Poverty Going Extinct

The Great Middle

Measuring Relative Income

Crossing Classes

Lucky Days

Orlando and SIC

“We of the sinking middle class may sink without further struggles into the working class where we belong, and probably when we get there it will not be so dreadful as we feared; for, after all, we have nothing to lose.”

– George Orwell

“A strong, educated middle class is what made America the greatest country in the world.”

– Lincoln Chafee

As we continue our tour of the widespread angst afflicting investors large and small today, I want to ask a more fundamental question: Is the angst all in our heads?

The quick answer: No, it’s not. The economic challenges we face are real. Fear, or angst, is often a perfectly reasonable response. I’ve said that, with one exception, we can muddle through the coming crises. But “we” doesn’t mean every single one of us. The nation will survive the next recession, but some of its citizens may not, at least not with the same financial security that they currently enjoy and expect. The coming pension crisis will put quite a dent in expectations. Economic strain can lead directly to sickness, disability, and sometimes suicide or fatal illness. It happens. I don’t want to minimize that risk.

It’s precisely the risk that we will find ourselves among those who can’t muddle through that creates so much angst. Worse, we know the risks aren’t randomly distributed. We have classes of Protected and Unprotected citizens, to use Peggy Noonan’s terms. But even the Protected are afraid they may slide down the scale into economic oblivion.

Actually, they probably wouldn’t slide much farther than the middle class – but they may find the middle class hollowed out when they get there. The middle class is a fairly new development in economics. Up until the last century or two, most societies had a tiny wealthy elite and great masses of common laborers. We now regard having this group in the middle, not wealthy but with their own assets and spending power, as a great achievement. We don’t want to lose it, but some people fear we will.

If you delve into the economic and social-psychological literature, and if you can put up with the academic language that does its best to obscure what’s actually being said, you will find that there is a general consensus around the idea that having a lot of money does not make us happy, once our basic needs are fulfilled. There is, however, some research – and it’s controversial – which indicates that relative income is important. A majority of respondents would rather have more relative income than more absolute income, especially if they are relatively lower-income than everybody else. On the surface of it, that proposition doesn’t make sense to many people; but we’re dealing with human emotions and feelings, which often don’t make sense. We just seem to be wired to want to keep up with – or do better than – the Joneses, and now many people suspect they are doing worse. (Remember, these studies measure only the average propensity, not what you and I might as individuals think or believe or feel.)

So, given the uncertainty of the times (and the data I will present here), there is reason for concern that the middle class is really under pressure. It’s not just in their heads; it’s an everyday, real-world situation.

With that in mind, we’ll look at some new income data and see if it can help us control our angst.

All of this angst – no matter your current circumstances – makes it more difficult to make decisions now than it is in more confident times. Those of us in the publishing business, as well as in the money management business, know that it is in times of high anxiety that is the most difficult to get our clients and readers to actually respond. The best time to elicit a response is in a boom period, and the next best time is, ironically, just after a bust, when people are ready to figure out what to do. I say ironically, because it is precisely when we have an economic and political situation like the one we have today, when there is actually time to make proactive decisions, that it appears to be the most psychologically difficult to do so. We procrastinate; we become like Wilkins Micawber from Charles Dickens’ novel David Copperfield, who was famously noted for saying repeatedly, “Something will turn up.”

Let me suggest that now is the time you should be thinking hardest about taking action to have your house in order when we hit the next rough patch. Next week I’m going to start writing about what I am calling “The Great Reset.” I think we are approaching that moment when the two greatest bubbles in human history – sovereign debt and government promises (which are conflated in many people’s minds) – will burst, and politicians and central banks will be forced to take actions that are unthinkable today.

One way you can help yourself is by taking one of the few remaining spots at my

Strategic Investment Conference, May 22–25 in Orlando. I have assembled an all-star cast of some of the finest analysts, economists, and geopolitical thinkers for a 2½ day deep dive into how the world will change over the coming 1–5–10 years. My full intention is for you to be able to walk away with the tools to create or enhance your own game plan. But if you can’t make it to the conference, we will soon be offering a full set of the speeches. They won’t give you the valuable interactions you would have at the conference with the speakers and other attendees; but that said, the recordings are the next best thing.

