On My Radar: Fundamentally Bipolar; Fed Tightening Cycles – Past and Present

Learn more about this firm“…the Fed has typically tightened too much and/or for too long.

From this long history, a well-established pattern is identifiable.

The economic growth rate along with inflation receded.

A financial crisis was more likely than not.”– Van R. Hoisington and Lacy H. Hunt, Ph.D.

Many years ago I created an economic investment dashboard of sorts to help me do my best to keep my head screwed on straight. If you subscribe to a handful of research services, you know what I mean. For every 10 bulls, there are 10 bears.

When I was a young Merrill Lynch financial consultant, in addition to ML’s research, I subscribed to over a dozen investment newsletters. I found myself spinning in a sea of mixed messages. My manager thought I was nuts. Perhaps he was right. Think of the research we now have at our fingertips. Really cool; but frankly, exponentially more confusing. It’s easy to get emotionally pulled off-sides. So it’s the dashboard for me.

On the dashboard, among other data inputs, are my favorite recession indicators and an inflation indicator chart. Depending on how your portfolio is positioned, both events will impact your net worth (favorably or unfavorably). Today, you’ll find below several recession prediction charts. You’ll see that I highlight in red (bad) or green (good) the checklist of things I follow based on the current state of each indicator.

I believe the recession watch charts are the most important. Why? We get one to two each decade, the last was in 2008 and we are due. Why? Because that is when all the bad stuff happens. Defaults rise and stock markets decline 40% or more. You’ll see below that the good news is the current probability of recession is low.

You can find my dashboard every Wednesday afternoon in the Trade Signals research page on our website. I also provide a link for you each week in On My Radar(link below). Note, I’m a trend follower so you’ll find a lot of trend-based indicators as well.

But before you jump into the recession data, I want to share something I feel deserves your attention. One letter that is a must-read is the quarterly investor letter from Van Hoisington and Dr. Lacy Hunt. I know of no one else that understands Fed policy and history better. So before you view the recession probability charts, let’s take a look at what they have to say about the Fed. They believe the Fed is leading us right into the next recession. Their insights and my charts tie together.

What to watch for? This from Van and Lacy:

The Federal Reserve has initiated the fifteenth tightening cycle since 1945. Conspicuously, in 80% of the prior fourteen episodes, recessions followed, with outright business contractions being avoided in just three cases. What is notable today is that the economy is in the 93rd month of this expansion, a length of time that is well beyond periods in prior expansions where soft landings occurred (1968, 1984 and 1995). This is relevant because the pent-up demand from the prior downturn has been exhausted; thus, the economy is extremely vulnerable to a shock, which could lead to recession.

Regardless of whether there was an associated recession, the last ten cycles of tightening all triggered financial crises. In conjunction with the non-monetary determinants of economic activity (referred to as initial conditions), monetary restraint served to expose over-leveraged parties and, in turn, financial crises ensued.

Fear not, my good friend. Just put in place a plan that enables you to risk manage what you’ve got. The last two recessions found the stock market declining by more than 50%. What aging, baby booming (me included) pre-retiree or retiree can afford to take that hit? On average, think -40% during recession.

