“In the short run, the market is a voting machine but in the long run, it is a weighing machine.”

– Benjamin Graham

When Ronald Reagan entered office in 1981, forward return expectations were a high 18.91% (see chart below: green line, left-hand side). Equally important was that risk of loss was a low -4.29% (red line, left-hand side). The prior bear market reached its end, yet few knew it. Scream as one might, clients weren’t buying. The 1966-1982 secular bear market did little to advance an equity market investor’s wealth. In 1981, it was the right time to aggressively own equities.

Today we sit on the opposite end of the seesaw. With valuations high, forward return probabilities near 0% (-0.35% green line, right-hand side in the following chart) and risk of loss at -27.07% (red line, right-hand side), President Donald Trump will have a great deal of trouble making stock returns “great again.”

I’m rooting for tax cuts. But to project the great returns of the Reagan days is a risky wager. Risk versus reward? Zero percent forward probable returns and risk near -30% is a really bad bet.

The above chart compares five-year average total returns of the S&P 500 Index and the maximum drawdowns that have occurred over the last 60 years at associated CAPE readings. (CAPE is the cyclically adjusted price-to-earnings ratio, commonly known as CAPE, Shiller P/E, or P/E10 ratio, is a valuation measure usually applied to the S&P 500 equity market. It is defined as price divided by the average of 10 years of earnings (moving average), adjusted for inflation.)

The following is from 720Global:

Despite the bargain basement equity prices, few investors believed that market trends would reverse. Equity valuations had been low and falling for so many years to that point, the trend became a permanent state in many investors’ minds by way of linear extrapolation.

Contrast that with today. As in early 1981, there is a new president in office with a non-typical background presenting non-conventional economic ideas to aid a struggling economy. Unlike Reagan, however, public support for Donald Trump is marginal.

Additionally, while Reagan’s and Trump’s economic policies may have similarities, there are stark differences between the economic landscapes that prevailed in the early 1980s and today.

Equity investors betting on Reagan in 1981 were investing in an environment where the probabilities of success were asymmetrically high. With Cyclically Adjusted Price-to-Earnings (CAPE) ratios below 10, investors could buy in to a stock market whose valuation on this basis had only been cheaper 8% of the time going back to 1885.

Given the likelihood of success as inferred from valuations, investors did not need much help from Reagan’s policies. Current equity market valuations require investors to believe beyond all doubt that Trump’s policies can produce strong economic growth and overcome hefty economic and demographic headwinds. More bluntly, the risk-return profile of 1981 is the polar opposite to that of today.

You can read 720Global’s full piece here.