And now, having urged you to make sure you have the strategies to “batten down the hatches,” let’s see why the middle class is under so much pressure.

Poverty Going Extinct

We’ll begin with some good news. Despite all our problems, on a global basis the number of people trapped in extreme poverty has plummeted this century. That trend doesn’t mean everyone everywhere is living comfortably. Many millions still endure terrible conditions. But their number is shrinking.

The reason for the improvement, I believe, is that technology and free trade brought economic growth to formerly stagnant economies. Yes, corruption and inefficiency diverted much of the growth into the wrong hands, but there has still been a general increase in living standards and incomes.

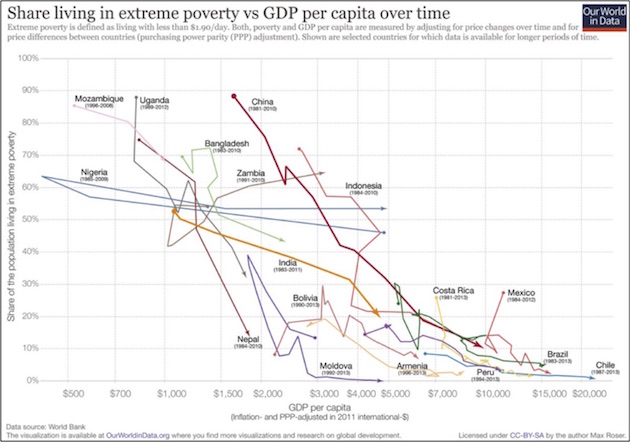

We can see this decline in extreme poverty in the following chart from Max Rosen’s Our World in Data site. The chart plots the share of a country’s population living in extreme poverty vs. growth in per capita GDP. “Extreme poverty” means living on less than the equivalent of $1.90 per day. The lines illustrate the change in that balance over time. You can see a nifty animated version of the chart here.

What we see here is that many countries began in the top left quadrant or close to it, with a high percentage of the population in extreme poverty and with low GDP per capita. Over time, countries slide to the lower right, meaning higher per capita GDP and a lower percentage of the population in extreme poverty.

So, it appears that a general increase in national income correlates with fewer people living in dire poverty. Correlation isn’t causation, of course, nor does this mean that all is well in these countries now. But there is at least an association between economic growth and reduced poverty. The rising tide seems to lift most boats.

That’s great news – something we should all celebrate. We in the developed world can’t truly comprehend what extreme poverty is like. $1.90 a day? Americans spend more than that on coffee and junk food. I don’t know how people buy food, shelter, and everything else with such a small amount.

I suppose extreme poverty seems normal if you have known nothing else. But increasingly, we all do know (or think we know) how the other half lives. That’s part of our problem, as we’ll see below.

My point here is simple: If you are reading this letter, you are already far ahead of most human beings in terms of wealth, health, education, leisure time, and more. Gratefully recognizing that fact helps with the angst. It’s not the complete answer by any means, but it helps.

The Great Middle

Now let’s consider some related data from Europe and the US, courtesy of Pew Research Center. In this case, we’ll look at the middle class.

