As the first quarter nears its end there is some debate as to where Q1 GDP growth will come in. As recently as yesterday the Atlanta Fed GDPNow estimate had GDP growth of .9% and this morning the NY Fed’s Nowcast is expecting 2.8%. Highlighting the disparity, the upper bound of the Atlanta Fed’s GDPNow is below NY Fed’s Nowcast. Needless to say, differences of this magnitude are quite odd when it comes to forecasting a highly studied and highly predictable series. The US GDP is not Snapchat’s revenue after all.

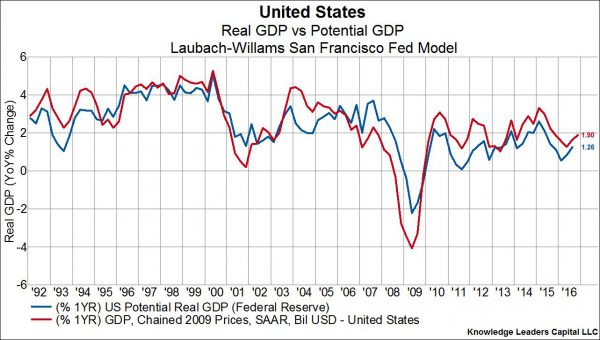

But does this even matter? We don’t overemphasize soft data like GDP growth in our analysis of macroeconomic happenings, but slowing to an annualized rate of .9% is a lot different from accelerating to a rate of 2.8%, especially when the Fed just raised rates. Tightening into a weakening economy could be much worse than tightening into an accelerating or already overheated one. We suspect Janet Yellen’s remarks about a nicely growing economy reflect a view that, if Q1 GDP were to come in near the Atlanta Fed’s number it would be an aberration, and that trend growth still remains above potential. Indeed, the Fed’s own model of the output gap (which is also the subject of some debate) shows that actual trend GDP is running 1.3% above potential GDP. So we can infer that the Fed’s actions this week imply a belief that, despite a very broad range of estimates for Q1 growth, trend GDP growth remains somewhere near 2.5% while potential GDP gorwth remains closer to 1.2%. Regardless of how bizarre it sounds, if the US economy is currently only built to run at 1.2% and we’re running it at 2.5%, it is running faster than it should and the consequence is higher inflation. This is not our view, it’s the Fed’s, and it’s the logic upon which policy is predicated. So, does Q1 GDP matter? Maybe to us, our readers and anyone on the watch for potential policy mistakes, but not to the Fed. Charts of the Fed’s output gap measure below.