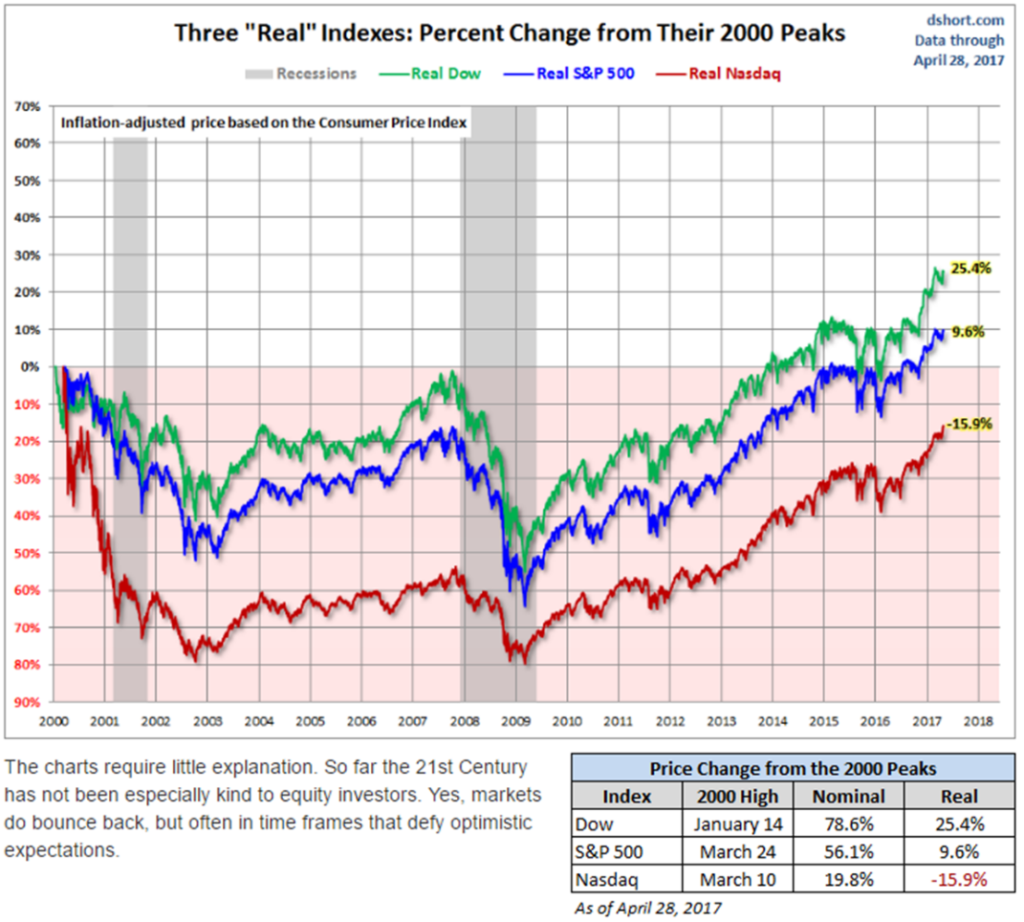

Like tech in 1999, scream as I did then, it was not enough to stop my 68-year-old client Roberta from transferring her account to a broker. Her new broker was putting her into as she told me then, “safe stocks.” By October 2002, her $1,000,000 turned into $500,000. I know this because her husband remained a client. After adjusting for inflation, it took her 15 years just to get back to even; assuming Roberta was able to stomach the ride and if she didn’t need some of that money for retirement.

It looked like this (inflation adjusted).

Source: dshort.com

Last Monday, the VIX broke below 10 to close at 9.77, the lowest level in more than a decade. There are only three other days the index has closed at lower levels, all of them in December 1993. Investors are complacent to risk. They shouldn’t be.

What can you do? Put some form of stop-loss risk management process in place. A little more than three years ago, I approached Ned Davis Research with an idea. I wanted to create a U.S. equity market indicator similar to Ned’s famous “Big Mo.” “Mo” is short for momentum. I love NDR’s work and I have been a happy client for years. Their services are not cheap, but it is an expense I am happy to pay.

We co-created something we call the Ned Davis Research CMG U.S. Large Cap Long/Flat Index. I previously used Big Mo and it’s a good indicator, but I now use the NDR CMG U.S. Large Cap Long/Flat Index to guide me in my long-term focused stock market exposure.

My point in mentioning this is that, despite my risk versus reward concerns, my defined equity market exposure (30% in moderate risk portfolios and 70% in aggressive risk portfolios) remains “risk on” and fully invested. Find something that works for you. Something that you can have full conviction in… then stick to the process. For your core portfolio allocations, you could diversify to several global ETF trading strategies. Broad diversification is key. On the other side of the next recession is the next great equity market opportunity. It is not today.

The impact of losses, in any given year, destroys the annualized “compounding” effect of money. It takes a return of 25% to overcome a loss of 20%. That’s doable and generally doesn’t take long to recover. It takes 100% to overcome a 50% loss and it takes 300% to overcome a 75% loss. Move forward carefully.

Roberta lost 50%. Others back then were ‘all in’ on tech stocks. They lost 75%. We’ve had one or two recessions per decade over the last 100 years. The last one was in 2008/09. Maybe this decade is the exception, but I doubt it. In recession, it is normal to experience a 40% decline in stocks.

“Those who do not remember the past are condemned to repeat it.”