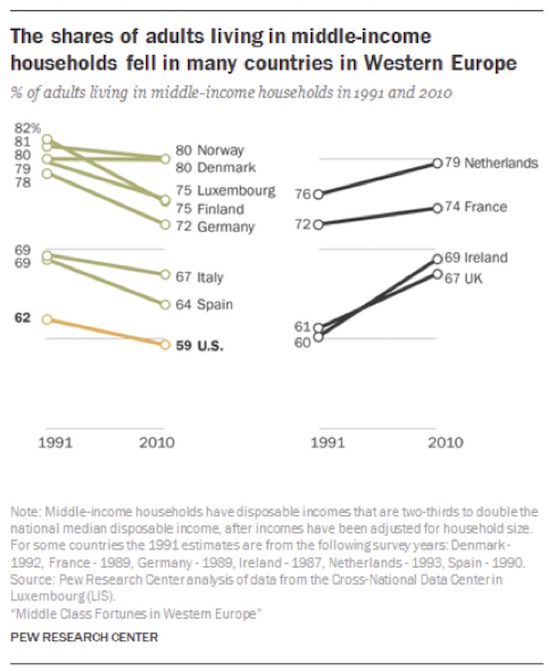

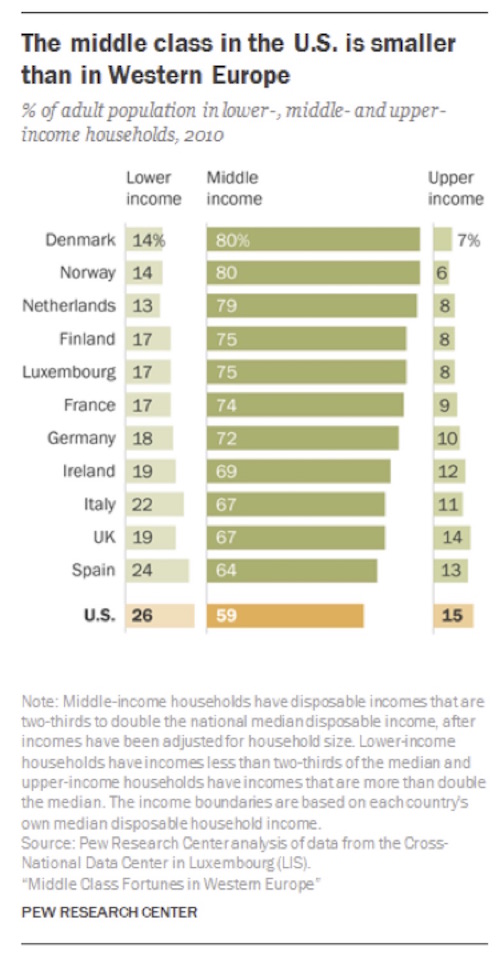

First question: What’s “middle class?” Pew defines it as adults living in households with disposable incomes ranging from two-thirds to twice the national median disposable income. In the US, that means a 2010 after-tax income between $35,294 and $105,881.

Pew found that from 1991 through 2010, the percentage of adults living in middle-class households in the US shrank from 62% to 59%.

More significantly, perhaps, the US has the smallest percentage of middle class adults of any of the advanced economies Pew studied. Notably, during this period the middle class expanded in the UK, Ireland, France, and the Netherlands.

The percentages in themselves don’t tell us much. A shrinking middle class might be good if it means that more people are moving into the upper strata. Of course, it’s not possible for everyone to be above the median. That’s what median means: half above, half below. But income-distribution curves can have different shapes. In 2010, 59% of US adults were in the middle class, 15% above it, and 26% below it. Not exactly the shape of curve you want to see.

(Incidentally, I know the word class isn’t exactly right in this context. We are talking strictly about income. Usually, class considers other identifiers, like education. Pew uses middle income and middle class interchangeably but acknowledges the terms can be ambiguous.)

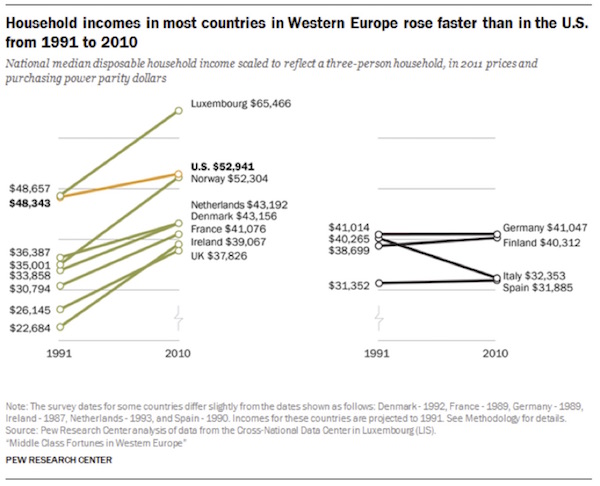

Now let’s look at a different data point: the median income that lies at the center of these distinctions. The chart below shows how the median changed from the beginning to the end of the study period. US median household income rose from an inflation-adjusted $48,343 in 1991 to $52,941 in 2010. That’s a 9.5% increase over 19 years. That’s pretty feeble, in my opinion, and indeed lower than in some European countries. Luxembourg’s median household income jumped almost 35% in the same period. But the trend was flat or even negative in Germany, Finland, Italy, and Spain. (More on US median income below.)

