Angst in America, Part 4: Disappearing Pensions

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDefined What?

Risk Transfer

Public Playground

Unionized Losses

Nowhere to Hide

Houston and Deadlines

“Companies are doing everything they can to get rid of pension plans, and they will succeed.”

– Ben Stein

“Lady Madonna, children at your feet

Wonder how you manage to make ends meet

Who finds the money when you pay the rent?

Did you think that money was heaven sent?”

– “Lady Madonna,” The Beatles

There was once a time when many American workers had a simple formula for retirement: You stayed with a large business for many years, possibly your whole career. Then at a predetermined age you gratefully accepted a gold watch and a monthly check for the rest of your life. Off you went into the sunset.

That happy outcome was probably never as available as we think. Maybe it was relatively common for the first few decades after World War II. Many of my Baby Boomer peers think a secure retirement should be normal because it’s what we saw in our formative years. In the early 1980s, about 60% of companies had defined-benefit plans. Today it’s about 4% (source: money.CNN). But today defined-benefit plans have ceased to be normal in the larger scheme of things. We witnessed an aberration, a historical anomaly that grew out of particularly favorable circumstances.

Circumstances change. Such pensions are all but gone from US private-sector employers. They’re still common in government, particularly state and local governments; and they are increasingly problematic. They are another source of angst for retirees, government workers who want to retire someday, and the taxpayers and bond investors who finance those pensions. Today, in what will be the first of at least two and possibly more letters focusing on pensions, we’ll begin to examine that angst in more detail. The mounting problems of US and European pension systems are massive on a scale that is nearly incomprehensible.

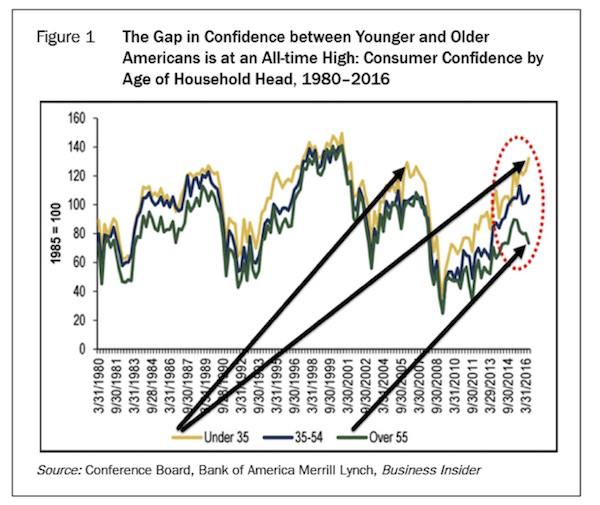

I came across a chart that clearly points to the growing concern of those who are either approaching retirement or already retired. This is from the October 2016 Gloom, Boom & Doom Report from my friend and 2017 SIC speaker Marc Faber. The gap in confidence between younger and older Americans is at an all-time high, after being minimal for many years. A survey by the Insured Retirement Institute last year noted that only 24% of Baby Boomer respondents were confident they would have enough money to last through their lifetimes, down from 37% in 2011. This is the case even after a most remarkable bull market run in the ensuing years.

Even though the equity market has more than recovered, the compounding effect that everyone expected for their pension funds and retirement plans didn’t happen as expected. If the money isn’t there, it can’t compound. If your plan lost 40% in the Great Recession, getting back to even in the ensuing years did not make up for the lost money that was theoretically supposed to come from that 40% compounding at 8% a year. And, as I highlighted in last week’s letter, the prospects for compounding at 8% or even 5% in the next 10 years are not very good. Thus the chart above.

And speaking of Marc Faber’s joining us at the conference; let me again invite you to come to Orlando for my Strategic Investment Conference, May 22–25. I have assembled an all-star lineup of financial and geopolitical analysts who will help us look at what is likely coming our way in the next few years. Then we’ll spend the final part of the conference examining various pathways for the next 10 years and what we have to do to navigate them successfully. There is truly no other conference like this anywhere. I’m continually told by people who attend the Strategic Investment Conference that it’s the best investment conference they’ve ever been to. You can find out how to register here.

Defined-benefit plans are generally the old-style pensions that came with a gold watch and guaranteed you some level of benefit for the rest of your life. Your employer would invest part of your compensation in the plan, based on some formula. In some cases, you, the worker, might have added more money to the pot. But regardless, at retirement your employer was obligated to send you a defined benefit each month or quarter – usually a fixed-dollar amount, sometimes with periodic cost-of-living adjustments.