― Benjamin Graham, The Intelligent Investor

Reagan had a great deal of wind at his back. Trump does not. Let’s get excited about tax cuts (after this past week that task may be tougher to achieve), but keep proper perspective about risk and reward. As the great Art Cashin says, “Stick with the drill – stay wary, alert and very, very nimble.”

When you click through below you’ll find a link to Trade Signals as well as a few charts I found interesting and I believe worthy of your review. Also, the NDR CMG U.S. Large Cap Long/Flat Index is posted on our website every Wednesday in Trade Signals. Thanks for reading. I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

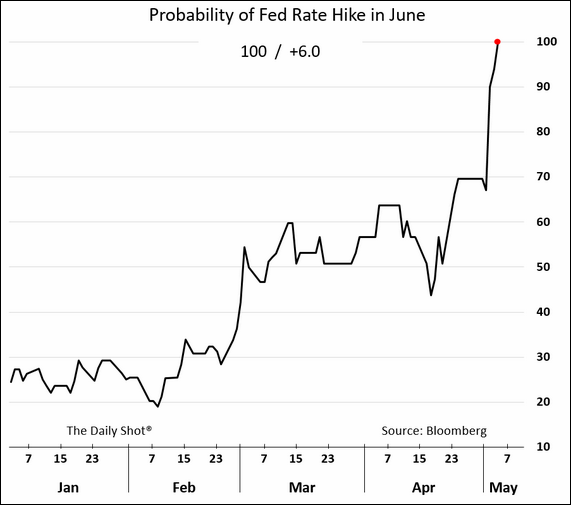

- Rate Hike Next Month is a Near Certainty

- U.S. Equity Market Capital Flows – To Large Cap Stocks (It Remains “Risk On”)

- Charts of the Week

- Trade Signals — Cyclical Equity Bull Market Remains Dominant Trend

- Personal Note

Rate Hike Next Month is a Near Certainty

From the WSJ – The Daily Shot

The dollar rose in response to what now looks like a near-certainty of a hike next month.

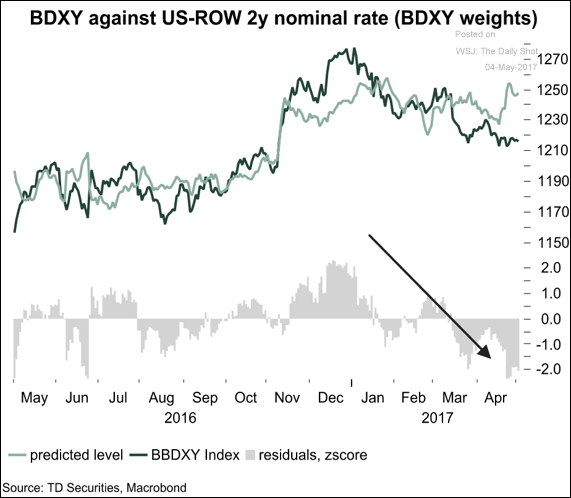

Based on the rising rate differentials with other countries, the dollar should be higher.

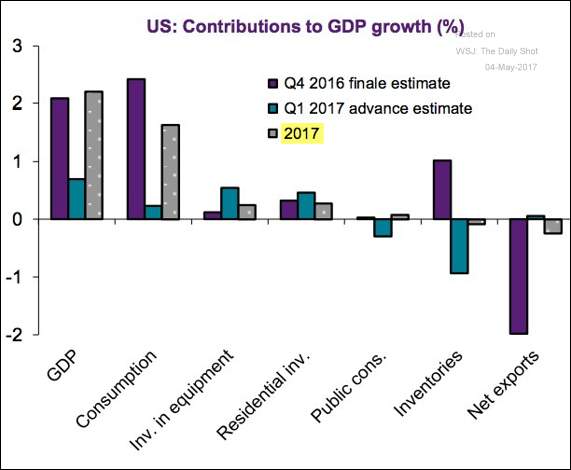

Despite a soft first quarter, economists continue to call for 2017 full-year GDP growth of just above 2%. Here is the breakdown from Natixis.

