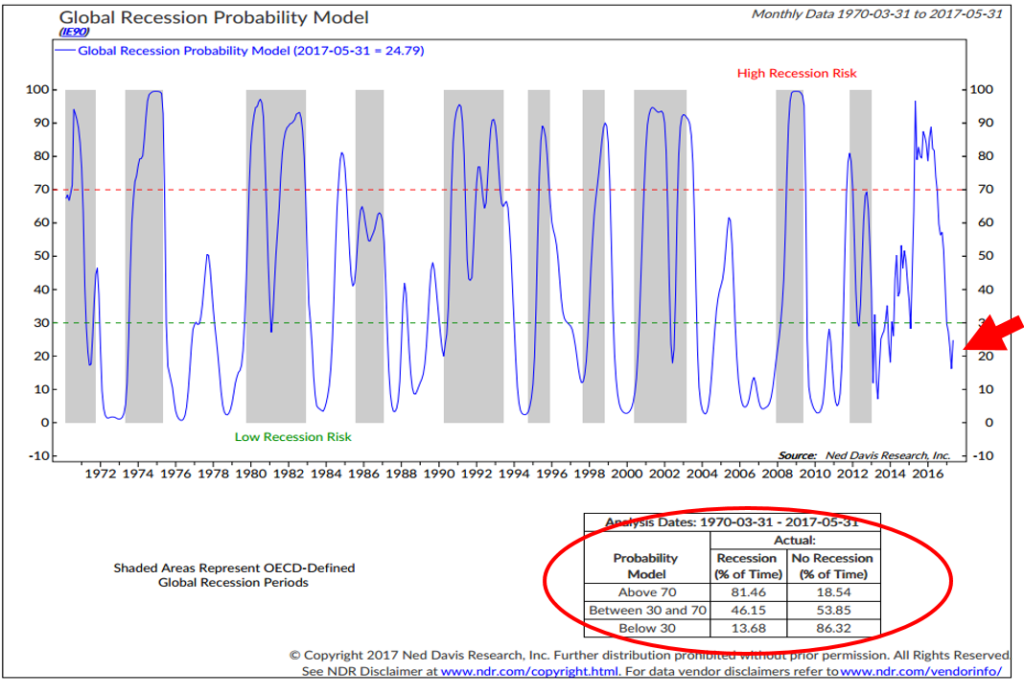

Each month I like to share with you my favorite recession watch charts. They are leading indicators. With “the long term looks scary” prediction in mind, most of the scary happens in recession and if we can get ourselves out in front of them, then that can help us better manage risk. Stocks can decline 40% to 60% or even 75%, like technology in 2002. The good news is that the current risk of recession is low.

Chart 1: Global Recession Probability Model = “Low Recession Risk”

Here is how you read the chart:

- Readings below 30 reflect low recession risk (red arrow)

