Following the election, stock market participants gained optimism on the view that the new administration would push through a reduction in regulations, sharply boost infrastructure spending, and achieve broad tax reform. Developments last week suggested that the Trump agenda was at risk. However, even with one-party control in Washington, it was always going to be an upward battle to get things done. Moreover, even if the full legislative agenda were to be achieved, economic growth would surely be restrained by the demographics.

Prior to his dismissal, FBI Director Comey was investigating ties between the Trump campaign and Russia. The day after his firing, Trump met with Russian officials in the oval office, where he has been accused of sharing “highly classified” information (that’s not necessarily illegal, but it doesn’t look good). While the administration put forth a number of reasons for Comey’s firing, the president admitted a couple of days later (on TV) that Comey was let go due to “the Russia thing.” President Trump has refuted the claim of Russian ties with his campaign and called the investigation “a witch hunt,” which, coincidentally, is the same phrase Richard Nixon used at the start of the Watergate investigation (you can’t make this stuff up). Critics of the president charge that Comey’s firing was obstruction of justice, which Trump appeared to admit to on live TV.

Is it too soon to talk about impeachment? That’s a rhetorical question, as people have already been discussing the possibility. The proper question is whether impeachment is likely. Recall that the House of Representatives needs only a simple majority to impeach. That means he would be put on trial in the Senate, where a two-third majority would be needed to remove him from office. At present, this doesn’t seem likely. Impeachment is essentially political, drawn along party lines. Andrew Johnson and Bill Clinton were both impeached. Neither was removed from office by the Senate (Johnson came close with a margin of a signal vote, 35-19, and Clinton was acquitted on two charges, 45-55 and 50-50). Nixon would have almost certainly been impeached, but resigned before that could happen.

While impeachment doesn’t appear to be likely anytime soon, the investigation will consume much of the oxygen on Capitol Hill over the next several months. Robert Mueller, who was confirmed as FBI Director by a Senate vote of 98-0 and served 12 years, has only just been appointed as special counsel. He will have to hire a team, find a secure location to conduct the investigation, and so on. Hearings will come later, if at all.

Stock market participants were only briefly sidelined by last week’s developments, still believing that the Trump agenda is intact. However, things are never easy in Washington.

As noted previously on these pages, infrastructure spending costs money and House members are unlikely to want to add to the budget deficit (except where tax cuts are concerned). Broad tax reform is virtually impossible, as nobody wants to get rid of their tax deductions. If you can’t pay for tax cuts by eliminated deductions, how about a border tax? That is dead on arrival, as it would prove extremely disruptive to supply chains. Lower tax rates are still possible (and likely), but on a much smaller scale than was hoped for previously. A tax holiday on foreign earnings is also possible, but studies show that when this was done during the Bush administration, the vast majority went to dividends or stock buybacks, and not to capital investment.

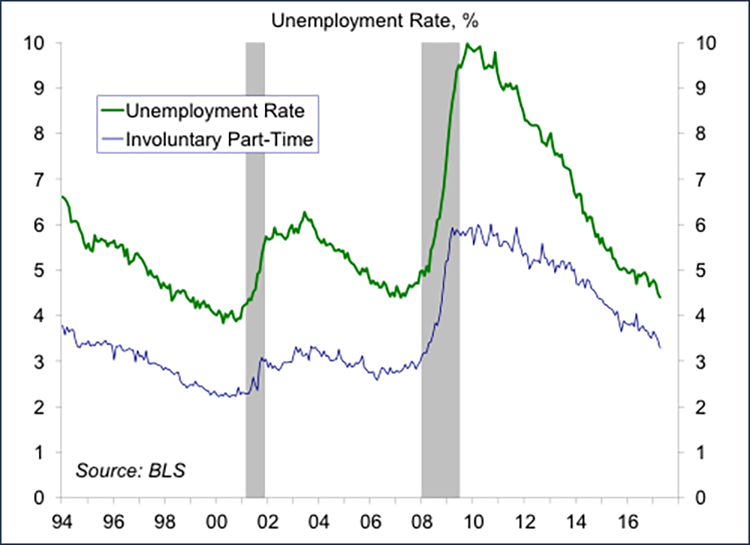

Still, even if the full Trump agenda were to be enacted, the economy is facing increased constraints in the labor market. Labor force growth is currently less than a third of what it was a few decades ago. So, unless we increase immigration or are able to sustain an unprecedented increase in productivity growth, the underlying trend growth in GDP will be limited. Granted, there may be greater slack in the job market than there appears. If that’s the case, GDP growth could pick up over a few quarters, but limits will eventually be reached, leaving growth near its long-term trend (1.5-2.0%, depending on the underlying pace of productivity growth).

For the Fed, the tighter job market is the main factor in moving toward a more neutral policy. The inflation outlook, the other key factor, remains moderate, with mixed pressures.

Investors who expect that the full Trump agenda will be enacted, lifting the pace of growth, will be disappointed. Yet, while slower than in previous decades, GDP growth is still expected to remain positive. Without any sense of irony, Trump campaign events (before and after the election) ended with the Rolling Stone’s “You Can’t Always Get What You Want.” And, indeed, if you try sometimes, you get what you need.