Summary

- The Trump “reflation trade” is being undermined by the failure of the new administration to implement planned legislation, specifically the Affordable Care Act (the ACA, also known as Obamacare), corporate and personal tax cuts and the border adjustment tax.

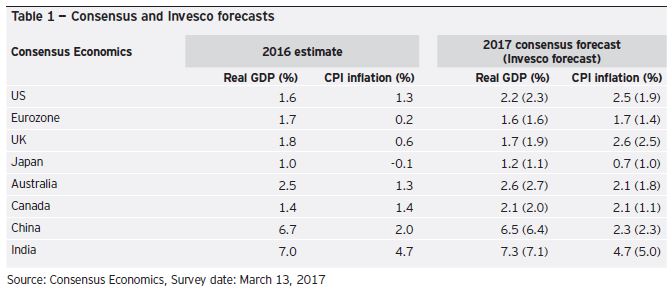

- Between Nov. 4 and March 1 US equity markets rallied by 15% to18%, largely in the expectation that US real gross domestic product (GDP) would accelerate and inflation would also rise, but so far there have been few signs of either. I expect only a modest upswing of growth to 2.3% in 2017 and 2.6% in 2018, a far cry from the growth of 3.5% to 4.0% that President Donald Trump promised in his election campaign.

- Moreover, most of the incremental growth in 2017 and 2018 will come not from the signature Trump proposals of fiscal stimulus, tax cuts or infrastructure spending, but from the strengthening business cycle President Trump has had the good fortune to inherit.

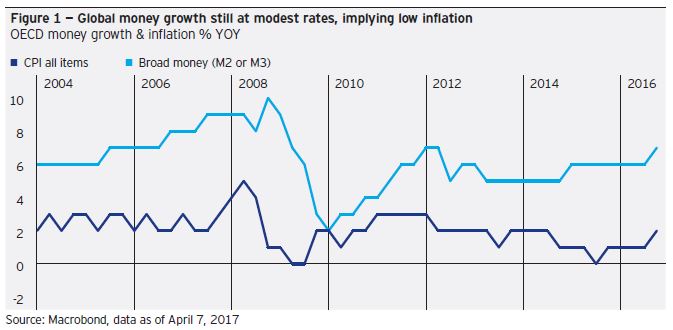

- US consumer price inflation may rise moderately, but will not be much affected by the fiscal deficit. Unless money and credit growth accelerate, inflation will remain broadly unchanged at around 2%. In February the index for core personal consumption expenditures (PCE) was up 1.75%, while core consumer price index (CPI) inflation was 2.2% year-on-year.

- Following the 0.25% hike in the US federal funds rate in March, I expect the US Federal Reserve (Fed) will raise interest rates twice more in 2017, taking the target range to 1.25% to 1.50% by year-end 2017.

- In the Euro-area the near-term environment has been and will be dominated by politics — the Italian referendum last December, the Dutch election held in March, the French presidential election in April/May, and the German election in September, all against the backdrop of extended negotiations over Brexit.

- The economic outlook for the Euro-area remains subdued in the short term, and still far from robust in the long term. Real GDP growth remains steady at around 1.5% to 1.7%, and although headline inflation temporarily increased to 2% in February, it is likely to fall back over the coming months. Core inflation remains at 0.9%, about half of the target rate.

- The European Central Bank (ECB) has reiterated that a shift to tighter policy is not imminent. From April 2017 asset purchases are scheduled to continue at a reduced rate of €60 billion per month at least until December 2017. Sadly, the ECB’s choice of quantitative easing (QE) strategy is failing to boost the purchasing power of households and companies.

- The triggering of Article 50 on March 29 for Brexit will lead to protracted negotiations between Britain and the EU over the next two years. During that period, I expect any progress or setbacks in the discussions to be directly reflected in sterling exchange rates, which will inevitably be volatile.

- Imported inflation from the depreciation of sterling will reduce UK consumer spending in real terms, while the overall uncertainty about the Brexit terms will undermine foreign direct investment (FDI) in the country. However, UK exporters are starting to benefit from a weaker sterling, and the government is beginning to concede that a free trade option could be more beneficial than EU membership.

- Meantime, the Bank of England’s (BOE) credit promotion policies implemented in August risk adding domestically generated inflation to imported inflation from a weak sterling.