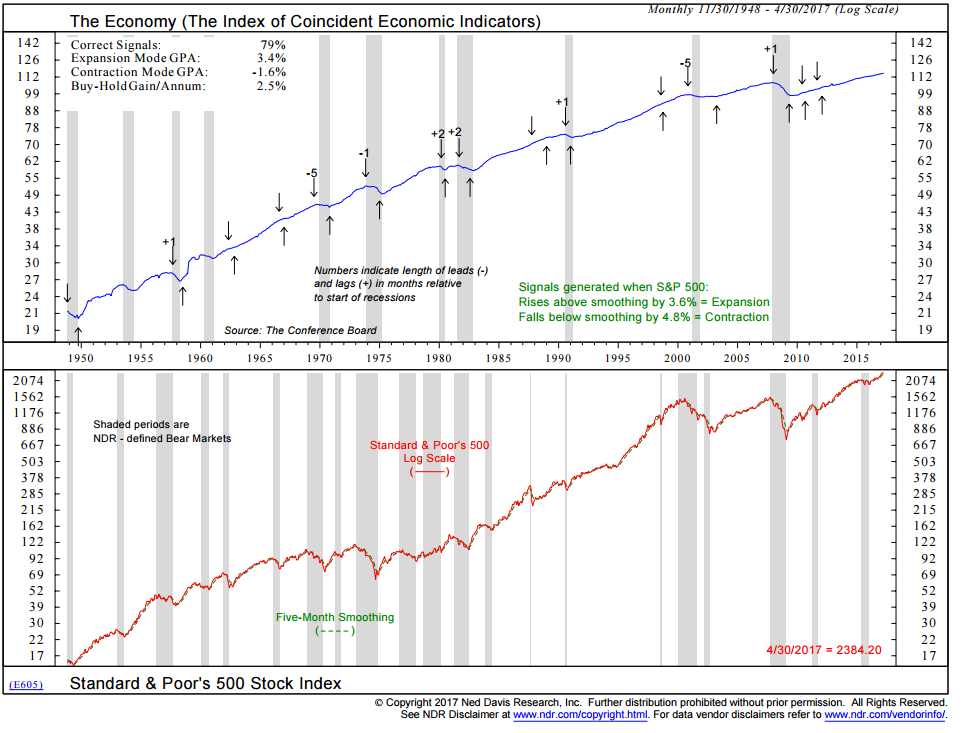

Chart 2: U.S. Recession Watch – No Sign of Recession

Here is how you read the chart:

- This one is simple. It looks at the S&P 500 Index in comparison to its five-month smoothed moving price average.

- When above the green dotted line (lower section), low recession probability.

- When below the green dotted line, high recession probability.

- Note “correct signals” since 1948 at 79%.

- Not perfect but pretty good. The idea here is that the stock market is a leading economic indicator (which it is).

Lakshman Achuthan, Co-Founder of the Economic Cycle Research Institute (ECRI), is presenting next week at the 2017 Strategic Investment Conference. He’s good. I’m interested in what his models are telling him. More on him next week.

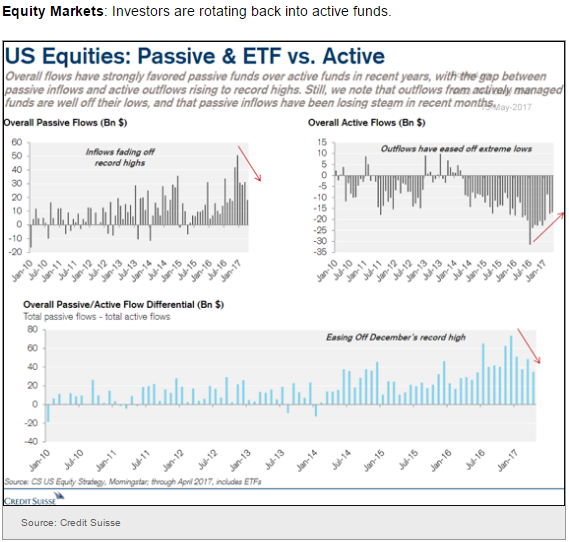

Chart 3: Equity market investors rotating back into active funds

Maybe investors are seeing the value in active management. I think active managers feel just as bad as the value managers felt back in 1998 and 1999. They were told their outdated ways were done. Until they were back in vogue. Sure feels like 1999 to me.

Source: WSJ The Daily Shot

Finally, this caught my eye this week: “AI Predicts Next U.S. Recession to Start in 2019.” San Diego-based Intensity Corporation has developed a machine learning forecasting engine. I’m going to do more research on this group. The engine is designed to deliver forecasts that are based on large sets of real-time data of different kinds and be responsive to the economy and market conditions in real time.

As of May 11, Intensity’s artificial intelligence (“AI”) process was signaling March 2019 as the expected start date for the next U.S. recession. However, this isn’t a fixed date. The forecast will change based on changing economic conditions. Earlier last year, the model was forecasting a start to the next recession in December 2017. By November 20, 2016, the model had pushed that date back to November 2018. Now, it sits at March 2019. Does it work? We don’t yet know. Source: http://www.financialsense.com/ai-predicts-next-recession-start-2019

Trade Signals — S&P 500 2,400, The Trend Remains Bullish for Stocks and Bonds

S&P 500 Index — 2,400 (5-17-2017)

Notable this week: No new signals since last week’s post. The equity market, as measured by the Ned Davis Research CMG U.S. Large Cap Long/Flat Index, remains bullish. Don’t Fight the Fed or the Tape remains neutral. The Zweig Bond Model remains in a buy signal. The short-term gold trend indicator is in a sell signal. Investor sentiment is now Extremely Optimistic, which is S/T bearish for equities. Inflationary pressures are high but moderating. The overall weight of trend and breadth evidence supports a continuation of the cyclical equity bull market.

