According to an article in Quartz today, March 9, 2017, marks the 8th birthday of the US bull market which started on March 9, 2009. According to the article, this is the 2nd longest and 4thstrongest bull market in history for the S&P 500. However, before we celebrate too excessively, we should pause and take a look at the S&P 500’s current valuation as a result.

However, before I discuss the S&P 500’s current valuation I think it only proper that I share my views about the stock market in general. I believe it’s very important for investors to focus specifically on what they own rather than the broad markets. Most renowned investors seem to agree that investing is most intelligent when it is most businesslike. Furthermore, they understand that the health and vitality of a specific company is reasonably ascertainable and generally accurate enough to be relied upon.

In contrast the often erratic and mostly irrational daily short-term volatility of stock prices in general is not. Therefore, once I have a solid handle on the intrinsic value of the companies I own, I never sweat the market. I know from a preponderance of evidence that the future rate of change of earnings and dividend growth when purchased at a sound valuation determines my longer-term future returns. That is all I concern myself with and trust it explicitly.

This attitude and opinion is based on my belief that it is a market of stocks rather than a stock market. However, with that said, common sense would indicate it’s harder to find attractive value when the general market is excessively high, as I believe it is today. So even though I do not sweat the market, I am smart enough and prudent enough to be cognizant of its relative valuation.

Moreover, as milestones go this article marks the 10th article that I have written on the S&P 500 since I started writing on Seeking Alpha in 2009. NOTE: You can find my previous articles by going to my profile and clicking on the ticker SPY. Considering that I started writing in the throes of the Great Recession, my previous offerings have been generally bullish. This can be attributed to the fact that I considered the market as represented by the S&P 500 fairly valued up to 2013, which was when I penned my last S&P 500 offering. As I will illustrate later, I considered the S&P 500 continuing to be reasonably valued until the fall of 2013.

However, that changed in August 2013, which partially explains why I haven’t written about the S&P 500 specifically since the beginning of 2013. The rest of my explanation can be attributed to my dear departed mother who taught me that if I didn’t have anything good to say, I shouldn’t say anything at all. But with reverence to my mother’s wishes, I feel I owe it to my readers to point out the excessive valuation I currently see with the S&P 500.

Setting The Stage: Principles Of Investing

As anyone who has been following my work knows by now, I don’t believe it’s possible to forecast stock markets or the economy, at least not with the precise timing that most people expect. As Warren Buffett once said: “The fact that people will be full of greed, fear or folly is predictable. The sequence is not predictable.”

On the other hand, there are rational longer-term expectations that can be relied upon. For example, I believe it is an absolute truth that every recession eventually ends. Whether it lasts 18 months, 11 months or 24 months, etc., doesn’t really matter to investors with a long-term perspective. What does matter is the absolute fact that it will end. Regarding the stock market, every bear market ends with a bull market and vice-versa. As the old adage states, “Wall Street Climbs a Wall of Worry” and that is all you really need to know about timing markets or the economy.

On the other hand, there are other important truths that I will only mention today, each deserving of their own independent post. For example, overvaluation or undervaluation is calculable with reasonable precision using simple and straightforward mathematics. Therefore, overvaluation should always be either avoided or recognized and then treated with extreme caution.

In contrast, I contend that undervaluation should be embraced by investors as risk is reduced and potential returns enlarged. It’s not possible and certainly not necessary to find perfect tops or bottoms. It’s more than enough to be essentially correct; investing is rarely a game of perfect. It’s also enough to know that recessions only happen every so often and always ends within a timeframe that precludes being referred to as the long term. There are other factors and characteristics to think about, but these are the major ones.

Given what has been written in this post thus far brings me to the focal point of the entry. The five or so years following every recession that I have observed in modern times have experienced strong above-average growth of earnings. Since earnings determine market price in the long run, this is vital knowledge. Of course, the reason is simple. Coming off of depressed earnings and business results, comparisons are easier as things return to normalcy. Therefore, above-average growth manifests, as trend line norms return. This is exactly what has happened since the last recession ended in the spring of 2009.