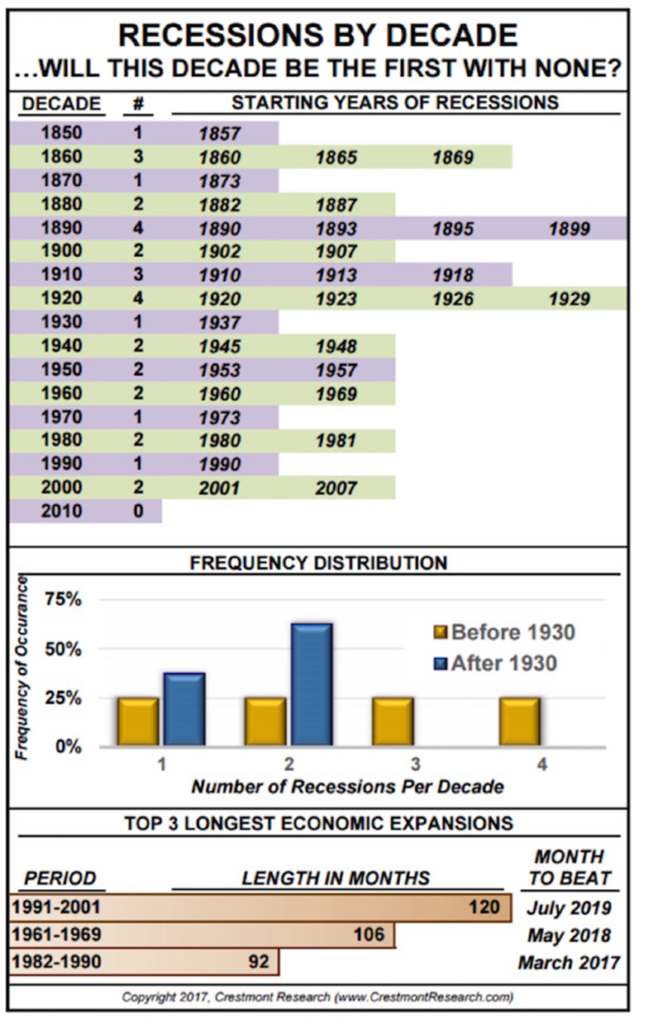

The last recession was in 2008-2009. There has been no decade since the year 1850 where we did not get at least one recession. Can this decade break the trend? I doubt it.

Because recessions are only officially known in hindsight and after all the bad stuff happens, we have to do our best to get in front of them. Thus, my recession obsession. To that end, today you’ll find my favorite recession watch charts in the Charts of the Week section below along with an explanation of how they work.

But first, read what Van and Lacy have to say. I share several highlights in bullet point form and provide a link to the full letter.

Read on… and have a wonderful, long holiday weekend!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- Fed Tightening Cycles – Past and Present, by Van R. Hoisington and Lacy H. Hunt, Ph.D.

- Charts of the Week

- Trade Signals – Low Risk of Recession Risk, High Risk of Inflation, Equity Trend Remains Bullish

- Personal Note

Fed Tightening Cycles – Past and Present

Following are my high level notes from Hoisington’s quarterly letter:

- Four important considerations exist today that were not present in past cycles and that may magnify the current restraining actions of the Federal Reserve:

(1) The Fed has initiated a tightening cycle at a time when significant differences exist in the initial conditions compared to the initial conditions in prior cycles. Additionally, the Fed is tightening into a deteriorating economy with last year’s growth in nominal GDP worse than in any of the prior fourteen cases.

(2) Business and government balance sheets are burdened with record amounts of debt. This means that small changes in interest rates may have an outsized impact on investment and spending decisions.

(3) Previous Federal Reserve experiments, primarily the periods of quantitative easings, have led to an unprecedented balance sheet (an action of “grand design”) to which the economy has grown accustomed. The resulting reduction in that balance sheet (reduction in the monetary base) may have a more profound impact on growth than anticipated.

(4) The monetary base reduction and the impact of the changing regulatory landscape, both in the U.S. and globally, has meant a significant increase in the amount of liquid reserves that banks are required to hold. Liquidity may have already been sharply restrained by the lowering of the monetary base, despite its massive $3.8 trillion size. This is evident as the monetary and credit aggregates are following the expected deteriorating pattern resulting from monetary restraint, suggesting recessionary conditions may lie ahead.

SBB: Here’s more… then Van and Lacy’s conclusion.

- Several factors that influence the economy (other than monetary policy) are far more problematic than those that existed in any of the prior tightening cycles. For instance, the U.S. is experiencing the weakest population growth since the 1930s and the lowest fertility rate since the records began. There has been a slowdown in the growth rate of household formation, and the U.S. has a rapidly aging society.

- For the full calendar year 2016, nominal GDP rose just 3.0%, the weakest reported since 2009. Last year’s growth rate was even less than the cyclical lows associated with the recessions of 1990-91 and 2000-01.

- Despite the lowest annual economic growth rate of this expansion and the second straight year of declining growth, no fiscal stimulus is expected for 2017.

- Monetary restraint implemented in late 2015 and 2016 has been followed by further restraint in 2017. How can the U.S. economy surge ahead this year with this additional restraint?

- Total domestic nonfinancial debt, excluding off balance sheet liabilities such as leases and unfunded pension liabilities, surged to a record 254.8% of GDP in 2016, 5.6% greater than in 2009 when Lehman Brothers failed.

- Total debt, which includes domestic nonfinancial, foreign and bank debt, amounted to 372.5% of GDP in 2016, compared with 251.9% of GDP in 2006, the final year of previous tightening cycle, which, in turn, was greater than in any earlier time from 1870 through 2006.