(Note: There are defined-benefit plans that small, closely held employers such as myself or doctors/dentists can create for themselves and their employees that have significant retirement planning benefits but that function more like defined-contribution plans. For the purposes of this letter we’re going to focus on the more or less conventional types of plans rather than the multitudes of retirement plans that creative accountants and businesses have developed.)

Once your benefit was defined in this way, your employer was on the hook to continue paying under the agreed-upon terms. DB beneficiaries had no control over investment decisions. All they had to do was cash the checks. Employers took all the risk.

This arrangement works fine as long as you assume a few things. First, that your employer will invest the DB plan’s assets prudently. Second, that your employer continues to exist and remains able to make up any shortfalls in the plan’s liabilities.

DB plans work pretty well if those two things happen. It’s simple math for actuaries to estimate future liabilities based on life expectancies. They are uncannily accurate if the group is large enough. So the plan sponsor knows how much cash it needs to have on hand at certain future dates. It can then invest the plan assets in securities, usually bonds, calibrated to reach maturity in the right amounts at the right times.

That all sounds very simple, and it was, but the once-common scheme ran into trouble for reasons we will discuss below. First, though, let’s contrast defined-benefit plans with the other category, defined-contribution (DC).

DC plans are what most workers have now, if they have a retirement plan at all. The 401(k) is a kind of defined-contribution plan (as are various types of IRAs/Keogh/SEP plans, etc.). They are called that because regulations govern who puts money into the plan, and how much. Typically, it’s you and your employer. Your employer also has to give you some reasonable investment options, but it’s up to you to use them wisely. Whether there is anything left to withdraw when you retire is mostly up to you. Good luck.

Which type of plan is better? The more salient question is, which is better for whom? Both have their advantages. People like feeling they have some control over their future, but they also like certainty. Companies, on the other hand, like being able to transfer risk off their balance sheets. DC plans let employers shuck the risk.

The rub, of course, is that abundant evidence now shows that most workers are not able to invest their 401(k) assets effectively. That reality explains some of the retirement angst we discussed two weeks ago. But DB plans are no bed of roses, either, particularly when you put elected officials in charge of them and make unionized government workers their beneficiaries.

Defined-benefit plans have issues going way back. The Studebaker Motor Company had such a plan when it began shutting down in 1963. The plan turned out to be deeply underfunded and unable to meet its pension obligations. Thousands of workers received only a small fraction of what they had been promised, and thousands more received zero.

That failure kicked off several years of investigations and controversy that eventually led to the law called ERISA: the Employee Retirement Income Security Act of 1974. It set standards for private-sector pension plans and defined their tax benefits under federal law.

Important point: Neither ERISA nor any other law requires employers to offer any kind of retirement or pension plan; it just sets standards for those who do. Those standards have turned into something of a mess, frankly. The IRS, Labor Department, and assorted other agencies all have their own pieces of the regulatory pie. It is no wonder that many smaller companies don’t have retirement plans. Simply doing the paperwork is a big job.

That aside, ERISA succeeded in bringing order to previously inconsistent practices. Workers gained some protections that hadn’t existed before, and employers had legal certainty about plan administration. ERISA also created the Pension Benefit Guaranty Corporation (PBGC) to insure pension plans from default and malfeasance.

Many experts believe the PBGC will run out of money in as little as 10 years at its current funding levels. The PBGC is not taxpayer-funded (yet) but exists as a classical insurance fund into which each retirement plan pays roughly $27 per year per covered employee. That figure would need to increase to $156 per year per person just to give the PBGC a 90% chance of staying solvent over the next 20 years.

And if your plan goes bankrupt and you fall into the gentle hands of the PBGC, your pension funding is likely to be cut by 50% or more. Plans that were at one point quite generous could see their beneficiaries lose as much as 75–80% of their previous monthly payouts.

ERISA was all to the good, but it couldn’t cure the biggest headache: the growing amount of money that companies had to to contribute to their plans to keep them fully funded. Plans that covered retiree health benefits had an additional headache trying to project future healthcare costs. Yes, that was a big deal even back in the 1970s.

In 1980, a benefits expert named Ted Benna discovered the 401(k). Yes, he literally discovered it in changes to the Internal Revenue Code that had become law two years earlier. No one set out to create the kind of plans we now recognize as 401(k)s; Benna just looked at the new law and realized it would allow such a thing. That’s where we got the defined-contribution plan.