- The Japanese economy and Japan’s companies benefitted from mild yen depreciation in November/December following the US presidential election, but domestic consumption and investment remain lackluster and are not likely to accelerate during 2017.

- China remains an enigma. On the one hand, rapid credit growth has slowed and interest rates have risen a little, but in a variety of individual markets the authorities continue to apply stimulus measures. At the same time, overcapacity in basic industries such as coal and steel and rising non-performing loans in the banking system are constraining the growth of new investment.

- On the external side China has been grappling with capital outflows that have outweighed the current account surplus, causing the currency to weaken. However, tighter controls on capital outflows and rising domestic interest rates are slowing the outflow.

- Despite the upswing in oil and certain metal prices over the past year, the anemic recovery in developed economies and the necessary debt workout in a number of emerging economies imply that the upside for commodities in 2017 is limited.

- Finally, the recovery in the US, although already seven and a half years old, is not likely to end anytime soon. Banks are repaired and creating credit; businesses and households are in good financial shape; and inflation is low. Contrary to some forecasters, I expect the current US expansion will continue for several years more.

United States

Coming up to his first 100 days in office, President Trump is falling far short of his intended progress. His executive orders on immigration have been countermanded by the courts, his reform of the ACA has been stopped and it is looking increasingly unlikely that his plans for personal and corporate tax cuts, the introduction of a border adjustment tax and a profit repatriation scheme will be implemented. His infrastructure spending plans (originally $1 trillion over 10 years with one quarter financed by the federal government, three quarters by private participation) are still in gestation. In contrast, President Trump’s executive orders allowing the go-ahead for the Keystone and XL pipelines and nullifying President Obama’s climate change efforts while blocking the closure of hundreds of coal-fired power stations and restoring the mining of coal are, as of this writing, his only significant achievements. The business of government is proving harder than running a group of unlisted, privately owned companies.

Meantime, despite the strong rally in the stock market, the sell-off in the bond market and the improvement in sentiment indicators, the “hard” indicators such as profits and revenue growth, manufacturing output and real GDP growth have been distinctly lackluster. While it is possible that these may move upwards in coming months, there would need to be an extraordinary jump in performance to achieve a growth rate of “at least 3.5% and as high as 4%.” Among the measures that might be expected to assist in reaching that goal are the president’s intention of rolling back the Dodd-Frank Act on banking regulation and the plan to invest in improving infrastructure. If as a byproduct of these changes faster money and credit growth can be achieved, then it is entirely possible that nominal indicators such as final sales, current GDP and corporate profits could start to move upwards more strongly.

For the present, however, such indicators have been disappointing. For example, industrial production in February was up just 0.45% over the preceding 12 months, and the Conference Board’s leading economic indicator was up only 3.1% in the same month compared with 6.3% at the end of 2014. New orders for manufacturing were up by a more encouraging 7.25% in February, although this figure should be compared with double-digit increases at the start of previous industrial upswings in the 1990s and early 2000s. Moreover, the Atlanta Fed’s “GDPNow” estimate for real GDP in the first quarter of 2017, which is based on a wide range of contemporaneous data points, was showing an increase of only 1.2% (at a seasonally adjusted annual rate) on April 4. The GDPNow Indicator seeks to forecast the growth rate of US real gross domestic product before the official estimates are released by the government.

Abroad, President Trump has said he will renegotiate the North American Free Trade Agreement (NAFTA), has withdrawn from the Trans-Pacific Partnership (TPP) and has threatened to impose substantial tariffs on “currency manipulators” to stop the inflow of subsidized and allegedly illegal products at below-market prices. He has therefore instructed the Commerce Department to prepare an analysis of the underlying sources of the US trade deficit within 90 days. But in my view, the Trump administration’s obsessive focus on the trade deficit represents a serious mistake in basic economics: Imports are the gains from trade while exports are the cost of trade — not the other way around as the Trump team appears to think. Goods and services — sometimes including capital — must be exported in order to pay for the imports US consumers and businesses need. If other countries choose to undervalue their currencies to supply exports to the US, their consumers and businesses will suffer because they must pay more for imports of raw materials or consumer goods. Similarly, if foreign countries subsidize their exports with cheap credit or tax exemptions, it is foreign taxpayers who ultimately pay the price, not US consumers or businesses. Closing the trade deficit is not the key to solving the nation’s economic performance woes.

