1. President Trump’s Economic Plan Promises 3-4% GDP Growth

2. Manufacturing Has the Best Job-Multiplier & Income Effect

3. Economic Policies Similar to Trump’s Have Worked Before

4. Trump’s Economic Plan vs Obama’s & the Media’s Reaction

5. Productivity Can Rebound if Policy Environment is Right

Overview

President Trump promises that his economic plan, if enacted, will result in 3-4% annual GDP growth. Yet I get the feeling most Americans don’t understand Trump’s economic plan. Maybe that’s because the mainstream media has criticized it at every turn, even though similar plans have jump-started the economy in the past – think Ronald Reagan.

Today we’ll take a closer look at Trump’s economic plan as outlined in a detailed report his team released last fall. Essentially, his economic plan is based on tax cuts for individuals and corporations, a regulatory rollback and significant infrastructure spending, among others.

Yet the mainstream media and even some respected economists say the plan has no chance of working and further, that it would explode federal budget deficits. As always, it depends on how the policies are implemented and how they’re paid for. Let’s get started.

President Trump’s Economic Plan to Reach 3-4% GDP Growth

I get the impression that many (if not most) Americans don’t understand what Donald Trump’s economic plan is. That’s understandable since Mr. Trump said many different things about his economic plan during the campaign.

The questions that we as investors need to answer are three-fold: 1) What is Trump’s economic plan; 2) Can it get us to 3-4% GDP growth; and 3) Will Congress cooperate and pass the laws (tax cuts, etc.) needed to implement the plan? I’ll try to sort it out for you today.

I think the clearest summary of Trump’s economic vision surfaced last September in a research report written by Wilbur Ross, Trump’s choice for Commerce Secretary, and Trade Advisor Peter Navarro. The report is titled “Scoring the Trump Economic Plan: Trade, Regulatory and Energy Policy Impacts.” Here are the highlights, beginning with the opening presuppositions.

– The “New Normal” is a Political Excuse for Weak Growth. A gaggle of well-known economists seem to have settled on the term ‘New Normal’ to describe the lackluster growth in the US economy over the last decade or so.

From 1947 to 2001, the nominal US GDP (not adjusted for inflation) grew at an annual rate of 3.5%. But from 2002 to today, that average has fallen to just 1.9%. This loss of 1.6 percentage points in real GDP growth represents a 45% reduction in the US growth rate from its historic pre-2002 norm.

The question is, why did the US growth rate fall so dramatically? Many economists blame the plunge in large part on demographic shifts, such as the declining labor-force participation rate, the movement of Baby Boomers into retirement and the decline in worker productivity.

These so-called experts tell us these trends are likely irreversible, and that we are doomed to such sluggish economic growth indefinitely, if not permanently. That’s a defeatist view, and I beg to differ! There is nothing inevitable about overregulation, higher tax burdens, anti-small business policies and poorly negotiated trade deals.

With the exception of our aging population, these are problems that can be reversed, in my opinion. For the most part, this is a politically-made malaise, and therefore, very little about the New Normal has to be permanent.

– Reduce Regulation, Lower Taxes & Encourage Trade – in That Order. Bad policies push capital investment offshore and discourage onshore investment. This so-called “offshoring drag” subtracts directly from GDP growth. Each additional point in real GDP growth translates into roughly 1.2 million jobs per year. When the US economy grows at a rate of only 1.9% annually instead of its historic norm of 3.5%, we create almost two million fewer jobs a year.

– Excessive Regulation is Killing Business. More than 80% of CEOs of large US companies agree. They say US business regulations are among the worst in the developed world. The situation is even worse for America’s 28 million small businesses. They have provided two-thirds of our post-recession job growth, yet have been hurt even more. Small-business compliance costs are excessively high.

The Heritage Foundation and the National Association of Manufacturers (NAM) have estimated regulatory costs to be in the range of $2 trillion annually – about 10% of our GDP. NAM finds that “small manufacturers face more than three times the burden of the average US business.”

In just eight years, the Obama Administration added regulations – environmental, labor, banking and consumer protection – that added $120 billion in annual compliance costs. Those costs, like all business costs, are passed along to consumers, who must pay more for products and services.

Manufacturing Has the Best Job-Multiplier & Income Effect

The Trump regulatory reform plan will disproportionately, and quite intentionally, help the manufacturing sector the most. This is the economy’s most powerful sector for driving both economic growth and income gains. These income gains will, in turn, inordinately benefit the nation’s middle-class workforce.

This high-multiplier effect is precisely why the Trump trade doctrine and overall economic plan seek to strengthen the US manufacturing base – and regulatory reform is a key structural reform. Here’s how.

According to a 2014 study by NAM, US manufacturers pay $19,564 per employee on average annually just to comply with federal regulations, or nearly double the $9,991 per employee in regulatory costs borne by all firms in the US as a whole. That figure alone is staggering.

Since the era of globalization, manufacturing as a percentage of the labor force in the US has steadily fallen from a peak of 22% in 1977 to about 8% today. I don’t think most Americans, and certainly not most politicians, realize that our manufacturing sector has shrunk to close to one-third of what it was 40 years ago.

To those who would blame automation (robots, etc.) for the decline in manufacturing, one need only look at two of the most technologically advanced economies in the world: Germany and Japan. Both are world leaders in robotics. Despite declines in recent years, almost 20% of Germany’s workforce is still employed in manufacturing, and almost 17% of Japan’s workers.

