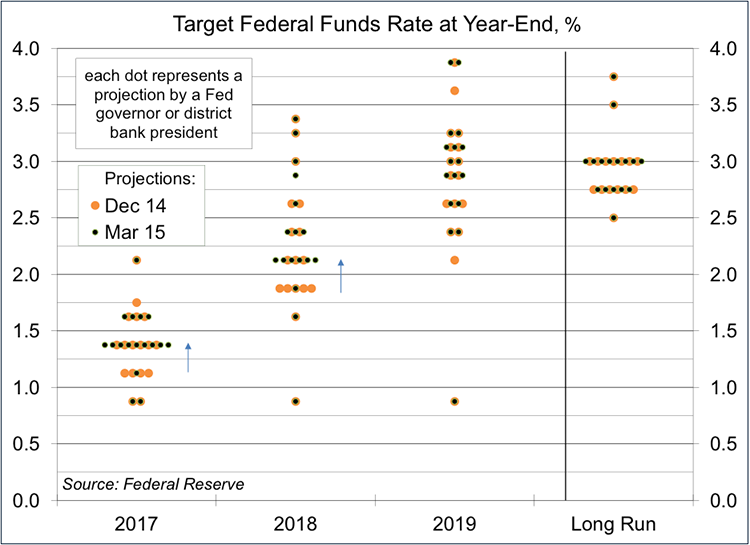

“The median projection for the federal funds rate is 1.4 percent at the end of this year, 2.1 percent at the end of next year, and 3 percent at the end of 2019, in line with its estimated longer-run value. Compared with the projections made in December, the median path for the federal funds rate is essentially unchanged.” – Fed Chair Janet Yellen (March 15)

The Fed’s outlook on the economy hasn’t changed much since December. In turn, policy expectations are largely the same as well. Officials are comfortable enough in their outlooks to continue gradually normalizing monetary policy, but they don’t see enough pressure to move more rapidly.

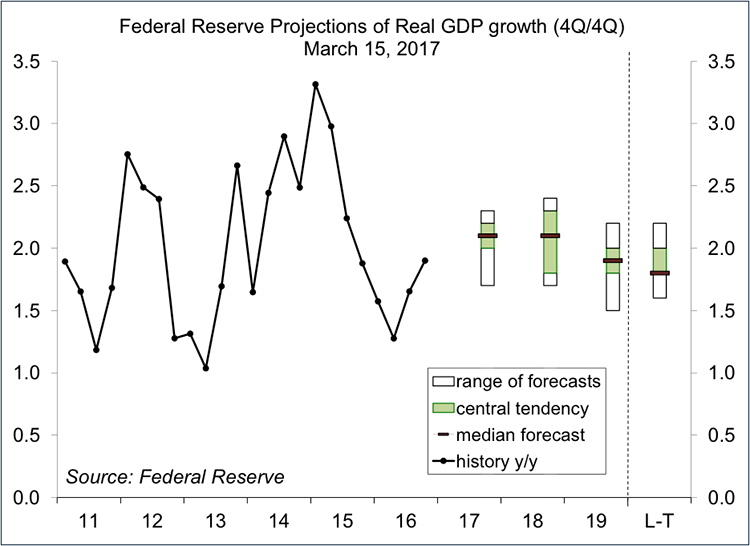

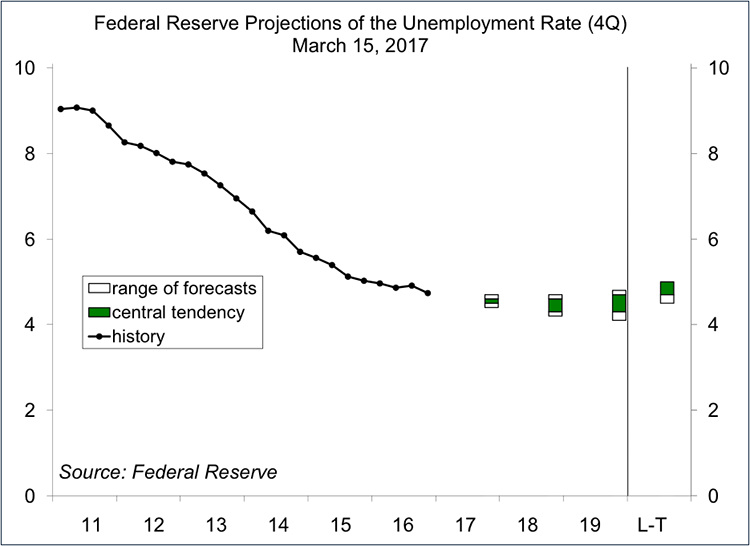

Officials continue to expect GDP growth of around 2% over the course of this year and over the next two years. That’s largely because we are approaching full employment. While increased business optimism may fuel a pickup in the pace of business fixed investment in the near term, the consumer is the driving force. Jobs and wage growth will be the key drivers.

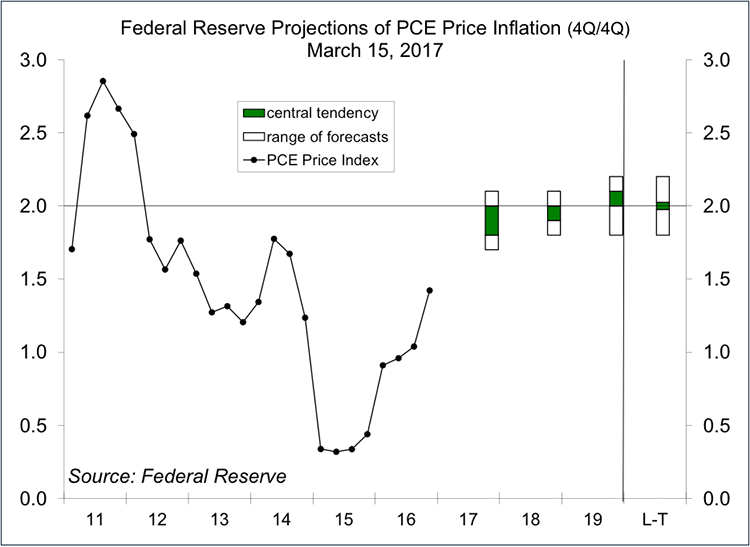

A tighter job market should lead to increased wage growth and there have been some moderate signs of pressure in prices of raw materials. However, the outlook for consumer price inflation is still moderate. Obviously, the Fed could raise rates a little faster if inflation pressures pick up more forcefully in the months ahead, but there’s little sign of that currently.

Over the last several quarters, financial market participants have placed far too much emphasis on the dots in the dot plot (these are the projections of individual Fed officials of the appropriate year-end federal funds rate). There’s a fair amount of dispersion among the dots and there’s a lot of uncertainty surrounding each of the dots. Yet, here was Fed Chair Yellen emphasizing the median number of rate increases. Go figure.

With the FOMC meeting behind us, we can get back to the larger conflict. That is, investors are optimistic that policies out of Washington will fuel a much faster pace of growth in the economy. In contrast, the Fed (and most economists) are expecting labor market constraints to limit the pace of the expansion. Something’s going to have to give.

© Raymond James

© Raymond James

Read more commentaries by Raymond James