1. US Economy Off to Slower Than Expected Start in the 1Q

2. Will Disappointing GDP Growth Head-Off a Fed Rate Hike?

3. The Fed/Central Banks’ $13 Trillion Gorilla in the Room

4. Unwinding Monster Balance Sheets Will be Difficult at Best

Overview

The US Federal Reserve, the European Central Bank and the Bank of Japan alone have over $13 trillion in quantitative easing assets on their balance sheets. The Fed recently hinted that it would like to start reducing its QE assets this year if possible. That has sparked an entirely new discussion on how the central banks could go about reducing their unprecedented QE asset holdings without sparking a new financial crisis.

This is a complicated issue and one that, if not handled properly, could be a disaster for the stock and bond markets in the years ahead. We’ll start today with a basic look at the problem, how it developed and some of the possible solutions.

Before we get into that, let’s take a look at last Friday’s very disappointing GDP report for the 1Q. In light of that weak report, some are asking if the Fed will hold off on raising interest rates again this year. I’ll give you my thoughts as we go along.

US Economy Off to Slower Than Expected Start in the 1Q

Americans say they feel more optimistic about the economy since President Trump was elected. But they certainly are not acting that way in terms of consumer spending, and that is shaping up to be a challenge for the Trump administration. The caution among consumers was particularly notable on big purchases like automobiles and durable goods.

Economic growth slowed in the first quarter to its slowest pace in three years as sluggish consumer spending offset impressive business investment. The Commerce Department reported on Friday that 1Q Gross Domestic rose only 0.7% (annual rate) in the first three months of this year. That was only one-third of the 2.1% pace in the 4Q of last year, and was well below the pre-report consensus of a 1.1% gain.

Some economists downplayed the weak showing in the 1Q noting that the Commerce Department frequently understates growth in the 1Q due to seasonal adjustments. They point out that growth in the first three months of each year has averaged only 1% since 2000, which is less than half the average for the other three quarters of the year over the same period.

Others warned that the disappointing GDP estimate for the 1Q is a sign of a real slowdown in the economy. They pointed to the fact that consumer spending, which accounts for apprx. 70% of GDP, rose an anemic 0.3% in the 1Q versus a better than expected jump of 3.5% in the 4Q. Others noted the very weak March employment report showing only 98,000 new jobs as compared to the monthly average of 180,000 for all of 2016.

Despite the latest disappointing report, most economists now expect the economy to pick up steam in the current quarter with GDP growth of 3.0% and 2.3% for all of 2017, according to a Bloomberg survey last week. That’s probably because Treasury officials said last week that President Trump’s plans to cut taxes and increase federal spending could boost the economy to 3% growth.

That assumes, of course, that Trump can get all or most of his tax cuts and spending plans through Congress. That’s a mighty big assumption if you ask me!

The bright side of the disappointing 1Q GDP report was the fact that business investment in new equipment and structures grew 9.4%. A turnaround in capital spending that began modestly in the second half of last year has picked up momentum now that the oil industry has rebounded and the global economy has improved.

Elsewhere, housing construction increased 13.7%, as limited home supplies have driven up prices and prompted developers to build units. The more favorable environment overseas bolstered exports, which grew 5.8% after declining sharply in the fourth quarter.

Friday’s GDP report was the first of three estimates the Commerce Department will issue. The second will come near the end of May and the final near the end of June.

Will Disappointing GDP Growth Head-Off a Fed Rate Hike?

The Fed’s policy committee is meeting today and tomorrow but there were already low expectations of a rate hike at this week’s meeting, even before Friday’s disappointing GDP report. Odds are much higher for a rate hike at the June 13-14 FOMC meeting when the Fed will issue new economic projections and Chair Yellen will hold a press conference afterward.

There is little doubt that the FOMC members will be watching the economic data closely between now and the June meeting. If we see some decent reports in the weeks just ahead, as most economists expect, then I would expect the FOMC to hike the Fed Funds rate by another 0.25% at the end of the June meeting.

The FOMC members no doubt noticed the pick-up in inflation in the 1Q GDP report last Friday. The Personal Consumption Expenditures Index (PCE), which is the Fed’s preferred inflation gauge, rose to a rate of 2.4%, the largest jump since 2011. So inflation is clearly above the Fed’s target for raising interest rates again.

You will recall that the FOMC raised its Fed Funds rate target range by 0.25% on March 15 to 0.75%-1.0%. That was the second increase in three months following the previous increase in December.

The Fed/Central Banks’ $13 Trillion Gorilla in the Room

The Federal Reserve, the European Central Bank (ECB) and to a lesser extent the Bank of Japan (BOJ) are under pressure to reduce their gigantic balance sheets, but doing so poses a risk of provoking another “taper tantrum” (market selloff) of serious proportions. Together, the Fed, the ECB and the BOJ are sitting on $13 trillion in assets purchased during years of so-called “quantitative easing.”