Another thing that strikes me here is the wide variation within Europe. In 2010, median income for a three-person household ranged from $31,885 in Spain to $65,466 in Luxembourg. You could say Luxembourg is small and unique; but Norway isn’t small, and at $52,304 its median household income is 64% higher than Spain’s. I suspect these differences have a lot to do with the European Union’s present travails – and its rising populist movements.

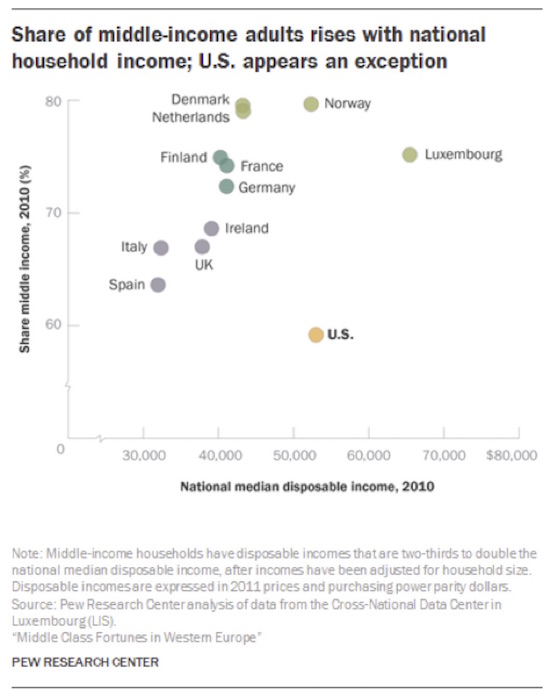

The US stands out in another way, which Pew illustrates with this scatterplot:

Comparing the size of each country’s middle class with its median income, we see that the US is a distinct outlier. Our middle class is smaller, but its income is higher than those of the middle classes in the other countries studied. Pew attributes the difference to another factor: The US has larger portions of its population in both the lower-income and upper-income categories than any of the other countries studied.

I don’t think these figures are a great mystery on the upper end. European countries have higher taxes, so they have relatively fewer wealthy people. Ditto on the lower-income end: It’s harder to be poor when your government has generous welfare programs. But these differences at the top and bottom ends are greater than I would have expected.

Measuring Relative Income

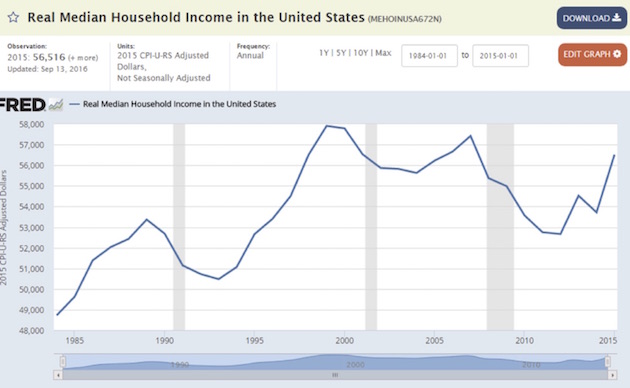

If the average person in this country feels as though they are going nowhere fast, there is a real reason for it. The next chart, from the St. Louis Federal Reserve FRED database, shows that median income in the US is actually down over the last 17 years and is only 3% higher now than it was 30 years ago. Those are inflation-adjusted numbers. But the reality is that, for the average person, inflation has been much higher than the average of 2% per year over that time, because the things that the average person actually buys, like housing and education and healthcare and all the other necessities of life, are rising at a much faster rate than 2%. So this chart reflects the fact that life has gotten much more difficult for average Americans. If people’s income hasn’t grown beyond what it was 30 years ago, they struggle just to make ends meet and to maintain the lifestyle they had. Can we say angst?