Leaner and meaner, well-run companies exit recessions poised for accelerated earnings growth. With inventories under control and competition lessened, higher margins and increased market share drives earnings upward. For the discerning long-term investor with money to invest low valuations followed by resurging growth offers a great buying opportunity. Consequently, 2009 represented exactly that opportunity which is why I have been writing bullish articles on the S&P 500. As previously mentioned, all things good or bad must someday come to an end. Although I believe it’s impossible to time it perfectly, after such a long bull run caution is certainly now in order.

The S&P 500 Earnings And Price Relationship

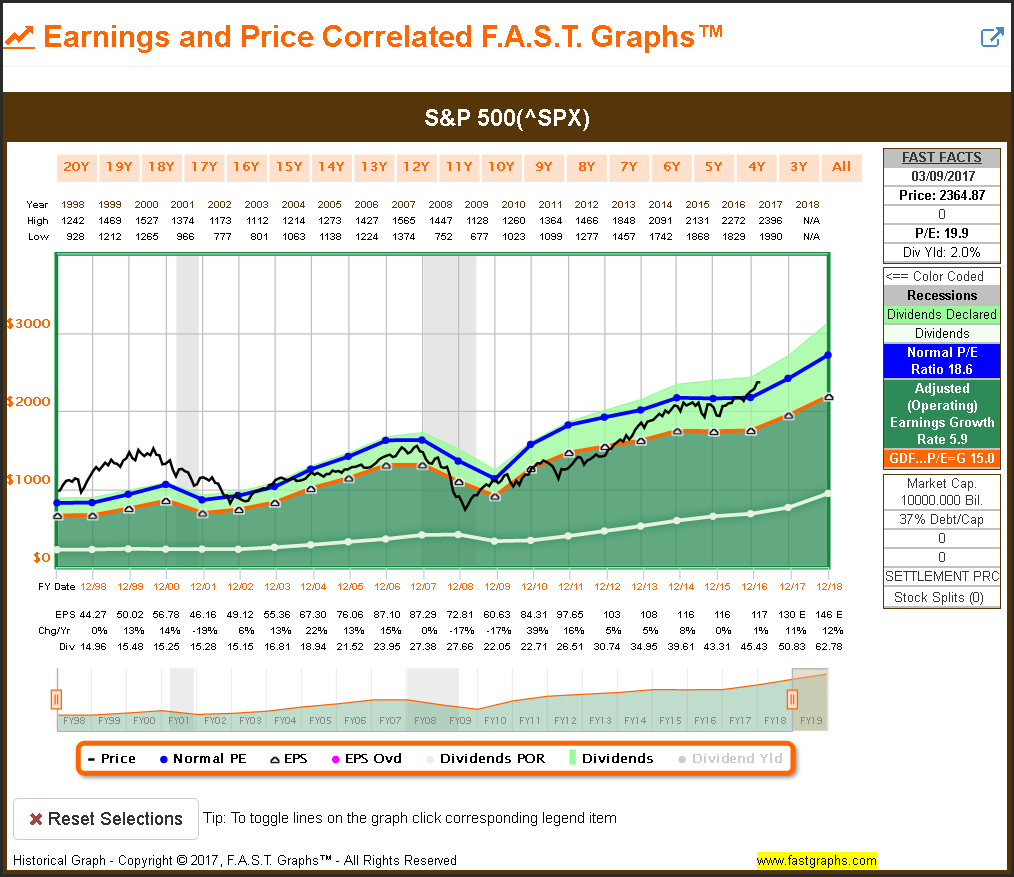

The following earnings and price correlated F.A.S.T. Graphs™ on the S&P 500 clearly illustrates the overvaluation I am writing about. There are two important valuation references that the reader should focus on. The orange line on the graph represents a P/E ratio (earnings multiple) of 15, which I consider a fair and reasonable valuation. The dark blue line represents a normal P/E ratio of 18.6 since 1998.