The initial idea was that the 401(k) would be a supplement to an employer’s DB plan, but employers soon realized that it could also be a replacement. That was an attractive option for many companies, so they began dropping their DB plans and instead expanded their 401(k) contributions.

Business owners will understand this well. I’ve been there, too. You have enough headaches as it is. Having the benefits manager come around at the end of a year when the market had underperformed, telling you to write an additional giant check to the DB plan, was not fun. With a 401(k), in contrast, you could add a little match to everyone’s checks on paydays and be done with it. No one would pop up years later and tell you it wasn’t enough. That some employees liked the idea of having control over their retirement accounts was even better.

DB plans got even less compelling when Alan Greenspan began pushing interest rates down ahead of Y2K. Lower rates meant employers had to pitch in more cash to keep the plans funded at the necessary level. Or, they had to take on additional investment risk and be ready to make up any losses from the company’s resources. None of that is attractive to most business owners. Now DB plans are all but unknown in the private sector, the main exceptions being union-run plans and those run by one-person professional corporations like physicians and lawyers.

Note carefully: The risks and worries associated with retirement plan funding have not disappeared. They have simply been dispersed from a small number of employers to a much larger number of employees. As we discussed earlier, very few of the latter are in a comfortable position. I don’t mean to be flippant here, but it’s true: If DC plan owners aren’t worried, they should be. The days of retiring with a gold watch and a guaranteed monthly check are gone.

ERISA applies only to private-sector employers. Government entities need not comply with ERISA’s many requirements, which is good because many of them don’t. They do, however, have massive retirement obligations to their retirees and workers that simple math says will land them in some form of default. The promises are too generous, and the resources to meet them are too scarce.

The really frustrating part is that this impending crunch was completely predictable, given what we know of politics in this country. Elected officials make extravagant promises to attract votes or contributions. But everything takes time in government, so politicians just delay making changes long enough that everyone forgets or finds other things to worry about.

Pension promises aren’t like campaign promises to build new parks or sewers; Governments can’t forget pension obligations. Pension plans are not like other, more general public services. They involve specific amounts of cash owed to specific people on specific dates. Those dates will arrive, and the cash has to be there. State and local governments can’t run endless deficits the way the federal government does.

That’s all obvious; yet, for some reason, two things happened in recent decades:

State and local politicians kept raising pension benefits.

State and local workers believed the promises.

In fairness, we can’t expect city council members and firefighters to be financial experts. But they have access to experts. The unions that negotiate most public pension contracts have their own lawyers, accountants, and actuaries. They should know whether they are being offered unrealistic projections and promises. And elected officials likewise have expert counsel, so they should know, too. So I’m not sure who is more at fault.

By the way, I have a great deal of respect for the people who keep our cities and states running. Those who protect citizens from harm or otherwise provide public services deserve fair wages and benefits. Pensions are part of that. However, we can’t make something from nothing.

One problem is that accounting rules permit governments to do things private companies can’t. They calculate contributions to their defined-benefit plans in, shall we say, aggressive ways that do not serve anyone well. And, they can shop around for consultants who will tell them what they want to hear. What they want to hear is that they can get away with adding less to the pension fund so they can spend more on shiny new buildings or just fix the roads and keep up with normal city services that make them look productive.

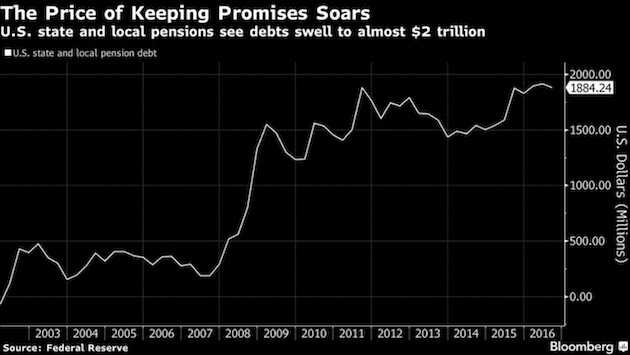

Here we see how state and local pension costs have soared in the last decade. Total unfunded liabilities amounted to only $292 billion in 2007. They have more than quintupled since then, to $1.9 trillion. That’s due to a combination of extravagant promises, poor investment results, and failure to contribute enough cash to the plans. Danielle reels off some startling numbers:

Federal Reserve data show that in 1952, the average public pension had 96 percent of its portfolio invested in bonds and cash equivalents. Assets matched future liabilities. But a loosening of state laws in the 1980s opened the door to riskier investments. In 1992, fixed income and cash had fallen to an average of 47 percent of holdings. By 2016, these safe investments had declined to 27 percent.

