“Indeed, at our meeting later this month, the Committee will evaluate whether employment and inflation are continuing to evolve in line with our expectations, in which case a further adjustment of the federal funds rate would likely be appropriate.” – Fed Chair Janet Yellen (March 3)

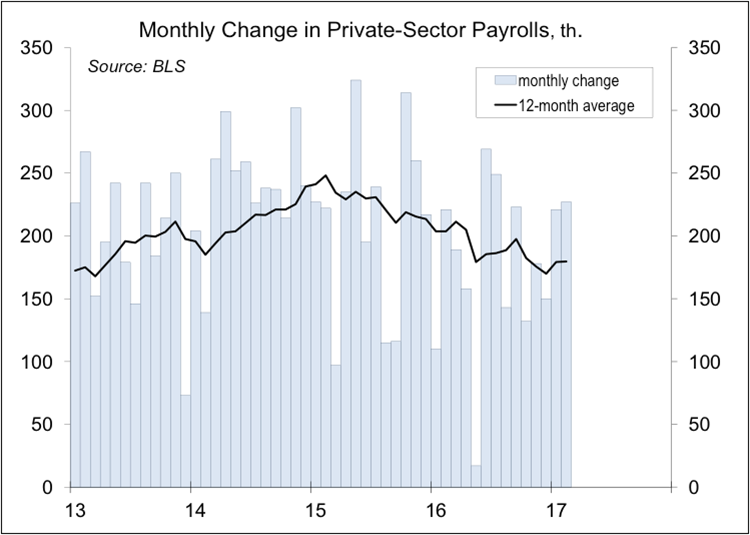

Prior to seasonal adjustment, the U.S. economy added more than a million jobs in February (unadjusted payrolls rose by 831,000 in February 2016 and by 832,000 in February 2015). Mild weather likely played a part and there is the normal statistical uncertainty, making it hard to tell how much of the job gain is due to improved business confidence (weather and statistical noise will wash out over time). However, job growth is still expected to slow as the labor market tightens.

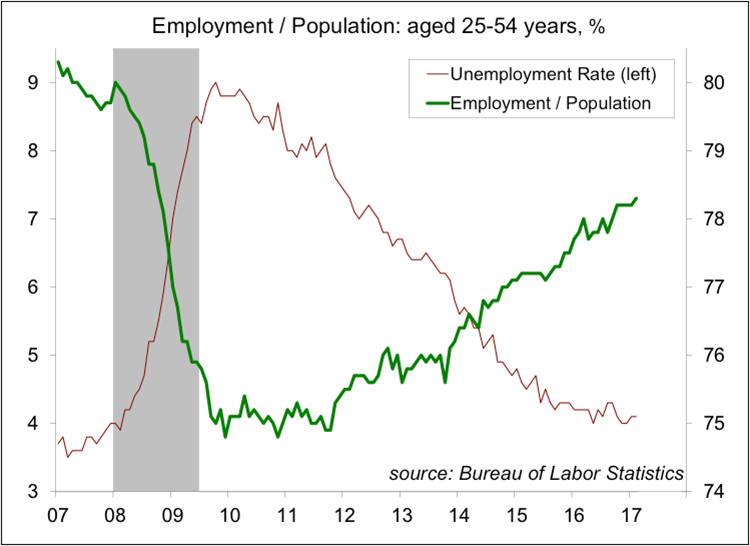

The unemployment rate edged back down to 4.7%, as labor force participation edged higher. The unemployment rate held steady at 4.1% for the key age cohort of 25-54. The employment/population ratio for this group continued to trend higher (not terribly far from the pre-recession level).

A tighter labor market should generate wage pressures. Average hourly earnings rose 0.2% in February (+2.8% y/y). Monthly wage figures are normally choppy, but the underlying trend in the year-over-year pace is only moderately higher. Wage gains should be higher in sectors where employees are more difficult to hire, but results appear mixed. For the three months ending February, average hourly earnings in tech rose 4.0% y/y. Retail rose 1.5% y/y, while leisure and hospitality led the way at 4.2%. Three-month averages can themselves be uneven over time, but the data do not suggest a sharp rise in wages. Of course, benefits also factor into the hiring decisions.

Job market data can be distorted by a number of factors in the early part of the year, but the broad range of indicators and recent anecdotal evidence suggest that, while labor market slack is being reduced, there’s still a fair amount left over from the recession. There’s nothing to indicate that the Fed needs to slam on the brakes at this point, but officials do need to gradually take the foot of the accelerator.

Investors were quick to take away Yellen’s message that the Fed is almost certain to raise short-term interest rates again on March 15. However, investors appear to have missed the other important signal in her March 3 speech on the economic outlook. That is, a number of factors kept the Fed from tightening more aggressively in the last two years – and absent a softening in job market conditions or a slowdown in economic growth, “the process of scaling back accommodation likely will not be as slow as it was in 2015 and 2016.”

Tighter monetary policy need not be a negative for stock market investors. After all, it depends on why the Fed is raising rates. In this case, it is because officials are more confident. There appears to be little danger that the Fed will be choking off growth or causing major disruptions to the global financial system. Still, the pace of tightening is expected to be gradual.

© Raymond James

© Raymond James

Read more commentaries by Raymond James