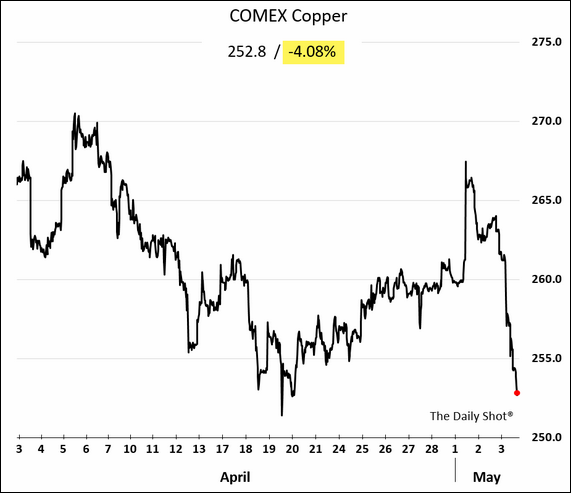

With the dollar on the rise and a possible China slowdown in the works, copper had the worst decline in 19 months.

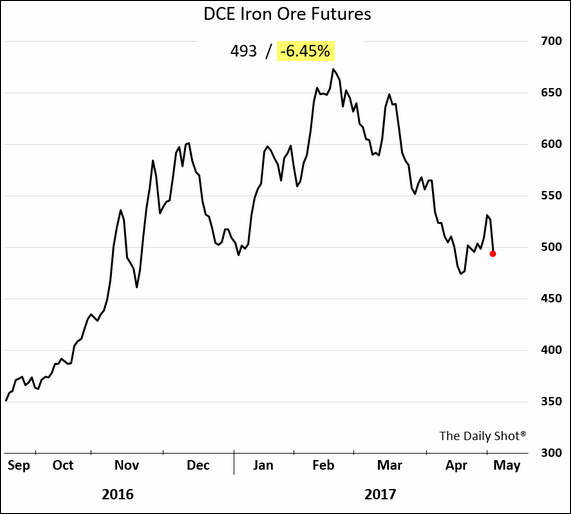

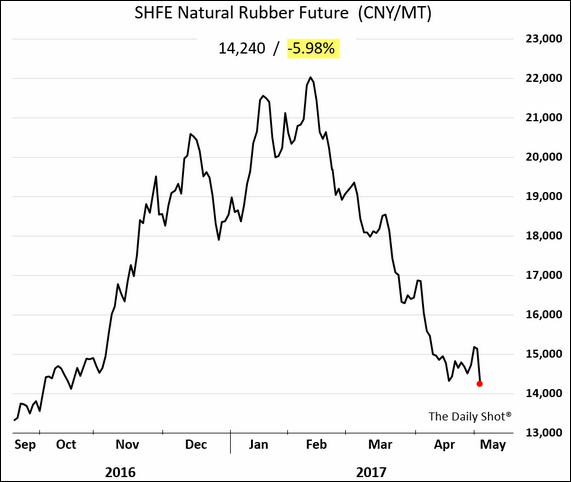

Iron ore was down nearly 6.5% on the day. And rubber futures tumbled 6%, continuing an unprecedented decline that started in February. Weak auto sales in the U.S. were not helpful.

