Weighing the Week Ahead: Will a More Aggressive Fed Derail the Stock Rally?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is light until the Friday employment report. Most of the punditry are still digesting the more aggressive talk in the recent speeches from Fed participants. With many observers expecting a correction and looking for a catalyst, pundits will be asking:

Will a more aggressive Fed derail the rally in stocks?

Last Week

Last week the news was mostly positive, and stocks responded again.

Theme Recap

In my last WTWA I predicted a discussion about whether stock prices had lost touch with reality. That was a good guess. There was plenty of talk about market valuation. Those bearish also questioned the lack of specifics in the Presidential Address to Congress – which had a greater immediate effect that the annual Buffett letter.

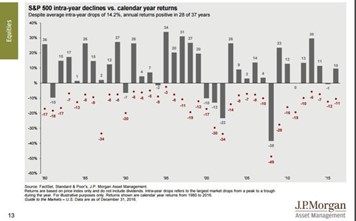

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short via Jill Mislinski. She notes yet another record close based on the week’s gain of 0.67%. We can also see the gap opening after the Presidential Address to Congress.

The rally story is even clearer in this chart, when begins before the election.

Doug has a special knack for pulling together all the relevant information. His charts save more than a thousand words! Read his entire post for several more charts providing long-term perspective, including the size and frequency of drawdowns.

The News

Each week I break down events into good and bad. Often there is an “ugly” and on rare occasion something very positive. My working definition of “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

This week’s news was mostly positive.

The Good

- Durable goods orders increased 1.8% after last month’s decline. Most of the increase was from the volatile transportation sector, but it was still a welcome boost.

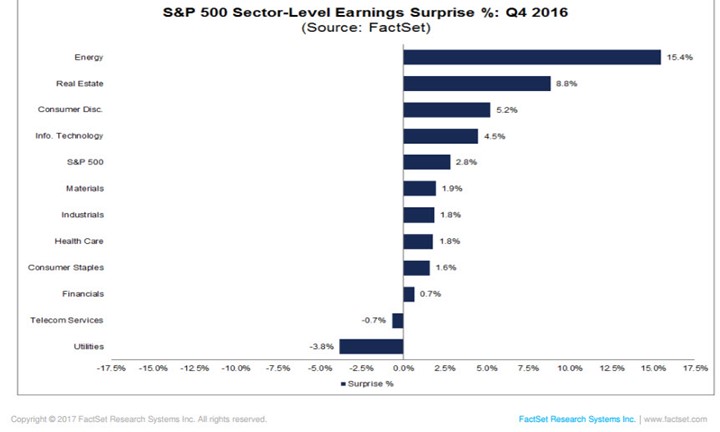

- Earnings news was positive. Brian Gilmartin emphasizes the favorable trend in estimate revisions.FactSet reports that the earnings and revenue beat rates are slightly lower, but outlook is stronger. Here is an interesting chart of surprises by sector.

- Investor sentiment turned more bearish. The AAII reports that sentiment is within historic ranges, but off recent highs. This is unusual given past behavior in a rising market. I score it as “good” since most regard it as a contrary indicator.

- Mortgage delinquency rate falls below 1%, the lowest since June, 2008. (Calculated Risk).

- ISM Non-Manufacturing rose to 57.6 (from 56.5). The employment index also moved higher. February was stronger than January.

- ISM manufacturing increased to 57.7 beating expectations and showing a solid increase over last month’s 56.1. The Chicago regional survey was also very strong.

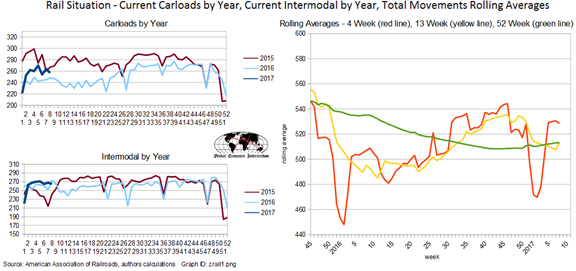

- Rail traffic in February was 4.2% higher than a year ago. Steven Hansen takes the look at the data we have come to expect, including various moving averages and trends. Read the whole post, but this chart captures some key points, especially the improvement over the last two years.