- Academic studies reflect that economic growth slows with over-indebtedness. Thus a powerful negative headwind is reinforcing the present monetary tightening.

SBB: I thought this next point was particularly important to keep in the back of our minds.

- Two macroeconomic textbooks (one written by Andrew B. Able (Wharton Professor) and Ben S. Bernanke (former Fed Chairman) and the other by N. Gregory Mankiw (Harvard Professor) both discuss over several chapters the transmission mechanism of monetary policy operations to the broader economy. They both describe a very similar process as to how Fed restraint impacts economic conditions.

- Their independently taught process exactly describes what is unfolding in the reserve aggregates, short-term interest rates, bank loan volumes and the monetary aggregates today.

SBB: Here is the main point!

- However, the established process may more severely impact the economy because these actions are being taken in the aftermath of three unprecedented rounds of quantitative easing that have led to a massively enlarged Fed balance sheet (an action of “grand design”) coupled with the legislative adoption of the Dodd-Frank Law.

SBB: I believe we must keep the idea of “unintended consequences” on our radars. From Van and Lacy:

- The late American sociologist, Robert K. Merton (1910-2003), who originated the concept of “unintended consequences”, identified the problems that arise when policy implements theories of grand design. Merton believed that middle range theories are superior to larger theories of grand design because larger theory outcomes are too distant for policy makers to realize how actions and reactions will change from the middle range theories under which they have typically operated.

- Merton argued that when dealing with broader, more abstract and untested theories, no effective way exists to test their success in advance.

- We believe these are problems the Fed is already facing as their actions have changed the monetary landscape from previous periods of monetary restraint.

- The Fed (and the entire economy) is now caught in a new format that never existed, and thus is without the ability to anticipate the outcomes to policy because there is no historical reference point. We suspect that the results of the Fed’s tighter policies will be exacerbated by its own balance sheet and by the larger cash and liquidity requirements mandated by the Dodd-Frank Law.

One of the most important 20 minutes you can spend is watching Ray Dalio’s “How The Economic Machine Works.” I say this as it relates to Van and Lacy’s comments on page 4 of their quarterly letter. Money and credit fuel the system. Borrow more, spend today, good for growth. Borrow too much, can no longer borrow, less money/credit available to you to spend, a larger percentage of income required to pay down debt, bad for growth.

Credit is available to us via banks. Raising interest rates in a highly indebted environment not only means we pay more on what we owe, it affects the rules around how much capital a bank has to lend. Van and Lacy go on to explain this quite brilliantly on page 4. They say, “Based upon an examination of all the monetary indicators closely linked to the policy rate and the reserve aggregates, the probability exists that the Fed, with three small increases in the federal funds rate, has now turned the money/credit creation process negative.”

- Traditionally, money and credit slowdowns have resulted in tighter bank lending standards, and this is currently the case.

- In the last three months, no growth was registered in total loans and nonfinancial commercial paper. Historically, the three-month growth has not been this weak until the economy is already in recession.

“…the Fed has typically tightened too much and/or for too long. From this long history, a well-established pattern is identifiable. The economic growth rate along with inflation receded. A financial crisis was more likely than not.”

Van and Lacy conclude:

- Our economic view for 2017 remains unchanged. We continue to anticipate no more than 2% growth in nominal GDP for the full calendar year.

- The downturn in nominal GDP growth suggests that a rise in inflation to above 2% will be rejected and that by year end the inflation rate will be considerably slower.

- In such an economic environment, long-term Treasury yields should continue to work irregularly lower over the balance of the year. Thus, the secular low in bond yields remains in the future, not the past.

Higher interest rates? Take that Gross, Gundlach (“the low in bond yields is in”), Pimco and Blumenthal. I’ve been in the “rates will rise this year” camp, but do think the next recession will see them lower one last time again. Another bite at refinancing that mortgage? Maybe. So I find myself feeling kind of fundamentally bipolar. To which, I am a trend following guy. It helped me avoid the -15% hit Lacy took last year and kept me in line with Lacy in 2015 despite my personal view (along with 25 out of 25 Wall Street analysts) that rates would rise.

Van and Lacy and trend following remained bullish and so did my positioning. The trend evidence kept me on sides. Right now, the Zweig Bond Model (as you’ll see below if you click through to the Trade Signals charts) remains bearish on bonds. I’m sticking with trend.