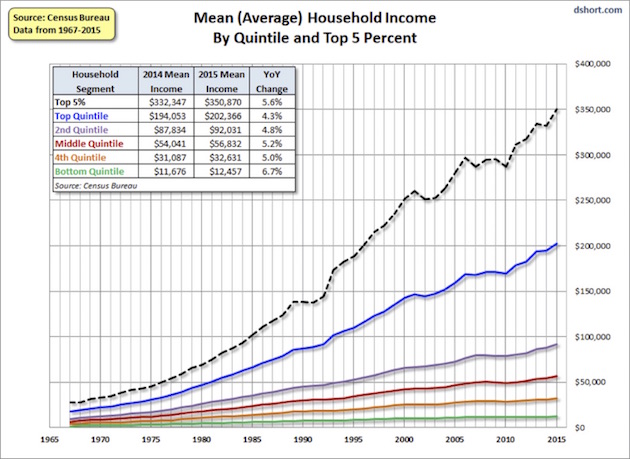

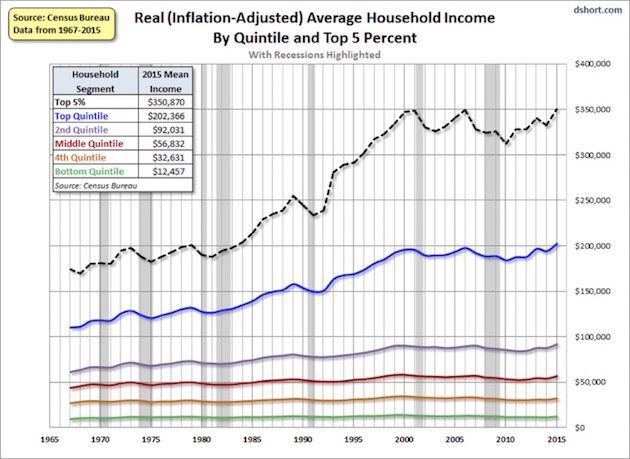

The Census Bureau updates its income figures about once a year, and the last real update we had was last fall, taking us through 2015. Doug Short did an analysis of those numbers, and I am going to borrow three graphs from him. (He does fabulous charts!)

He breaks the country into quintiles, calculates the average household income for each quintile, and then also shows the top 5%. Notice that the average income for the top 5% is $350,000. We will come back to that figure in a moment.

It looks like everybody’s income is rising, especially those in the top 20% and 5%. But if we inflation-adjust those numbers, the illusion of growth goes away. What we see is that there has been almost no movement for the bottom 60%, while the middle quintile has grown somewhat, and – this won’t surprise anyone – the top 20% and 5% have done very well.

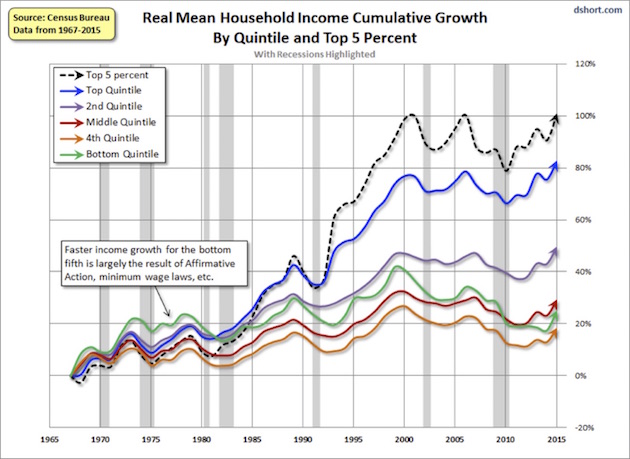

The next chart shows what that growth looks like in percentage terms. We find that the bottom quintile saw their income grow by only 25% over the last 49 years, less than ½% per year. Interestingly, the fourth quintile grew even less than the bottom one, at around 19%, mainly because of government programs that supported those in the lowest 20%.

But what about the 1%, I hear you asking? Investopedia conveniently gives us that answer:

To be certified as a one-percenter, you needed to bring home an adjusted gross income of $465,626 more for the 2014 tax year, according to data from the IRS. The Washington Center for Equitable Growth put the average household income for this group at $1,260,508 for 2014.

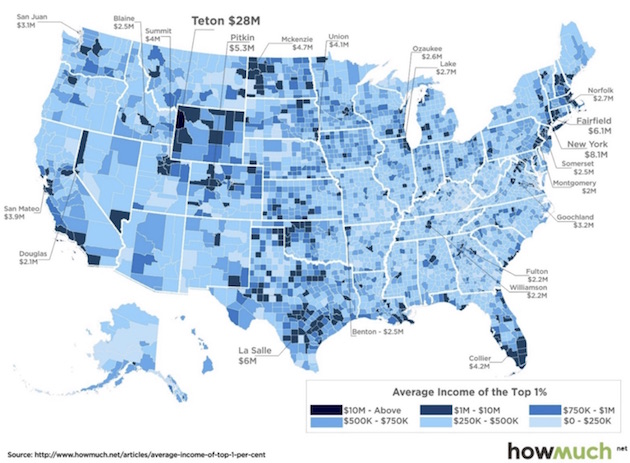

But as the saying goes, your mileage may vary. It turns out there is quite a lot of variation among counties around the US as to what it takes to qualify for the top 1%. To make the grade in New York, you will need about $8 million in annual income. But that amount wouldn’t help you very much in Teton County, Wyoming (we’re talking Jackson Hole here), where you will need a tidy $28 million per year to make it into the top 1%. On the other hand, there are many counties around the country where the top 1% take in less than $200,000; and in Quitman County, Georgia, you only need $127,000 a year to be elite. I found it odd that in LaSalle County, Texas, you had to make $6 million to land in the top 1%. Now, that county has only about 6000 residents, and the median income is quite low. It turns out there are many rural counties in America with a similar pattern, either because some of their residents “fly in” or because there is oil fracking involved. If you are interested in that phenomenon, you can check out

this story in the

Washington Post.

Crossing Classes

My gut feeling as I travel around the country and read a lot, is that more people are worried about staying where they are or not sliding down than are trying to figure out how to get up to the next level. It’s just the times we are living in. We are also seeing fewer new companies being started than ever before. I don’t think we can attribute that fact to generational differences – there is just a great deal of nervousness about being entrepreneurial.

The possibility that we might slide down the class scale is the source of much angst. Upper-income people worry they will decline to mere upper-middle-class status, while the middle class doesn’t want to join the ranks of the lower class.

It’s not so much that those upper-income people are worried about being middle class, it’s that they have created expenses and lifestyles around a certain level of income. If that income falls, they will have to change the lifestyle they have become used to. That is remarkably difficult for many of us to do. Our sense of self-esteem and emotional well-being are, it seems, tied into our lifestyle.

A little personal revelation: I am no exception. I could certainly live a less expensive lifestyle. To some extent, I simply tell myself to enjoy life as I find it and work hard to try to maintain my businesses and to grow them if possible. That is more difficult than you might imagine when the very foundations of the industries that I choose to work in seem to be shifting underneath my feet in directions I can’t control. You just have to adapt. I have had to downshift my lifestyle on three occasions in my life; and while that’s not fun, I seem to adjust. Maybe there’s a little bit of Wilkins Micawber in me. In those lean periods, something always does seem to turn up. Then again, my great goal in life is not to have to make that hard adjustment yet one more time. In a real sense, I’ve created my own personal angst. It’s kind of silly, really. But it does tend to drive me. I’m sure the psychologists among you can have a field day with that.

