Growth in nonfarm payrolls rebounded in April, following a soft increase in March, consistent with a longer-term downward trend. The unemployment rate fell to 4.4%, the lowest level in over a decade. The results in recent months remain consistent with a labor market that is getting tighter. Average hourly earnings rose 0.3%, up just 2.5% from a year ago – a relatively soft pace considering the job market picture. This is consistent with the Fed gradually increasing short-term interest rates. However, might the Fed want to let things ride a lot longer?

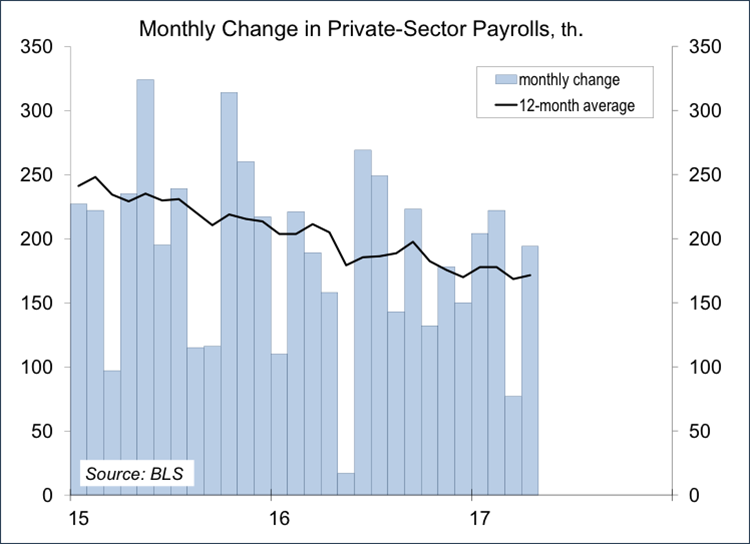

Nonfarm payrolls rose by 211,000 in the initial estimate for April, following a 79,000 gain in March (revised from +98,000). Needless to say, there is a fair amount of statistical noise from month to month (the monthly change in payrolls is reported accurate to ± 120,000) and seasonal adjustment is often challenging (we added 1.026 million jobs prior to seasonal adjustment in April, a little less than we saw a year earlier). Looking at payroll gains over a period of months smooths out a lot of the noise. Private-sector payrolls averaged a 164,000 gain in the last three months, compared to a 170,000 average for all of last year (vs. +213,000 in 2015 and +239,000 in 2014). The underlying trend in job growth has been slowing.

Weekly claims for unemployment benefits continue to trend at a very low level. Job destruction is limited. Anecdotal reports suggest that firms are increasingly having a harder time finding qualified workers, a consequence of tighter job conditions.

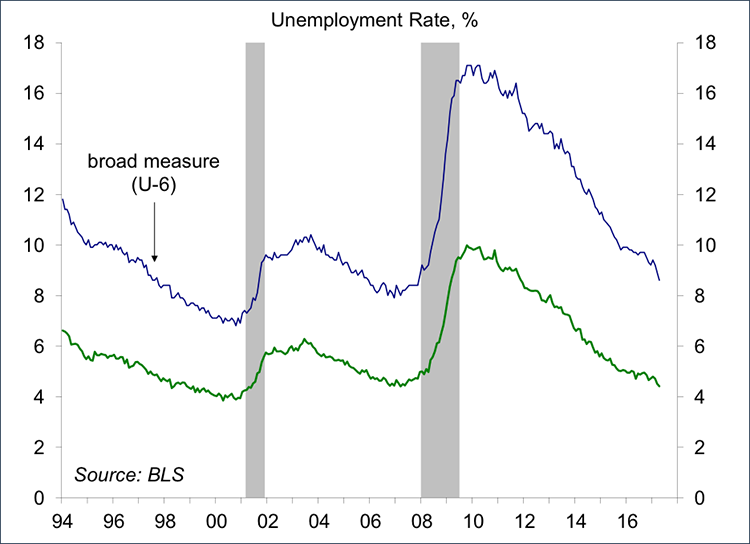

The unemployment rate fell further in April, now well below what Fed officials believe to be the natural rate. The broad U-6 measure fell even more sharply, reflecting a drop in involuntary part-time employment (those working part-time, but wanting full-time employment). Involuntary part-time employment rose sharply during the recession, but has actually declined since the Affordable Care Act went into effect.

While the job market has grown tighter, there is still a wide difference in the demand for skilled and unskilled labor. Wages for skilled workers should be picking up. There are couple of reasons that wage growth may be slower than in past periods of tight job conditions. One is that union membership is a lot lower than a few decades ago, suggesting less bargaining power for workers. The other is that there has been a consolidation of major firms, consistent with greater bargaining power for those employing workers. For the relatively unskilled workers, there is little bargaining power, and apparently, still a lot of slack remaining. Efforts could be made to educate those workers, but it’s typically unclear what kind of work to train people for. Training would best be handled by the firms, and can be encouraged through tax incentives (although reducing such deductions is expected to be a key issue in tax reform efforts).

How does this relate to the inflation outlook and monetary policy? The Fed’s thinking is that a tighter job market will lead to higher wage inflation, which will be passed through to higher consumer prices. That was the story of the inflation booms of the 1970s and early 1980s. However, firms may not be able to raise prices of the goods and services they produce. Higher wages should then lead to a more efficient use of labor, boosting productivity growth. As workers move up to better jobs, that leaves space for new entrants to come in and acquire work skills. This seemed to be the story of the late 1990s. The Federal Reserve, under Chair Greenspan, was willing to test the theory of the natural rate. Yet, the conclusion, for most Fed officials, is that policy needs to keep economic growth on a more even keel and prevent wage inflation from taking hold.

At this point, the analogy remains largely the same – the Fed is not hitting the brakes, but is taking its foot (gradually) off of the accelerator pedal. There are other arguments for normalizing policy, but the Fed should be willing to let this run.

© Raymond James

© Raymond James

Read more commentaries by Raymond James