Meantime, the Federal Reserve has continued with its policy of gradually normalizing – not tightening -- interest rates. This means that the Federal Open Market Committee (FOMC) has raised rates in line with what the economy is capable of tolerating, but not enough to squeeze credit (as would be necessary if inflation was a problem). It is true that in recent months US bank loan growth has slowed from 7.8% in September to 4.7% in March, but deposits on the other side of bank balance sheets have continued to grow at a healthy pace, generating M2 growth of 6.4% in the 12 months through February. In addition, bond issuance in the first quarter of 2017 was a vigorous $480 billion following record issuance of $1.54 trillion in 2016. The key point is that other items – such as interbank loans which were up 16.7% in March, and corporate bond issuance -- have compensated for slower loan growth to non-bank customers.

I forecast real GDP growth to improve to 2.3% in 2017 and 2.6% in 2018, and I expect consumer price (CPI) inflation to average 1.9% in 2017.

The eurozone

In the Euro-area the near term environment has been and will be dominated by politics — the Italian referendum last December, the Dutch election held in March, the French presidential election in April/May, and the German election in September, all against the backdrop of extended negotiations over Brexit. Already, in the referendum of Dec. 4, the Italian electorate decisively rejected the proposals of Prime Minister Matteo Renzi for constitutional reform, leaving a political vacuum to be filled by yet another unelected administration, and in the Dutch elections on March 15 the populist party of the right was convincingly defeated. With conventional center-right or center-left governments in France and Germany likely to succeed in the polls during the remainder of 2017, the risk of a disruptive, populist threat to conventional parties appears largely overcome. However, there is still a high level of discontent in Italy (reflected in the popularity of the 5-Star Movement), and in Greece the government is facing debt repayments that will be challenging. Moreover, the unwillingness of the International Monetary Fund (IMF) to roll over its existing loans to Greece suggests there could be a confrontation between the IMF and the EU. In short, political disruption of the status quo cannot be ruled out.

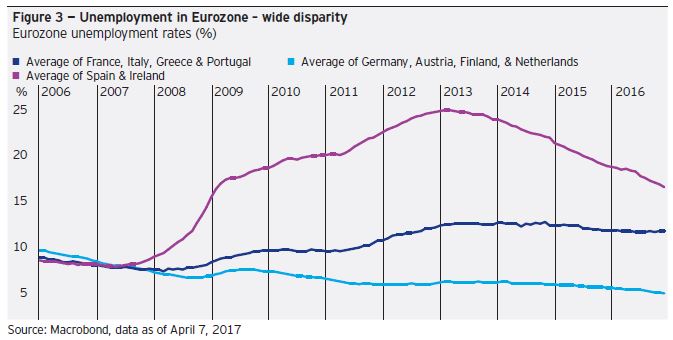

The economic outlook for the Euro-area remains subdued in the short term, and still far from robust in the long term. Real GDP growth remained steady at 1.7% year-on-year in the fourth quarter of 2016, and although headline inflation temporarily increased to 2% in February, it is likely to fall back over the coming months. Core inflation remains at 0.9%, about half of the target rate. Among the headwinds holding back a stronger recovery are the slow progress of bank resolution, the fundamentally unsound design of the ECB’s QE program and the subsequent unwarranted descent into negative interest rates. Unemployment across the Euro-area was 9.5% in February — twice the level in the US or UK — and real household consumption expenditure growth remains at 1.8%. In the short term the PMI indicators have improved to 56.4 in March (according to the composite measure), but lending growth to nonfinancial corporations (1.6% year-on-year in February) and households (2.4% in February) does not suggest any upturn is imminent.

Surveying the fourth-quarter 2016 GDP data for different economies shows a diverse picture across the single currency zone: Ireland grew by 6.6% year-on-year, Spain by 3.0%, Germany by 1.7%, France by 1.1%, and Italy by 1.0%, while Greece saw a year-on-year decline of 1.4%. Despite much better growth figures in Ireland and Spain, these economies are not large enough to shift growth in the entire Euro-area to a higher trajectory, or to attract employees from other member economies as would happen in a well-integrated currency union like the US or Canada. Moreover, the contrast between the recovering economies of Ireland and Spain and the struggling economies of Italy and Greece is likely to be long lasting, heightening interest rate differentials and political tensions across the area.