I imagine my Susan and your client reading this last section and their eyes begin to cross. I get it… this is really deep wonk stuff. Here’s the bottom line. We and the Fed find ourselves in a very tricky economic spot.

Charts of the Week

Following are several charts I came across recently that I found of particular interest.

Number of Recessions per Decade

My Favorite Recession Indicator Charts

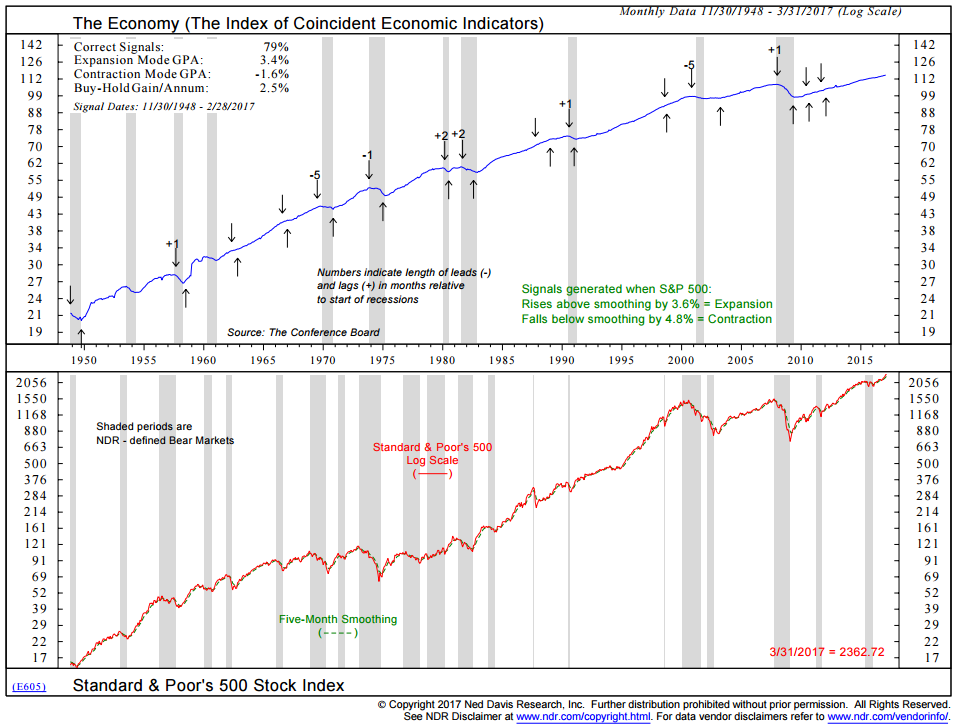

This first chart looks to the stock market to predict recession in advance or near recession start. The idea is that stocks are a leading economic indicator. You and I voting with our money. Company earnings are a gauge of economic activity. If a company’s fundamentals decline, we might sell.

Here’s how you read the chart:

- The lower section (red line) tracks the S&P 500 Index. The dotted green line is the Five-Month Smoothing of the S&P 500 Index’s price. Think moving average.

- When the red line drops below the smoothed green line by 4.8% or more, recession has followed in most cases.

- The down arrows mark the recession signal. +1 or -5 or +2 etc. tell us how many months after (+1) or before (-5) recession started. Again, the rules of recession are only known more than six months after they are deemed to have begun.

- Expansion periods or up arrows are signaled when the red line rises above the green line by 3.6% or more.

- 79% of the signals in the data series were correct.