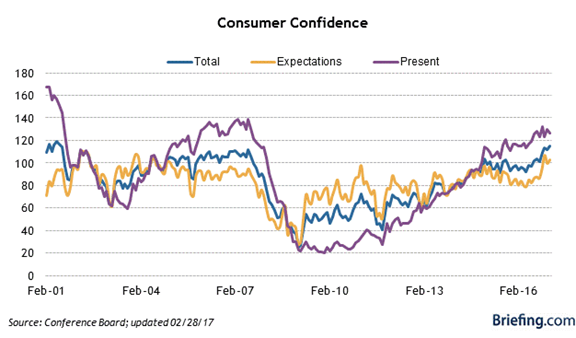

- Consumer confidence spiked to 114.8, a post-recession high. Briefing.com covers this series.

- Initial jobless claims rose slightly on the week, but dropped to the lowest level since 1973 on the widely-followed four-week moving average. (Calculated Risk).

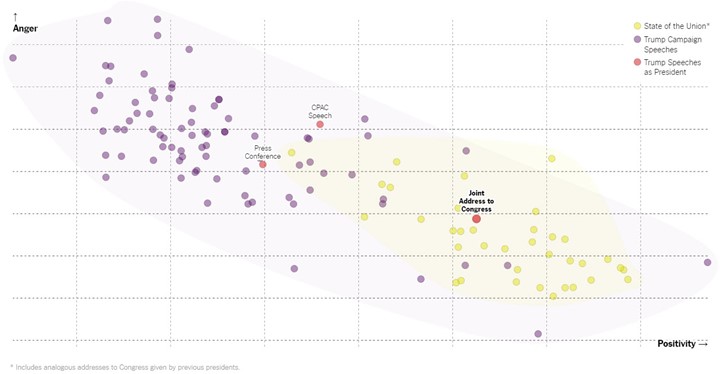

- President Trump’s speech was very well-received. Most preview articles mistakenly emphasized the need for specifics. Commentators right after the speech did the same. My own preview did not provide advice on what to go out and trade right after the speech. Instead, I drew upon experience and the current policy environment to highlight the key element – the potential for compromise. This chart shows the dramatic shift in this Trump presentation, more like SOTU speeches than nearly anything else he has done. (The Upshot)

The Bad

- Construction spending fell 1%.

- Money supply is drifting to the neutral range – possibly even tilting negative. (New Deal Democrat). Despite complaints about Fed policy, this is a possible economic drag.

- Pending home sales fell 2.8% and December was revised lower.

- Debt Limit will be reached in mid-March. Even the extraordinary efforts will be exhausted in September or October. Will this play out any better with a GOP President and Congress? Douglas A. McIntyre has a good story on this issue.

The Ugly

My concern about hacking and threats to the Internet’s weak spots continues. Rick Paulas’s article is not about events from last week, but is just as relevant. Perhaps even more so with the Barron’s cover story on robots.

The article explains that even rather unsophisticated attacks can work on the 6.4 billion Internet of Things devices in use. Little is being done to protect on this front.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. No award this week. Nominations are welcome. Potential award winners can find daily inspiration at several websites!

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

We have a moderate week for economic data, featuring the employment report on Friday.

The “A” List

- Employment situation (F). Despite +/- 100K sampling error and multiple revisions, this is seen as most important data

- ADP private employment (W). Good independent alternative to the BLS numbers

- Initial jobless claims (Th). Not the same time period as the Friday report.

The “B” List

- Trade balance (T). Attracting more interest in the Trump era

- Wholesale inventories (W). Desired or undesired? That is always the question.