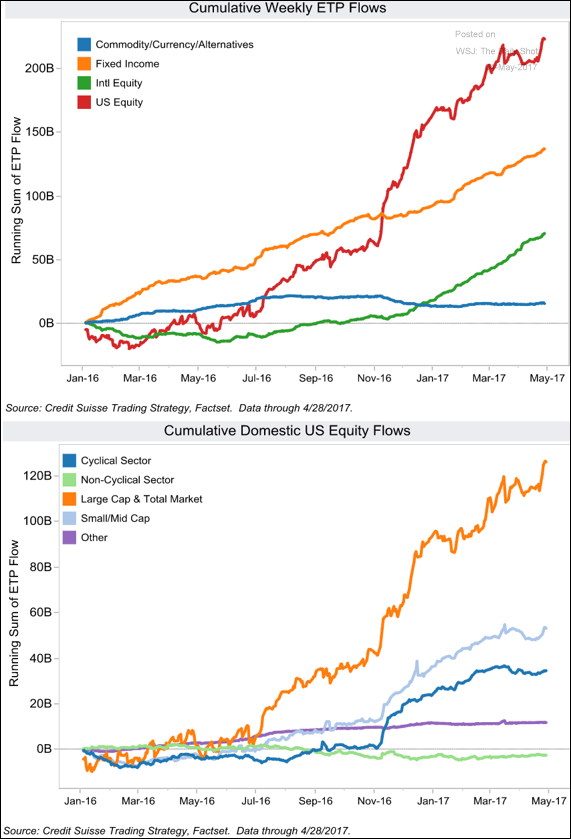

U.S. Equity Market Capital Flows — To Large Cap Stocks (It Remains “Risk On”)

Here is how to read the chart:

- Look at the flows into U.S. equities

- Most of those flows are going to large cap and total market equities

Charts of the Week

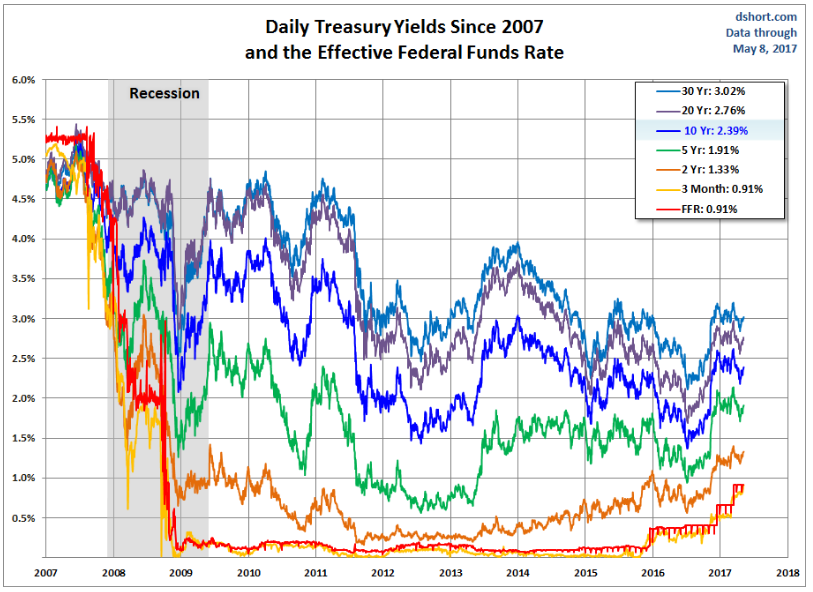

Chart 1 — A look at interest rates since 2007:

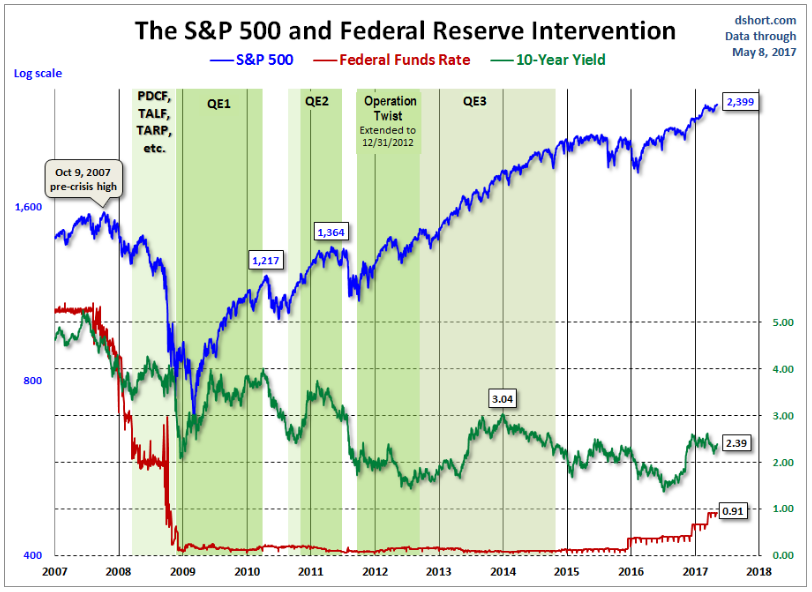

Chart 2 — The S&P 500 and Fed Intervention:

