Wesbury sees other signs of a pickup in economic growth ahead. Business fixed investment soared in the 1Q, growing at a 9.4% annual rate, the fastest pace for any quarter since 2013. And corporate profits are accelerating. With roughly 60% of the S&P 500 companies having reported for the Q1 so far, earnings are up over 15% from a year ago.

Meanwhile, home building grew at a 13.7% annual rate in the Q1, the fastest pace for any quarter since 2015. Although the recovery in home building is almost seven years old, Wesbury expects gains in housing to continue for at least the next couple of years as builders battle pent-up demand from population growth and years of under-building.

Wesbury admits that consumer spending grew at a disappointing 0.3% annual rate in the 1Q, but he sees signs of a hearty rebound in the current quarter. First, autos sales were unusually weak in the 1Q, in part due to an unusually late March snowstorm in the East.

Second, unusually warm weather in January and February suppressed utility (heating) output, which was a drag on GDP. Third, that same warm weather may have suppressed winter clothing sales. Wesbury is confident that these patterns have reversed and economic growth is now on the rebound.

Wesbury concludes: “Although it’s still early, we are looking for real GDP to grow at a 3.5% annual rate in Q2. That would put the first half of the year at a growth rate of 2.1%, right at the Plow Horse trend. Even more important, the Trump Administration looks serious about supply-side tax cuts that will boost the economy’s long-term growth potential.”

On Wesbury’s final point, I would caution that there is no assurance that President Trump will get his tax cuts through Congress. Even if he does, it remains to be seen how significant they will be. And then it takes time for them to boost the economy.

There Are Reasons to be Optimistic, But Not 3.5% GDP

Even though the US economy expanded at the slowest rate in three years in the 1Q, and consumer spending ground to a near halt, there were some encouraging signs in the latest GDP report, as discussed above. There were some other positive developments in the 1Q which look likely to be continuing in the 2Q, but are unlikely to boost GDP growth to 3.5% as First Trust and others expect.

First of all, the US labor market is near “full employment” and consumer confidence remains near multi-year highs, suggesting that the mostly weather-induced sharp slowdown in consumer spending in the 1Q was probably temporary.

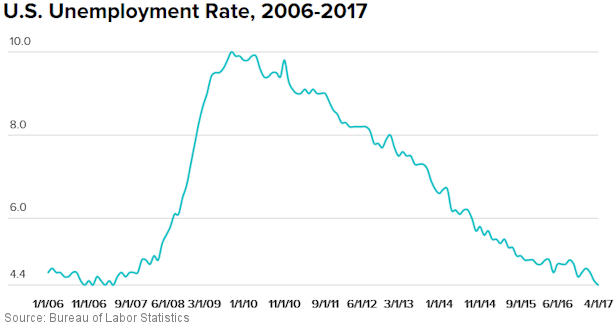

The US economy added a whopping 211,000 net new jobs in April, and the headline unemployment rate plunged to 4.4%, the lowest level in a decade. Most economists agree that the US is now at full employment, meaning the unemployment rate is not likely to go down significantly more.

It’s a situation where employers will have to pay up to hire, because it becomes harder to find workers. That’s why wage growth is expected to pick up. Wages grew 2.5% (annual rate) in April, which is better than in prior years but not considered robust yet. The Federal Reserve says it would like to see wage growth closer to 3.5%.

April’s jobs report showed other signs of progress. US under-employment, which includes Americans in part-time jobs, those marginally attached to the workforce, etc., hit its lowest mark in a decade too. The largest measure of underemployment – known as the “U-6” rate – fell to 8.6%, which is down from 17% in 2010 and even lower than a year ago.

Job gains came across the board. Healthcare added 20,000 new positions, business services gained 39,000 jobs and hotels and restaurants brought on 55,000 more workers. Even construction, mining and manufacturing saw gains in new jobs.

Experts attribute the gains, particularly in manufacturing, to the health of the global economy, and less so to the optimism of Trump's promises for tax cuts, infrastructure spending and deregulation.

Yet despite these positive developments, experts caution that there are still areas of concern. For example, a high level of “prime age” Americans between ages 25 and 54 remain out of work for a variety of reasons. Although part-time jobs have declined, there are still 5.3 million Americans working in part-time jobs because they can’t find full-time work.

It remains to be seen if the US economy has fully emerged from the 1Q slump in the 2Q. Clearly, the 0.7% GDP reading in the 1Q was a big disappointment. However, there were some encouraging elements in the recent jobs reports. The question is, have those positive trends continued and/or accelerated in the 2Q?

We’ll see. The Commerce Department’s first estimate of 2Q GDP growth will not be released until near the end of July.

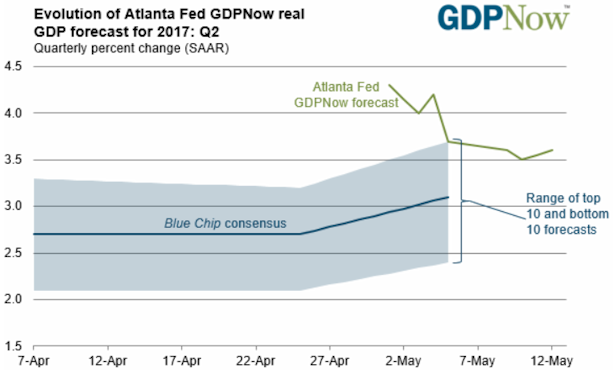

Atlanta Fed Forecasting 3.6% 2Q GDP, But Very Volatile

Another reason many economists are upping their 2Q GDP estimates is the fact that the Atlanta Fed’s GDPNow Forecast has been quite strong over the last month or so. At one point, it was as high as 4.3% and currently stands at 3.6% for the 2Q.

It is important to keep in mind, however, that the GDPNow Forecast is often very volatile. For instance, the GDPNow estimate for the 1Q of this year was as high as 3.4% at one point, yet the final number came in at only 0.7%. For this reason, I would not read too much into the GDPNow Forecast until we get closer to the end of the quarter.

Will Fed Hike Interest Rates at June 14-15 Policy Meeting?

Federal Reserve Chair Janet Yellen and other members of the policy-setting committee have made it clear in recent months that they intend to raise short-term interest rates at least two more times this year. Most Fed-watchers expect another rate hike at the June 14-15 meeting.

However, the much weaker than expected GDP report for the 1Q (+0.7%) has raised new questions about how the Fed should proceed. While the 1Q GDP report was indeed a clear disappointment, there were some positive elements within the report, as discussed above.

Most forecasters now believe the 1Q GDP report was an aberration rather than a trend, and I expect a majority of the Fed Open Market Committee members to agree when they meet again on June 14-15. So I expect another 0.25% hike in the Fed Funds rate target on June 15, barring some other negative news between now and then.

Fed Funds futures agree and now signal a near 90% chance of another Fed rate hike at that meeting. I’ll keep you posted as we get closer to the June 14-15 policy meeting.

All the best,

Gary D. Halbert

|

Forecasts & Trends E-Letter is published by Halbert Wealth Management, Inc. Gary D. Halbert is the president and CEO of Halbert Wealth Management, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, Halbert Wealth Management, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

|

|

| |

| |

| |

| |

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management