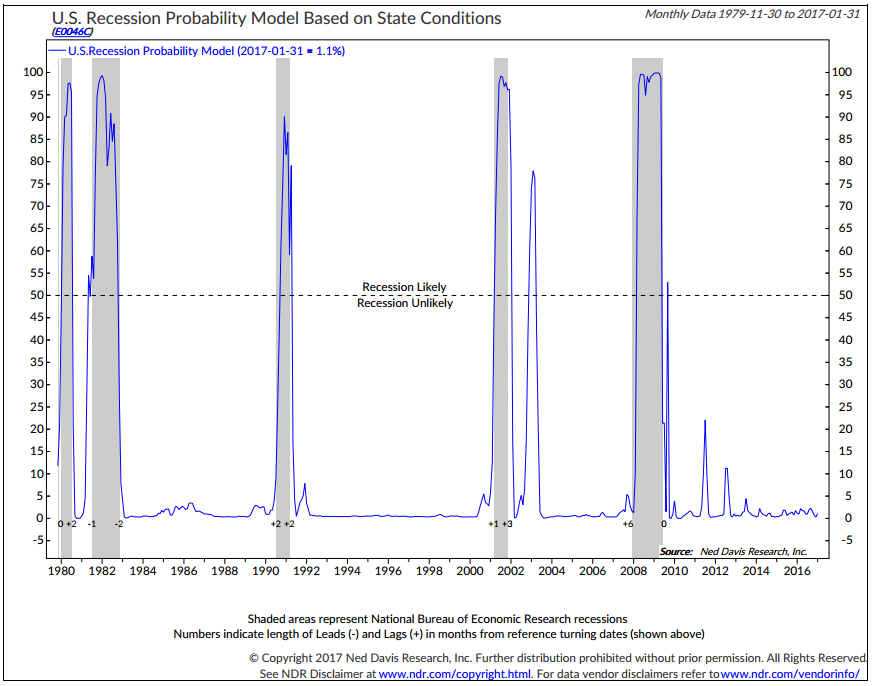

Recession Probability Model – Based on State Conditions

Here is how you read the chart:

- The individual state indexes combine nonfarm employment, average manufacturing hours worked, the unemployment rate, and real wages and salaries. As economic conditions deteriorate across a growing number of states, the estimated recession probability for the U.S. increases.

- Conversely, as conditions hold positive or improve across a growing number of states, the estimated recession probability declines. Historically, the Model has identified NBER-defined recessions within two months of the actual date. Source: Ned Davis Research

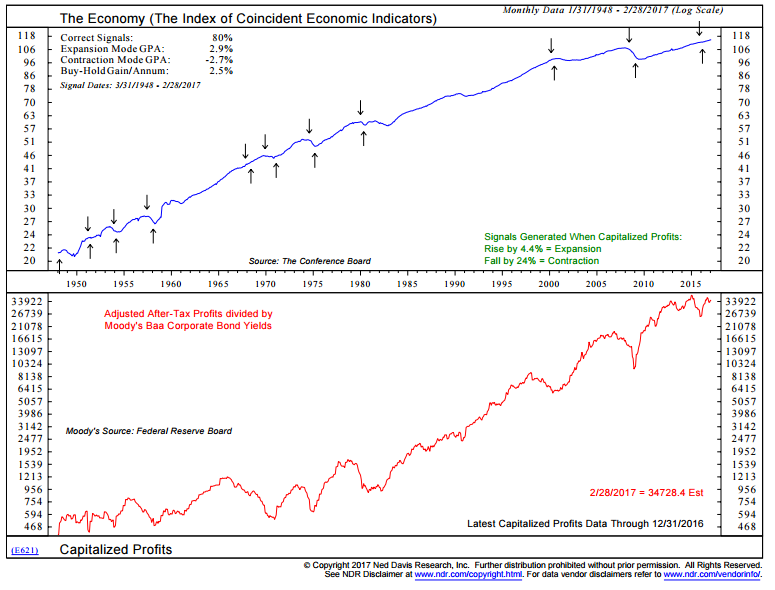

The Economy – After Tax Profits divided by Moody’s Baa Corp Bond Yields

Here is how you read the chart:

- Up arrows mark economic expansion.

- Down arrows mark economic contraction.

- 80% of signals in data series (back to 1948) were “correct.”

- Current signal = “Expansion”