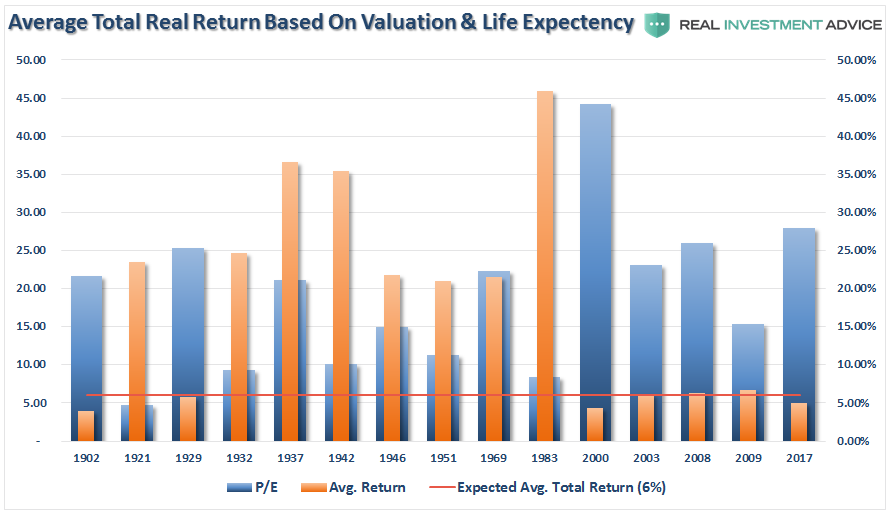

Chart 3 — Average Total Real Return Based on Valuation & Life Expectancy:

Here is how you read this next chart:

- Plotted are the P/E ratios in blue – think of that as your starting investment point

- The blue bar shows the average return from that point in time until end of life (based on life expectancy tables)

- Note that when valuations were high, the average return was low and when valuations were lower, the average returns were higher

- The horizontal red line shows when, ON AVERAGE, you failed to achieve 6%-annualized average total returns (much less 10%) from the starting age of 35 until death

Source: Advisor Perspectives

For long-term retirement income, it’s best to begin when your starting point is one where valuations are low and attractive… not high and expensive. Stay patient and risk minded until that opportunity presents.

