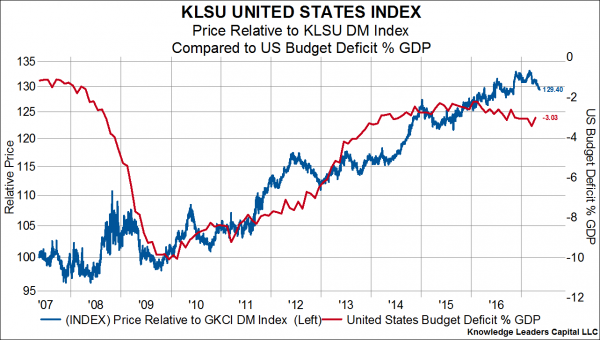

USD, Valuations, Probability of Rising Budget Deficit all Point to US Equity Underperformance

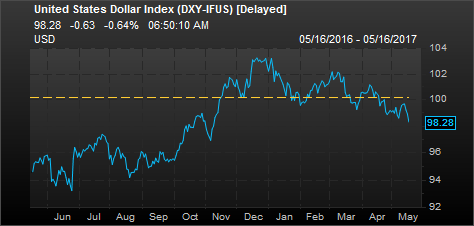

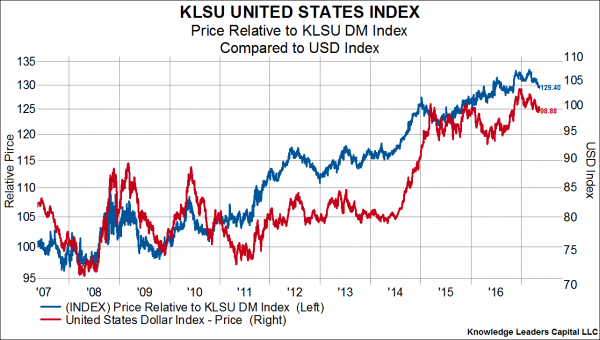

With the USD now about 5% off its January peak and having made a series of four lower lows and lower highs, it’s fair to say that the period of US dollar strength we witnessed for most of 2016 has come and gone. This is quite important for equity investors because the relative performance of US and foreign equities is heavily influenced by the direction of the US dollar. As the dollar rises, US equities tend to outperform. As the dollar falls, the US equities tend to underperform. Chart 2 shows this dynamic rather clearly.

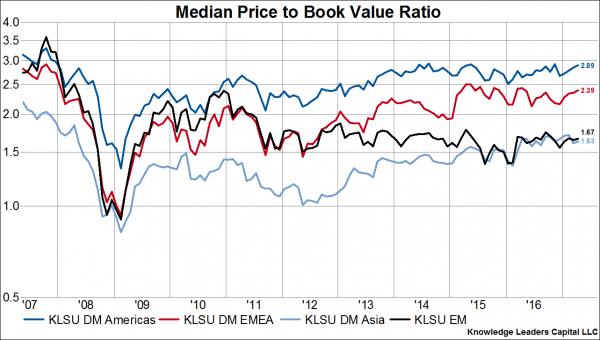

Additionally, there are other factors that are lining up in favor of US equity underperformance, namely relative valuations and the US budget deficit. Experienced investors understand that valuations are rarely a catalyst for major market moves, but they are supportive of longer-term trends. As chart 3 shows, the median DM Americas company is valued at the high end of the price/book value range over the last decade. Meanwhile, the median DM Asia company and the median EM company are hovering somewhere in the middle of their historic ranges. This dynamic is supportive of foreign equity outperformance.