If major world banks in the US, Europe and Japan don’t properly coordinate and execute the unwinding of some $13 trillion in assets built up since 2008 -- risk assets including stocks and mortgage-backed securities – that could set off a major downward market correction (or worse) in the stock and bond markets. In the worst-case scenario, the global economic recovery, which is looking robust for the first time in a decade, might be at risk of a recession.

But first a little background. Following the financial crisis of 2008 that marked the start of the Great Recession, central banks around the world engaged in monetary policy efforts to stabilize their economies. Unorthodox policy tools such as quantitative easing (QE) allowed central banks to purchase riskier assets, including mortgage-backed securities (MBS) and other non-government debt.

Many experts believe that these asset purchases stabilized markets and bolstered the financial sector, keeping the recession from growing any deeper. The result, however, was that central bank balance sheets exploded!

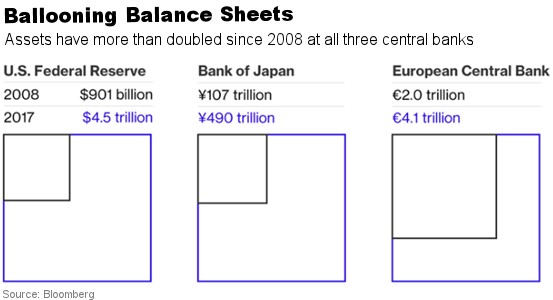

The Fed’s balance sheet grew from just under $1 trillion in assets in 2008 to $4.5 trillion in 2016. The ECB’s balance sheet more than doubled from E2.0 trillion to E4.1 trillion. The BOJ’s balance sheet more than quadrupled from Y107 trillion to Y490 trillion. Together, these assets are valued at apprx. $13 trillion.

The QE assets held by the Fed include US government bonds and mortgage-backed securities (MBS). In Japan and Europe, the central bank purchases included more than various government debt securities. These two central banks actively engaged in large direct purchases of corporate stock in order to prop up equity markets. This made the BOJ the largest equity holder of a number of Japanese companies indirectly via large positions in exchange traded funds (ETFs).

Unwinding Monster Balance Sheets Will be Difficult at Best

Economists and investors alike are stepping up their analysis of central bank balance sheet reduction after the minutes from the Fed’s policy meeting in March revealed that the Committee favors kicking off the process as soon as this year.

Unwinding, or “tapering,” these enormous positions is likely to spook the markets since a flood of supply is likely to keep demand at bay. Moreover, in some more illiquid markets, such as the MBS market, central banks became the single largest buyers of those assets in recent years.

In the US, for example, with the Fed no longer a buyer and under pressure to sell instead, it is unclear if there are enough buyers to take these assets off the Fed's hands at fair prices. The fear is that asset prices will collapse in these markets, creating a widespread panic.

If mortgage bonds fall in value, the other implication is that the interest rates associated with these assets will rise, thus putting upward pressure on mortgage rates in the market and putting a damper on the long but slow housing recovery.

And keep in mind that we are in totally uncharted waters. Quantitative easing has never been used in such enormous quantities by multiple central banks around the world. Everyone agrees that the “unwind” of these massive positions will be very tricky – if it ever happens at all (a subject for a separate discussion at another time).

Before central banks begin the unwind, they will gradually reduce the amount of securities they are currently purchasing on the open market. In December 2016, the ECB said that bond purchases would be extended until at least the end of 2017, putting the total amount of assets purchased under QE near 2.28 trillion euros.

Yet ECB officials have also said the monthly purchase amounts will be reduced gradually this year. At the April meeting, the ECB cut its monthly pace of purchases to 60 billion euros from 80 billion euros prior. Eventually, these purchases will stop altogether.

One strategy that would almost certainly calm fears is for the central banks to let certain bonds mature and refrain from buying new ones, rather than outright sales in the market. According to Bloomberg, “Fed officials’ current game plan is to start the balance sheet run-down with a phasing out of reinvestment in maturing securities. The central bank will have $426 billion of its Treasuries mature in 2018 and another $357 billion in 2019."

Yet even with phasing out purchases, the resilience of the financial markets is unclear since central banks have been enormous and consistent buyers of these QE securities since 2008. With regard to Japan in particular, it is unclear how equity markets around the world (not just in Japan) will react if the BOJ ceases asset purchases.

I wanted to introduce this potentially huge negative to you now since it has received very little coverage in the press after the Fed hinted at beginning its QE unwind this year if possible. Will it be a shock for the stock and bond markets? It depends on how monetary officials decide to proceed and how they communicate their intentions.

All I can tell you at this point is that the central banks in the US, Europe and Japan alone have accumulated apprx. $13 trillion in securities on their balance sheets. Nothing remotely this large has happened in world history.

No one on the planet knows for sure how, or if, these massive central bank balance sheets can be unwound. Only time will tell if this $13 trillion gorilla in the room will fade away quietly in the years to come, or if it will lead to a financial crisis that makes 2008 look tame. I’ll keep you posted.

All the best,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management