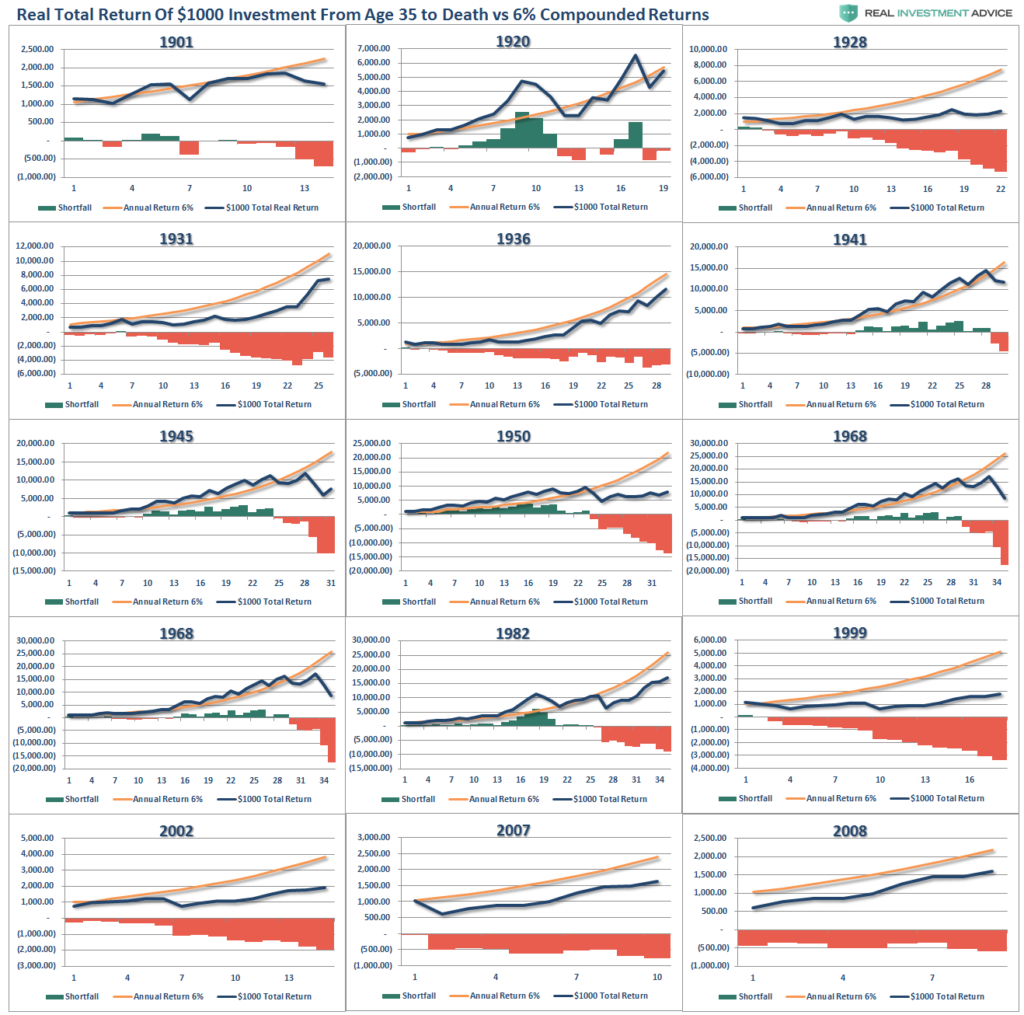

Chart 4 — Selected Retirement Start Dates (Examples Age 35 to Death):

Here is how to read the chart (following from Lance Roberts):

- As shown in the chart box below, I have taken a $1,000 investment for each period and assumed a real, total return holding period until death. No withdrawals were ever made. (Note: the periods from 1983 forward are still running as the investable life expectancy span is 40-plus years.)

- The gold sloping line is the “promise” of 6% annualized compound returns. The blue line is what actually happened with invested capital from 35 years of age until death, with the bar chart at the bottom of each period showing the surplus or shortfall of the goal of 6% annualized returns.

- In every single case, at the point of death, the invested capital is short of the promised goal.

- The difference between “close” to goal, and not, was the starting valuation level when investments were made.

- This is why, you must compensate for both starting period valuations and variability in returns when making future return assumptions.

- If you calculate your retirement plan using a 6% compounded growth rates (much less 8% or 10%) you WILL fall short of your goals.

Source – Advisors Perspectives: Lance Roberts is the Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report.”

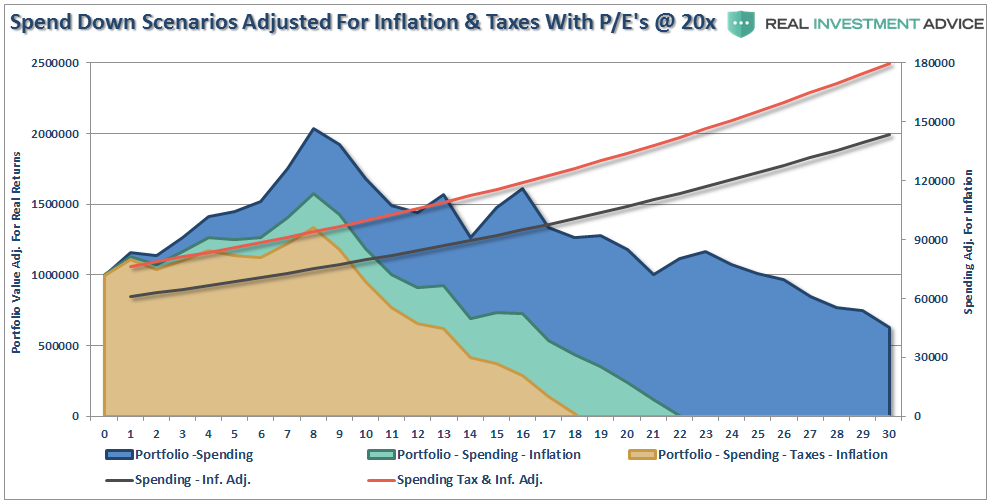

Chart 5 — The Spend Down Problem:

The reality is that retirees in general will need to live off their retirement savings. Charts 1 and 2 don’t take into account the need for portfolio income.