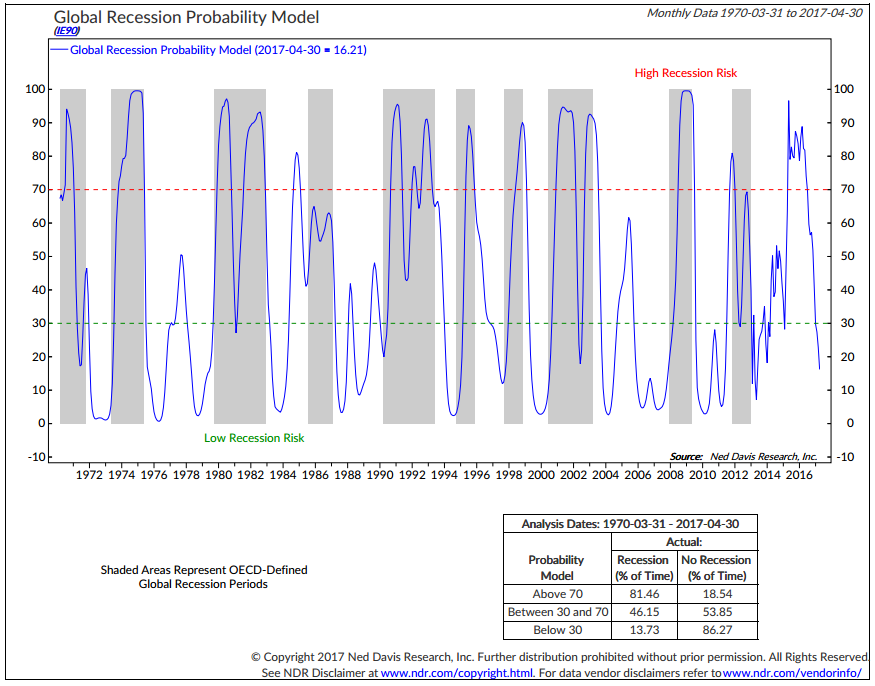

Global Recession Probability Model

Here’s how you read the chart:

- Focus in on the data in the lower right-hand section of the chart.

- 4% of the time that the blue line was above the dotted red line, recession occurred. Above 70 equals “High Inflationary Risk.”

- 37% of the time the blue line was below the dotted green line, recession occurred. Below 30 equals “Low Inflationary Risk.”

- Currently signaling low inflationary risk.

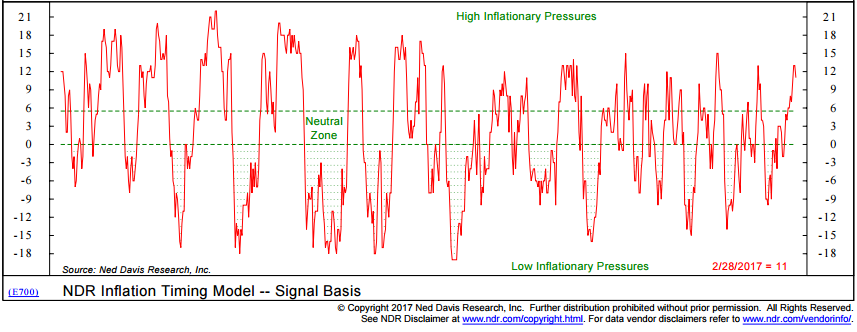

And here is the Inflation Watch Chart

- Currently signaling high inflationary pressures.

- Here is my thinking: If pressures stay high, expect the Fed to continue to raise rates, which takes my mind back to the Van and Lacy comments above.

- The Fed, as they have in past cycles, we drive us into the next recession.

I’m a very big Ned Davis Research fan. I’ve been a subscriber and happy client since the mid 1990’s. They kindly let me share certain charts with you, but I story them in a way to share with you how I’ve been using many of the charts for many years. I love the data and I think NDR is one of the best independent research shops in the business. They serve institutional clients, but also offer a less expensive abridged service.

If you’d like to learn more about their subscription services, contact Dan Dortona via email at [email protected]. Please know I don’t get paid a penny from NDR nor a reduction in my subscription fee. Just a happy client.

