If Trump Gets Taxes and Infrastructure, Who Pays, and What Does it Mean for Stocks?

With the dissolution of health care legislation barely final, murmurers out of Washington seem to suggest tax reform/cuts and infrastructure may be tackled in tandem in a way that attracts bipartisan support. If it comes to pass, it would go a long way in meeting the market’s expectations for pro-growth policies from the new administration. But the question of which stock prices will benefit the most may come down to who foots the bill.

Both tax reform/cuts and infrastructure suggest at least the likelihood of higher budget deficits. The republican leadership seems hard set on making any new policy revenue neutral, but the need for bipartisan support may water down that requirement. Indeed, the main idea to raise revenue on the tax side, the border adjustable tax (BAT), is unpopular on both sides of the isle, and the left are in opposition to tax credits as a means to finance an infrastructure buildout. That leaves either 1) tax and infrastructure policies that underwhelm markets or 2) tax and infrastructure policies that meet market expectations, but raise the budget deficit. With option 2 seeming more likely by the day, let’s take a quick look at who may be in a position to finance a higher budged deficit, and the knock on effects.

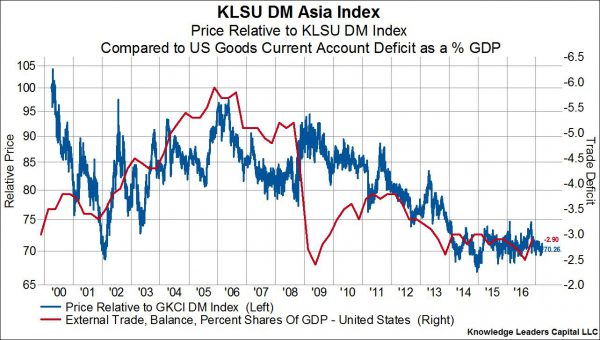

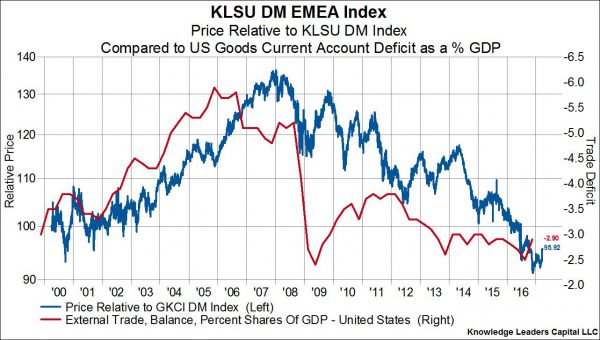

The math of financing government dissaving (budget deficits) is really pretty simple: it must be financed by an excess of savings from the domestic private sector (US companies or households), by the central bank, or by foreigners. Right away we can eliminate option 2 as the source of any financing of higher budget deficits since the Fed is on a tightening path. So this leaves the source of financing as either the domestic private sector or foreigners.

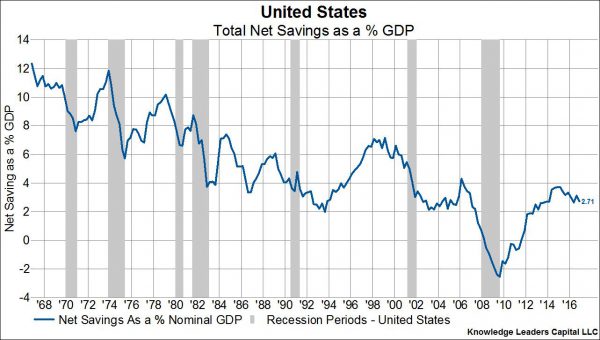

In the first chart below we show the net savings position of the US. Combined government dissavings plus corporate and household sector savings yields just 2.7% of GDP, which is near the lowest level of the last 50 years outside of 2008-2009.

Simply put, there is not the combined national savings necessary to finance a budget expansion, or a corporate capex expansion for that matter. This leaves it to foreign capital to do the heavy lifting. An influx of foreign capital takes the form of a widening current account deficit, which by the way is the same thing as a widening trade deficit. What is the impact of widening current account/trade deficit? The outperformance of foreign vs domestic stocks.