Here’s how you read this next chart:

- Grab a cold beer or two – The chart does not paint a pretty picture.

Lance concludes, “Time To Get Real”

“The analysis above reveals the important points that individuals should OF ANY AGE should consider:

- Expectations for future returns and withdrawal rates should be downwardly adjusted due to current valuation levels.

- The potential for front-loaded returns going forward is unlikely.

- Your personal life expectancy plays a huge role in future outcomes.

- The impact of taxation must be considered.

- Future inflation expectations must be carefully considered.

- Drawdowns from portfolios during declining market environments accelerates the principal bleed. Plans should be made during up years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

- The yield chase over the last eight years, and low interest rate environment, has created an extremely risky environment for investors. Caution is advised.

- Expectations for compounded annual rates of returns should be dismissed in lieu of variable rates of return based on current valuation levels.”

Lance’s hard advice to investors: “You cannot continue under-saving for your retirement hoping the stock market will make up the difference. This is the same trap that pension funds all across this country have fallen into and are now paying the price for. Importantly, chasing an arbitrary index that is 100% invested in the equity market requires you to take on far more risk that you most likely realize. Two massive bear markets over the last decade have left many individuals further away from retirement than they ever imagined.”

Folks, we investors need to save more. The importance of a great trainer is to get you doing the extra reps that are required to make you stronger. It is not fun to do. It’s hard to push ourselves. Some can do it, many can’t. The importance of a great advisor is much the same.

Picture yourself in the gym with your client. It might just be time to get up in their grill and push them to do a few extra reps. I was too nice to Roberta in 1999. It might have been better for me to scream. It’s time to scream.

Trade Signals — Cyclical Equity Bull Market Remains Dominant Trend

S&P 500 Index — 2,398 (5-10-2017)

Notable this week: The equity market, as measured by the Ned Davis Research CMG U.S. Large Cap Long/Flat Index, remains bullish. Don’t Fight the Fed or the Tape remains neutral. The Zweig Bond Model remains in a buy signal. The short-term gold trend indicator is in a sell signal. Investor sentiment is now Extremely Optimistic, which is S/T bearish for equities. Inflationary pressures are high but moderating. The overall weight of trend and breadth evidence supports a continuation of the cyclical equity bull market.

Click here for the charts and explanations.

Personal Note

The prom is this weekend for sons, Matt and Kyle. Brianna is coming in from NYC and we’ll have a fun time taking pictures and being together. Susan’s on the road to Connecticut to coach her soccer teams. My job is to get some good photos.

Happy Mother’s Day to you (your spouse and your mother). There is no more important person on the planet than mom. Through you comes life and love. May you always be held in the highest honor. Raise a glass and toast with me: To our wonderful mothers…

On Sunday, I’ll be toasting with red wine held high to my beautiful mother who I lost too many years ago. Mom, I feel you with me and I am grateful for you. And I’ll be toasting to my beautiful wife. And to my ex-wife as well. A good friend and wonderful mother to our children.

Travel ramps back up again next week. I’ll be traveling to Dallas on Wednesday for a two-day advisor due diligence meeting to advance the ball forward with a dozen advisors interested in the Mauldin Solutions Smart Core Strategy. The following week I’ll be in Orlando on May 22-25 for Mauldin’s annual Strategic Investment Conference. The speaker lineup is outstanding. I’m really looking forward to learning a great deal. I’ll share my high-level notes with you over the coming weeks.

Hug your mother! All the best to you and your wonderful family. Have a fun weekend!

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group