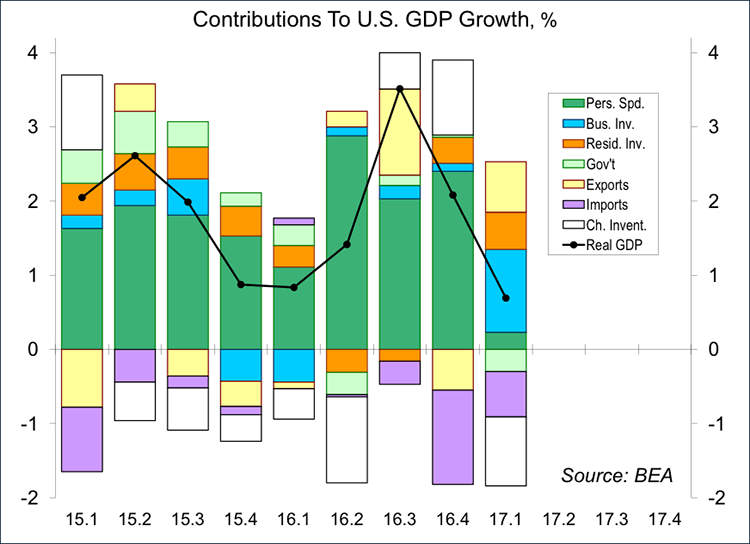

Real GDP rose at a 0.7% annual rate in the advance estimate for 1Q17, below the median forecast (+1.1%). Relatively speaking, that’s not a huge forecasting error. The headline growth figure will be revised and revised and revised over the next few months. The story behind the numbers was largely as anticipated, and that shouldn’t change much from here. However, the GDP data raise some important questions about the prospects for growth in the remainder of the year.

No surprise, consumer spending growth slowed sharply in the initial estimate for the first quarter – a 0.3% annual rate (vs. +3.5% in 4Q16). A slower pace of motor vehicle sales subtracted nearly a half of a percent from overall GDP. Personal income rose moderately in 1Q17, but inflation was higher, limiting consumer purchasing power. Mild temperatures reduced home heating expenditures, which are part of consumer spending. The near-term trend in gasoline prices has been relatively flat recently, which means that real income growth should pick up. More normal temperatures should lead to an unwinding of the dip in household energy consumption. The University of Michigan’s April consumer sentiment survey results noted that, over the last two months, evaluations of current personal finances posted the strongest improvement in 15 years.

Business fixed investment surged in the first quarter (a 9.4% annual rate, vs. +0.9% in 4Q16). Consumer optimism doesn’t always translate into higher consumer spending growth. However, business investment decisions are, by necessity, forward-looking. Business structures accounted for nearly half of the first quarter surge in nonresidential fixed investment. That could have been helped by mild weather. Spending on information-processing equipment picked up. Spending on industrial equipment was moderate. Inventory growth slowed sharply, subtracting 0.9 percentage point from GDP growth.

Can the strength in business investment continue beyond the first quarter? Businesses do not exist simply to sell to other businesses. The consumer is the end-point. Businesses will need to see a sustained increase in the demand for the goods and services they produce to keep expanding. A big part of the 1Q17 pickup in business investment has to do with the situation in Washington. Surveys show that households generally feel better about their personal financial situation regardless of their political affiliations. However, there is a sharp divide in expectations about the further. Naturally, one-party control has led to a sharp increase in optimism for Republicans and a decrease in optimism for Democrats. Most business owners are Republicans – hence, the increase in business confidence.

One might be led to conclude that an economist’s outlook, like that of any individual, is based on his or her political viewpoint, and in some cases that may be true. However, the broader conclusion is driven by arithmetic. The demographic story has become more accepted. The underlying trend in labor force growth is a lot slower than in previous decades and will slow even more in the years ahead. While GDP growth over the last several years has been viewed as subpar, it’s been beyond a sustainable pace. We know that because the job market has gotten tighter over the last several years.

Does that mean we can’t get to much stronger GDP growth? Not at all, but clearly, the main issues should be whether to increase (not decrease) immigration and what efforts can be made to boost productivity growth. The last time we had strong productivity growth was in the late 1990s, when new technologies (cell phones, networking equipment, the internet) came into play (assisted partly by a misallocation of capital).

Over the next couple of months, the economic data will be key. We’ll find out whether consumer spending growth will rebound and whether business investment will stay strong.

© Raymond James

© Raymond James

Read more commentaries by Raymond James