Investment Strategy: What Matters in the Search for More Return Sources

A prior blog post shared the view that the low return environment requires investors to tap many return sources. One of these sources is dynamically adjusting portfolio allocations. This is easier said than done, though, and this blog will explore how investors can put dynamism into practice.

Cycle, Value and Sentiment

In our investment strategists’ investment strategy, we focus on three lenses to help us identify dynamic market opportunities: Cycle, value and sentiment.

Our value discipline identifies asset classes, markets, or factors that are currently cheap against other investment opportunities or relative to their history. The bigger the discount, the bigger the opportunity. Where assets are trading at a premium, the risk of owning them in a downturn is greater.

Cycle uses what we know about the relationship between financial markets and the macro-economy and an informed view of where we are in the business cycle to forecast which markets and factors are likely to do well in the years ahead.

Our measures of sentiment look to indicators of trending behavior or market switchbacks to help understand the short-term outlook for the assets we invest in.

Taken together, these disciplines help our investment strategists to judge potential asset attractiveness from three different standpoints in a way to help to improve the likelihood of investment success. It is as if we are looking at the age, color and firmness of an unopened avocado to determine whether we want to buy it and cut it up in our salad. None of them guarantees a good-tasting avocado, but using all three gives you a better chance of getting it right. But what does that tell us about the markets now?

A Slumbering Market

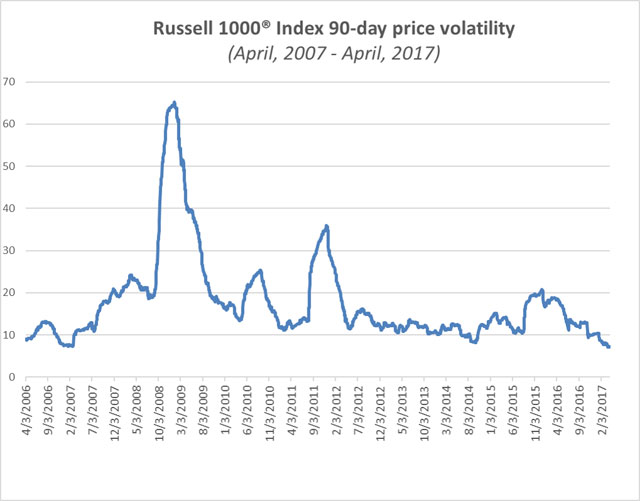

An eerie calm has descended onto equity markets in the United States. Despite the constant noise and drama in Washington D.C., Wall Street is the picture of quiet confidence. The U.S. equity market is experiencing extraordinarily low levels of price volatility. As seen in the chart below, realized market volatility has also been very modest by historical standards. Should investors see this as an "all-clear" signal to take on more risk?

Source: Russell 1000® Index, as of April 3, 2017.

Note: 90-day Price Volatility equals the annualized standard deviation of the relative price change of the 90 most recent days closing price, expressed as a percentage.

To answer that question, we need to take a closer look. The combination of the so-called Trump trade— which anticipates substantial economic benefits from fiscal stimulus provided by the new administration and the reflation trade—which posits healthy global economic growth—have lifted markets and seemingly quelled the uncertainty that gives rise to market volatility.

On the surface, then, all seems well. U.S. economic data has been strong, as Kara Ng pointed out in last week’s blog post. High hopes for the new president's fiscal plans lend credence to potential upside opportunity. And, given extremely low equity market volatility, the market seems comfortable with the upward trend in market values.

These investment disciplines complicate our view regarding the U.S. market.

As noted in our latest Global Market Outlook-Q2 Update, U.S. equities look expensive by most measures, which mean short-term risk and compressed medium-term return potential in our view. While enthusiasm for potential U.S. administration policies pushes the market up, a strong dollar, creeping wage inflation and a U.S. Federal Reserve seemingly committed to raising rates suggest we may be past the most equity-friendly part of the U.S. economic cycle. Sentiment is supportive in as much as the trend is favorable, but even when viewed through that lens, U.S. equities appear somewhat overbought.

Looking globally for potential return sources

All of this suggests caution with regard to U.S. equity investments, but what looks better? We believe that European and emerging market equities, buoyed by better valuations and an improving economic outlook, are certainly more attractive and a case can be made for some select fixed income sectors. This too is covered in our latest report.

Being strong for the long-run

But the overriding message from our research is one that is likely obvious to many—we think that there are not currently the kind of enormous return opportunities we have seen after economic downturns or at valuation lows. Investors need to have the intestinal fortitude to help to avoid getting sucked into taking too much risk late in the cycle. As history shows, the market will turn again, and a dynamic process can help to provide the ability to keep investors at the ready for new return sources as they arise.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page.

This material is not an offer, solicitation or recommendation to purchase any security. Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type.

The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth.

Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

The Russell 1000® Index measures the performance of the 1,000 largest companies in the Russell 3000® Index, representative of the U.S. large capitalization securities market.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

Copyright © Russell Investments 2017. All rights reserved.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI – 11038