Mario Draghi, President of the European Central Bank (ECB), reiterated in a speech on April 6 that a shift to tighter policy was not warranted. From April 2017, the ECB’s asset purchases under its QE program are scheduled to continue at a reduced rate of €60 billion per month at least until December 2017. Sadly, however, the ECB’s choice of QE strategy — buying securities from banks instead of non-banks — is failing to boost the purchasing power of households and companies. As a result, M3 growth slowed in February to 4.7%, instead of growing at 7% to 8% as would be feasible if all the ECB’s asset purchases had been focused on nonbanks.

The consensus forecast for eurozone real GDP growth in 2017 is 1.6%, which matches my own forecast. On the inflation front, I expect inadequate M3 growth to continue, keeping inflation at 1.4% compared with a consensus figure of 1.7%, both still undershooting the ECB’s target of “close to but below 2%.”

United Kingdom

The United Kingdom has continued to defy commentators who predicted a post-Brexit downturn, as the economy’s performance has consistently beaten expectations since June. In November the UK’s fiscal watchdog — the Office of Budgetary Responsibility (OBR) — had to revise up its 2017 GDP estimate from 1.4% to 2%, one of its biggest ever upgrades. The two components of GDP that were poised to see a slowdown were investment and household consumption. So far, they have been remarkably buoyant. The depreciation of sterling has been the most obvious result of June 2016’s referendum. Sterling fell 19% against the US dollar from June to November 2016, and 14% on a trade-weighted basis. Since November, with the sudden economic downturn failing to materialize, it has traded more strongly, recovering 2.3% against the dollar and 4.4% against the euro.

So what has confounded the negative forecasts? First, the underlying UK economy has been performing well for several years with GDP growth since 2013 averaging 2.3% annually, aided by the process of private sector balance sheet repair (which has now been largely completed), stable money and credit growth. Thus the UK was the fastest-growing economy in the G7 in 2016. Second, exporters have been the beneficiary of the sterling devaluation with the current account deficit narrowing to 2.4% of GDP in the fourth quarter of 2016, its lowest since 2011. Third, thanks to the UK’s flexible labor market, the economy remains close to full employment. The unemployment rate was 4.7% in January, its lowest rate since 2005, and is expected to remain at around the 5% mark. In contrast to the eurozone, the UK’s inflation rate is now above the Bank of England’s (BOE) target, mainly due to the pass-through from sterling depreciation.

This strong underlying growth, together with the reality that the imposition of tariffs may not be at all damaging even in a “hard” or “clean” Brexit scenario (and could be offset by a fall in sterling), has meant that the weakness in investment has not been as great as many expected. There may of course be a long lag, and there may yet be a decline in investment, but signs show that as long as the economy continues to grow and there are tailwinds for exports from the currency depreciation, investment will continue to remain firm. In March, the UK PMIs for manufacturing, services and construction were 54.2, 55.0, and 52.2 respectively, all well above the expansionary figure of 50.

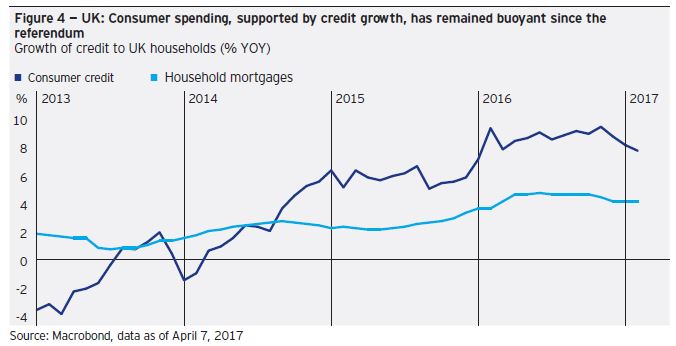

Real private consumption expenditure has continued to grow, seemingly unaffected by the referendum or by the rise in consumer prices, accelerating to 2.9% in the fourth quarter of 2016. Consumer confidence, fuelled by the strength of the labor market and general economic growth, has not suffered the knock that many economists believed would happen after the Brexit result, even if real wage growth is now slowing. Consumption has also been supported by the continued rise in consumer credit, which was growing at 7.7% year-on-year in February 2017, while household mortgage growth was 5.4%.