Click here for the charts and explanations.

Personal Note — It’s All About Team

I had a nice talk with Avi this week. He’s been with me for many years and has two young boys. Those early years with children are hard, as you well know, but as my dad used to say, “The prize is worth the price.” I sure understand that better now and sit beautifully on the other side of all that hard work when the children are young. I feel Susan and I are now collecting the dividends and, boy, do they feel good.

It is true in sports (all those wind sprints, hard days, disappointments and victories), true in investing, true in business and true with most things earned in life. Love, of course, is the best prize. Avi will blink and his young boys will be young men.

And here is my blink. Yesterday, I rushed from my meeting in Dallas to DFW only to find a 90-minute delay of my flight. Not good. My son, Matthew, a high school senior, was being honored at his school’s sports achievement ceremony. Reflecting back about three years ago, I dropped him off at a Philly Junior PGA golf tournament in New Jersey. He complained of a stomachache on the ride there. Was it sickness or nerves? I told him he’s playing. I dropped him off and told him to give it his best and not to worry about the outcome. Adding, as is the rule in our house, you committed to the tournament and you have to honor that commitment. Everything in me wanted to pick him up and hug him. I helped him sign in and I left. That was really hard to do.

About 20 minutes later, he called in tears. He had vomited as he walked to his ball on hole #1. Halfway through the second hole he bailed. I told him he could wait on the patio at the course or play. I said I’d be back in four hours and hung up. As I sat in a local coffee shop, the phone rang again. Just 20 minutes had passed. He was distressed. I went and picked him up. The car ride was quiet. He broke the silence. I shared my disappointment. Quietly, I had no idea how I could help him overcome his fear.

Here we are three years later and I’m rushing to his awards event. I’m stuck in seat 12F on an American Airlines flight to Philadelphia. A communications issue we are told. Ninety minutes later, we are in the air. I was worried I’d be late and I was. The event had started, but fortunately, the lacrosse team is big. Just minutes after I arrived, Matt’s golf coach spoke of his athletes. A proud dad watched Matt’s accomplishments. Captain of his golf team, a 3 handicap and an individual third place finish in a competitive league. I was happy he faced that fear three years earlier and learned to compete.

A quiet leadership style has served Matt and his team well. His personal standing came second to his team’s results. He might score poorly on a given day but if his team won, that’s what lifted him most. While Matt finished third, his team came in second. That made for a happy Matthew. To him, it’s all about the team. I like that. I’m not sure how we got from there to here but what a dividend. I thought of Avi’s young boys. I thought of my young boys, now young men. Hug your kids. The ride goes by so fast.

Matthew Blumenthal

I fly to Orlando on Monday for the 2017 Strategic Investment Conference hosted by good friend John Mauldin. It is one of the best economic gatherings. The speaker lineup is outstanding. David Rosenberg, Dr. Lacy Hunt, David Zervos, Mark Yusko and geopolitical strategists Ian Bremmer and George Friedman… and many more. The debt solution requires a political resolve. Here and globally.

I listened to Bremmer last month in NYC. I’m looking forward to seeing him debate Friedman and seeing both be pressed on hard questions by the audience. Yusko is a great story teller and doesn’t hold back. Hunt is one of my all-time favorites and I remember many days listening to Rosenberg when he was a Merrill Lynch analyst and I a young financial consultant. I’m looking forward to Mauldin’s open and unique format. No one walks away unchallenged. I’ll share my notes with you in the weeks to come.

Here is to the many hard won dividends in your life. Wishing you a great weekend!

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group