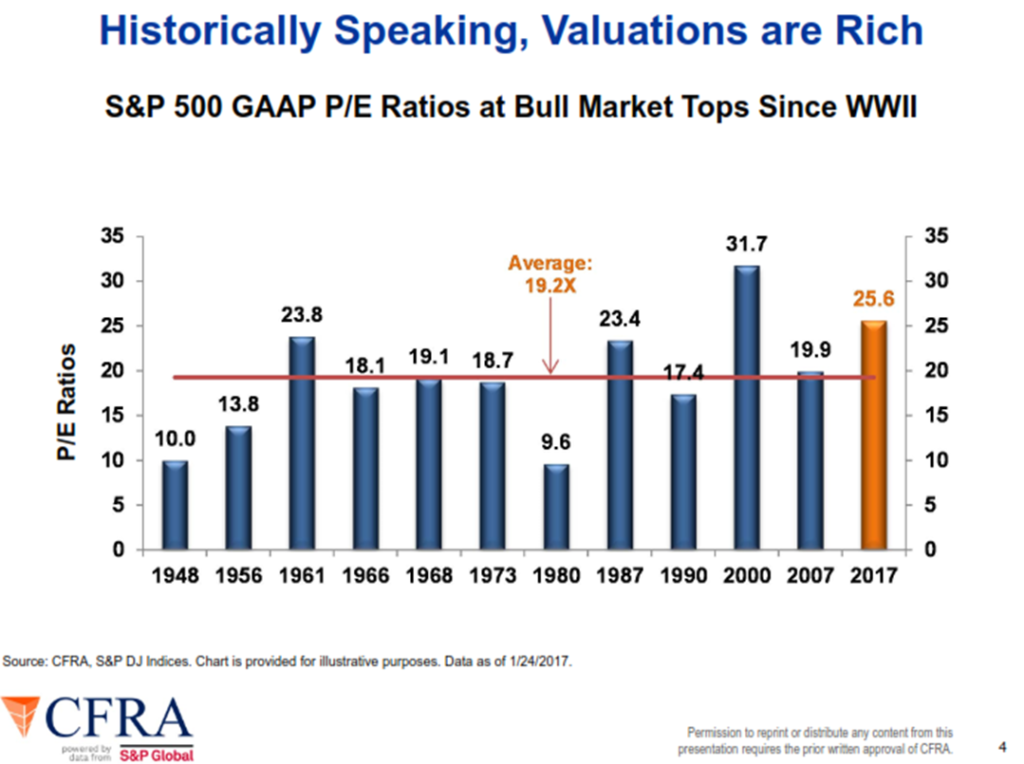

As if we need any more reminders… Historically Speaking Valuations are Rich

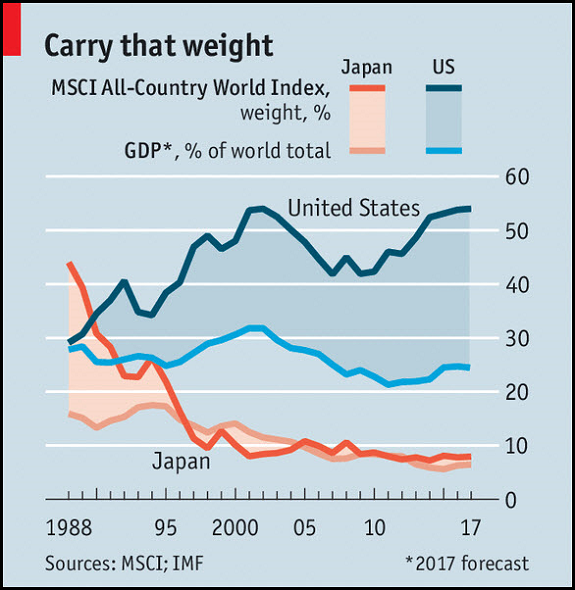

Finally, I found this next chart interesting – America’s Disproportionate Weight in Global Stock Market Indices, from The Economist. From the article:

American market has a weighting of 54% in the index, as high as it has ever been (it reached the same level in 2002). In other words, anyone using the index to monitor the market is seeing a picture heavily distorted by Wall Street. The relative performance of international fund managers against the index will largely depend on how much exposure to America they are willing to take on. Anyone buying a tracking fund is, in effect, making a big bet on the American market.

SBB here: We might not be getting the diversification we think we are. Correlations will move to 1 in times of crisis.

One last point from the article:

American companies trade on a multiple of 21 times last year’s earnings, compared with 18 for Europe, 17 for Japan and 14 for emerging markets. On a cyclically adjusted basis (averaging profits over ten years), the ratio of the American market to earnings is as high as it was in the bubble periods of the late 1920s and 1990s.

OK, that’s enough fun charts for the week. Very low current recession risk. Let’s raise a beer to that… As you’ll see next in Trade Signals, the equity market trend remains bullish. Let’s raise a second beer to that.

Trade Signals – Low Risk of Recession, High Risk of Inflation, Equity Trend Remains Bullish

S&P 500 Index — 2,346 (4-12-2017)

The weight of evidence for the equity market remains bullish. For investors in our strategies: the CMG Opportunistic All Asset ETF Strategy remains overweight equities (both US, EM and Developed World). The CMG Managed High Yield Bond Program remains in a buy signal. The CMG Tactical Fixed Income Strategy is invested equal weight to a muni bond ETF and an emerging market sovereign debt ETF.

The Zweig Bond Model signal remains in a sell signal – the trend for fixed income remains negative (signaling higher interest rates). Both the long-term and short-term gold trend indicators are in buy signals (suggesting some exposure to gold).