From these valuation references we can see that stocks as represented by the S&P 500 were at or below the orange line as we came out of the Great Recession and have risen above it since the fall of 2013. But most importantly, as it relates to this article, prices have risen above the higher normal P/E ratio of 18.6 since the beginning of this year.

Bonus Video: A Deeper Analysis of the S&P 500 valuation.

Be Smart: Invest For the Long Term

This article is dedicated to the prudent long-term investor. Long-term oriented investors never assume that their investments will produce instant success. Long-term investors understand that the most reliable way to generate above-average returns is to be a long-term investor in above-average businesses purchased at sound valuation.

In the fall of year 2000, at the height of a bull market, Al Berkeley, then president of the NASDAQ Stock Market, wrote an article in Forbes ASAP Magazine that made a strong and clear distinction between long-term investing and short-term speculation as follows:

“A Trustworthy market does not mean that people will not overpay for stocks. Witness the recent fluctuations in securities. This shows that the market is different things to different people. Three levels of game theory are at play in the market: games of chance, games of skill and games of strategy. The same market, the same stock, the same day, even the same trade, has a different meaning for different players.

Most of us think of the market as a place for investors. Investors, in our vocabulary, look at the fundamental competitive position of a company, buy the stock, and let the management’s good work build value over time. For them, truth plays out over time, often years or decades.

Speculators play a game of skill. They are the so-called momentum players. They know they are playing a fast game, but they consider themselves better, more skilled than the competition. They believe they understand the other fellow’s psychology. The underlying mathematics resembles musical chairs, but they’re confident there will be a chair for them. For speculators, truth plays out over weeks or months, rarely years.

Gamblers play a game of chance. For gamblers, Truth plays out in minutes and hours, maybe a few days.”

My advice, be smart be an investor. In the long run you will be richer for it.

Summary and Conclusions

Common sense would indicate that when investing in stocks, you can’t do what’s popular and expect to make money. When you think about it, you realize that the highest price (valuation) is achieved when the demand is highest. Conversely, the lowest price (valuation) happens when selling is greatest. The real bargains will not be found where everyone else is shopping. To find the best values you have to look where few others are looking.

Unfortunately, because we are by nature social animals, it’s hard for people to venture alone. We seek the comfort and security of groups or crowds. However, let me repeat a statement I offered to clients during the irrational exuberant period of the mid to late ‘90s. The danger with running with the herd is that your ultimate destination is the slaughter house. In truth, it does not take courage to step out alone, it takes smarts. As Warren Buffett said in his October 17, 2008 New York Times article, “Be fearful when others are greedy, and be greedy when others are fearful.” Perhaps there hasn’t been a better time to be fearful in over 8 years.

Furthermore, short-term price volatility is unpredictable and often irrational. Therefore, it’s imperative that decisions be made without imposing a time limit. If you want to succeed owning equities, never invest what you may need in the near future. Business results, primarily profits, drive long-term returns. It takes time for businesses to grow earnings. Give your portfolio the time it needs and deserves. Also, and most importantly, be sure as possible that valuation makes sense. Therefore, and to be clear, I am not suggesting that the S&P 500 will fall in the near future. Instead, I’m simply pointing out that the valuation of the S&P 500 is currently excessive relative to recent historical norms.

Finally, I also contend that there will always be value to be found whether we are in a bear or in a bull market. Of course, finding value towards the end of a strong bull market like we have today becomes very rare and therefore difficult. Consequently, in light of what I’ve written here, my suggestion is to evaluate the valuation of each of your current holdings. If some of your holdings are currently trading at extreme valuations, I believe it would be wise to evaluate the risks associated with holding on. On the other hand, if you own stocks that are still attractively valued, I wouldn’t fear a bear market. This is especially true if the fundamentals of your fairly valued stocks are strong. In short, be analytical rather than reactive. And remember: Running with the Herd Leads You to the Slaughter House!

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.