It’s no coincidence that pensions’ flight from safety has coincided with the drop in interest rates. That said, unlike their private peers, public pensions discount their liabilities using the rate of returns they assume their overall portfolio will generate. In fiscal 2016, which ended June 30th, the average return for public pensions was somewhere in the neighborhood of 1.5 percent.

Corporations’ accounting rules dictate the use of more realistic bond yields to discount their pensions’ future liabilities. Put differently, companies have been forced to set aside something closer to what it will really cost to service their obligations as opposed to the fantasy figures allowed among public pensions.

The situation is actually far worse than the chart shows. The $1.9 trillion in liabilities presumes that the plans will earn far more over time than the 1.5% return they actually made in 2016. Danielle says unfunded liabilities are as much as $6 trillion by some estimates.

Anytime we see a liability, the unspoken assumption is that someone is liable. Who is liable for public pension obligations? Probably you, depending where you live or own property. State and local governments’ prime asset is the ability to tax their residents. We are financially responsible for the poor and/or self-interested decisions of the politicians we elect. That’s one reason we ought to pay far more attention to local elections than most of us do. Congress and the White House matter a great deal – but so do state legislatures, school boards, and city councils.

When we have a significant bear market during the next recession (that is not an if but rather a when), that $6 trillion figure will balloon to double that amount or more. And remember, those are state and local obligations that must be paid from state and local tax revenues. Paying them would require tax increases for many municipalities and would more than double current tax rates.

Sound incredible? My own city of Dallas, whose Police and Fire Pension System was advertised as solvent just a few years ago, is now so deep in the hole that it would take almost a doubling of city taxes to plug the gap. Note that I bought my Dallas apartment after that news was announced. I was not pleased when I read that headline. Such an increase would make my taxes cost more than my mortgage. Can you say taxpayer revolt? Houston is another city with such problems.

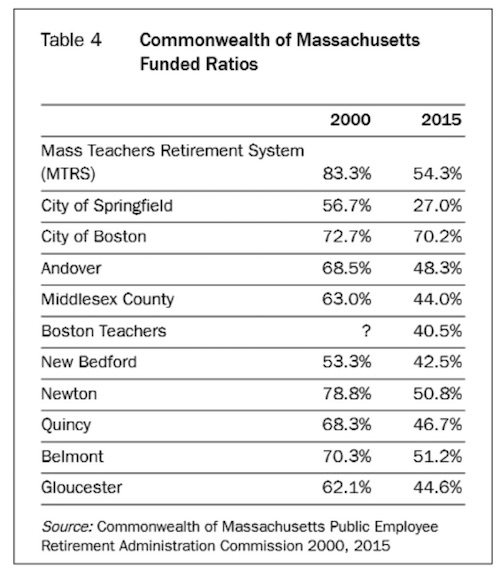

Nationwide, state and municipal spending has risen from $730 billion in 1990 to $2.4 trillion in 2015. And yet the amount of money used to fund pensions has risen only a fraction of the amount that other spending has. The financial problems of Illinois and many California cities are well known. Let’s turn to a chart listing some of the problem areas in the state of Massachusetts:

(Note that most Massachusetts government workers are not eligible for Social Security. This is going to be a serious tragedy when push finally comes to shove.)

It is almost actuarially impossible for pension funds that are less than 50% funded to catch up without massive tax hikes that are implemented solely to allow increases in pension payments but that also result in reductions in services, not only for retirees but for the general public as well. Those pension-funding levels are going to be further eroded during the next recession because more and more cities and states are increasing their equity exposure, and low interest rates are not helping matters.

We have here the proverbial irresistible force/immoveable object quandary. Government agencies signed contracts guaranteeing retirement benefits to their workers. The workers did their jobs, many for decades, trusting that the promises were solid. Now we see that they often weren’t.

It’s hard to imagine good outcomes here. Retirees want what their contracts promised, but the money just isn’t there. Governments have little recourse but to raise taxes, but the taxpayers aren’t captives. Higher property taxes will make them move elsewhere. Higher sales taxes will make them shop elsewhere.