Giving extra juice to consumer spending and investment has been the BOE’s monetary policy. In the aftermath of the “Leave” vote in the referendum, the BOE responded by cutting the base rate to 0.25%, adding £60 billion of asset purchases (additional QE) and introducing a new Term Funding Scheme on Aug. 4. This now looks to have been an unnecessary stimulus given that the economy was already expanding satisfactorily. The August measures led to a further acceleration in money supply M4x and its lending counterpart: M4x reached 7.4% in October 2016 and was 6.5% in January 2017, both on a year-on-year basis. To keep inflation subdued, these measures of money will need to cool off. Otherwise, in the wake of accelerated money growth and rising consumer credit, full employment, and above target inflation, there may be a case for a rate rise later this year. However, the Monetary Policy Committee remains overwhelmingly dovish, and has attributed price rises to faster-than-expected pass-through from sterling’s devaluation rather than domestically generated money growth.

In sum, while it would be naïve to think that Britain is out of the woods in regard to its exit from the European Union, the country maintains a sound foundation for growth provided monetary policy is managed sensitively. Sterling is likely to remain the safety valve for any negative news emerging from the Brexit negotiations with the EU.

Japan

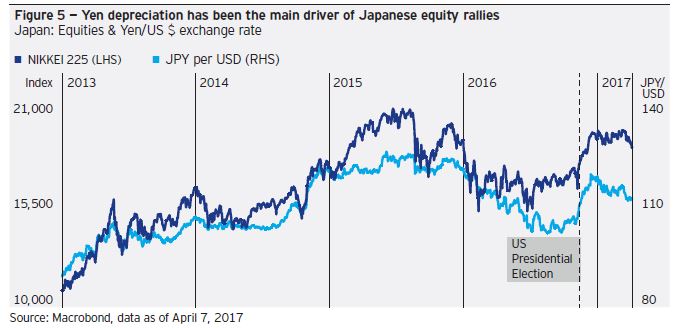

Thanks to an annualized real GDP growth rate of 1.2% in the fourth quarter of 2016, the Japanese economy has now grown for four consecutive quarters — the longest run of growth in three years. This modest growth rate was primarily the result of increased exports, while real private consumption remained subdued at 1.0% year-on-year. The depreciation of the yen has given a boost to exporters and corporate profits, but it is doubtful the increased profits will be passed on to workers in the form of increased wages.

Since the US presidential election on Nov. 8, the yen had depreciated 6% against the US dollar by April 7. Over the same period, the Nikkei 225 Index, benefiting from the currency move and the “Trump trade,” has seen a gain of 14.8% in yen terms and 8.4% in US dollar terms.

The “Abenomics” policy for reviving the economy via the “three arrows” of monetary expansion, fiscal stimulus and structural reform, has still not delivered any meaningful pickup in the domestic economy despite being in operation for nearly five years. Meanwhile the Bank of Japan’s (BOJ) balance sheet has expanded by nearly 200% since March 2013, when the new monetary policy under Governor Haruhiko Kuroda was implemented. Total BOJ assets as of April 3 were 490 trillion yen, of which 95% was domestic government debt. As I have explained here before, I believe the BOJ’s design of its QE is flawed since it purchases assets from banks rather than from the nonbank private sector, and it also still buys short-term paper. The result is that Japanese broad money M2 has not grown anywhere near enough to produce meaningful inflation or growth. M2 was 4.2% year-on-year in February 2017, which is an improvement, but it will need to grow faster (I estimate by 6% per annum) and over a sustained period for the policy to be successful. Japan’s February 2017 headline inflation rate CPI was 0.3%, while the “core-core” CPI — excluding food and energy — increased by just 0.1%.

The Trump administration plans to crack down on economies that it considers currency manipulators. It has highlighted Japan, China and Germany, which all run large current account surpluses, for having manipulated their currencies. Whether the administration takes any countervailing action remains to be seen. So far, China and Mexico have attracted most of the administration’s opprobrium. One area where Japan may suffer from a US shift to greater protectionism is the possibility of a 20% border tax on imports. This would obviously be a problem for Japanese automakers who export cars, trucks and components from Mexico and Japan into the US, although they also have manufacturing operations in the US.

One of President Trump’s first acts in office was to sign an executive order withdrawing the US from the nascent Trans-Pacific Partnership (TPP). This was a concern for Japan as the US is the country’s biggest trading and investment partner. On a positive note, Japan’s exports were up 7.7% in yen terms in the three months to February compared with a year ago, and following February’s meeting between President Trump and Prime Minister Shinzo Abe, a framework for future US-Japan economic discussions was agreed upon.