- Factory orders (M). January data. Modest gain expected.

-

Crude inventories (Th). Recently showing even more impact on oil prices. Rightly or wrongly, that spills over to stocks.

FedSpeak will be light and earnings season is ending. Employment will be the big story.

Next Week’s Theme

The punditry, especially those who explain the stronger stock market as enthusiasm for Trump policies, is even more amazed than a week ago. To them it seemed that the lack of specifics in Tuesday’s Trump speech should have provided a dose of reality.

Many will now turn to the most common explanation for strong stocks, the ever-popular Fed theory. With several speeches emphasizing that the March FOMC meeting is “in play” for an increase, interest rate markets are adjusting to the probability of three rate hikes in 2017.

Much of the commentary next week will raise the question:

Will a more aggressive Fed spark a stock market correction?

Some might add “finally”!

The question actually has two parts:

- Will the Fed increase rates at a pace greater than expectations?

- Will this lead to a correction?

Friday’s employment report will have special significance for those with these fears. It will be the final and most important piece of evidence for the FOMC decision.

Both questions have a bullish and bearish side.

- An increased pace of Fed rate hikes was the consensus at week’s end. (Bloomberg). Leading Fed observer Prof. Tim Duy’s careful look at the important Dudley speech (before Yellen) was not so decisive.

- Bears invoke the hoary adage, “three steps and a stumble.” (David Rosenberg). As you review the evidence, you might consider the starting point for interest rates, as well as the yield curve. More constructively, Neal Frankle analyzes the frequency (often) and severity (moderate) of corrections.

What does this all mean for investors? As usual, I’ll have a few ideas of my own in today’s “Final Thought”.

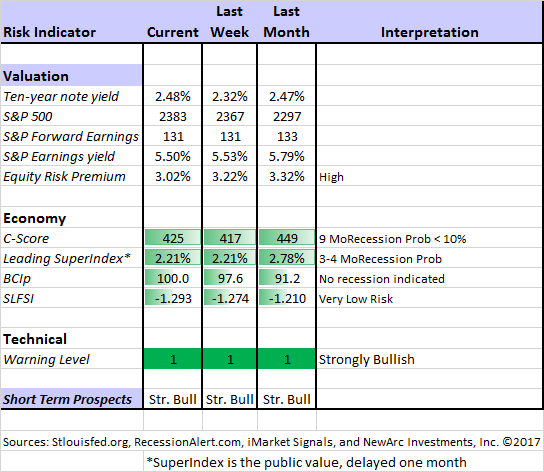

Quant Corner

We follow some regular great sources and the best insights from each week.

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Bob Dieli: The “C Score” which is a weekly estimate of his Enhanced Aggregate Spread (the most accurate real-time recession forecasting method over the last few decades). His subscribers get Monthly reports including both an economic overview of the economy and employment. (see below).

Holmes: Our cautious and clever watchdog, who sniffs out opportunity like a great detective, but emphasizes guarding assets.

RecessionAlert: Many strong quantitative indicators for both economic and market analysis. While we feature his recession analysis, Dwaine also has several interesting approaches to asset allocation. Try out his new public Twitter Feed.

Georg Vrba: The Business Cycle Indicator and much more.Check out his site for an array of interesting methods. Georg regularly analyzes Bob Dieli’s enhanced aggregate spread, considering when it might first give a recession signal. His interpretation suggests the probability creeping higher, but still after nine months.

Brian Gilmartin: Analysis of expected earnings for the overall market as well as coverage of many individual companies. His most recent post notes that the expected growth rate in S&P earnings is now 8.41% — the highest level since October, 2014.