My good friend Marc Faber generously let me use one of his newsletters in Outside the Box last week. In discussing household wealth, he notes that while the nation’s $22 trillion in pension fund assets is a main component of household wealth, much of it may be illusory. The illusion is slowly being exposed, and not just with regard to public-employee pensions. Union plans are in trouble, too. Marc explains with a February 2017 New York Daily News story.

Narvaez, 77, got a union certificate upon retirement in 2003 that guaranteed him a lifetime pension of $3,479 a month.

The former short-haul trucker – who carried local freight around the city – started hearing talk in 2008 of sinking finances in his union’s pension fund.

But the monthly checks still came – including a bonus “13th check” mailed from the union without fail every Dec. 15.

Then Narvaez, like 4,000 other retired Teamster truckers, got a letter from Local 707 in February of last year.

It said monthly pensions had to be slashed by more than a third. It was an emergency move to try to keep the dying fund solvent. That dropped Narvaez from nearly $3,500 to about $2,000.

“They said they were running out of money, that there could be no more in the pension fund, so we had to take the cut,” said Narvaez, whose wife was recently diagnosed with cancer.

The stopgap measure didn’t work – and after years of dangling over the precipice, Local 707’s pension fund fell off the financial cliff this month. With no money left, it turned to Pension Benefit Guaranty Corp., a government insurance company that covers pensions.

Pension Benefit Guaranty Corp. picked up Local 707’s retiree payouts – but the maximum benefit it gives a year is roughly $12,000, for workers who racked up at least 30 years. For those with less time on the job, the payouts are smaller.

Narvaez now gets $1,170 a month – before taxes.

This is stunning. The union worker they mention went from a $3,479 monthly benefit, supposedly guaranteed for life, to $1,170 a month. That’s a 66% pay cut. Worse, it seems to have happened with almost no warning, to a man in his late 70s with a cancer-stricken wife. What an awful situation – and it will be an increasingly common one for anyone depending on a union pension. The story quotes one union pension lawyer:

“This is a quiet crisis, but it’s very real. There are currently 200 other plans on track for insolvency – that’s going to affect anywhere from 1.5 to 2 million people,” said Nyhan. “The prognosis is bleak minus some new legislative help.”

I am sorry to disappoint Mr. Nyhan, but “legislative help” is not on the way. Legislatures have their own pension headaches. So he’s right that the prognosis is bleak. PBGC doesn’t have infinite resources. The only answer is some combination of benefit cuts for current retirees and higher contributions from current workers.

That $156 annual per-worker hike that I mentioned above for the PBGC? As more and more companies and governments abandon their defined-benefit plans, there will be fewer and fewer people to make those contributions, which means that future contributions to the PBGC will potentially need to be much higher still.

So we have seen that both public employees and union workers are right to worry about their pensions. We saw in part 3 of this series that millions more have no significant retirement savings. What about private-sector pensions? As noted, defined-benefit plans are disappearing, but many companies still have legacy plans covering current retirees and those approaching retirement. Marc Faber is not optimistic for them:

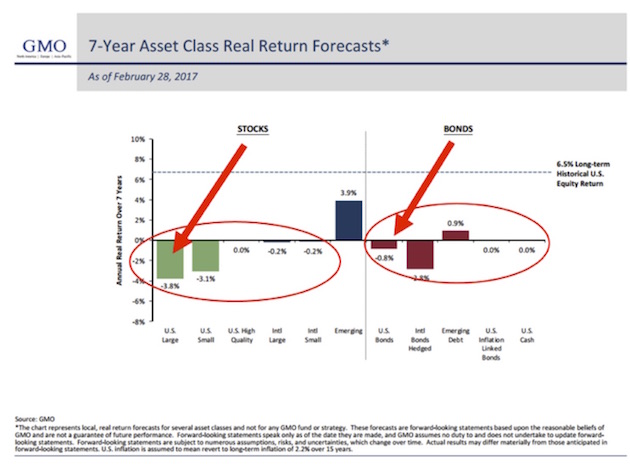

So, whereas prior to the 2008/2009 crisis S&P 1500 companies were fully funded, today funding has dropped below 80% (see Figure 7 of the October 2016 GBD report). I also noted that I found the deteriorating funding levels of pension funds remarkable because, post-March 2009 (S&P 500 at 666), stocks around the world rebounded strongly and many markets (including the US stock market) made new highs. Furthermore, government bonds were rallying strongly after 2006 as interest rates continued to decline. My point was that if, despite truly mouth-watering returns of financial assets over the last ten years, unfunded liabilities have increased, what will happen once these returns diminish or disappear completely? After all, it’s almost certain that the returns of pension funds (as well as of other financial institutions) will diminish given the current level of interest rates and the lofty US stock market valuations.