I expect Japanese real GDP growth to average 1.1% in 2017, while some weakening of the yen (not domestic monetary growth) will raise headline inflation CPI to 1.0% in 2017.

China and the emerging economies

Figuring out what has been going on in China over the past year has been challenging. On the one hand, government spending accelerated from 8% to 18% between late 2015 and the end of 2016, while the central bank lowered some rates but kept others stable. At the same time, the authorities eased lending standards for mortgages and cut auto sales taxes from 10% to 5%. On the other hand, domestic credit growth in China slowed abruptly from 25% to 17% over the past year, the auto tax was raised again to 7.5% and since November the People’s Bank of China (PBC), China’s central bank, has started raising interest rates, allowing the Shanghai three-month interbank rate (Shibor) to rise by almost 150 basis points. In part, the PBC has been closely following the US Federal Reserve to prevent the Chinese currency from depreciating, and it also has been keen to curtail a renewed surge of house prices. Prices in Tier 1 cities had increased by 28% year-on-year last September and were still rising at 22% in February.

On the external side, China’s exports have continued to be lackluster, essentially declining persistently since February 2015 (on a 12-month moving average basis in US dollar terms), while imports have only very recently started to recover. Given that the recent upswing in imports may be associated with base effects stemming from commodity price weakness until December 2015, it would be fair to say that Chinese external trade has basically been contracting in US dollar terms since the start of 2015, or for two years.

Since China is by far the largest EM and the biggest buyer of commodities on world markets, the growth — or lack of growth — of China’s imports matters immensely to many commodity exporters. Unless China can engineer a steady domestic recovery over the next few months, the outlook for those commodity-exporting economies will remain mediocre at best through 2017. In light of the slowdown in domestic credit mentioned above, and the much-discussed problems associated with China’s build-up of indebtedness, such an upswing does not seem feasible, at least in the short term.

Turning to the smaller, manufacturing economies of East Asia, which are heavily involved in regional supply chains (including China), these will depend far more for export improvements on the ongoing business cycle upswing that is underway in the US than on a turnaround in the domestic Chinese economy. The eurozone, Japan and the UK will gradually add to the improvements in final demand coming from the US, but it is the US that remains the key locomotive economy in this process.

Commodities

Regular readers will know that I have been cautious on the outlook for commodity prices over the past three years on the grounds that the recovery in developed economies was still anemic, while emerging economies were either in recession or had big debt problems that would inhibit rapid recoveries. Therefore, the overall demand for commodities would remain weak. However, the recovery of oil and metal prices in 2016 began to suggest that the bear phase might be coming to an end. At the present juncture, with President Trump’s infrastructure plans still on the drawing board and China slowing its credit injections, commodity prices have not taken off, and consequently my forecast remains largely intact.

For example, iron ore prices in China have fallen 9.2% since mid-March 2017. This fall comes after a collapse of 75% from the peak prices of 2010-11 to a low in late 2015 and early 2016. Subsequently there was a recovery of 53% between January 2016 and March 2017 (explained largely by Chinese government manipulation as discussed here previously). Much of 2016’s price rise was due to increased stimulus for the construction industry in China, as authorities fretted about an economic slowdown, but with large inventories — a record 132.5 million tons — in China and continuing excess capacity in the steel industry, the recent momentum is starting to disappear from this market. The other major input in steel production is coking coal, which also saw a dramatic price recovery in 2016 due to Chinese government curbs on the number of days of operation for local mines, but its price is also down 3.8% this year on the Dalian Commodity Exchange.1

The outlook for iron ore and coking coal are both closely dependent on Chinese economic growth. With the critical 19th Communist Party Congress scheduled for autumn 2017, the authorities will likely try and keep GDP at its current growth rate until then, while cracking down on speculators by tightening access to credit facilities. Thus the China Banking Regulatory Commission recently announced plans to crack down on the lending activities of asset management firms seen as risky actors in the shadow banking sector and major creditors to commodity speculators. Overall, it seems unlikely that iron ore and coking coal prices will rise much from current levels.