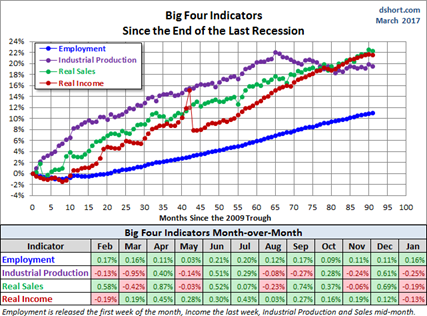

Doug Short: The World Markets Weekend Update (and much more). His Big Four chart is the single best method to monitor the key indicators used by the National Bureau of Economic Research in recession dating.

How to Use WTWA (especially important for new readers)

In this series, I share my preparation for the coming week. I write each post as if I were speaking directly to one of my clients. Most readers can just “listen in.” If you are unhappy with your current investment approach, we will be happy to talk with you. I start with a specific assessment of your personal situation. There is no rush. Each client is different, so I have eight different programs ranging from very conservative bond ladders to very aggressive trading programs. A key question:

Are you preserving wealth, or like most of us, do you need to create more wealth?

Most of my readers are not clients. While I write as if I were speaking personally to one of them, my objective is to help everyone. I provide several free resources. Just write to info at newarc dot com for our current report package. We never share your email address with others, and send only what you seek. (Like you, we hate spam!)

Best Advice for the Week Ahead

The right move often depends on your time horizon. Are you a trader or an investor?

Insight for Traders

We consider both our models and the top sources we follow.

Felix and Holmes

We continue with a strongly bullish market forecast. All our models are now fully invested. The group meets weekly for a discussion they call the “Stock Exchange.” In each post I include a trading theme, ideas from each of our four technical experts, and some rebuttal from a fundamental analyst (usually me, but some noted guests experts are coming). We try to have fun, but there are always fresh ideas. Last week the focus was on trading an overbought market. The week before we considered sector rotation strategies, with a recent example from Oscar.

Top Trading Advice

Morgan Housel draws upon Ed Thorp’s work to discuss the advantages and dangers of trading with a small edge.

I agree. Every busted card-counter starts with the statement: “The deck got really good”.

Brett Steenbarger has so many strong entries that picking a favorite is a challenge. Here is one I especially liked from last week – reading the market’s psychology. Hint: Do not impose your own preconceptions on what is really happening.

In case you were unable to attend Brett’s master class in NY, SMB’s Bella has a summary of key takeaways. I especially like #6. The successful trader finds more than one way to win. Check out the five “inspirations” as well.

Insight for Investors

Investors have a longer time horizon. The best moves frequently involve taking advantage of trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would once again be Warren Buffett’s annual letter to his investors. It is full of wit and humor – and plenty of great insights. Last week I recommended his annual letter to investors. For those who (mistakenly) did not take the time to read it, you can now check out the “Cliff Notes.”

- Methodology and screening expert Marc Gerstein applies Buffett principles. Check out his interesting list emphasizing book value.

- Twenty-eight highlights from Exploring Markets. I especially like this one: When a person with money meets a person with experience, the one with experience ends up with the money and the one with money leaves with experience.

- Ed Yardeni explains why the oft-cited “Buffett Rule” gets complicated when interest rates are so low. It is why Mr. B regards stocks as cheap.

- Gil Weinreich has a list of great quotes with his own comments added.

Stock Ideas

Chuck Carnevale does his typical comprehensive analysis of j2 Global (JCOM). It includes business model analysis, the important stats, education on how to analyze, and much more. Even if this particular stock does not trip your trigger, you will learn from the article.

Our Stock Exchange always has some fresh ideas. There is usually something from four different approaches. Our momentum trading model, Athena, highlighted Principal Financial Group (PFG). You will probably identify with one of the characters, and your questions are welcomed.

Bottom Fishing

There are some high dividend stocks – often a sign of danger. Are these dividends safe?

Frontier Communications (FTR) yields 14%. Stone Fox Capitalanalyzes the risk.

Target (TGT) declined 12% after announcing poor earnings and a weak outlook. Simply Safe Dividends believes that the yield of 4%+ is probably safe, but a significant increase next year is unlikely.