On the economic front: from both global and domestic perspectives, risk of recession remains low, however, risk of inflation is elevated and warrants regular monitoring.

Click here for the charts and explanations.

Personal Note

I’ll be NYC April 19-20 and Sonoma, California the following week from April 24-26 for the CMG & Peak Capital Advisor Summit. Dallas on May 15-17 and Orlando on May 22-25 for the Strategic Investment Conference. The conference topics are ultimately tied to best ideas on how to position and make money. It’s an investing, economics and geopolitical data download with some of the most influential thinkers presenting. Speakers include David Rosenberg, Dr. Lacy Hunt, Mark Yusko, Neil Howe, Ian Bremmer (Charlie Rose recently interviewed him), David Zervos from Jeffries and more. You can learn more about the conference here. Similar to years past, I’ll be taking a lot of notes and promise to share them with you.

It’s a long weekend ahead and, importantly, it’s Easter. Susan and I are sneaking away to Stone Harbor for the weekend. It’s been in the 80s much of this week and the forecast looks pretty good for the next few days. Hope you have some fun plans in your weekend.

Wishing you and your beautiful family a wonderful holiday.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.

Social Media Links:

CMG is committed to setting a high standard for ETF strategists. And we’re passionate about educating advisors and investors about tactical investing. We launched CMG AdvisorCentral a year ago to share our knowledge of tactical investing and managing a successful advisory practice.

You can sign up for weekly updates to AdvisorCentral here. If you’re looking for the CMG white paper, “Understanding Tactical Investment Strategies,” you can find that here.

AdvisorCentral is being updated with new educational resources we look forward to sharing with you. You can always connect with CMG on Twitter at @askcmg and follow our LinkedIn Showcase page devoted to tactical investing.

A Note on Investment Process:

From an investment management perspective, I’ve followed, managed and written about trend following and investor sentiment for many years. I find that reviewing various sentiment, trend and other historically valuable rules-based indicators each week helps me to stay balanced and disciplined in allocating to the various risk sets that are included within a broadly diversified total portfolio solution.

My objective is to position in line with the equity and fixed income market’s primary trends. I believe risk management is paramount in a long-term investment process. When to hedge, when to become more aggressive, etc.

IMPORTANT DISCLOSURE INFORMATION

Investing involves risk. Past performance does not guarantee or indicate future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by CMG Capital Management Group, Inc. or any of its related entities (collectively “CMG”) will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. No portion of the content should be construed as an offer or solicitation for the purchase or sale of any security. References to specific securities, investment programs or funds are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities.

Certain portions of the content may contain a discussion of, and/or provide access to, opinions and/or recommendations of CMG (and those of other investment and non-investment professionals) as of a specific prior date. Due to various factors, including changing market conditions, such discussion may no longer be reflective of current recommendations or opinions. Derivatives and options strategies are not suitable for every investor, may involve a high degree of risk, and may be appropriate investments only for sophisticated investors who are capable of understanding and assuming the risks involved. Moreover, you should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from CMG or the professional advisors of your choosing. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisors of his/her choosing. CMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

This presentation does not discuss, directly or indirectly, the amount of the profits or losses, realized or unrealized, by any CMG client from any specific funds or securities. Please note: In the event that CMG references performance results for an actual CMG portfolio, the results are reported net of advisory fees and inclusive of dividends. The performance referenced is that as determined and/or provided directly by the referenced funds and/or publishers, have not been independently verified, and do not reflect the performance of any specific CMG client. CMG clients may have experienced materially different performance based upon various factors during the corresponding time periods.

NOT FDIC INSURED. MAY LOSE VALUE. NO BANK GUARANTEE.

Certain information contained herein has been obtained from third-party sources believed to be reliable, but we cannot guarantee its accuracy or completeness.

In the event that there has been a change in an individual’s investment objective or financial situation, he/she is encouraged to consult with his/her investment professional.

Written Disclosure Statement. CMG is an SEC-registered investment adviser located in King of Prussia, Pennsylvania. Stephen B. Blumenthal is CMG’s founder and CEO. Please note: The above views are those of CMG and its CEO, Stephen Blumenthal, and do not reflect those of any sub-advisor that CMG may engage to manage any CMG strategy. A copy of CMG’s current written disclosure statement discussing advisory services and fees is available upon request or via CMG’s internet web site at www.cmgwealth.com/disclosures.

© CMG Captial Management Group

© CMG Capital Management Group