Whether your worries are groundless or real, those fears are greater if you know you’re at the lower end of your peer group. The wealthiest .001% don’t have to worry – they’ll be fine in just about any scenario. But people in the 85–95th percentiles are in danger of taking a fall in the next big market and economic upheaval.

And of course, the lower middle in the 25–50th percentiles are very vulnerable to downward mobility. A New York Times report on the Pew study starts with one of their usual personal vignettes:

Mike McCabe’s neighbors in rural Gillespie, Ill., consider him lucky. After being out of work for a year, he landed a job in January making cardboard boxes at a nearby Georgia-Pacific plant for $19.60 an hour.

He would agree with them, were it not for the fact that his previous job in a steel mill near St. Louis paid $28 an hour. “I’ve had to rethink my whole life to make ends meet on what I’m now making,” Mr. McCabe said. “The middle class is struggling for sure, and almost anybody in my position will tell you that.”

That short passage actually says a lot about angst in America. Let’s unpack it.

Your neighbors will consider you lucky if you stay unemployed for a year and then find work for 30% less money than you made before. Maybe so, but you’ll still be hurting. The statistics suggest that people in situations like this probably had little savings and burned through whatever they had while unemployed. They may have gone deeply into debt to survive.

“I’ve had to rethink my whole life to make ends meet on what I’m now making.”

That’s haunting because I think we can all imagine ourselves in that spot, no matter where we are now. What if you had to (a) go a full year with no income and (b) return to work at only 70% of your former earnings? Would you have to adjust your lifestyle? I sure would. My dad taught me that you do what you have to do, but fear of having to do it is the source of much of our angst.

At the same time, if his neighbors consider this guy to be “lucky,” there must be many others in far worse straits. Remember the Maine guide I talked about last summer, who lost his job due to a plant closure and is now having to work through his retirement savings, 10 years before he turns 65? That kind of puts my angst and maybe the angst of most of my readers in real perspective.

Lucky Days

Part of our angst is that we feel captive to forces beyond our control. We suspect the bad luck that might push us downscale is more prevalent than the good luck that might propel us higher.

I think we also worry that it’s not luck that will hurt us but rather our own weaknesses. My friend Barry Ritholtz made an interesting point in his Bloomberg column recently.

A surprising thing I learned from interviewing some of the most successful people in finance is how frequently they credit good luck. Indeed, in most of the almost 150 Masters in Business interviews I have done, our guests mention – unprompted by me – the crucial role of serendipity. This isn’t false modesty or humility, but rather, an honest acknowledgment that chance can make a significant difference in people’s lives.

Note that the role of chance doesn’t imply successful people don’t need to be educated, smart and diligent. Rather, it recognizes that lots of insightful, intelligent, hard-working people may not achieve the same level of success as other folks with the exact same qualities – and that those who are more successful may have had lucky breaks that others didn’t get.

I think part of this is ego. It feels good to blame bad news on things we can’t control while taking full credit for whatever successes we have. But there’s more to it. Luck does indeed cut both ways.

In the US we have a cultural imprint that I think traces back to our Puritan origins. It tells us that everyone gets what they deserve. If you’re wealthy, you must be smart and hardworking. Conversely, the poor are poor because they’re lazy and make bad choices.

Both of those things are true in many cases, but not always. I have known many brilliant, hardworking people who have struggled financially. I’ve also known some very wealthy people who were, shall we say, less than genius-level intellects and whose work habits were suspect. The fact that there are exceptions proves that the rule isn’t absolute.

Nonetheless, our Puritanical attitude is widespread and is even built into our laws. If your net worth is above a certain threshold, you’re an “accredited investor” and presumed to be sophisticated enough not to need certain consumer protections and disclosures. And if your net worth falls below a certain threshold, you are “protected” from investments that might offer higher returns to those who are better off than you are, presumably because your current economic circumstances suggest you wouldn’t understand the investments, regardless of your education and experience. Both of those assumptions by the government are nonsense.