How about Snap?

A fashionable IPO always attracts attention. In the absence of actual earnings data, everyone is free to spin a story. Initial trading was very positive. Does that mean that investors should consider buying it at market prices? (Those who get an allocation at the offering price have already made a bundle – depending upon when they sell).

Valuation guru Prof Aswath Damodaran provides the careful look we would expect from a top expert. While his final range is wide (and includes current prices) the overall conclusion is not promising. If you are attracted to the stock because you like the concept or company, you should look at this post.

MarketWatch reports that most analysts have stock targets below the $17 IPO price.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. If you are a serious investor managing your own account, this is a must-read. Even the more casual long-term investor should make time for a weekly trip on Wednesday. Tadas always has first-rate links for investors in his weekly special edition. As usual, investors will find value in several of them, but my favorite is the discussion of ten things you must know about personal finance. It is important to get fundamental decisions right before launching your investment program.

In a similar personal finance emphasis, Seeking Alpha Editor Gil Weinreich cites the top four savings ideas from BlackRock’s clients.

If you have been struggling with your own decisions, you might want to read my (free) short paper on the top investor pitfalls. It is a good test of whether you can successfully fly solo. Send a request to main at newarc dot com.

Watch out for…

Scam season. One person gets you in the back yard to discuss landscaping, while the other is inside your home, stealing. The IRS does not take payments through credit cards or gift cards. If it seems in the slightest bit suspicious, check it out. The elderly are frequently targeted.

Final Thoughts

Your investment conclusions are strongly influenced by your preconceptions and current position. Last week I had an especially good summary of the two main themes. If it matters, Warren Buffett went on TV the day after I wrote this, expressing a similar opinion about stock valuations.

-

Stock values are attractive

- Emphasis on earnings expectations and forecasts

- Belief in relative valuations – comparing stock expected performance, with bonds, real estate, gold, etc.

- Confidence that a recession is not imminent.

-

Stocks are over-valued

- Emphasis on trailing earnings

- Analysis based partially on 19th century data

- Belief that valuation is absolute. A sector’s value is independent of the alternatives

- Focus on headline risk – uncertainty, world events, etc.

Your choice of world view controls how you interpret fresh news, and your key investment decisions. If you are getting it wrong, you need an epiphany!

The market is rising despite the lack of specifics in the Trump plan and the realization that there will be delays in his proposals – even if he can sell them to Congress. The reason is straightforward:

The economy has been getting better in the post-election period. Dr. Ed Yardeni, declares that The Recession Is Over. He is thinking globally, noting that worldwide improvement cannot be linked to the U.S. election.

Charles Lieberman reviews the entire array of factors, including what to worry about.

Briefing.com’s excellent Big Picture column (worth a paid subscription) explores the possible causal relationships. Here is a key chart.

The Fed rate increases will be consistent with a stronger economy, an environment that implies solid growth in earnings. Scott Grannis explains why higher rates are not a threat in the current market:

It’s very likely we’re still in the early stages of more of the same. Interest rates are going to be rising, probably by more than the market currently expects, because the outlook for the economy is improving and inflation is at the high end of the Fed’s target range, yet interest rates are still relatively low because of the market’s willingness to pay up for safety—and that won’t persist for much longer. Stocks are going to be buoyed by improving earnings and the prospect of stronger economic growth. Interest rates will be moving higher because of stronger growth—higher rates are not yet a threat to growth. The Fed is still a long way from raising rates by enough to threaten growth. If the FOMC hikes rates in two weeks it won’t be a tightening, it will be a sensible reaction to stronger growth and improved confidence.

Worries?

Sure. If the Fed gets behind on inflation and accelerates rate increases, even though the economy is sluggish, it will be an early sign of an impending recession. I am watching this closely, and so should you.

Meanwhile, do not be scared witless (TM OldProf euphemism).

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits