Consumer spending accounts for 69% of Gross Domestic Product. Last week, the data on the household sector were mixed. The Conference Board’s Consumer Confidence Index surged to a 16-year high. Meanwhile, inflation-adjusted consumer spending has been tracking at below a 1% annual.

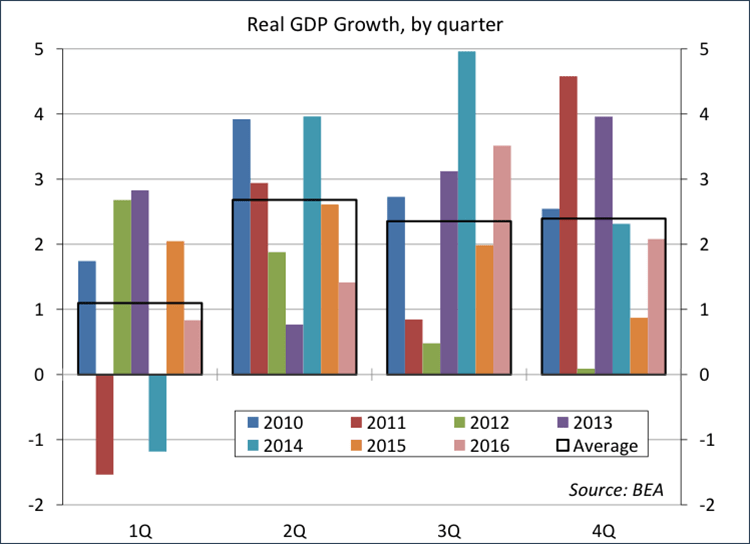

The Bureau of Economic Analysis reports its advance estimate of first quarter economic growth on Friday. In recent years, the National Income and Product Accounts have exhibited what’s called “residual seasonality” in 1Q growth. That is, first quarter growth has tended to be below that of the rest of the year. Investors may be willing to dismiss a soft first quarter. There are other reasons to be skeptical of soft 1Q data, but the ongoing difference between various sentiment survey results and the hard economic data add to the view that labor market constraints will limit the pace of growth in the quarters ahead.

There are regular seasonal patterns in the economy. The holiday shopping season, the school year, and the summer travel season are the most notable examples. Most economic data are seasonally adjusted. Since the Great Recession, on average, 1Q GDP growth (+1.1%) has been less than half of the 2Q-4Q pace (+2.5%). It’s possible that the severity of the recession generated a permanent change in the seasonal pattern, but if so, the government’s seasonal adjustment will adapt over time – and we may find that this residual seasonality disappears in future revisions to the national accounts.

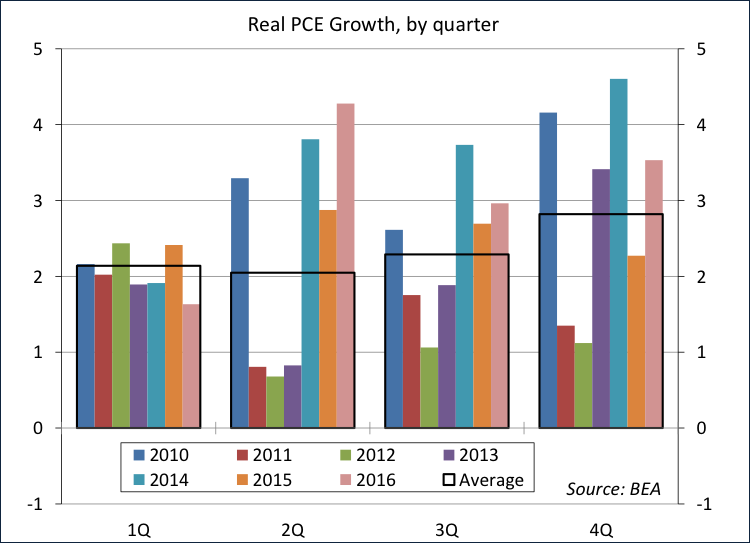

The advance estimate of 1Q17 GDP growth is expected to be held down by a sluggish pace of consumer spending growth. Consumer spending accounts for 69% of GDP. Interestingly, there is no evidence of residual seasonality in first quarter consumer spending growth (although fourth quarter figures have tended to be above the average of the rest of the year).

Still, there are other reasons to take soft 1Q17 consumer spending numbers in stride. Notably, at a 3.5% annual rate, 4Q16 consumer spending growth was strong and it’s not unusual to see a strong quarter followed by a soft quarter. Job and wage growth should continue to provide support for consumer spending growth in the second quarter.

Consumer and business attitude surveys have improved sharply since the November election. By themselves, consumer confidence figures generally reflect the strength of the overall economy. They fall in recessions and rise in recoveries. However, consumers don’t spend confidence. Spending is largely a function of income growth, but it also depends partly on wealth and the ability to borrow. Inflation-adjusted income should pick up. Consumer credit has begun to tighten, not terribly, but that will bear watching in the months ahead.

In contrast to the household sector, business sentiment plays a significant part in capital spending. Orders and shipments of nondefense capital goods began to pick up last summer, partly reflecting a bottoming out in energy extraction and some improvement in the global economy – and they picked up further following the November election. However, business sentiment may fall back. Washington’s inability to advance the Trump agenda, especially on tax reform, may be a factor. However, to remain optimistic, firms must eventually see increased demand for the goods and services they produce.

For economists, the divergence we’re seeing between the soft and hard data isn’t unusual. The soft data are useful, but you wouldn’t want to bet the ranch on them. The hard data also have limitations (statistical noise, sampling uncertainty, difficulties in the seasonal adjustment), which is one reason to look to the anecdotal information. Note that you can tie yourself in knots relying on the word-of-mouth assessments. In practice, look at everything (especially if you’re a Fed official).

The hard data / soft data divide points back to the key underlying story. That is, there are limits in the labor market which will restrain economic growth in the quarters and years ahead. Unless we see a sharp rise in productivity growth, slower labor force growth means slower economic growth. That’s not necessarily bad, but you might want to curb your enthusiasm.

© Raymond James

© Raymond James

Read more commentaries by Raymond James