Turning to the oil market, my previous contention that oil prices would stay subdued despite the Organization of Petroleum Exporting Countries’ (OPEC’s) production cut has also held true. The key reason was the resilience of the US shale industry, which is ramping up production again. The US rig count is up to 809, a 100% increase from May of last year, which was the nadir of the rig count. This is still less than half the number of rigs that were operating before the oil price fall of 2014, implying there is still plenty of scope for further increases in shale production.

The resurgence of shale has followed a dramatic contraction in the industry between the third quarter of 2014 and the second quarter of 2016. During that period, over 100 US shale companies went bust as they defaulted on at least $70 billion of debt. The surviving companies and new entrants have made efficiency improvements and technical advances allowing them to make a profit at current lower oil prices. This has led to a rise in output of 7.1% since October 2016, with the US currently producing 9.1 million barrels of oil per day. Shale has permanently changed the structure of the oil market and eroded the ability of OPEC to manipulate international oil prices. It will also put pressure on the cartel’s cohesion if OPEC’s recent efforts to raise prices prove to be ineffective.

Turning to soft commodities, US grain and soy farmers are very wary about the threat from President Trump’s protectionist trade policies. They are already suffering from the strong dollar, which has reduced their competitiveness and led to four years of falling earnings. With Mexico being the largest importer of US corn, there is anxiety about President Trump tampering with NAFTA. Already Mexico is talking of reducing tariffs on Argentine and Brazilian grains to zero, which would give South American exporters the same advantage as US producers have under NAFTA. US farmers will be very resistant to any proposed changes to NAFTA, and prices are unlikely to rise much under any scenario that features a domestic US glut.

Conclusion

The Trump “reflation rally” has driven equity markets across the developed and emerging world in the four months since the US election, while at the same time generating a meaningful upturn in longer term bond yields. However, with the new president now meeting opposition to his programs — notably his contested executive orders on immigration and his attempt to repeal the ACA — there are starting to be significant doubts about his ability to implement other elements of his program such as the proposed personal and corporate tax cuts, the Ross-Navarro infrastructure spending plan and the repeal of the Dodd-Frank legislation. While these concerns could well cause stock market momentum to pause, the more important driver of long-term stock market performance is the direction of the US business cycle.

In every business cycle, the value of equities and real estate are fundamentally driven by the level of business activity (or expectations for such activity). In this respect President Trump’s inheritance is a singularly favorable one. Banks and households that were overleveraged in the 2008-09 crisis have mostly completed the repair of their balance sheets, inflation is low and the Fed has been able to start normalizing short-term interest rates. Therefore, there is very little risk to a continuation of the current business cycle upswing in the US. Moreover, because the US is so large and dominant not only in terms of GDP but also in terms of its financial impact on credit, equity, real estate and other developed and emerging financial markets, this has hugely important implications for the world economy as a whole.

With the US Fed having moved to raise interest rates (to normalize but not tighten monetary policy) three times — in December 2015, December 2016, and March 2017 — the critical issue will be whether money and credit growth can be sustained at 6% to 8% per annum (as it was in 2015-16). If the Fed, commercial banks and the capital markets together are able to maintain these money and credit growth rates, then even if bond and equity markets are temporarily jolted by random political or protectionist shocks, the US and global economies will, in my view, be able to shrug off the gradual interest rate normalization and continue expanding for several more years before the business cycle hits a peak.

1 Source: Macrobond

John Greenwood Chief Economist

Based in London, John is Chief Economist of Invesco Ltd. with responsibility for providing economic analysis and forecasts to Invesco portfolio managers and clients.

John started his career in 1970 as a visiting research fellow at the Bank of Japan. He joined our company four years later in 1974 as Chief Economist, based initially in Hong Kong and later in San Francisco. As editor of Asian Monetary Monitor in 1983, he proposed a currency board scheme for stabilizing the Hong Kong dollar. John was a director of the Hong Kong Futures Exchange Clearing Corporation for four years until 1991, and in 1992 became a council member of the Stock Exchange of Hong Kong, a position he held for twelve months. In that same year, he was an economic adviser to the Hong Kong Government. He has been a member of the Committee on Currency Board Operations of the Hong Kong Monetary Authority since 1998. He is also a member of the Shadow Monetary Policy Committee in England, and he serves on the board of the Hong Kong Association in London.

John holds an MA from the University of Edinburgh, and an Honorary PhD, also from the University of Edinburgh.

Important information

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2017 Invesco Ltd. All rights reserved.

Quarterly economic outlook for the second quarter of 2017 by Invesco.