Whatever our income or class, we all face challenges over which we have some influence, yet we may find ourselves subject to a fate that we can’t control. The challenge that we have today is to recognize that the political, economic, and investment forces that we have become used to dealing with over the last 70 years, through all their ups and downs, are getting ready to shift more radically than we have yet seen or can even imagine. We will have to think more deeply and creatively than ever about how to prepare for the changes – the transformation – coming to our lives.

Orlando and SIC

If I haven’t missed putting anything else on my calendar, my next trip will be to the Strategic Investment Conference, May 22–25 in Orlando. Then on the 26th Shane and I fly up to Washington DC to be with Neil Howe and bride Gisela at their wedding.

I know I mentioned the Strategic Investment Conference at the beginning of the letter, but let me offer you some new reasons why you should attend. My friend Marc Faber has now agreed to speak and serve on a few panels. The last day will be a panel composed of George Friedman, Mark Yusko, Neil Howe, and Matt Ridley. George needs no introduction to my readers. Mark Yusko is a renowned investor who is the founder and chief investment officer of Morgan Creek Capital Management. Neil Howe wrote The Fourth Turning, which was the driver for Steve Bannon’s documentary, Generation Zero. Neil will be telling us what the next 10 years are likely to hold as we enter the latter half of this Fourth Turning). Matt Ridley is the brilliant Libertarian thinker/philosopher and prolific author who wrote The Rational Optimist and The Evolution of Everything, which I think is one of the best books of the last five years.

I’m going to moderate the panel and engage them in a discussion about how the next 10 years will unfold. I can’t imagine anything more exciting. Well, except the rest of the conference, where Ian Bremmer and Pippa and Harald Malmgren will not only make their own presentations but then sit down with George Friedman in a no-holds-barred panel on current geopolitics. Lacy Hunt, David Rosenberg, Raoul Pal, Grant Williams, Martin Barnes, some of the most noted cutting-edge biotech scientists, and an energy panel with two billionaires who actually know how to pull oil out of the ground and tap energy from the sun. They are not just investors; they have built their own “mini-empires” from scratch and have an extraordinary view on the future of energy and natural resources. And the list goes on and on and on.

You really do want to figure out how to get Orlando May 22–25, if you haven’t already made arrangements. This is where you can get the information you need to make the course adjustments that will be required for The Great Reset. Make sure your spot is reserved.

Now, I mentioned that next week I’m going to write about The Great Reset and talk specifically about how I think we need to adjust our core portfolios. But in the meantime, as part of the launch of my new portfolio management company, I will be hosting, on May 17 at my home, a chili and prime dinner for independent brokers and advisers, where we will share with you the specifics of how we are going about changing the way you manage the core of your portfolio. As I keep saying, the key is to diversify trading strategies, not just asset classes. Technology has allowed us to do some marvelous new things, and portfolio diversification that smoothes out the ride is one of them. One of my goals is to be able to help brokers and advisers get their clients through the storms that we all know are coming as the world struggles to figure out how to deal with the massive amounts of debt and government obligations that are building up. Maybe not this year, but at some point there has to be a Great Reset, and you need to be able to get your clients through it. If you’re interested in attending to learn more about what we’re doing, drop a note to me at [email protected]. Give me your name and your firm, and we’ll get back to you ASAP.

I actually played nine holes while in Sonoma, and I only lost two balls! And I reminded myself that I need to get out more and relax. It was just good for the soul. Shane and I went to a charity event last night, and after the requisite live auction and money raising, we settled back to listen to some badass Texas blues the way the good Lord intended them to be played. Matt Tedder and Paul Harrington teased more sound from a guitar and harmonica than I have ever heard before. There is a reason why many think Paul Harrington is the best harmonica player in Texas. You probably don’t recognize the name, but you have heard him play on a lot of famous musicians’ recordings. If you want to have a fun evening, start with this link and then just start clicking on more links and Google the names that come up.

And with that I will hit the send button. You have a great week, and if Texas blues isn’t your thing, then spend some time with your own favorite music. It’s good for the soul.

Your wishing I could play the harmonica analyst,

John Mauldin

[email protected]

© Mauldin Economics

www.mauldineconomics.com

© Mauldin Economics

Read more commentaries by Mauldin Economics