What if returns over the next seven years look like these projections from Jeremy Grantham of GMO (whose accuracy correlation has been running well north of 95%):

The deeper you look, the worse this pension situation gets. Angst is a perfectly reasonable response for anyone who is retired or thinking about retiring in the next decade. People don’t have sufficient IRA or 401(k) savings; Social Security will be of limited help; defined-benefit pensions are unlikely to be as generous as advertised; and healthcare costs keep climbing. All of the above will keep taxes rising, too, even as the economy remains mired in slow-growth mode at best or enters a long-overdue recession.

I want to end this letter on a positive note. Can we see any glimmers of hope? Some, yes. As I noted last week, one answer for older workers is to work longer and delay retirement. That gives you more years to save and fewer years to consume your nest egg. It doesn’t have to be drudgery if you plan ahead and design your encore career strategically.

Finally, someone responded to part 3 of this series by pointing out that the Baby Boomer generation is still set to receive trillions in assets held by their still-living parents. That could help. The oldest boomers are now 72, which means their parents are likely in their 90s.

That said, if your retirement plan consists of waiting for your parents to die and leave you their house, you are still in a very risky position. For one thing, how much is the house really worth? How much will it be worth as more people like you try to sell houses like that one? Who will buy them?

I talked in part 3 about our tendency to deal with immediate needs first. So many other things seem like higher priorities than retirement planning and saving. What do you do?

Theodore Roosevelt may have had the best answer: “Do what you can, with what you have, where you are.” Angst frequently paralyzes us. Don’t let it. Maybe you can’t do everything it takes, but you can do some of it. Start there.

I will have a quick daytrip to Houston next week, but my calendar looks amazingly clear for almost a month, except for a flurry of conference calls. The next big event seems to be the Strategic Investment Conference May 22–25! You really should plan on joining me there.

Being at home for a while is good, because I have so many deadlines and so much research and reading to do that I really need some time to catch up. I glance at the inbox on my computer, and I find that I have achieved a personal all-time high number of unanswered messages at 602 – which is not exactly something I should be proud of. I probably owe a bunch of you responses. Hopefully I will get to them in the coming weeks. Plus, I have a number of deadlines, both business and writing, that are looming in the next month, so not traveling might actually enable me to meet some of them.

In my defense, I did mostly unplug while I was at the Masters (which, if you are a golfer, is as awesome as you think it would be). And this year’s final day shoot-out was just the stuff of legends. What a great Masters to attend! It was really fun to watch Sergio against one of the greatest young golfers in a head-to-head battle. That, and I had some of the greatest hosts you could possibly want to have. They asked me not to mention their names, but they know they are, and Shane and I are thoroughly grateful.

And then I ended up spending an extra day in Florida, delving into the future of biotechnological research and aging. Things seem to be happening a lot faster than I expected just a few years ago. Or maybe I’m thinking it was just a few years ago when I last caught up with this field, and it was actually more like 10. In any event, I’m convinced that if you are younger than 55, you really do need to plan to work longer than you expected to. And those of us who are older need to take better care of ourselves so that we have a chance for some of these new developments to actually make a difference for us.

When I heard Ray Kurzweil say some 15 years ago that it was his goal to live long enough to live forever, I sighed. Now, I am no longer sighing. I am actively planning how to go about doing that very thing. No, I don’t want to be a 105-year-old shriveled up ghoul, barely able to move about. The promise that induced tissue regeneration seemingly holds for reversing the effects of old age within my lifetime is astonishing, and what was impossible now seems potentially doable. There still a long way to go, but there are researchers who believe they can see a path where none existed before.

So for now, let’s hope that some of the true antiaging drugs that are in the labs actually turn out to be useful. But there are some things we know now: A healthy diet, working out and getting plenty of aerobic exercise, taking the medicines that we know are helpful (like blood pressure medicine), keeping mentally active and involved, and maintaining healthy relationships will go a long way to increasing our life and health spans.

There’s nothing you can do about accidents, genetic diseases, and so forth. Yet. But I just hope that I can be writing this letter for a very long time and that you will be with me as we figure out how to manage an ever-changing and ever-more-interesting world.

Have a great week and make it your Easter resolution to get into the gym more.

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All