The point is, we are not permanently resigned to the New Normal of 2% annual GDP growth or less. President John Kennedy proved it; President Ronald Reagan proved it; and maybe just maybe, President Trump can prove it as well – if he can get his pro-growth policies passed.

Economic Policies Similar to Trump’s Have Worked Before

CNBC’s economic analyst Larry Kudlow is one of my favorite commentators. Below is my summary of his latest views on Trump’s economic policies that appeared last Friday in National Review.

Virtually the whole world is beating up on the Trump administration for daring to predict that lower income tax rates, regulatory rollbacks, infrastructure spending and the repeal and replacement of Obamacare will generate 3-4% economic growth in the years ahead.

The critics say Trump’s policies, if enacted, will balloon the federal budget deficits. Yet in a CNBC interview last week, Treasury Secretary Steven Mnuchin doubled-down on this optimistic economic forecast. He also argued for “dynamic budget scoring” from the CBO to illustrate how faster growth due to the Trump changes would not balloon the deficits.

The mainstream media launched similar criticisms of President Ronald Reagan when he was championing his large tax cuts in the early 1980s. Yet once Reagan’s tax cuts were enacted, the economy soared and federal tax receipts increased significantly. That could happen again.

Trump’s Economic Plan vs Obama’s & the Media’s Reaction

What’s so interesting about all the economic growth naysaying today is that President Obama’s first budget forecast roughly eight years ago was much rosier than Trump’s. And there was hardly a peep of criticism from the mainstream media outlets and the consensus of economists.

As a reminder, Obama’s budget plan predicted real economic growth of roughly 3% in 2010, near 4% in 2011 and over 4% in 2012 and 2013. I don’t have to remind you, but it turned out that actual growth ran below 2% during this period.

Was there any howling by the mainstream media and liberal economists about this disappointing result back then? Of course not. It seems they saved all their grumbling for the Trump forecasts of 3-4% growth in recent months.

What’s really interesting is that the Obama policy didn’t include a single economic growth incentive. Not one. Instead, there was a massive $850 billion so-called spending “stimulus” and a bunch of “shovel-ready” public-works programs, most of which never got off the ground.

And finally there was Obamacare, which really was one giant tax increase. Remember when Supreme Court Chief Justice John Roberts ruled that the healthcare mandate was in fact a tax? But it wasn’t just a tax. It was a tax hike.

On top of that, there was the 3.8% “investment tax” hike, the tax increase on so-called “Cadillac” insurance plans and yet another tax increase on medical equipment. So eight years ago, a tax-and-spend plan from Obama was perfectly okay.

Moreover, the projection that Obama’s plan would produce a 4% economic growth rate was welcomed by the same economists and the media. Make sense? No, it does not.

So here’s President Trump reaching back through history for a common-sense growth policy that worked in the 1960s, when JFK slashed marginal tax rates on individuals and corporations. It worked again in the 1980s, when Ronald Reagan slashed tax rates across-the-board and sparked a two-decade boom of roughly 4% real annual growth.

Yet the mainstream media don’t buy Trump’s economic and tax plans. One after another, Trump critics argue that because we’ve had sub-2% growth over the past 10 years or so – the so-called New Normal – we are doomed to continue that forever. This is nonsense.

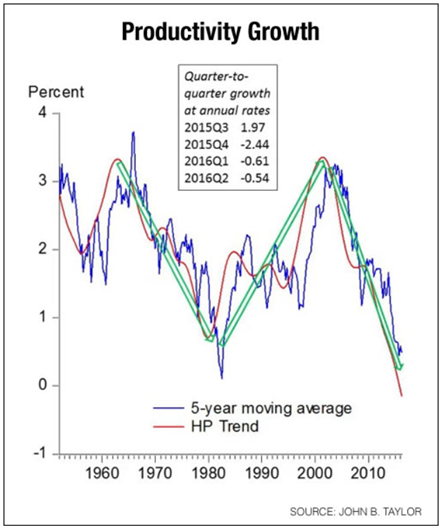

Productivity Can Rebound if Policy Environment is Right

Most of the Trump critics point to the decline in worker productivity over the past 15 years. They say, unless productivity jumps to 2.5% or so annually, and unless labor-force participation rises, we can’t possibly have 3-4% economic growth.

So Kudlow offers the chart below from Stanford University economics professor John Taylor, who’s also a research fellow at the Hoover Institution. Taylor, one of the nation’s top academic economists, shows that productivity declines can be followed by productivity increases over long periods of time.

Taylor notes that bad economic policy leads to slumping productivity, living standards, real wages and growth. Taylor notes that, “Huge swings in productivity growth in recent years, are closely related to shifts in economic policy, and economic theory indicates that the relationship is causal.”

He adds: “To turn the economy around we need to take the muzzle off, and that means regulatory reform, tax reform, budget reform, and monetary reform.”

Kudlow concludes: “Get rid of the state-sponsored barriers to growth. Then watch how these [Trump] common-sense incentive-minded policies turn rosy scenario into economic reality.

It remains to be seen how all this will turn out. I’ll keep you posted.

All the best,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management

© Halbert Wealth Management

Read more commentaries by Halbert Wealth Management